US M&A settles back down

Deal value in the first half of 2022 could not match the record-breaking level of activity in 2021

US M&A deal levels remain robust, despite dropping from historic highs set in 2021

US M&A activity eased off in the first half of 2022 following an annus mirabilis for US M&A in 2021. Total value slipped to US$995.3 billion, a 29 percent year-on-year fall, though this is consistent with dollar volumes seen before the pandemic and so remains healthy by historic standards. Deal volume also fell, by 21 percent to 3,818 transactions. While this also remains above average, there was a material softening in the frequency of deals moving through Q2, which saw a quarter-on-quarter drop of 22 percent to levels last seen in Q1 2020, when the market was just beginning to recover from the initial shock of the pandemic.

A lot has happened this year to test acquirers’ nerves. Inflation concerns had already begun to set in before the war in Ukraine started. The conflict catalyzed further unease in capital markets as well as exacerbated supply chain troubles which have, in part, contributed to inflationary pressures. The S&P 500 officially entered a bear market in mid-June, and the Federal Reserve has embarked on a monetary tightening program to bring prices under control, leading to an increase in financing costs.

Regulations are another consideration. The SEC has taken the SPAC market to task, proposing accountability for deal parties and intermediaries for inflated projections. This type of transaction ground to a standstill in Q2 this year, as participants digested their risk exposure and the implications of the regulator’s proposals weighing on overall M&A volume. More recently we have seen some truly innovative SPAC structures that have the potential to re-stimulate interest in these deals.

For the most part, the US M&A market has stood up impressively to everything that has been thrown at it, which alone is solid grounds for optimism. Despite technology stocks being sold off heavily in equity markets, the sector has once again outperformed on the M&A front as companies and PE sponsors, who remain heavily armed with dry powder in spite of the more challenging deal financing conditions, continue to be attracted to innovation.

The fall in price-to-earnings ratios in the public markets and EBITDA multiples in private markets mean that, all else being equal, acquisitions are more attractive today than they were a year ago. Naturally, investors remain cautious as they closely watch how inflation plays out, the Fed response and the impact of those actions on underlying economic growth. However, the second half of 2022 has the potential to reclaim some of the confidence lost in recent months.

Deal value in the first half of 2022 could not match the record-breaking level of activity in 2021

Despite facing economic and regulatory hurdles in H1, PE dealmaking remains resilient, and looks set to reach its second-highest value on record

After a series of rollercoaster years for the SPAC market, investors and sponsors are finding ways to improve deal integrity

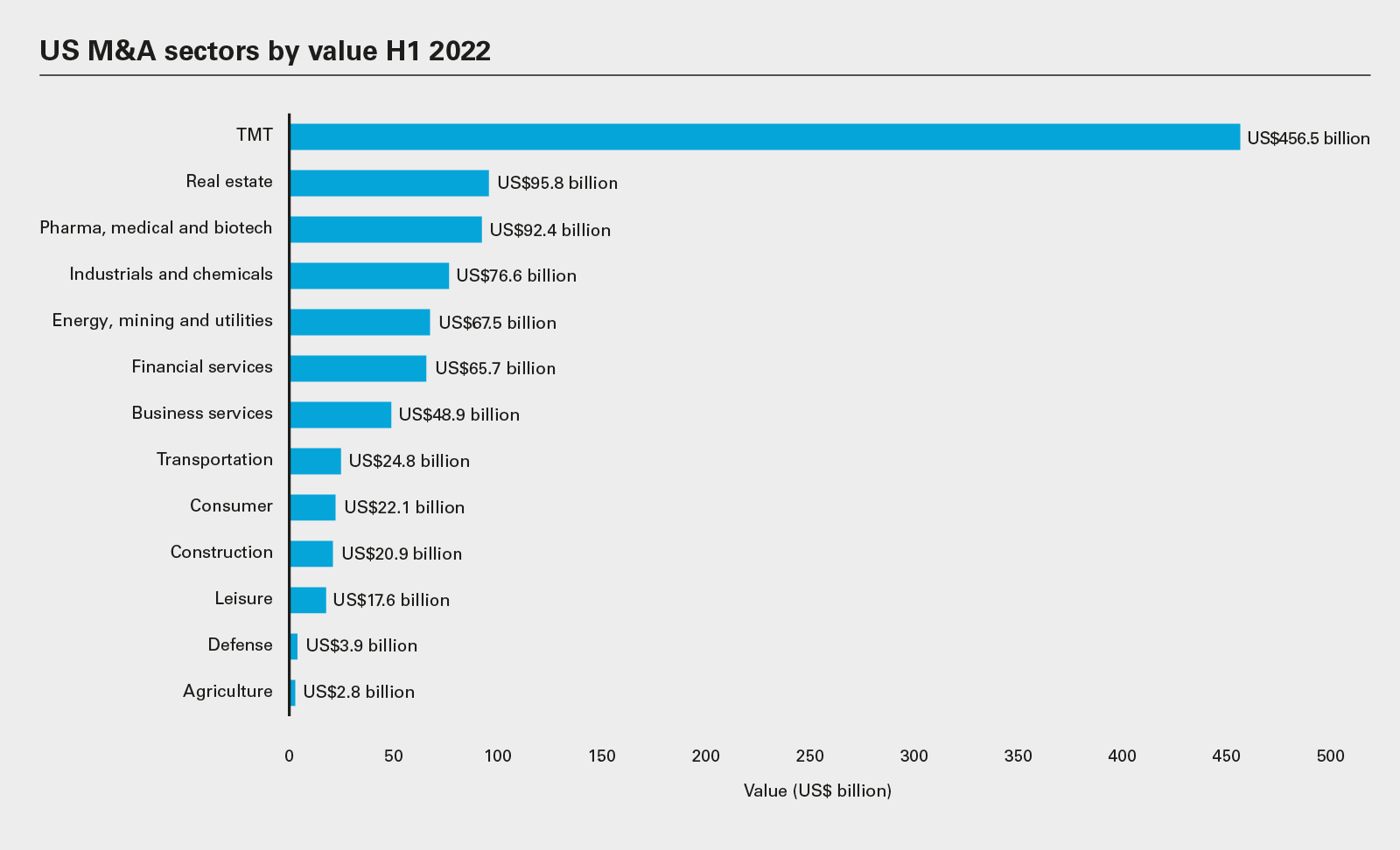

Boosted by a few record-setting tech deals at the top end of the market, TMT continues to dominate US M&A value

Explore the data

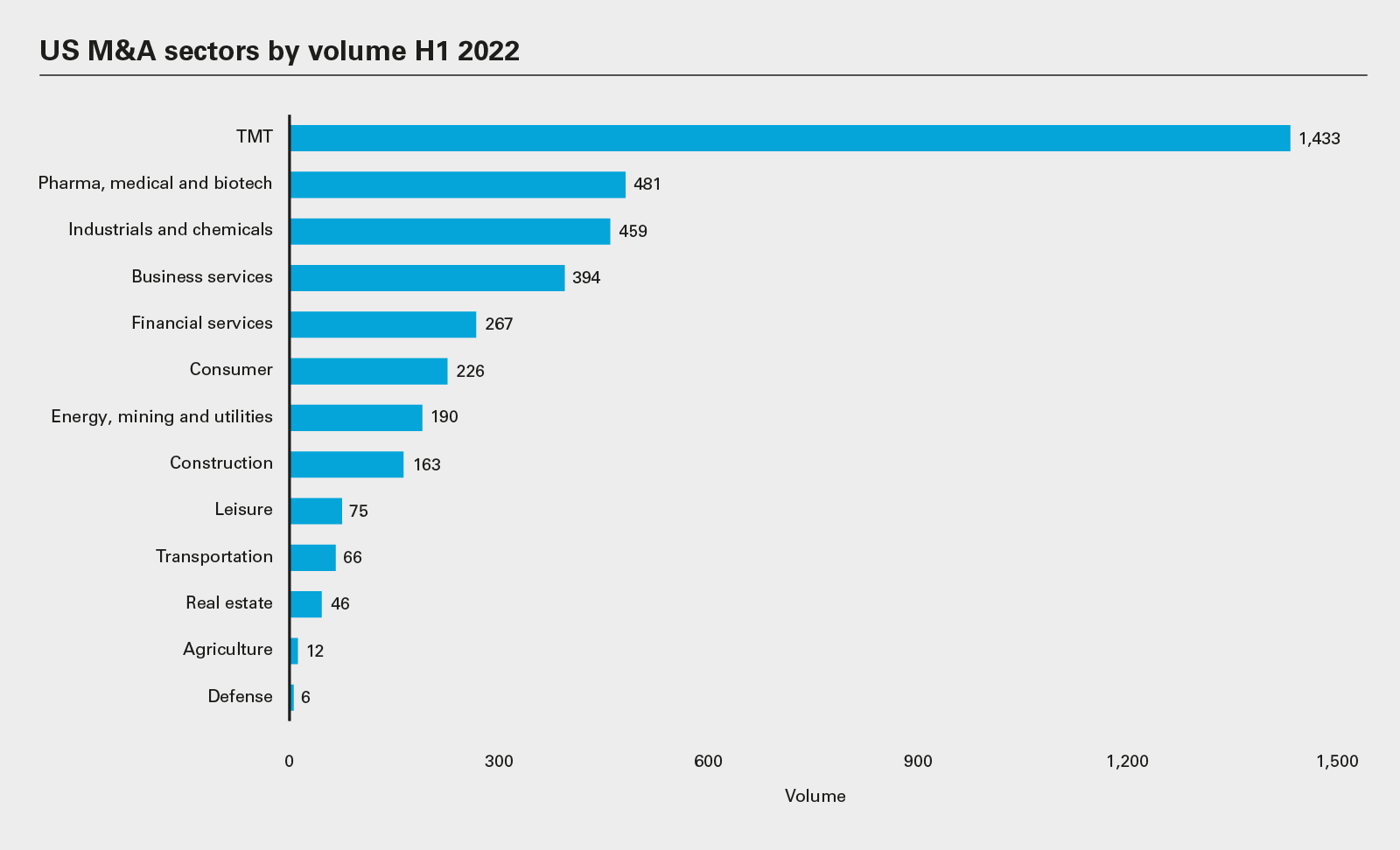

Technology, media and telecoms (TMT) continued its reign as the dominant sector for US M&A in the first half of 2022, despite a year-on-year collapse in the value of media and telecoms deals. Technology remains at the core of America’s innovation economy and it shows in the deal data. There were US$415.4 billion worth of tech transactions, up 5 percent on the first half of 2021. Media and telecoms acquisitions fell by 79 percent and 40 percent, respectively, to US$31.3 billion and US$9.8 billion. This is despite a much-discussed softening of technology stock prices in the public markets.

All of the top-three largest M&A transactions so far this year have been tech plays, led by Microsoft’s US$75.1 billion bid for gaming company Activision Blizzard. Second to this was chipmaker Broadcom’s US$71.6 billion offer for software business VMware, followed by Elon Musk’s since-rescinded US$41.3 billion Twitter overture.

Even discounting these three outsized acquisitions would put the technology sector in the lead by a factor of more than two. What’s more, technology delivered the most transactions by a vast margin. There were 1,299 tech M&A deals in H1 2022, down 4 percent year-on-year, nearly three times the second-highest volume sector, pharma, medical and biotech (PMB), which counted 481 deals, down 29 percent on the same period last year.

Real estate just beat PMB as measured in aggregate value, with a total of US$95.8 billion, a 109 percent annual gain. Nearly a third of this came from the US$27.9 billion all-stock acquisition of Duke Realty Corp. by Prologis, competing industrial real estate investment trusts specializing in warehouse logistics.

In many ways, the pandemic has left a lasting impression on M&A markets. Supply chains have been under immense pressure over the past two years, and best-in-class logistics services can help to relieve some of that burden by improving efficiencies and costs. In the case of PMB, which recorded US$92.4 billion, down 51 percent, Pfizer claimed the largest deal with its US$11.6 billion purchase of Biohaven Pharmaceutical. The pharma giant aims to commercialize the drug Rimegepant, sold under the Nurtec brand for the treatment of episodic migraines. Pharma giants are flush with cash since the pandemic, and are looking to deploy capital to shore up their drug pipelines.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP

View full image: US M&A sectors by volume H1 2022 (PDF)

View full image: US M&A sectors by volume H1 2022 (PDF)

View full image: US M&A sectors by value H1 2022 (PDF)

View full image: US M&A sectors by value H1 2022 (PDF)