Surging M&A surpasses expectations

All the stars aligned in 2021, creating a confident and exceptionally busy M&A market

Challenges loom—including the possibilities of tighter regulations, rising inflation and a stock market correction—but markets show little sign of slowing down

The value of US M&A blew past the US$2 trillion mark in 2021, ending the year more than 30 percent above the previous record set in 2015. US deal value reached US$2.6 trillion, twice the value of 2020, and volume set a new record at 7,896 transactions.

Confidence reigned among dealmakers as stock markets continued to rise; increasing numbers of SPACs sought merger targets; and private equity houses set new records, deploying some of the sector's historic levels of dry powder. All of which was underwritten by flexible and cheap debt financing.

Technology was a major driver of M&A, fueled by pandemic-related trends that continued to accelerate deployment of digital technologies across all sectors. The tech sector itself led the sector charts. Companies with product mixes boosted by the pandemic, including those in the pharma and healthcare sector, turned to M&A to complement and add to their existing business portfolios.

Despite a continuing positive outlook, dealmakers will need to keep potential risks in mind in 2022. Under the Biden administration, CFIUS went on a recruitment drive, and it will clearly continue to take a more aggressive stance across sectors, particularly when deals involve technology.

Indeed, regulatory scrutiny is tightening from a number of angles. The Securities and Exchange Commission under chair Gary Gensler is taking a tougher stance on enforcement and has its sights set on SPACs, cryptocurrencies and ESG. And the Federal Trade Commission has announced far-reaching antitrust policy changes that may require companies that reach settlements to observe a ten-year mandatory clearance period on new acquisitions and disposals—the new rules would even apply to buyers of affected assets.

This increasingly tough approach to regulating M&A has so far had little impact on dealmakers' appetites for transactions—although new rules may eventually render some deals less attractive.

In response to recent inflation, the Fed will increase interest rates, which could pose another challenge for dealmakers. But given that rates are so low by historical standards, increases are unlikely to have any direct significant effect on M&A for most of 2022.

One of the biggest questions is whether stock markets will continue to hold up. A correction seems inevitable at some point, but it's unclear what might trigger one in the foreseeable future. For example, markets seem to have shrugged off concerns related to the emergence of the Omicron variant of COVID-19—at least at the time of writing. And private equity still has a mountain of capital to deploy. Recent events, however, suggest that markets will be volatile.

As a result, although regulatory hurdles continue to multiply, we expect 2022 will be another strong year for US M&A, with robust activity through the first half and possibly well beyond.

All the stars aligned in 2021, creating a confident and exceptionally busy M&A market

Transaction values more than doubled year-on-year, as firms deployed ever-larger amounts of dry powder

Dynamics may be changing as the focus shifts to de-SPACs and regulatory scrutiny intensifies

In what was a stand-out year, M&A picked up the pace in almost every sector

Dealmaking may continue to rise, as price volatility abates and companies embrace energy transition

The pervasiveness of technology, particularly since the pandemic, continues to drive deals to all-time highs

Despite the absence of megadeals, M&A in the sector climbed from 2020 levels thanks in part to strong PE and SPAC activity

After dropping in 2020, real estate M&A ramped up significantly in 2021

The Federal Trade Commission is taking an increasingly stringent approach to antitrust investigations

Increased sector scope and concerns around a more aggressive approach to identifying non-notified transactions is leading to rising numbers of filings

Dealmakers should be braced for a more aggressive stance under Chair Gary Gensler

Borrower-friendly terms over the past few years have helped boost M&A totals—and a number of factors suggest the financing will not change dramatically in 2022

With data privacy laws tightening and cyberattacks on the rise, due diligence of technology networks and data processes should be a top priority for dealmakers

In the second half of 2021, Delaware courts issued several decisions affecting M&A dealmaking

Five factors that will shape dealmaking over the coming 12 months

Transaction values more than doubled year-on-year, as firms deployed ever-larger amounts of dry powder

Explore the data

In line with the broader M&A market, private equity firms had an exceptionally busy 2021. Deal value soared to US$987.6 billion in the year, more than doubling what was an already high total of US$474.5 billion in 2020. This is now the highest value recorded for any year on Mergermarket record (since 2006). Volumes were also up significantly, rising 59 percent to 3,460 deals—again, a new annual record.

US$987.6

billion

The value of US PE-related deals in 2021— more than double the same period in 2020

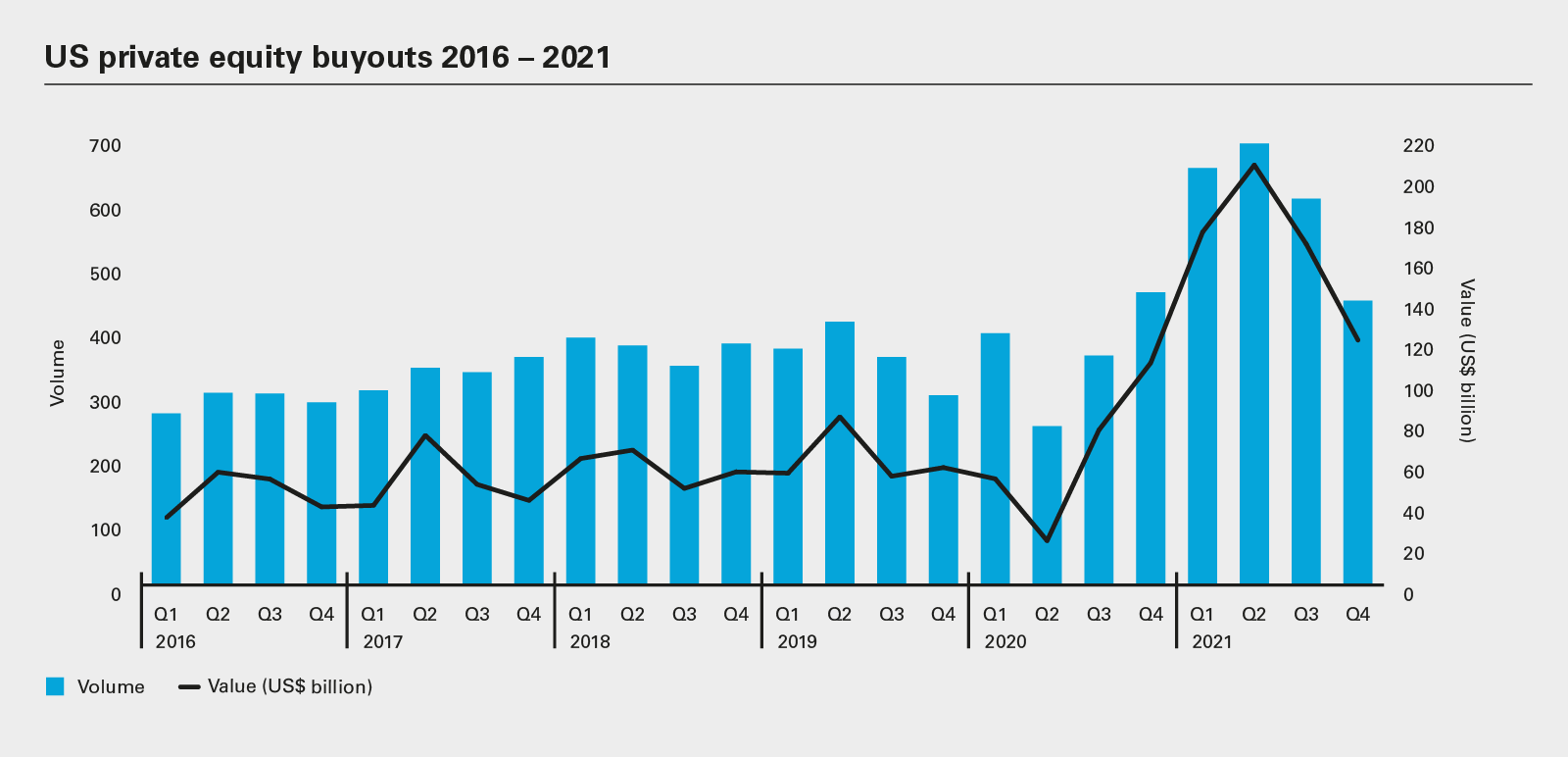

Buyouts drove much of this increase, as aggregate deal value jumped 157 percent on 2020 totals to US$665.5 billion, with volumes rising 64 percent to 2,385 deals. This high level of activity reflects the significant stores of dry powder at private equity firms' disposal. Globally, this stood at US$2.3 trillion in August 2021, according to Preqin, with US firms holding approximately 50 percent of the total. In addition, thanks to the trend for co-investment by private equity fund investors—the limited partners—the industry's firepower is significantly larger than these figures suggest.

Technology and healthcare continued to be among the more popular sectors for US-based private equity deals, accounting for more than half of the industry's total deal value. Indeed, the largest US private equity deal of the year was in healthcare. Medline Industries, a medical supplies manufacturer, was acquired for US$34 billion by a consortium that included The Carlyle Group, Hellman & Friedman, Blackstone Group, Abu Dhabi Investment Authority and GIC.

This transaction also demonstrates the recurring popularity of club deals. The profileration of club deals clearly reflects a step-up in the deal size some firms are targeting—an unsurprising trend given the fact that investor commitments are concentrating among larger firms—the top-25 firms between them are sitting on half a trillion dollars of dry powder.

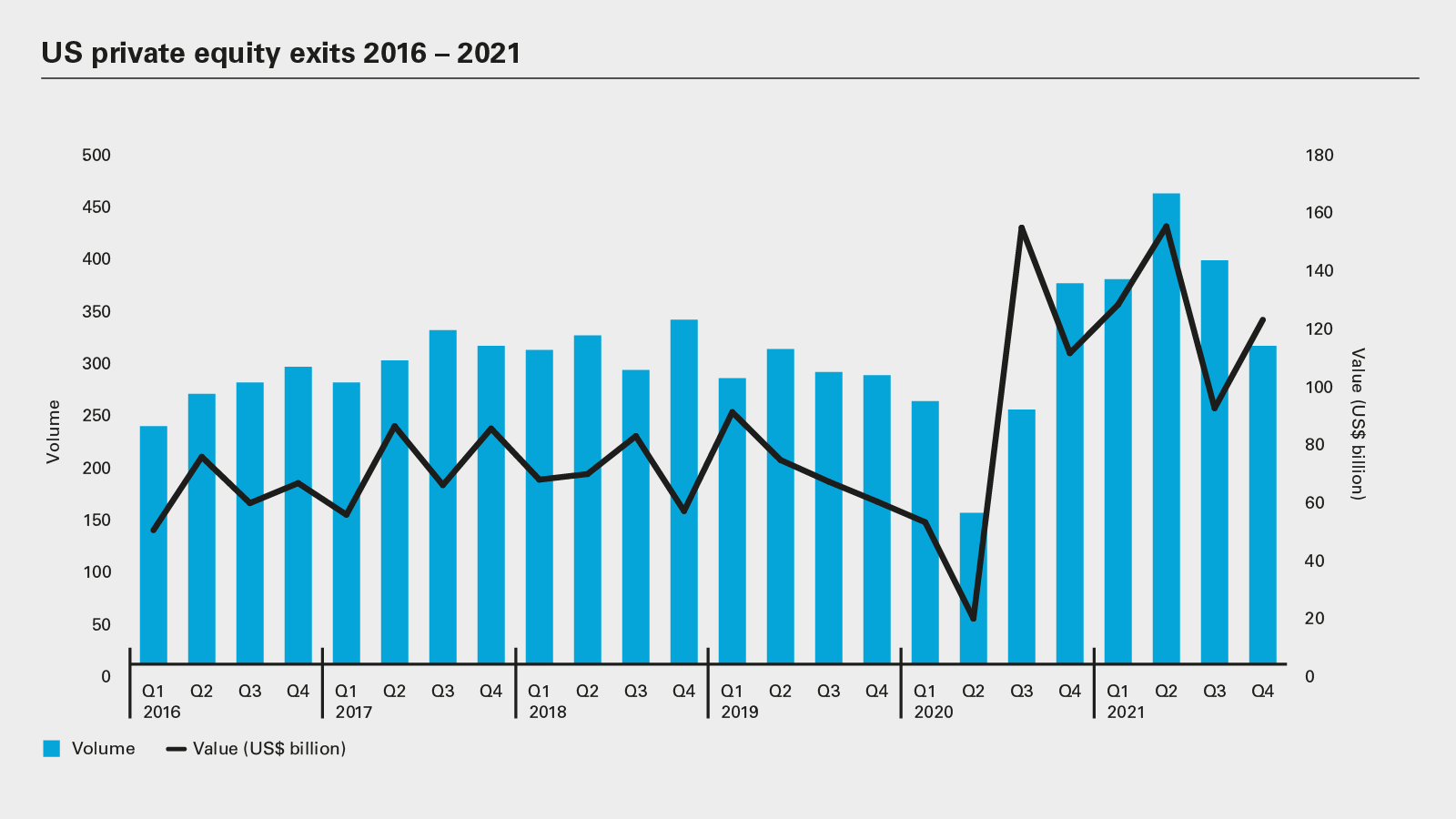

Given higher valuations, it's unsurprising that exit activity also rose in 2021, up 49 percent by value to US$482.2 billion and up 50 percent by volume, totaling 1,511 deals. Private equity houses are also clearly taking advantage of a seller's market to crystallize returns for their investors.

Among popular exit types is merging portfolio companies with a SPAC. Blackstone did just that to exit benefits provider Alight in a deal that valued the company at US$7.3 billion. With so many SPACs raised looking for targets, this trend may be only just beginning.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP

View full image: US private equity buyouts 2016 – 2021 (PDF)

View full image: US private equity buyouts 2016 – 2021 (PDF)

View full image: US private equity exits 2016 – 2021 (PDF)

View full image: US private equity exits 2016 – 2021 (PDF)