Decarbonizing in a downturn: Can the mining & metals sector afford (not) to change?

Softening commodity prices and economic headwinds may deter miners and metal companies from deploying the significant capital expenditure required to decarbonize.

Russia's actions in Ukraine fueled an unprecedented rally in mineral and metal prices earlier this year, with multiple metals breaking historical records. However, this rally was short-lived. Within six months, metal prices collapsed back to 2020 levels in the most volatile first half of the year. There are myriad factors that are lining up to cap mineral and metal prices in the coming months, the most significant of which, we believe, is the rapid deterioration of the global economy.

In recent times, the mineral commodities cycle has been out of synchronization with the global macro-economic cycle—this time the cycles appear to be converging. With the prospect of global downturn looming, we ask the question, "Is the mining & metals sector prepared?" Is the sector truly resilient to disruption in supply chain, inflationary pressures, headwinds on demand, increased funding costs and of course, the drive to net-zero? Or will China's fiscal and monetary policies and the latest legislative developments in US and EU regulation provide enough support to the sector so that miners and the rest of the supply chain can capably respond to market conditions? Can the ESG agenda and decarbonization projects contribute to the long-term sustainability of the sector itself?

We are thinking critically about what a downturn means and whether this could, in fact, be a major opportunity to distinguish the sector from its traditionally dominant counterpart, the oil & gas sector. We hope you find Mining & Metals 2022: Putting the Resilience Rhetoric to the Test a stimulating read.

The mineral commodities cycle, in recent times, has been out of synch with the global macro-economic cycle—this time the cycles appear to be converging

Softening commodity prices and economic headwinds may deter miners and metal companies from deploying the significant capital expenditure required to decarbonize.

A steady supply of minerals critical to the energy transition must be ensured through the expected recession.

Mining & metals companies have been increasingly focusing on enhancing their environmental, social and governance credentials in recent years as part of the energy transition. But with a global recession looming, will they be able to maintain their commitment?

China is looking beyond its borders to maximize the returns from the minerals needed to make the energy transition happen.

Participants in the mining & metals supply chain will see many challenges—but also opportunities—in playing both offense and defense in an economic downturn.

Mining & metals companies can take advantage of low prices in the leveraged finance markets to manage their liabilities amid the expected recession.

Financial crime flourishes in a downturn, and the mining & metals sector is not immune to it. The sector faces a number of industry-specific risks, and will need to react to the ensuing likely surge in enforcement activity.

Softening commodity prices and economic headwinds may deter miners and metal companies from deploying the significant capital expenditure required to decarbonize.

Every company and every industry will be transformed by

the transition to a net-zero world. The question is, will you lead, or will you be led?

Larry Fink

CEO, BlackRock

Achieving a mining & metals sector with net-zero carbon emissions will require a transformation to the ways that minerals are extracted, processed, refined, brought to market and incorporated into the global supply chain. This transformation will require clean technology to be integrated into new mines, metal refineries and related transport infrastructure, as well as into existing projects, particularly when a long mine life remains.

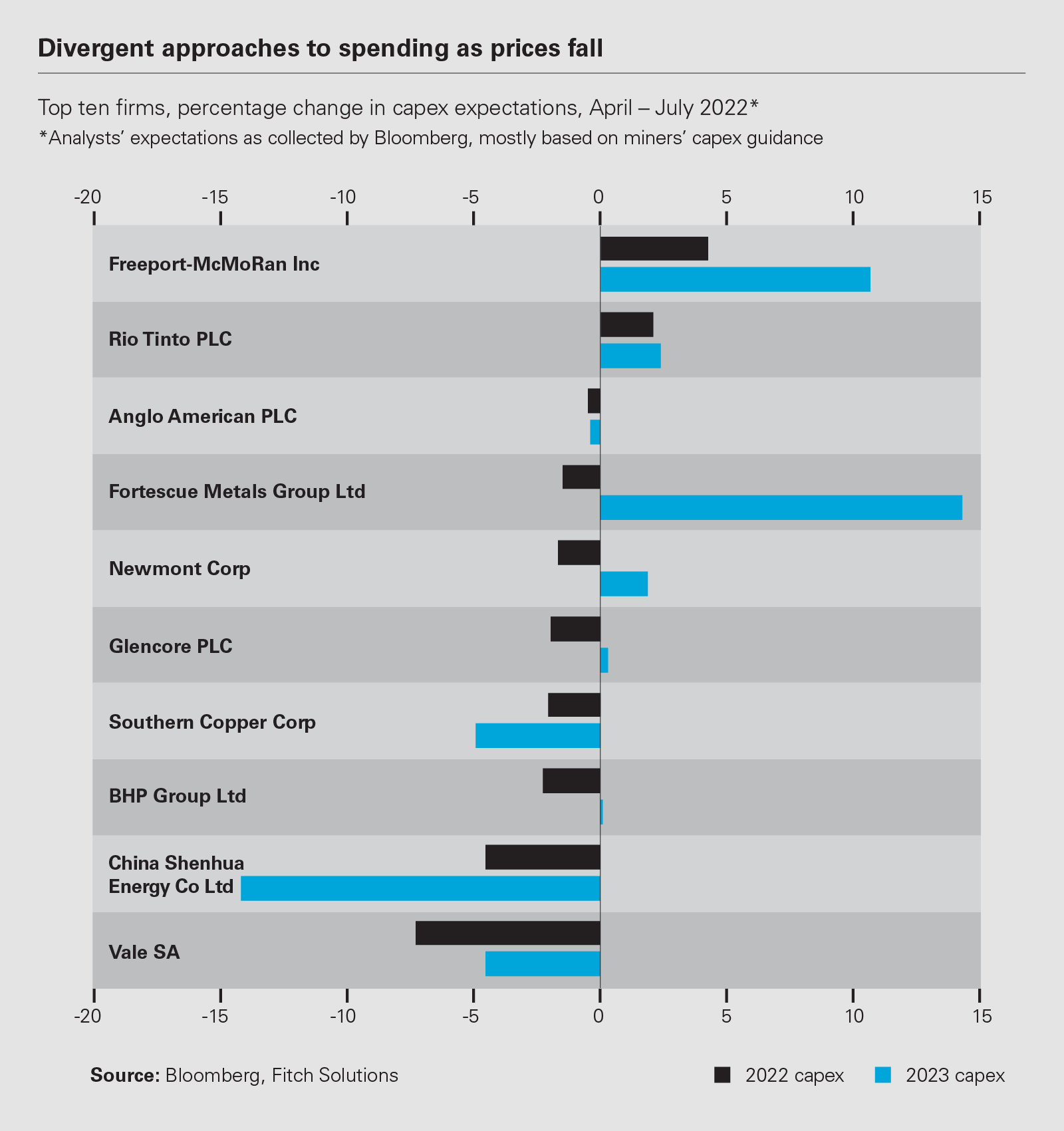

While the capital costs of clean technology are dropping, the upfront capital costs of green technologies remain invariably higher than the costs of their conventional counterparts. Developing major capital projects is challenging in the best of markets, and analysts expect that most of the major mining firms will reduce their capital expenditure in the coming year as commodity prices soften and economic headwinds blow.

While deferring major capital projects may help mining & metal companies conserve cash and minimize debt as the sector enters less favorable market conditions, deferring the capital projects necessary to decarbonize risks creating future issues and missed opportunities for slow movers in the sector.

Early movers, on the other hand, are likely to have advantages in solidifying their positions as market leaders in a new net-zero mining & metals sector. As BlackRock CEO Larry Fink wrote in his 2022 annual letter to CEOs: "Every company and every industry will be transformed by the transition to a net-zero world. The question is, will you lead, or will you be led?"

The wall of regulation for a low-carbon economy is coming, currently led by Europe, and this momentum is unlikely to be dissipated by a downturn in the sector. On the other side of the downturn, mining & metals companies that defer the decarbonization of their operations will find themselves lagging as decarbonization targets and requirements tighten.

For those with the vision to push forward with the transformation now, there are a number of dedicated sources of capital available to support projects with strong ESG credentials, as well as other options for companies to strengthen their capital structure to enable strategic projects to proceed.

While not without risk, there is potential in a number of areas for mining & metals companies to allocate their capital and push forward with capital projects to decarbonize the sector. Even if there is a downturn, these projects are likely to play out well in the long, and in some cases even the nearer term, for those companies with the vision and capacity to move now.

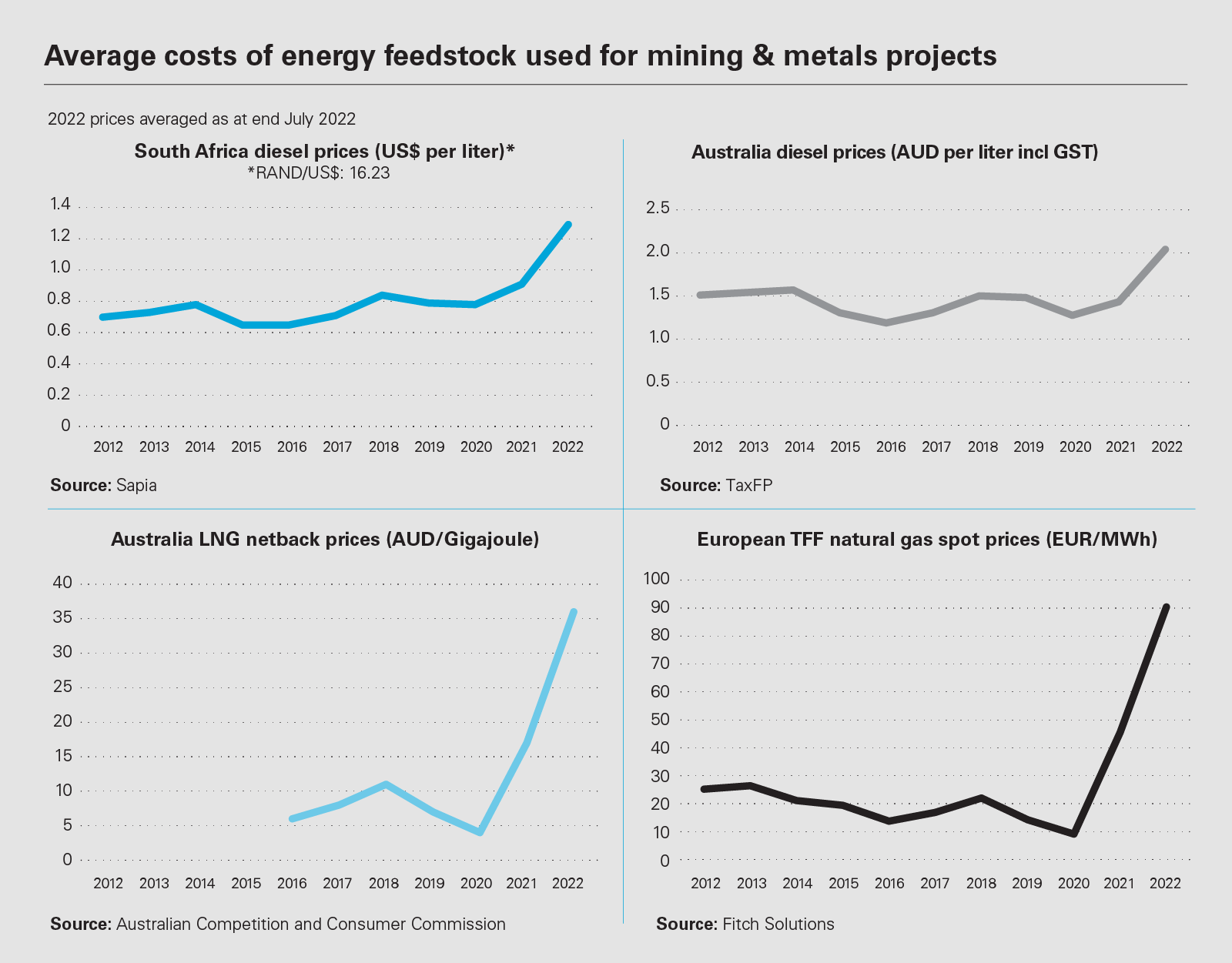

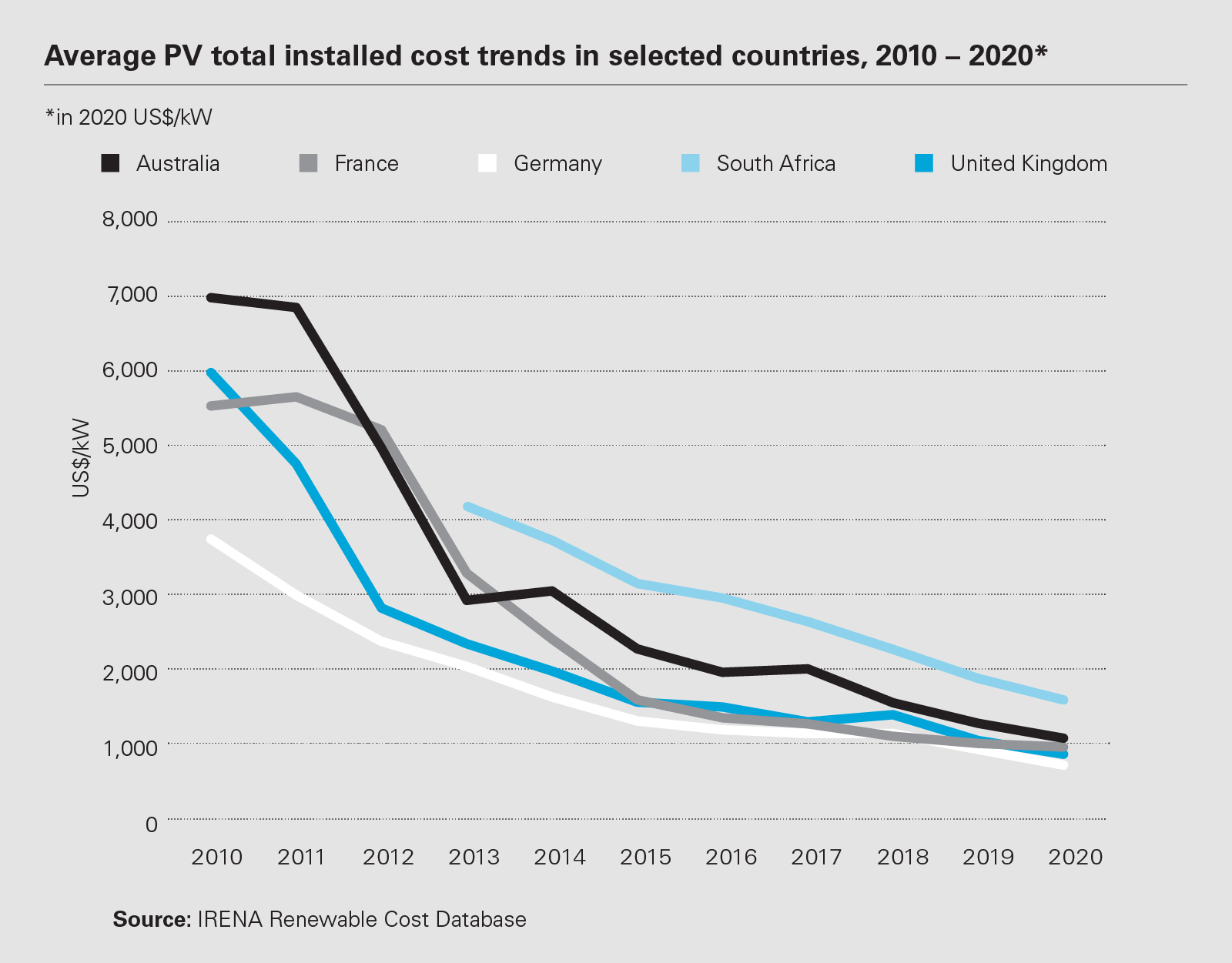

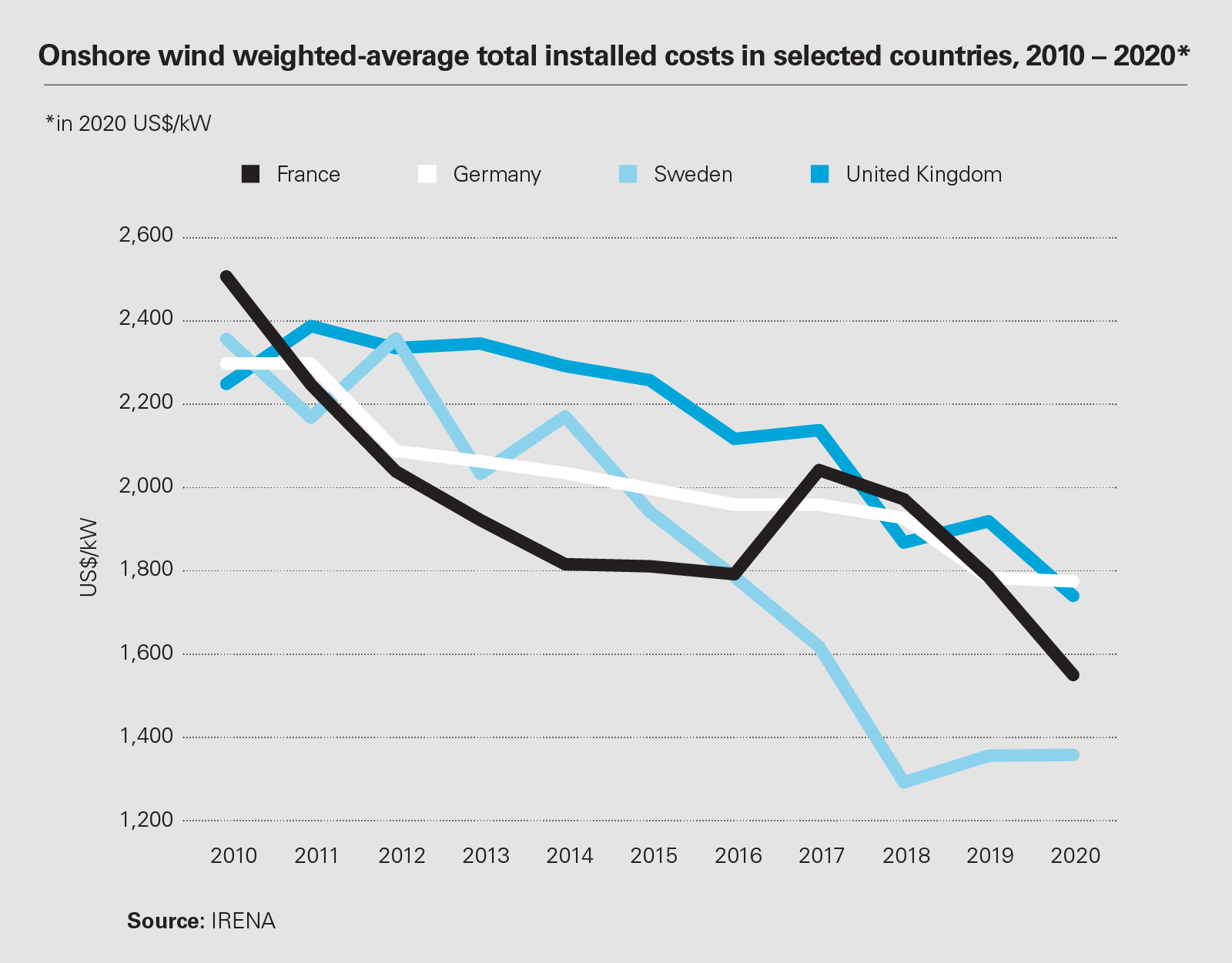

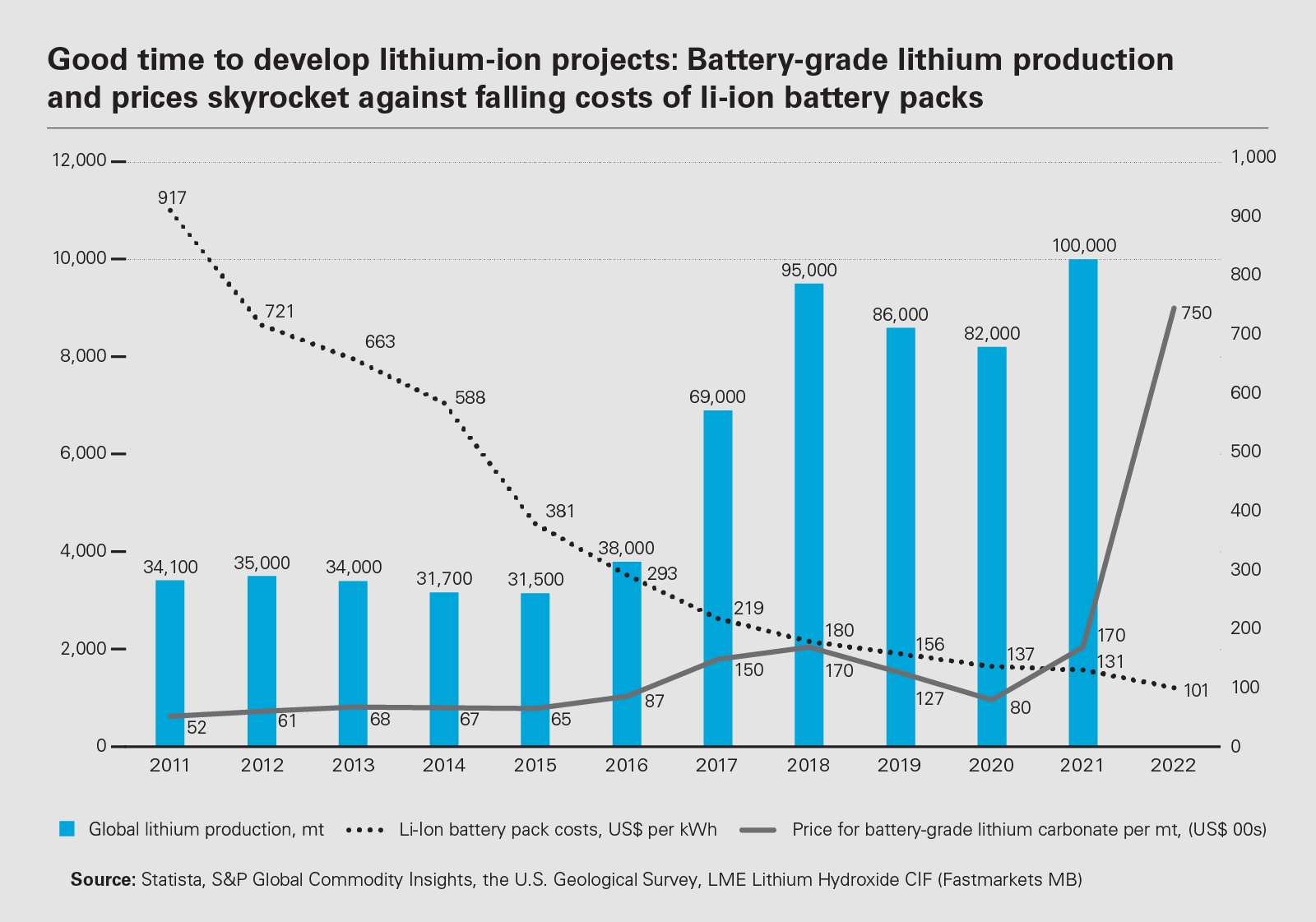

The last decade has seen solar PV, onshore wind and lithium-ion battery storage systems move from being high-cost and novel technologies to being established technologies with substantially reduced capital costs. Over the same period, prices for diesel and gas, the traditional sources of energy for mining & metals projects, have been at times volatile. The most recent spike in global oil & gas prices is the latest shock in a long history of unpredictable fossil fuel prices.

$70,000

Lithium carbonate prices have risen from $5,000 per ton in July 2020 to about $70,000 per ton in July 2022

Source: Market data

Advances in lithium-ion battery storage technology and dramatic drops in the capital costs of installing solar PV, have made 100 percent-green renewable energy captive power solutions a real possibility for miners in locations with good sunlight hours and irradiation. While upgrading or replacing existing power solutions may not be top of the agenda for mining & metals companies heading into a downturn, there are advantages for those who do.

As well as dramatically reducing a mining site's scope 1 and 2 emissions, a captive renewable power solution utilizing sunshine reduces and stabilizes a project's operational expenditure, by cutting diesel and natural gas consumption, and reducing the exposure to fluctuations in global oil & gas prices.

The reliability of grid power and transport of fuel feedstock are major issues for many miners, particularly in remote locations and developing countries. A captive renewable power solution with energy storage overcomes both these issues. Depending on local regulatory and grid connection requirements, captive power systems may even be able to generate additional revenues for projects by selling surplus power back to the public electricity grid.

Currently, the number and capacity of reputable manufacturers and suppliers of solar, wind and energy storage equipment are limited, and these companies are already experiencing unprecedented demand for their products. Early movers will be able to take advantage of current capital costs to install, which despite global demand are near historic lows, and will have lead-time advantages and will entrench relationships with suppliers.

On the other hand, late comers may in the future struggle or pay higher prices to execute capital projects necessary to decarbonize their power solutions. This could especially be the case if future regulatory changes cause a huge rush in orders, or the availability of lithium and other key metals necessary for a transition to a low-carbon economy do not keep pace with rising demand, particularly with the rise of EVs and green hydrogen projects.

Electrifying processes onsite and moving to renewable power sources are just one way for the mining & metals sector to reduce its scope 1 and 2 emissions. More challenging aspects of the emissions created by mining & metals projects and their supply chain await technologically proven and commercially available solutions to enable the sector to fully decarbonize. For instance, heavy haulage onsite trucks and the seaborne transport of bulk commodities currently remain very much fossil fuel-dependent.

To tackle these problems, some mining & metal companies are becoming more involved in their supply chains, supporting research and development, and making more venture capital-style investments to try and find ways to transition the sector to net-zero.

For example, Fortescue Metals Group recently announced a partnership with German-Swiss equipment manufacturer Liebherr for the development and supply of green mining haul trucks, which will integrate zero-emission power system technologies currently being developed by Fortescue Future Industries and Williams Advanced Engineering.

As your industry gets transformed by the energy transition, will you go the way of the dodo, or will you be a phoenix?

Larry Fink

CEO, BlackRock

The best timing and value of any R&D or venture capital-style investment is inherently uncertain, and companies may be hesitant to make such investments in the face of an impending downturn. However, for those that persevere with these investments during the downturn, there could be significant advantages, as the sector emerges from the downturn and regulations tighten around carbon emissions and supply chain transparency.

Intellectual property for green technology could be vested in or controlled by miners who are early movers and invest in or collaborate with R&D in this space. This IP could be used by early movers as a competitive advantage in a tightening regulatory environment, or as an additional source of revenue if they choose to sell or license the technology for use in the wider sector.

Those companies that find a solution to the carbon emissions caused by the seaborne transport of bulk commodities will help mining & metals companies navigate incoming regulations such as the EU Due Diligence Directive and the EU Carbon Border Adjustment Mechanism, and help future-proof their access to markets that penalize carbon-intensive imports.

The Cargo Owners for Zero Emissions Vessels (coZEV) is a recently established initiative designed to enable major seaborne freight customers to come together to accelerate the decarbonization of marine shipping. To date, a number of major sea freight customers including Amazon and Ikea have signed up to the initiative, but no mining or metal companies have yet added their names.

As a general market downturn and rising interest rates compound general disruption and cash flow issues in the global supply chain, mining & metal companies with resilient balance sheets and capital structures may find there are strategic M&A opportunities to acquire impacted suppliers, allowing major mining & metal companies to vertically re-integrate their supply chains. Greater vertical integration will help companies buffer supply chain disruptions and make these companies well placed in a post-downturn market with greater regulatory requirements around transparency on supply chain and carbon emissions.

The push to decarbonize the mining & metals sector and other heavy industries has also opened the door for the creation of new products and markets, with green hydrogen, green ammonia and green metals projects all emerging.

In particular, over the past two years, green hydrogen has been pushed as a potentially transformational fuel to power heavy industry in a green and sustainable way, including in the mining & metals sector. There is also continued heavy interest in the development of green hydrogen projects as well as an emerging range of global policy and regulatory initiatives to support these projects.

Fortescue Metals Group, through its subsidiary Fortescue Future Industries, is so far the biggest player in the sector to move into the green hydrogen space, exploring potential projects in its home market of Australia, as well as abroad, including recently in Djibouti.

The emergence of green steel is also an age-defining development in the decarbonization of the metals sector, and existing and new players will invariably fill this market as it develops. Reducing the sector's emissions by expanding the extraction and recycling of metals from waste is an area that will grow and offer new opportunities for sector participants, as reflected by Glencore's announcement earlier this year that it was partnering with a major recycler in the lithium-ion battery recycling sector.

The capital costs of developing green hydrogen, green ammonia and green metals projects are considerable. While these new products present great promise for a low-carbon mining & metals sector and wider economy, the market is still very much in its infancy, which may make mining & metals companies reluctant at the current time to commit to the considerable capital expenditure required to construct these projects and bring these products to market.

A wider global downturn may also depress the value that the market is willing and able to pay for green hydrogen, green ammonia and green metal products, challenging the economic viability and bankability of these projects. However, despite the current economic headwinds, some companies are pushing forward with capital investments in projects to deliver these new products, and may ultimately be vindicated for a range of reasons.

Hydrogen plants, ammonia refineries, steel mills, alumina refineries and even major recycling facilities all have multi-year design and construction phases, meaning that projects cannot be brought to market swiftly to react to changing consumer demands. If existing customers of hydrogen, steel and alumina are prepared to pay a price premium for a recognized "green" version of these products, then early movers in the construction of these plants will have a captive market, at least for an initial period.

A shortage in raw materials necessary to manufacture energy storage systems and electrolysers necessary for green hydrogen projects could hit and delay players who defer capital investment in these projects until the downturn has passed.

Fast-moving startup companies, such as H2 Steel in the green steel sector, may emerge as major players in these new markets. Transitions in other markets, such as the shift in the motor industry to electric vehicles, has shown that early movers and startups, such as Tesla, can capture market share from incumbent majors if those incumbents are slow to transition.

Whether developing and constructing major green hydrogen or green metals plants, or upgrading and retrofitting equipment and power sources at existing mining projects, the capital expenditure required to decarbonize the mining & metals sector will undoubtedly be significant, and there will be those that in a downward market either hold back, or for various reasons are simply unable to press ahead with, the necessary capital projects.

For companies that do move forward, these works should not be viewed simply as a cost, but also as an opportunity to gain both short and medium-term competitive advantages in the market, and ultimately as an investment to secure a place in the new low-carbon economy that is expected to span all industries and sectors.

As mining & metals companies grapple with difficult capital expenditure budgets and allocations for the coming years, they would do well to consider another question posed by Fink in his 2022 letter: "How are you preparing for and participating in the net-zero transition? As your industry gets transformed by the energy transition, will you go the way of the dodo, or will you be a phoenix?"

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP

View image: Divergent approaches to spending as prices fall (PDF)

View image: Divergent approaches to spending as prices fall (PDF)

View full image: Average costs of energy feedstock used for mining & metals projects (PDF)

View full image: Average costs of energy feedstock used for mining & metals projects (PDF)

View image: Average PV total installed cost trends in selected countries, 2010 – 2020* (PDF)

View image: Average PV total installed cost trends in selected countries, 2010 – 2020* (PDF)

View image: Onshore wind weighted-average total installed costs in selected countries, 2010 – 2020* (PDF)

View image: Onshore wind weighted-average total installed costs in selected countries, 2010 – 2020* (PDF)

View image: Good time to develop lithium-ion projects: Battery-grade lithium production and prices skyrocket against falling costs of li-ion battery packs (PDF)

View image: Good time to develop lithium-ion projects: Battery-grade lithium production and prices skyrocket against falling costs of li-ion battery packs (PDF)