US M&A settles back down

Deal value in the first half of 2022 could not match the record-breaking level of activity in 2021

US M&A deal levels remain robust, despite dropping from historic highs set in 2021

US M&A activity eased off in the first half of 2022 following an annus mirabilis for US M&A in 2021. Total value slipped to US$995.3 billion, a 29 percent year-on-year fall, though this is consistent with dollar volumes seen before the pandemic and so remains healthy by historic standards. Deal volume also fell, by 21 percent to 3,818 transactions. While this also remains above average, there was a material softening in the frequency of deals moving through Q2, which saw a quarter-on-quarter drop of 22 percent to levels last seen in Q1 2020, when the market was just beginning to recover from the initial shock of the pandemic.

A lot has happened this year to test acquirers’ nerves. Inflation concerns had already begun to set in before the war in Ukraine started. The conflict catalyzed further unease in capital markets as well as exacerbated supply chain troubles which have, in part, contributed to inflationary pressures. The S&P 500 officially entered a bear market in mid-June, and the Federal Reserve has embarked on a monetary tightening program to bring prices under control, leading to an increase in financing costs.

Regulations are another consideration. The SEC has taken the SPAC market to task, proposing accountability for deal parties and intermediaries for inflated projections. This type of transaction ground to a standstill in Q2 this year, as participants digested their risk exposure and the implications of the regulator’s proposals weighing on overall M&A volume. More recently we have seen some truly innovative SPAC structures that have the potential to re-stimulate interest in these deals.

For the most part, the US M&A market has stood up impressively to everything that has been thrown at it, which alone is solid grounds for optimism. Despite technology stocks being sold off heavily in equity markets, the sector has once again outperformed on the M&A front as companies and PE sponsors, who remain heavily armed with dry powder in spite of the more challenging deal financing conditions, continue to be attracted to innovation.

The fall in price-to-earnings ratios in the public markets and EBITDA multiples in private markets mean that, all else being equal, acquisitions are more attractive today than they were a year ago. Naturally, investors remain cautious as they closely watch how inflation plays out, the Fed response and the impact of those actions on underlying economic growth. However, the second half of 2022 has the potential to reclaim some of the confidence lost in recent months.

Deal value in the first half of 2022 could not match the record-breaking level of activity in 2021

Despite facing economic and regulatory hurdles in H1, PE dealmaking remains resilient, and looks set to reach its second-highest value on record

After a series of rollercoaster years for the SPAC market, investors and sponsors are finding ways to improve deal integrity

Despite facing economic and regulatory hurdles in H1, PE dealmaking remains resilient, and looks set to reach its second-highest value on record

Explore the data

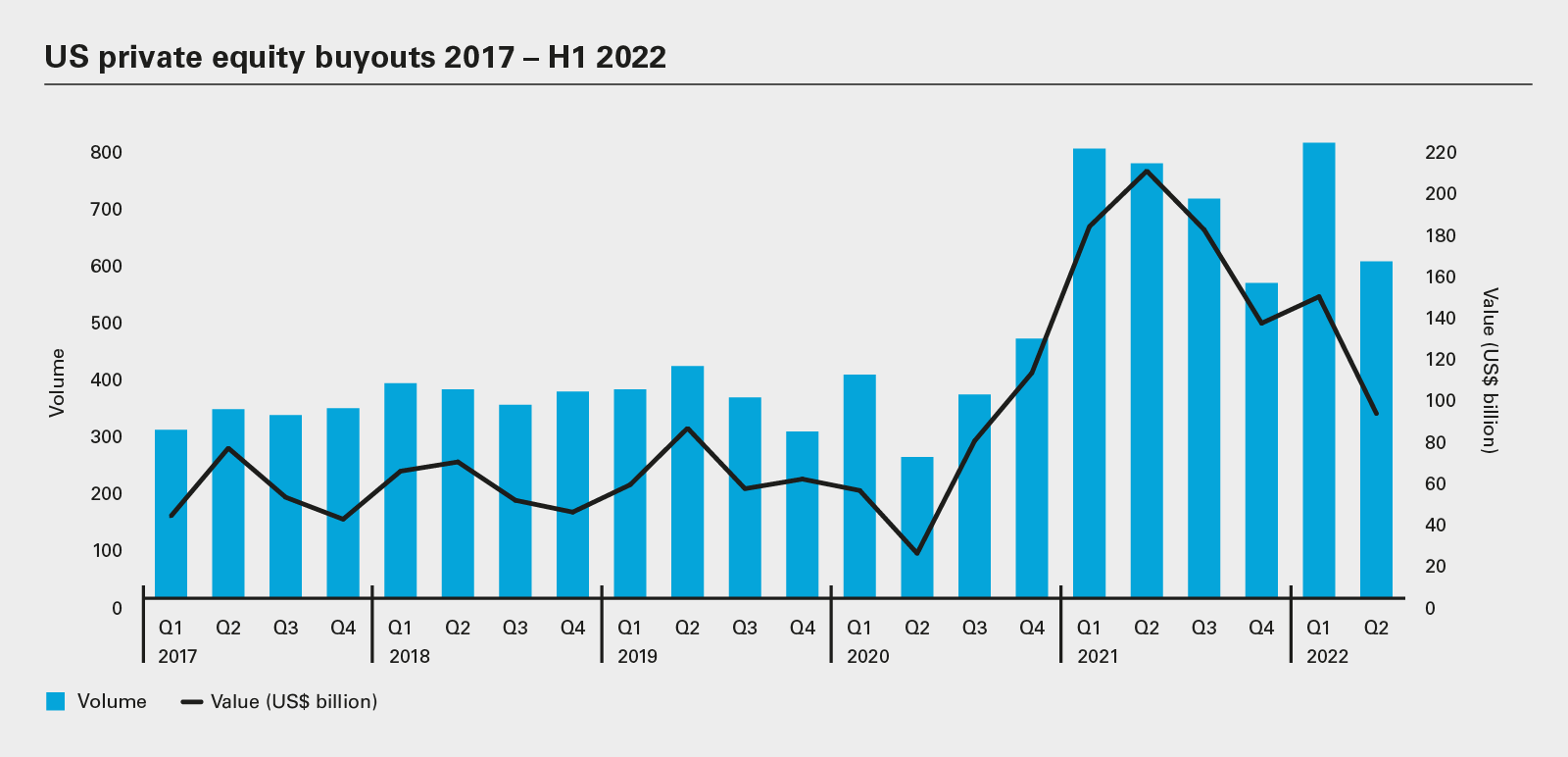

In line with overall M&A activity, US PE dealmaking in H1 lagged behind 2021 in terms of both value and volume. Total deal value of US$415 billion during the first half of the year represents a 28 percent fall year-on-year—yet this level of activity looks on track to reach the second-highest annual deal value in Mergermarket’s history (since 2006), after the record-topping 2021.

A deal volume of 1,727, while 20 percent below the 2021 total, is still firmly ahead of pre-2020 activity levels. This resilience proves that a new level of US PE dealmaking is being set in the post-pandemic era.s

US$415

billion

The value of US PE-related deals in H1 2022

727

The number of PE buyouts in the TMT sector in H1 2022 - a 17% increase versus H1 2021

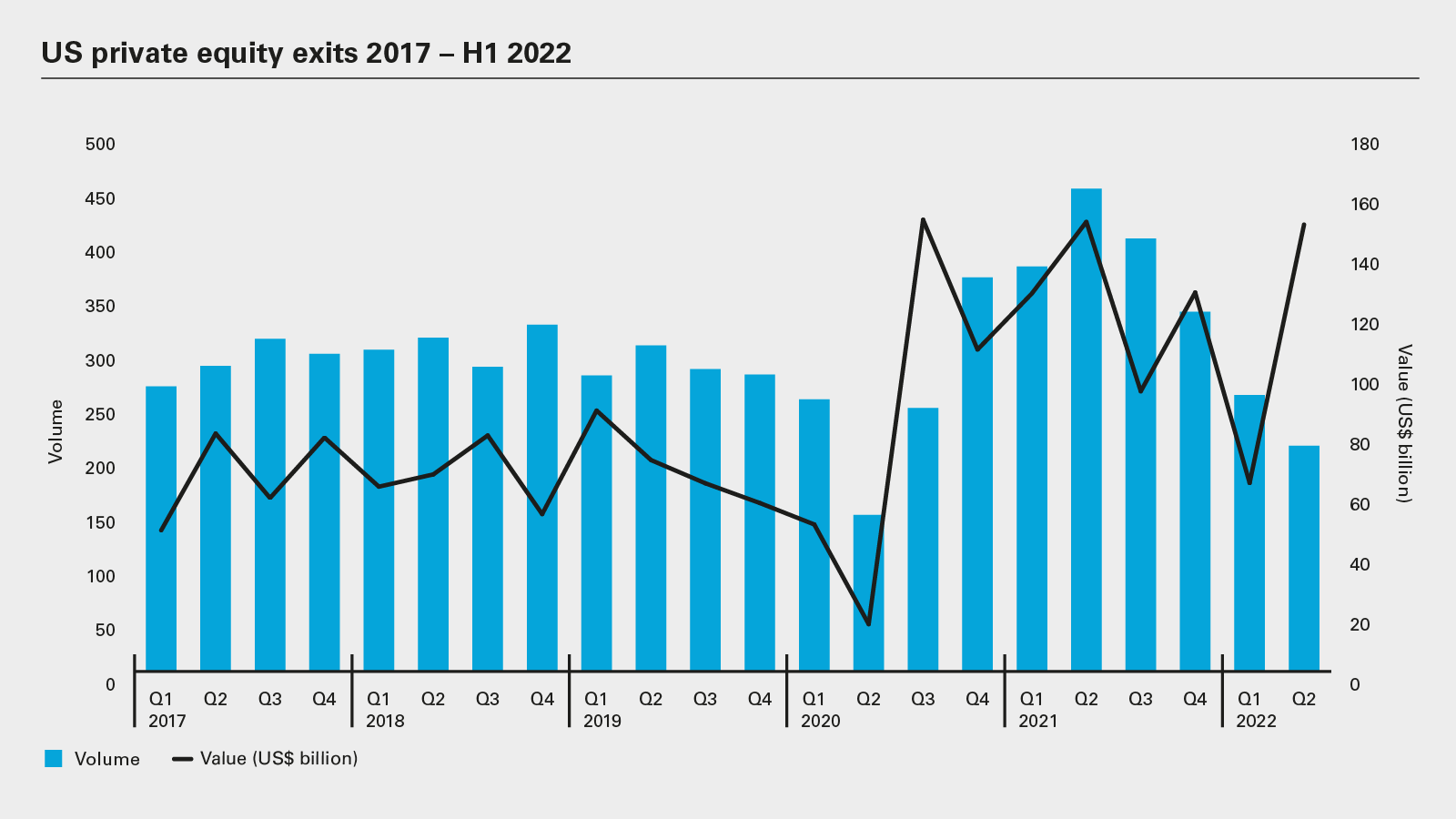

PE firms have managed to achieve this level of activity despite more challenging macroeconomic conditions, with rising interest rates making it increasingly difficult to agree on valuations. Tighter monetary conditions also mean that GPs are finding financing more difficult for their buyouts. When facing economic headwinds, PE firms are also more likely to extend their investment periods, which may cause a slowdown in the exit market.

Yet, while an economic downturn is widely anticipated across the market, PE firms are well placed to take advantage of the investment opportunities these conditions present.

The TMT sector saw the greatest level of buyout activity in the first six months of this year, by both value and volume. The number of transactions increased by 17 percent year-on-year to 727 deals—making it one of the few sectors that experienced an annual increase in the number of buyout transactions this year.

Transaction value stayed steady from H1 2021 to the same period this year, coming to a total of US$133.1 billion, just under the previous year’s US$133.2 billion total.

The largest buyout announced was Vista Equity Partners’ US$16.6 billion purchase of Citrix Systems—a clear bet on a more permanent shift to hybrid working. Citrix’s software—which enables employees to work securely from their devices remotely—saw demand soar amid the pandemic.

In response to investor pressure and consumer demand, PE investors are increasingly shifting their attention to clean energy targets. In January, US PE giant Blackstone conducted a landmark transaction in the renewable power space, investing US$3 billion in solar and wind developer Invenergy Renewables. Blackstone has already committed nearly US$13 billion in investments consistent with the broader energy transition since 2019.

The rest of the market is following suit. According to data from S&P Global Market Intelligence, US and Canadian venture capital and private equity firms invested a record US$6.8 billion in 2021 in energy efficiency, storage and management, along with new technologies to reduce carbon emissions.

Although the private equity industry looks well positioned to take advantage of a more challenging economic climate, PE players are also bracing for higher levels of regulatory intervention.

Biden administration officials have been vocal about how greater scrutiny should be applied to the industry. The DOJ’s recently appointed head of antitrust, Jonathan Kanter, pledged to take a tougher stance on roll-up deals based on anti-competition concerns. Divestiture deals will also come under increased focus, if the sale is seen as making a company less competitive within its industry.

To gain a more accurate competitive picture of deals, the DOJ, along with the FTC, is in the process of increasing disclosure requirements on pre-merger notification forms, while conducting an overhaul of merger guidelines in order to clamp down on anti-competitive deals.

The SEC, meanwhile, has taken steps to increase its oversight of private financial markets, voting in favor of a string of proposed regulations in February. The proposed rules, which include banning certain fees that buyout firms charge and blocking preferential terms for certain investors, are said to be the biggest step that the SEC has taken to improve oversight in the market since the passing of the Dodd–Frank Act in 2010.

While these regulatory changes have yet to materially impact the PE industry, buyout firms will be keeping a close eye on developments. Regulatory compliance may become more burdensome but, with adequate preparation, should not deter sponsors from transacting.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP

View full image: US private equity buyouts 2017 – H1 2022 (PDF)

View full image: US private equity buyouts 2017 – H1 2022 (PDF)

View full image: US private equity exits 2017 – H1 2022 (PDF)

View full image: US private equity exits 2017 – H1 2022 (PDF)