A look at the market and the most significant transactions

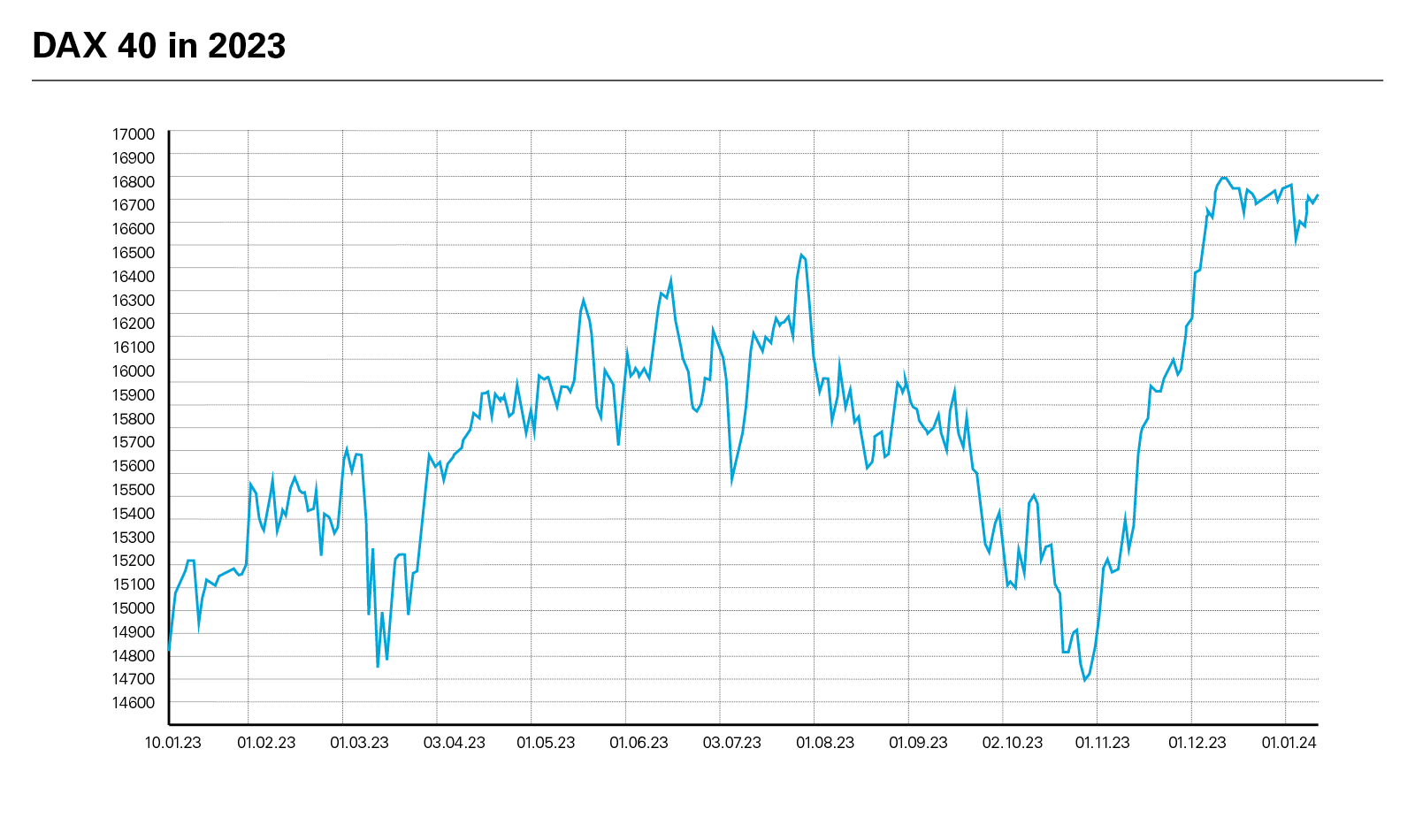

The public takeover analysis for 2023 appears at first glance to be a reprise of the previous year. The trends identified in 2022 continued, particularly the rather low number of transactions and average transaction volume, the significant role of private equity investors in larger transactions, the high proportion of delisting offers and the scarcity of takeover premiums. After initial weakness, the German stock market recovered in 2023 and the DAX 40 reached new record levels at the end of the year.

View full image: DAX 40 in 2023 (PDF)

View full image: DAX 40 in 2023 (PDF)

In 2023, potential bidders in the public takeover market acted with hesitation in view of geopolitical challenges. Their hesitancy was also likely due to the increased cost of debt financing.

At the end of the year, a surprising rally emerged, both on the stock market and in the public M&A market, with four public offers each with a transaction volume exceeding EUR 1 billion. The public M&A rally began in late October 2023 with private equity bidder Cinven's offer to acquire Synlab, a provider of laboratory and medical diagnostics services. The transaction volume amounted to around EUR 1.3 billion (corresponding to an underlying valuation for Synlab of around EUR 2.2 billion). The transaction attracted significant public attention, not least because of the role of Elliott, an activist shareholder. This was despite the fact that, prior to the offer, Cinven already held around 42.75 percent of the voting rights in Synlab and managed to secure access to a total of around 80 percent of the shares in advance of the offer by concluding agreements with other major shareholders, including Synlab's founder, Bartholomäus Wimmer. Cinven first acquired a stake in Synlab in 2015 and floated the company on the stock exchange in the spring of 2021. In the context of the acquisition offer, Cinven was able to purchase a further 35.39 percent of the voting rights and thereby increase its shareholding to 84.65 percent of Synlab's share capital.

Another deal that received significant public attention was the container shipping company MSC's voluntary takeover offer for the Hamburg-based port logistics company HHLA, which was published in late October 2023, with a transaction volume of EUR 1.3 billion (corresponding to the value of all issued shares of HHLA). By concluding qualified non-acceptance agreements for around 75 percent of the HHLA shares, the financing volume was reduced to around EUR 314 million for the remaining 25 percent of the HHLA shares. The City of Hamburg and MSC had announced their intention to jointly manage HHLA in the future by transferring their respective shareholdings, totalling 92.3 percent of all shares, to a (new) joint venture. However, HHLA's works council expressed strong opposition to MSC's participation.

In November 2023, automotive supplier Schaeffler published an offer to acquire Vitesco, a drive specialist, in which Schaeffler already held 49.94 percent of the shares through a holding company. The transaction volume amounted to EUR 1.8 billion, corresponding to an underlying valuation for Vitesco of around EUR 3.6 billion. After successfully increasing its stake, Schaeffler intended to fully integrate Vitesco into the Schaeffler Group through a merger. The offer was published without the prior conclusion of a business combination agreement with the target company. Such an agreement was only entered into during the acceptance period for the offer and provided for, among other things, an increase in the offer price. Nor did the offer provide for a minimum level of acceptance. At the end of the acceptance period, Schaeffler announced that it had acquired (directly and indirectly) 79.82 percent of the shares in Vitesco. Schaeffler thereby achieved the qualified majority required to approve the merger at Vitesco's general meeting scheduled to be held in early February 2024. Schaeffler's offer was successful despite opposition from the hedge fund Greenlight Capital, as well as the fact that Vitesco's management published a neutral reasoned statement on the offer because they considered the (increased) offer consideration to be too low based on three fairness opinions.

In early December 2023, the Spanish telecommunications group Telefónica published a partial acquisition offer to the shareholders of its German subsidiary Telefónica Deutschland (known under its brand name O2). Telefónica aimed to acquire up to 18.52 percent of the share capital, which corresponded to a transaction volume of EUR 1.29 billion (based on an underlying valuation of around EUR 6.99 billion). The offer was accepted for 7.86 percent of the shares, allowing Telefónica to increase its stake in Telefónica Deutschland to 93.10 percent.

In addition, reports of a very large transaction appeared in the press in mid-December 2023, according to which the Abu Dhabi-based oil company ADNOC intended to acquire shares in Covestro by way of a public takeover with a transaction volume of EUR 11.6 billion. However, neither a notification of the bidder's decision to submit an offer pursuant to section 10 of the German Securities Acquisition and Takeover Act (the "Takeover Act") nor an offer document had been published on the website of the Federal Financial Supervisory Authority (BaFin) by the end of 2023.

The only other voluntary takeover offer with a transaction volume of more than EUR 1 billion published in 2023 was the offer made by US private equity fund Silver Lake to the shareholders of Software AG (with a transaction volume of EUR 2.9 billion, including new shares resulting from the conversion of the outstanding convertible bonds). It briefly looked as if a bidding war would break out between Silver Lake and British private equity firm Bain Capital. Despite Silver Lake's controlling stake, Bain Capital (whose shareholding was significantly smaller) prepared a more attractive offer without the support of Software AG's management. Bain Capital fought for the support of its American opponent, as well as that of the target company's major shareholder, Software AG Stiftung, and planned to merge Software AG with its portfolio company Rocket Software following the takeover offer. However, Silver Lake was able to present more attractive plans for the target company, with the result that Bain Capital did not ultimately publish its planned offer. Silver Lake was subsequently able to increase its stake to more than 60 percent. The delisting of Software AG was announced at the end of December 2023.

Key figures and features of Takeover Act procedures in 2023

Trend towards delisting offers

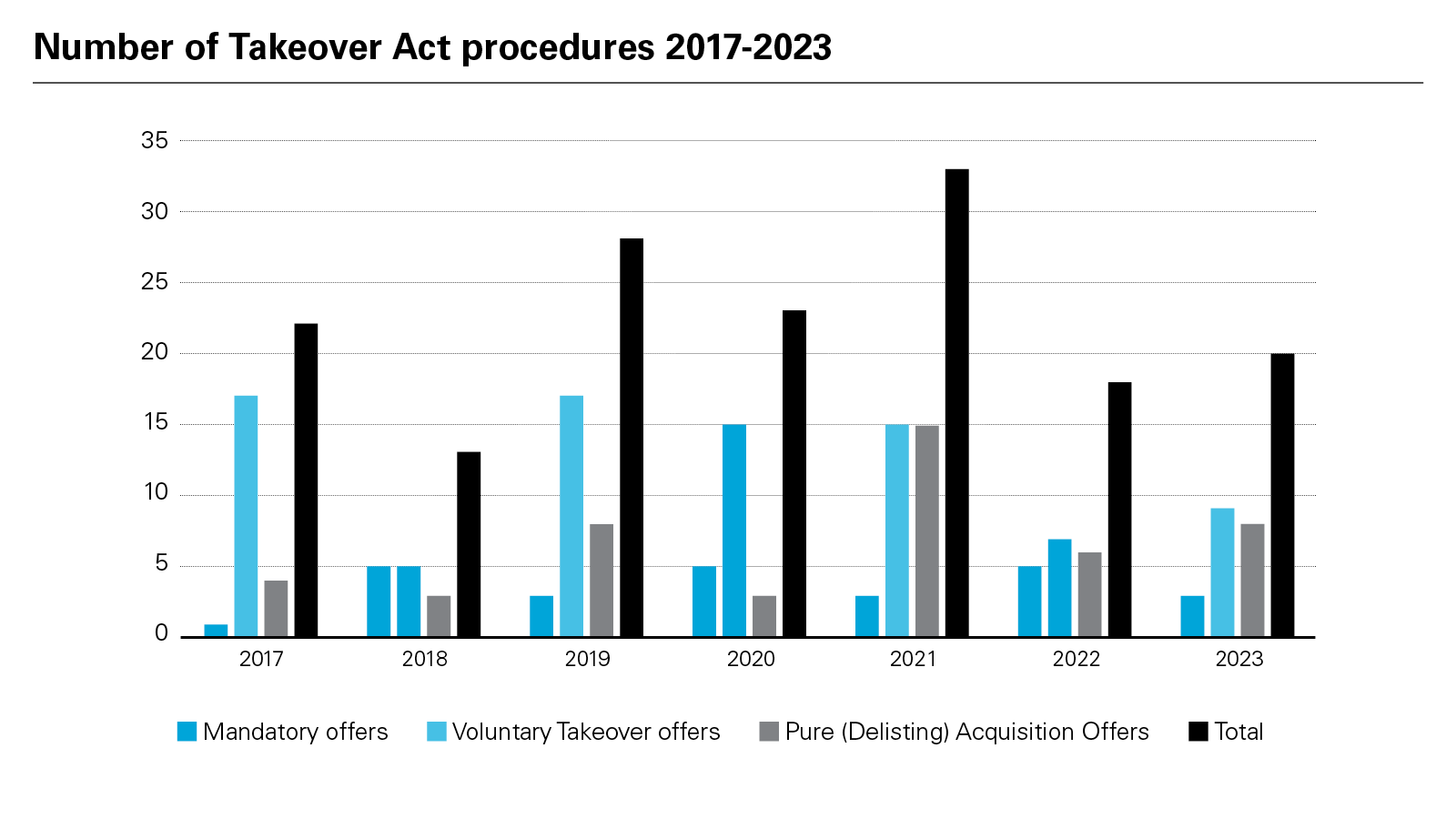

The continued high proportion of delisting offers in 2023 was noteworthy. Eight out of 20 published offers were delisting offers, compared to six out of 18 offers in 2022. This indicated investors' view that a stock market listing is currently unattractive. Furthermore, the trend of coupling voluntary takeover offers or mandatory offers with a delisting offer continued with three cases in 2023 (namely SD Thesaurus' mandatory offer for Bauer and the voluntary takeover offers of MS Proactive Verwaltung GmbH for MS Industrie AG and TPPI for Schumag). Plain mandatory offers remain the exception, with only three in 2023.

View full image: Number of Takeover Act procedures 2017-2023 (PDF)

View full image: Number of Takeover Act procedures 2017-2023 (PDF)

Bidders (strategic investors vs. private equity funds)

The billion euro offers of Silver Lake for Software AG and Cinven for Synlab, as well as KKR's offer for aerospace company OHB with a transaction volume of around EUR 264 million (OHB having a market capitalization of around EUR 800 million) demonstrate private equity's significance in the public takeover market. The delisting offer with the highest transaction volume of EUR 1.7 billion, made to the shareholders of Vantage Towers AG, was published by a private equity consortium comprising KKR and GIP. Private equity bidders were involved in seven out of 20 transactions under the Takeover Act in 2023.

However, the last three offers under the Takeover Act published in 2023 show that strategic investors are increasingly prepared to acquire listed companies. All three offers had a transaction volume exceeding EUR 1 billion and were prepared by strategic investors. In 2022, the three offers with a transaction volume exceeding EUR 1 billion were all prepared by private equity bidders.

There was no apparent industry focus in 2023. The voluntary takeover and acquisition offers that were not published directly in preparation for a delisting concerned target companies from diverse sectors, including telecommunications, automotive suppliers, port logistics, laboratory and medical diagnostics services, aerospace technology, IT and software, steel and metal distribution, lithium-ion battery technology, holding companies and a company for thermal transport boxes.

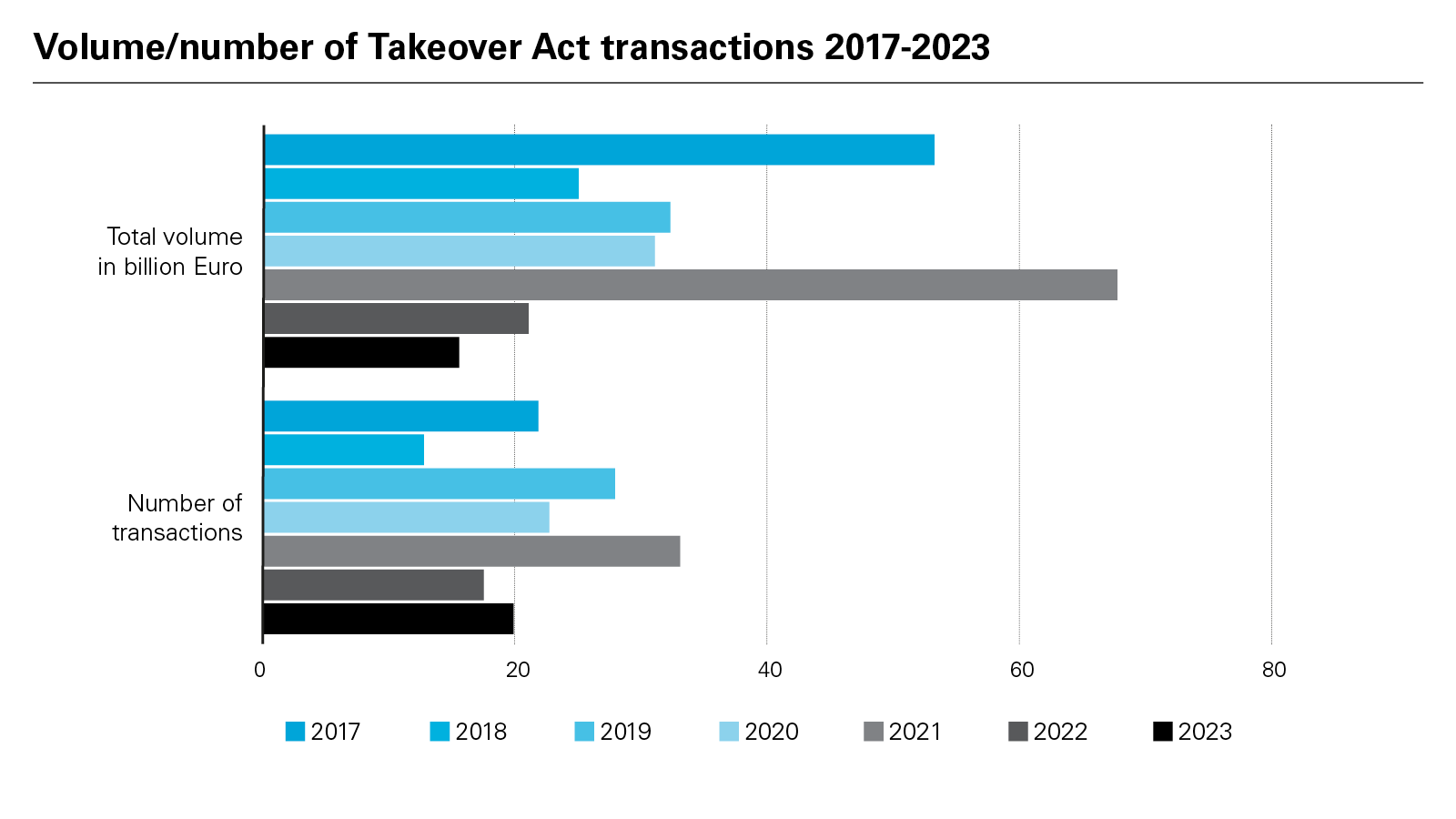

View full image: Volume/number of Takeover Act transactions 2017-2023 (PDF)

View full image: Volume/number of Takeover Act transactions 2017-2023 (PDF)

Consideration and financing measures

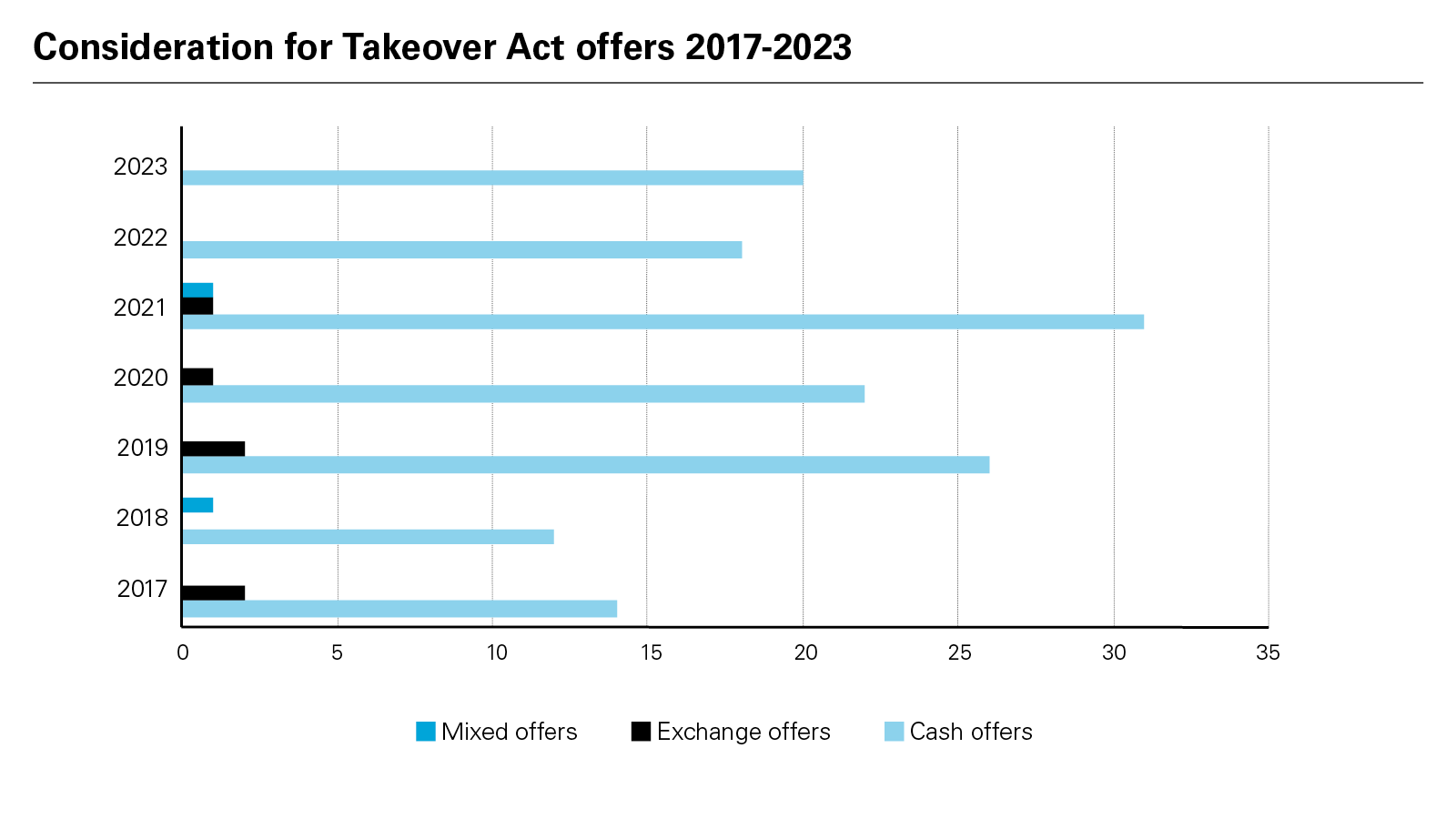

Furthermore, the trend of reducing the financing volume in Takeover Act procedures by concluding non-tender agreements was reinforced. If one disregards the shares economically excluded from the financing confirmation through the conclusion of such agreements, then the total transaction volume (and thus the financing volume to be demonstrated for the financing confirmation according to section 13 of the Takeover Act) of the 20 Takeover Act procedures in 2023 amounts to only EUR 11.9 billion.

In theory, the sharp rise in interest rates since September 2022 could have led to a renaissance for exchange offers in structuring public takeovers. However, a judgment of the Frankfurt Higher Regional Court on exchange offers, dated 11 January 2021, has led to the perception that a use of shares as consideration is not a viable option when structuring an offer under the Takeover Act. This is due in particular to the court's interpretation of the term "liquid share" and resulting high legal and practical obstacles for exchange offers. Shares were not offered as consideration for any takeover transactions in 2023, not even as part of "mixed consideration".

View full image: Consideration for Takeover Act offers 2017-2023 (PDF)

View full image: Consideration for Takeover Act offers 2017-2023 (PDF)

In the current market environment of rising interest rates and expectations of stagnating or even declining share prices, willingness among investors to pay high premiums when acquiring a listed company is the exception. In 50 percent of the 20 offers under the Takeover Act, the consideration corresponded to the statutory minimum price pursuant to section 4 of the Takeover Act's Offer Regulation (i.e., the value of the highest consideration granted or agreed for shares in the target company by the bidder or a person acting jointly with the bidder in the six months preceding the publication of the offer document). It is interesting that premiums were paid again when the takeover market began to recover towards the end of 2023, even though three of the four offers were plain acquisition offers and, therefore, not subject to the price requirements stipulated by the Takeover Act and the Offer Regulation. Compared to the shares' three-month volume-weighted average price, Telefónica offered a premium of 36.3 percent to O2 shareholders, Schaeffler offered a premium of 23.4 percent to Vitesco shareholders (after increasing the consideration during the offer period) and MSC offered a premium of 48.78 percent to HHLA shareholders. Aside from the foregoing, only Fujitsu was willing to pay a premium (of 34.66 percent) in its offer for GK Software, likely due to the high valuations of software companies.

Prohibitions

BaFin did not prohibit the publication of any offer documents in 2023.

Mostly positive joint reasoned statements by the management board and the supervisory board of target companies

As in the previous year, the target company's management board and supervisory board generally published a joint reasoned statement on an offer under the Takeover Act. Separate statements from the management board and the supervisory board are no longer market practice.

The target company's management supported the offer in 14 of the 20 published Takeover Act procedures. In most cases, one or more fairness opinions, which are usually published together with the management's reasoned statement, were obtained to support the decision on whether the offer price was adequate. For delisting offers, management generally either did not obtain fairness opinions or made reference to the opinion obtained for the previous voluntary takeover offer. A valuation report in accordance with the IDW S-1 standard was obtained for the combined voluntary takeover and delisting offer for MS Industrie, while a fairness opinion was obtained for the combined mandatory and delisting offer for Bauer AG.

In almost all procedures, the bidder and the management of the target company entered into negotiations in advance of the takeover offer and, sometimes, did so during the offer period. This often resulted in the conclusion of a business combination/investment agreement or, in the case of delisting offers, in a delisting agreement. The subject of such an agreement is usually the commitment of the target company's management to support the offer. In the case of the high-volume acquisition offers launched at the end of the year (Cinven/Synlab and Schaeffler/Vitesco), the target's management board and supervisory board issued neutral joint reasoned statements because they considered the offer price to be too low, despite discussions with the respective bidders.

No target company's management considered an offer "hostile" in 2023. When management rejected the offer, the consideration was always considered too low (in the case of the SWOCTEM/Klöckner voluntary takeover offer, this was supported by a fairness opinion, while this was based on the management's own assessment in the case of the Triathlon/Voltabox and Endurance/exceet mandatory offers). In all three procedures, no agreement was reached between the bidder and the target company's management board.

Works councils published their own reasoned statements more often than in previous years. The works councils provided positive support for both KKR's offer for OHB and Cinven's offer for Software AG. This is noteworthy because employee representatives were often critical towards private equity bidders in the past. In the case of HHLA, however, the employee representatives rejected MSC's offer.

New trends in transaction protection

Generally, there appears to be a certain reluctance to make the success of a takeover or acquisition offer dependent on extensive closing conditions. Mandatory offers and delisting offers cannot be subject to conditions in any case.

Nine of the ten voluntary takeover and acquisition offers published in 2023 were subject to conditions. It is noteworthy that obtaining necessary regulatory clearances and approvals was the only condition in some cases. For example, the voluntary takeover offer for HHLA was conditioned upon obtaining approvals under subsidy control law and foreign trade and payments law as well as approval by Hamburg's state parliament, while Octapharma's voluntary takeover offer for SNP Schneider-Neureither & Partner was conditioned upon approval by the German Federal Cartel Office. Investment control conditions had to be included in seven cases and the conclusion of (new) subsidy control procedures was a condition to three takeover offers (see "Increasing importance of regulatory approvals" below).

Few bidders still consider it constructive to include a minimum acceptance threshold as a condition in their offer. This condition was identified in three offers in 2023, namely in the Fahrenheit/va-Q-tec voluntary takeover offer, in Fujitsu's offer for GK Software SE and in Silver Lake's offer for Software AG. However, Silver Lake waived the minimum acceptance threshold of 50 percent + 1 share during the acceptance period and managed to secure 84.29 percent of shares during the additional acceptance period. In the other two instances, the minimum acceptance threshold was successfully exceeded during the offer period.

In principle, the inclusion of a "minimum acceptance threshold" condition in public takeovers was thought to guarantee achievement of an appropriate acceptance rate. Bidders' concern that they will fall short of the minimum acceptance threshold is due to the fact that a large share of institutional investors typically tender their shares only shortly before expiration of the acceptance period or only during the additional acceptance period. As a result, bidders often do not have an opportunity to react if, at the end of the acceptance period, the number of tendered shares does not exceed the minimum acceptance threshold. The bidder's right to lower the minimum acceptance threshold until the end of the acceptance period (but not during the two-week additional acceptance period provided for takeover offers after the regular acceptance period), often leads to undesirable, sub-optimal results. Whether the condition has been satisfied and, consequently, whether the offer has succeeded or failed, should not be unclear to shareholders or the target company for an extended period of time. It would therefore be beneficial if the legislature would allow a bidder to reduce the minimum acceptance threshold until publication of the acceptance rate after expiration of the acceptance period in accordance with section 23 paragraph 1 sentence 1 No. 2 of the Takeover Act. While the Financing for the Future Act implemented several changes to technical aspects of the Takeover Act at the end of 2023 (see below "The impact of the Financing for the Future Act and the EU Listing Act on takeover law"), it did not introduce extensive reforms.

In addition to the minimum acceptance threshold, Silver Lake's takeover offer for Software AG included several other extensive conditions, including a market MAC clause (relating to the development of the SDAX), the non-implementation of capital measures or other structural measures as well as the absence of a determination of a material compliance violation (as confirmed by a neutral expert). Similarly extensive conditions can be found in Schaeffler's offer for Vitesco, KKR's takeover offer for OHB and Fujitsu's takeover offer for GK Software SE.

The current geopolitical situation was reflected in SWOCTEM's offer for Klöckner & Co. In addition to various standard conditions, the offer was subject to the condition that the North Atlantic Council not invoke the collective defense clause in Article 5 of the North Atlantic Treaty of 4 April 1949. This condition was first used in Oaktree's 2022 offer for Deutsche Euroshop.

Increasing importance of regulatory approvals

The significance of regulatory proceedings in the context of public takeovers has increased continuously over the years. Merger control approvals were required (in some cases in multiple jurisdictions) in nine of the 20 procedures in 2023.

The German legal regime governing foreign direct investments (FDI) was strengthened several times in recent years to impose stricter control over foreign direct investments in Germany, with the consequence that FDI approvals have become increasingly important in public takeovers. In 2023, investment clearances (in some cases in multiple jurisdictions) were a closing condition in seven cases.

In 2023, the German Federal Ministry for Economic Affairs and Climate Action ("BMWK") abandoned its earlier strategy of progressive updates to the FDI legal framework. In early September 2023, it presented an evaluation of the first act amending the Foreign Trade Act as well as the latest amendments to the Foreign Trade Regulation, which aimed to provide a comprehensive assessment of investment control laws in Germany. The report concludes that current rules provide effective protection for German and European security interests without calling into question Germany's general attitude of openness toward foreign investors. Nevertheless, the BMWK is planning a comprehensive update of the German FDI rules to reflect increasing geopolitical concerns, as well as experience gained during the FDI procedures conducted in recent years.

Although the BMWK has not yet published statistics for 2023, it can be assumed that the number of transactions examined was even higher than in previous years (306 cases in each of 2021 and 2022). It continues to adopt a critical approach towards investments from Russia and China and has strengthened its review of investments by state-owned enterprises, particularly from the Middle East.

The EU Foreign Subsidies Regulation (FSR) came into force on 12 January 2023, adding another regulatory approval to be considered when preparing a public takeover. Transactions must be notified if the acquired company (or one of the companies to be acquired) or the joint venture is resident in the European Union, generated a total turnover of at least EUR 500 million in the European Union in the last financial year, and the companies involved in the transaction received financial contributions from non-EU countries of more than EUR 50 million in the last three years.

The notification requirements are accompanied by prohibitions on completion: M&A transactions requiring notification cannot be closed and public contracts cannot be awarded to the bidders concerned as long as the commission's review is pending. Significant fines can be imposed in the event of violations of the notification requirement and/or the prohibition on completion.

Last year, the new regulatory notification requirement was included as a condition in three voluntary takeover offers, namely the offers for HHLA, Synlab and OHB. Given the extent of "third-country financial contributions" recorded, a significant number of transactions will require notification and review going forward, which should be considered when planning a transaction.

The impact of the Financing for the Future Act and the EU Listing Act on takeover law

The legal framework for public takeovers has remained largely unchanged since the introduction of the Takeover Act in 2002. With the Financing for the Future Act, effective since 15 December 2023, the German legislature made a significant step towards digitalization of the takeover procedure and has implemented some procedural changes in the Takeover Act.

Communications with BaFin and the notification regime

The electronic filing of applications, documents and other communications required under the Takeover Act must now be carried out exclusively through BaFin's reporting and publication platform (MVP). This applies to bidders, applicants, target companies and other eligible persons such as attorneys (section 45 of the Takeover Act). The BaFin published guidelines on 14 December 2023 with details on the procedure for takeovers.

The introduction of mandatory electronic communications has dispensed with the requirement for wet-ink signatures on the offer document, in addition to making other consequential changes in relation to communication with BaFin (see section 11 para. 1 of the Takeover Act). Nonetheless, the wet-ink requirement continues to apply to the bidder's obligation to inform the target company's management board and to the financing confirmation (section 10 para. 5 sentence 1 and section 13 para. 1 sentence 2 of the Takeover Act). This is because the BaFin is not involved in such correspondence and, therefore, its electronic platform is not available.

Slight adjustments of a more technical nature were made to the reporting regime under takeover law. The requirement to notify BaFin 30 minutes prior to the publication of a notification of a decision to submit an offer pursuant to section 10 para. 2 sentence 1 of the Takeover Act has been repealed given its practical insignificance according to BaFin. New notification requirements were introduced by the Financing for the Future Act related to corrections to the offer in accordance with section 14 para. 3 sentence 3 of the Takeover Act and to reciprocal reservation agreements within the framework of the European regime on rules to prohibit frustrating actions (section 33c para. 3 sentence 5 of the Takeover Act). However, the prohibition of frustrating actions in the sense of sections 33a et seqq. of the Takeover Act has not played a role in German practice so far.

Time periods

One helpful change introduced by the Financing for the Future Act relates to the day-count convention in calculating applicable time periods, which had previously been based on a term for business days (Werktage) used in the Takeover Act that was not statutorily defined and, according to BaFin's practice, included Saturdays. By imposing a uniform method of calculating time periods under takeover law based on the term for business days used in prospectus law (Arbeitstage) and including a new defined term, the amendment ensures that, in principle, time periods will not end on days that are not work days at BaFin's headquarters in Frankfurt am Main. Practical curtailments of time periods, which occurred when a time period expired on a public holiday in Frankfurt, are no longer an issue.

Multi-voting shares

The Financing for the Future Act reintroduced multi-voting shares into German stock corporation law, which can affect interactions with German takeover law in certain scenarios. The new section 12 of the German Stock Corporation Act provides for the expiration of multiple voting rights after an initial public offering or in the event of a transfer of the multi-voting shares ("transfer-based sunset clause"). Upon expiry of the multi-voting rights, the total number of voting rights in the company is reduced, which can shift the proportion of voting rights and cause a shareholder to exceed the control threshold relevant for takeover procedures (section 29 para. 2 Takeover Act). The legislature provided affected shareholders the ability to obtain an exemption from the obligation to publish a notification of the acquisition of control and a subsequent mandatory offer (according to section 37 Takeover Act in conjunction with section 9 sentence 1 no. 5 of the Takeover Act's Offer Regulation). Section 9 sentence 1 no. 5 of the Takeover Act's Offer Regulation expressly lists a "reduction in the total number of voting rights in the target company" as one of the reasons for granting such exemption. The legislature explained in an explanatory memorandum to the Financing for the Future Act that this exemption should also cover scenarios where the reduction in the total number of voting rights results from a reduction of multiple voting rights.

Treatment of protracted processes under insider dealing law

The EU Commission's proposal for the EU Listing Act could also have an impact on the planning of public takeovers. The preparation of a public takeover consists of numerous intermediary steps and, in many cases, constitutes a so-called protracted process within the meaning of the legal regime governing insider dealing and ad hoc disclosures under the Market Abuse Regulation (MAR). Under current law, such intermediate steps can constitute insider information (regardless of whether the occurrence of the final event is more likely than not) and thus trigger a notification obligation of the bidder and the target company. If it is in doubt as to whether an ad hoc disclosure is required, Article 17(4) MAR provides for the possibility of delaying the disclosure of the relevant insider information (so-called self-exemption). According to ESMA Guidelines, there is a legitimate interest in delaying disclosure if it is not likely to mislead the public and the issuer is able to ensure the confidentiality of that information. Compliance with MAR primarily affects the target company. However, listed bidders also have to regularly determine at which point in time they publish their decision to submit an offer in accordance with section 10 of the Takeover Act and how this interacts with the disclosure obligations under MAR (including in respect of any previous intermediary steps).

In the case of protracted processes such as M&A transactions, the obligation to publish insider information would no longer apply to intermediate steps under the proposed Listing Act; only the final event would have to be published. The EU Commission would publish a delegated act with a (non-exhaustive) list of typical examples of insider information to simplify the assessment as to which information has to be disclosed. Because the precise structure of the provisions on insider-related protracted processes under the new Listing Act is still unclear, the effects of new provisions with respect to insider dealing on the preparation of public takeovers remain uncertain.

Acting in concert

Also relevant to public takeover practice is an article published by BaFin on 30 March 2023 on "collaborative engagement" by institutional investors regarding sustainability issues and the attribution of voting rights. It points out that institutional investors often come to an agreement with each other in order to more effectively represent their positions on ESG topics vis-à-vis the companies in which they invest, but that such collaborative engagements can be classified as acting in concert. Such exchanges can vary in their extent, ranging from non-binding discussions on sustainability issues to agreeing on a joint approach vis-à-vis the company's governing bodies. According to BaFin, such agreements can fulfil certain criteria for the attribution of voting rights under the German Securities Trading Act (WpHG) and the Takeover Act and can, in particular, meet the legal prerequisites for "acting in concert". This, in turn, means that shareholders or their subsidiaries are deemed to be acting in concert if they coordinate their conduct regarding a listed company. Acting in concert means that the parties involved reach an understanding on the exercise of their voting rights or otherwise collaborate with the aim of bringing about a lasting and material change in the issuer's business strategy. This does not include agreements in individual cases.

According to its own statement, BaFin follows rulings of the Federal Court of Justice (BGH) and discusses various types of cases based on examples. Where such an agreement is reached in connection with the preparation of an offer under the Takeover Act, this is also deemed to be a case of acting in concert.

Judgments relevant for Public Takeovers in 2023

In 2023, there was only one – albeit remarkable – judgment regarding takeover law: on the Stada voluntary takeover offer in 2017. Following the regular acceptance period, in which the bidders Bain and Cinven were able to reach the (previously reduced) minimum acceptance threshold of 63 percent, the bidders entered into an agreement in the form of an "irrevocable commitment" with the hedge fund Elliott during the additional acceptance period. Pursuant to the agreement, Elliott committed to approve a domination and profit and loss transfer agreement (DPLTA) at the general meeting of Stada, provided that the compensation paid to shareholders would be at least EUR 74.40 per Stada share. The shareholders who tendered their shares during the public takeover offer had received only EUR 66.25.

Based on the irrevocable commitment agreement, Elliott was able to secure at least the difference to the original offer price for its Stada shares of EUR 8.15 per share, without having to tender these shares during the acceptance period of the takeover offer. Ultimately, Elliott only tendered its shares during the acceptance period of the later delisting acquisition offer, when the consideration had been further increased to EUR 81.73 per share.

For the shareholders who had already tendered their shares during the voluntary takeover offer and who had received the significantly lower consideration, the question arose as to whether they had a claim to subsequent payment based on the principle of equal treatment of all shareholders of the same share class, as stipulated in the Takeover Act. Generally, a bidder who purchases shares outside the stock exchange at a higher price within one year after the expiry of the acceptance period is obliged to pay the price difference to the shareholders who accepted the takeover offer (section 31 para. 5 of the Takeover Act). This includes agreements concluded during this period that entitle one party to demand the transfer of shares (section 31 para. 6 of the Takeover Act). Share purchases made "in connection with a legal obligation to pay compensation" (section 31 para. 5 sentence 2 of the Takeover Act) are excluded from the obligation to make additional payments, which also includes payments of compensation in connection with the conclusion of a DPLTA.

On 23 May 2023, the Federal Court of Justice (BGH) issued two identical judgments (court references II ZR 219/21 and II ZR 220/21) ruling in favour of equal treatment of shareholders. In relation to the post-takeover period, the court restricted individual agreements that certain major shareholders had preferred in practice with a view to a future DPLTA, a delisting or a squeeze-out. This is in line with other recent BGH judgments on Takeover Act-related issues (McKesson/Celesio and Deutsche Bank/Postbank), which focused on economic considerations in terms of equal treatment of shareholders in advance of a takeover bid.

The approach taken by the irrevocable commitment in the case of Stada was innovative from a legal point of view. The bidders did not acquire any other shares directly and did not receive a claim to purchase Elliott's shareholding. Rather, the consideration received by the bidders initially consisted only of Elliott's commitment to approve the proposed resolution on the DPLTA at the general meeting. According to the statutory wording, only agreements that entitle the bidder to demand the transfer of shares are treated as equivalent to a subsequent acquisition. Therefore, the Stada bidders argued, the irrevocable commitment had not triggered the subsequent payment obligation. In addition, the bidders took the view that the agreement related to an acquisition "in connection with an obligation to pay compensation" and was therefore also exempt from the subsequent payment obligation. The Frankfurt Higher Regional Court had considered this structure permissible and rejected claims to subsequent payment.

The Federal Court of Justice rejected both arguments. In an extensively reasoned judgment that referred to the legislative materials and the spirit and purpose of the statutory provisions, the court explained that how the bidder's subsequent share purchase comes about is irrelevant and that the exception for statutory compensation payments does not cover preliminary agreements relating to a DPLTA like the irrevocable commitment in question. The decisive factor was "the bidders' decision to be inclined from an objective point of view", to purchase the Elliott shares at a significantly higher price than the offer consideration paid to the other shareholders who tendered during the acceptance period of the takeover offer. This decision provided Elliot "with arbitrage opportunities that do not deserve protection".

The BGH has thus decoupled major shareholders' arbitrage opportunities under takeover law, which are generally not worthy of protection, from some of the special features of price formation in the context of a DPLTA and squeeze-out, and aligned the interpretation of the rules related to any subsequent claims in connection with takeover procedures with those applying under international pricing and takeover rules. The equal treatment of shareholders thus continues to receive a high degree of protection under public takeover law.

2024 Outlook

The start of 2024 has not given rise to expectations of a boom for public takeovers in Germany in the near term. Because the Financing for the Future Act recently made amendments of a largely technical nature to the Takeover Act in December 2023, further changes, such as a legal basis for greater flexibility for bidders to amend offers, are desirable, but not to be expected. It remains to be seen whether the legislature will reduce the high requirements imposed by the Frankfurt Higher Regional Court regarding the liquidity of the shares used as consideration in exchange offers to a level that would allow bidders with a lower market capitalization to proceed with an exchange offer. Currently, this is only wishful thinking in capital markets law.

Nevertheless, some potential bidders could be encouraged by the expectation of at least slightly lower interest rates to develop plans for debt-financed takeovers. It is therefore advisable, from the perspective of potential target companies, to carefully prepare potential defense strategies.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2024 White & Case LLP