Global IPOs hit back strongly after COVID-19 crash

IPO activity ground to a halt following the outbreak of the pandemic, but activity in the second half of the year more than made up for the downturn

The impacts of the pandemic were inescapable, but the global IPO market registered significant successes during 2020, ending the year on a high

With much of the world in lockdown, COVID-19 inevitably depressed the global IPO market during the first half of last year. But while both the number and value of listings declined, 2020 was anything but a write-off for new issues, as the second half of the year saw a significant pick-up. A record-breaking year for the special purpose acquisition company (SPAC) market also provided a boost.

Certainly, IPOs slowed to a trickle at times during H1 2020, notably at the height of the pandemic's first wave in Western Europe and North America in early spring. A year that began with promise—IPO activity was robust in January and February—was derailed by a black swan event.

However, certain sectors proved resilient. Technology, media and telecoms businesses, largely immune from the impacts of COVID-19, or even boosted by the pandemic, continued to come to market. The pharma, medical and biotech sector—at the center of the battle against the virus—also performed strongly.

Moreover, even businesses facing difficult market conditions proved that IPOs of attractive companies would continue to win support, and could be executed through the innovative use of technology. The listing of the coffee group JDE Peet's, managed through a three-day virtual roadshow, was a case in point.

This report, which features exclusive data provided by Mergermarket, considers the performance of the global market in 2020, highlighting key regions and trends. It also looks to the year ahead, finding real reasons for optimism, despite the ongoing impacts of COVID-19.

IPO activity ground to a halt following the outbreak of the pandemic, but activity in the second half of the year more than made up for the downturn

After more than a decade of buildup, special purpose acquisition companies (SPACs) have exploded and are gaining momentum in the US and beyond

Early-year highs gave way to a pandemic-driven downturn, which was then followed by a revival in H2

Although COVID-19 hit the region hard, there was a surge of IPOs in the second half of last year, mainly centered around Brazil’s consumer industry

As the pandemic continues to overshadow financial markets and the global economy, the following factors will have a major impact on the IPO market in 2021

Early-year highs gave way to a pandemic-driven downturn, which was then followed by a revival in H2

Stay current on your favorite topics

World in Transition

Our views on changing dynamics in energy, ESG, finance, globalization and US policy.

Some market sectors proved resilient during the pandemic, or even received a boost. Areas such as technology and e-commerce and biotech all continue to outperform, adding to investors’ appetites for good stocks.

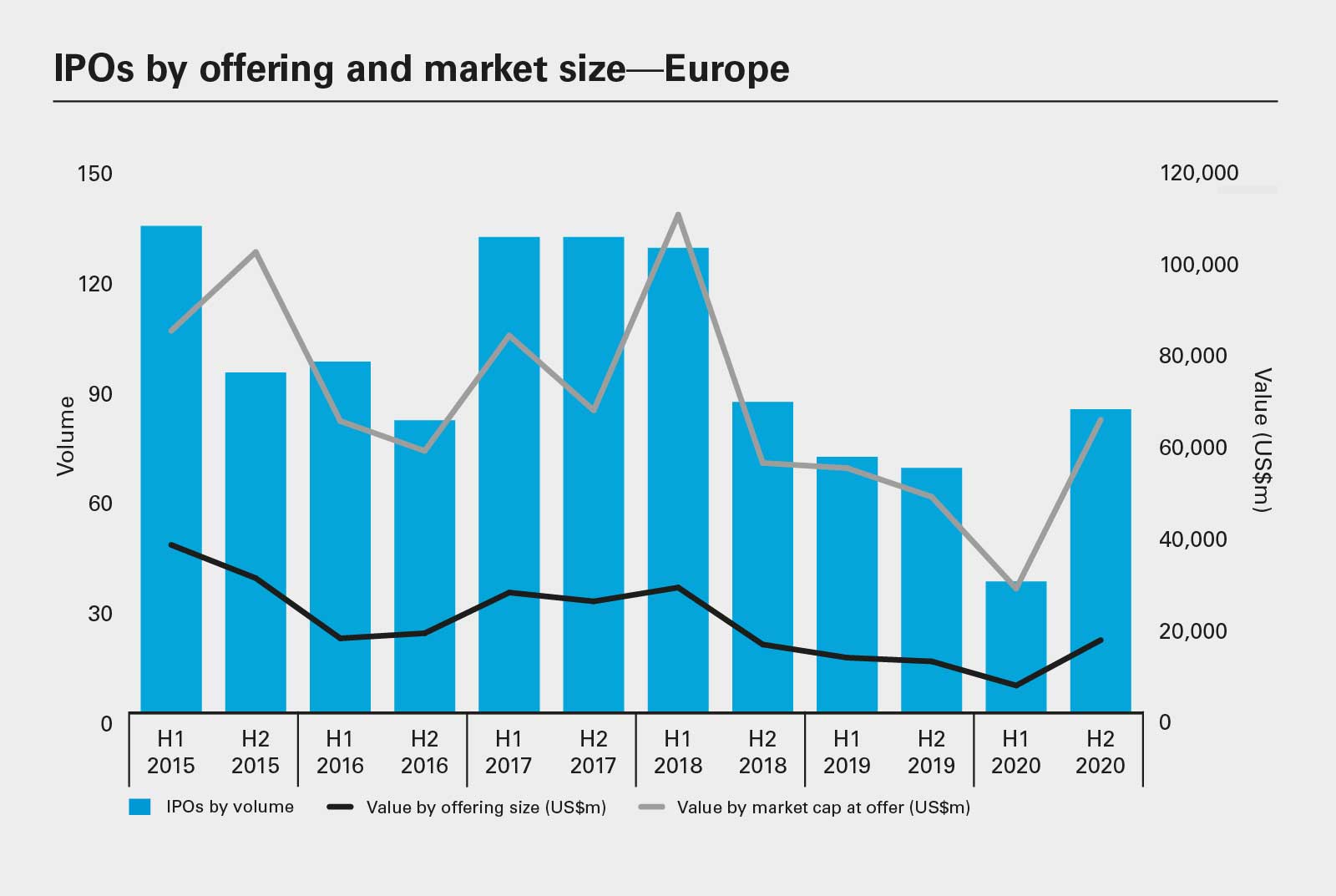

In line with global activity, the European IPO market was rocked by COVID-19 but staged a dramatic comeback in the second half of the year. And, surprisingly, the sources for this revival did not come from the continent's biggest economies.

The pandemic hit Europe harder than most markets. The first half of 2020 was the slowest such period for IPO activity in the region in the past five years. There were just 36 IPOs in the region during the first half, with a collective offering value of US$5.9 billion in total. That represented a 49 percent drop in volume compared to 2019 and a 51 percent decline in the total offer value.

The pre-COVID-19 period (January and February) had been characterized by optimism and IPO activity was relatively robust due to favorable conditions. Equity markets were in good health, buoyed by political stability following an agreement between the UK and the EU on how the former's departure from the EU would take place; December's decisive general election result in the UK also provided reassurance. Demand for good-quality IPOs also looked secure, particularly in sectors such as technology.

But as the scale and severity of the pandemic became apparent, IPOs were postponed or canceled altogether. Of the ten-biggest listings in the first half, not a single one took place during March or April, at the height of the crisis.

Those listings that did get off the blocks in the first half of the year were mainly clustered in the technology, media and telecoms (TMT) sector, which generated more IPOs than any other: 12.

The consumer sector, meanwhile, accounted for the greatest share of the market by value, raising US$3.2 billion. Almost all of that consumer total came from the IPO of the coffee giant JDE Peet's, the largest European IPO in the first half of the year. Indeed, its successful listing on Euronext Amsterdam, which raised almost US$2.9 billion, represented something of a turning point in May. The IPO was managed through a three-day virtual roadshow that circumvented COVID-19 travel restrictions and proved it was possible to get even large transactions underway in the face of the pandemic. In Italy, the IPO of industrials group GVS, the largest IPO in Italy and the second-largest deal in Europe in the first half of the year, took a similar approach.

49%

The year-on-year percentage decrease in volume of the Western European IPO market in H1 2020

The second half of the year saw a dramatic turnaround, with 83 listings including top-ten offerings for UK e-commerce firm The Hut Group and Polish online retailer Allegro. eu, with both raising approximately US$2.5 billion. This contributed to an H2 total of US$15.8 billion—the highest half year value since H1 2018. In total, US$21.7 billion was raised in 2020 from 119 deals—only 6.2 percent and 13 percent down, respectively, on the previous year, which shows the strength of the comeback and that solid fundamentals underpin the European market.

In addition, some market sectors proved resilient during the pandemic, or even received a boost. Areas such as technology, e-commerce and biotech all continue to outperform, adding to investors' appetites for good stocks. In terms of market share, TMT took the largest share of value with 35 percent followed by consumer with 16 percent. Volumewise, industrials took the top spot with 21 percent of listings, with TMT just behind at 20 percent. However, even more than sectors, it was the locations of the listings that made interesting reading and could provide a roadmap for future growth.

In almost any other year, the top region for listings in Europe for IPOs would have been the UK or Germany, in terms of both volume and value of listings. In 2020, however, new regions took precedence. In terms of volume, the Nordics had by far the most listings with 53—the UK was second with 18. Central and Eastern Europe had the highest listings value with US$5.4 billion, although a sizable chunk of that came from the Allegro.eu IPO in Poland. Amsterdam also proved to be a high-value location playing host to Europe's biggest IPO in the shape of JDE Peet.

One of the most innovative and busy exchanges in the region has been the Norwegian Merkur Market, a trading facility for small and medium-sized companies, which has seen astounding growth in the past year, especially from IT and renewables companies.

This spread of listings across Europe, rather than just the usual LSE and Euronext powerhouses, is a cause for genuine optimism in 2021.

Add to this a growing pipeline of deals, the continued early engagement of investors and, more importantly, a vaccine rollout across the continent, and Europe's strong recovery is very likely to continue.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP

View full image:IPOs by offering and market size—Europe (PDF)

View full image:IPOs by offering and market size—Europe (PDF)