European NPLs: Market earns welcome breathing room

What's inside

The ongoing decline in NPL volumes in 2022 and pivot towards smaller disposals leave European lenders well positioned to withstand adverse economic conditions.

Lenders are enjoying the fruits of their labours. Having offloaded their most toxic bad loans, in 2022 banks were instead able to focus on smaller, strategic NPL disposals, even as macroeconomic hardship began to mount.

Europe's banks have been on quite a journey to get their non-performing loans (NPLs) under control through NPL disposal tools including portfolio sales and securitisations. While disposals of toxic debt were interrupted by the COVID-19 crisis, this work has been unrelenting. In last year's edition of this study, we described how NPL sales in Europe in 2021 had bounced back from pandemic disruption; 12 months later, we can report that sales continued in 2022, though at much reduced levels.

That slowdown reflects the extensive progress already made by banks. Most have reached a point where the imperative to further trim their NPL volumes is much diminished—they are free to make disposals according to their strategic and tactical priorities, rather than to avert disaster. That remains true despite the mounting economic and geopolitical volatility that Europe has faced over the past 18 months.

In this year's report, we examine the outlook for Europe's NPL market, including for secondary sales, over the months and years ahead. The first section considers the changing market dynamics, including the latest NPL data and analysis of what is driving activity. The second section offers a deep dive into key markets across Europe.

The future is highly uncertain. There is a case to be made both for a resurgence in NPL volumes and deal activity, and for a continued slowdown. Much will depend on the economic outturn, where uncertainty levels are even more elevated. The good news, however, is that these are precisely the market conditions in which new opportunities abound.

European NPLs: New buyers emerge as disposals shrink

Despite broad economic turmoil, countries across Europe have so far avoided recession. Banks have been able to catch their breath with the NPL market shrinking steadily post-pandemic. But looking forward, Europe is hardly anxiety-free.

Regional spotlight on NPLs: Italy, the UK, Greece and Spain

Total NPL volumes across Europe are down and ratios remain stable, with countries such as Italy and Greece having worked especially hard to deal with toxic assets. Even with economic growth set to slow, banks have reason to be broadly optimistic about their NPL levels.

Declining NPL ratios have put banks in a somewhat more comfortable position than they were this time last year, but the threat of macroeconomic hardship looms over borrowers.

European NPLs: New buyers emerge as disposals shrink

Despite broad economic turmoil, countries across Europe have so far avoided recession. Banks have been able to catch their breath with the NPL market shrinking steadily post-pandemic. But looking forward, Europe is hardly anxiety-free.

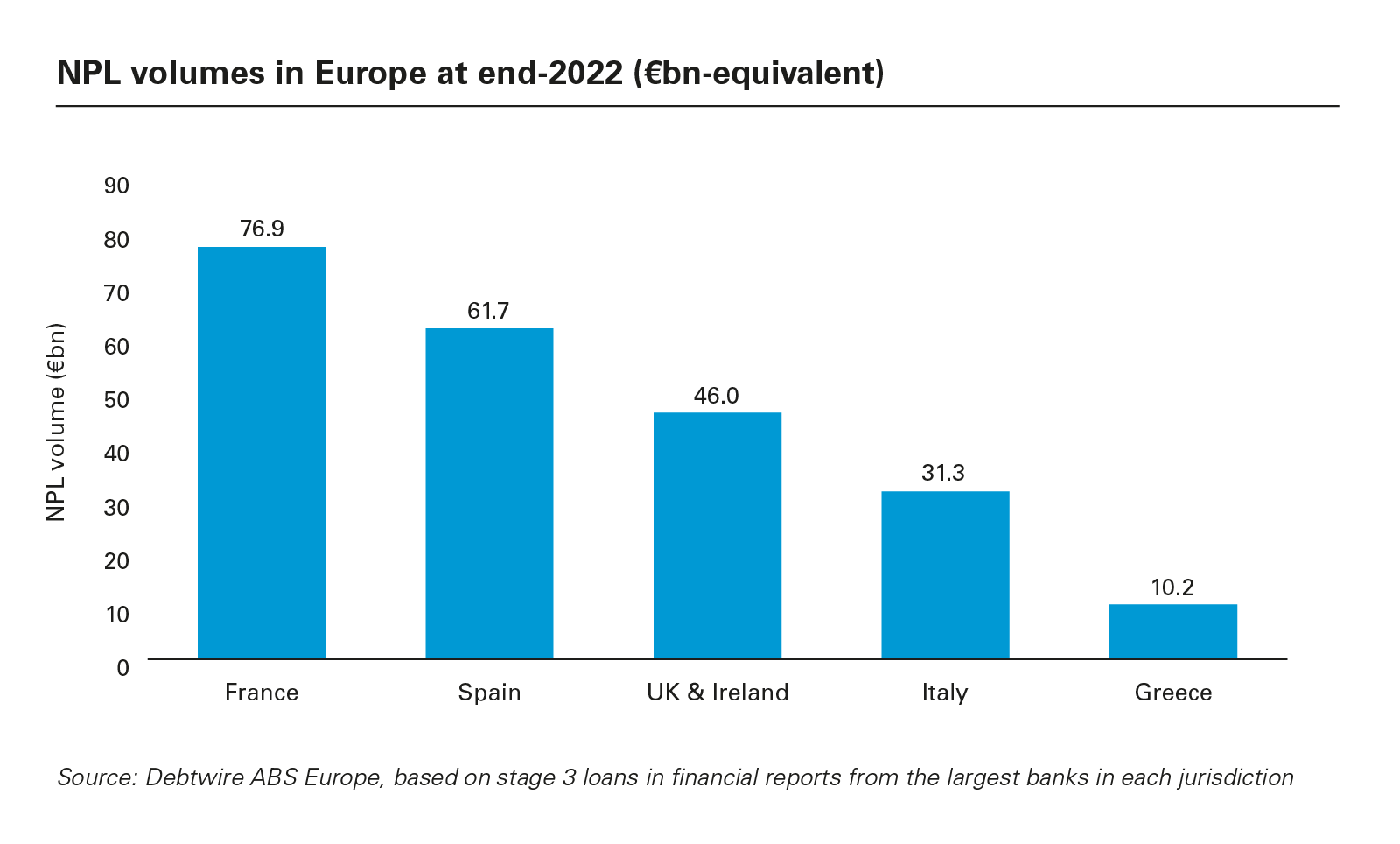

Value of NPLs held by the largest banks in major jurisdictions across Europe at the end of 2022

European NPL volumes fell by approximately 9 per cent in 2022, as recovery from the COVID-19 crisis continued. But Russia's full-scale invasion of Ukraine, darkening economic clouds and concern about growing geopolitical tensions all cast long shadows.

Against this backdrop, the European Banking Authority (EBA) exhibited considerable caution in its Q4 2022 Risk Dashboard. "Higher interest rates, persistency in inflation and macroeconomic uncertainty could weigh on economic growth and unemployment rates, which in turn could adversely affect banks' asset quality," the EBA warned. It pointed to data from Eurostat revealing that declared bankruptcy numbers had reached an all-time high at year-end.

Nonetheless, the data for 2022 looks relatively benign. Analysis from Debtwire ABS Europe shows that, at the end of the year, the largest banks across Europe held approximately €279 billion in stage 3 loans on their books, down from about €305 billion at the end of 2021. As in previous years, NPLs at banks in France, Spain, the UK, Italy and Greece accounted for the lion's share of that total—approximately €190 billion—with France leading the way.

Though hardly insignificant, these figures do represent a continuing downward trend. To put the 2022 data into context, European NPLs eclipsed €1 trillion in 2014.

That decline follows action to address historic NPLs—by banks themselves, as well as by policymakers in countries such as Greece and Italy. But it is also a reflection of the industry's more conservative stance on underwriting in recent years, reducing the risk of non-performance.

Against that, recent increases in capital costs may be prompting banks to take action more quickly to identify under-performing loans. All the more so given that rising levels of profitability—the EBA says banks' return on equity reached 8 per cent by Q4 2022—make it possible to confront losses. Still, the overall picture is of an NPL market that has shrunk steadily.

The question now is whether that will continue. The EBA points out that NPL ratios had already begun to widen in certain sectors of the economy last year—notably agriculture, mining and financial services, writing in its Q4 dashboard that "the trend of rising bankruptcies has recently become broader-based among countries."

The economic outlook has, of course, deteriorated. The latest forecast by the International Monetary Fund (IMF) for euro area GDP growth in 2023 is just 0.9 per cent. That compares to a forecast of 1.2 per cent when the previous edition of this study was published a year ago.

Inflation may be moderating in Europe, but it remains elevated by recent standards. Interest rate hikes are taking a toll and may make it challenging for struggling borrowers to refinance debt that was originally sourced at a much lower price. Besides these financial concerns, there appear to be few prospects of an end to the war in Ukraine in the near term.

In some countries, these pressures already appear to be feeding through. Several banks have reported significant increases in their volumes of stage 2 loans—those in the early stages of underperformance—particularly in the UK, Germany and the Netherlands. Banking sector stress, exemplified by the crises earlier this year at Silicon Valley Bank and Credit Suisse, adds to the sense of anxiety.

Given all these factors, there is no guarantee that NPL volumes will continue to fall over the course of 2023. Indeed, George Georgakopoulos, Intrum's Global Head of Servicing, emphasised that although there has not been a material increase in delinquency, it is only "a matter of time" until the NPL market becomes "lively" again. The market may have reached a turning point.

NPL disposals slow sharply

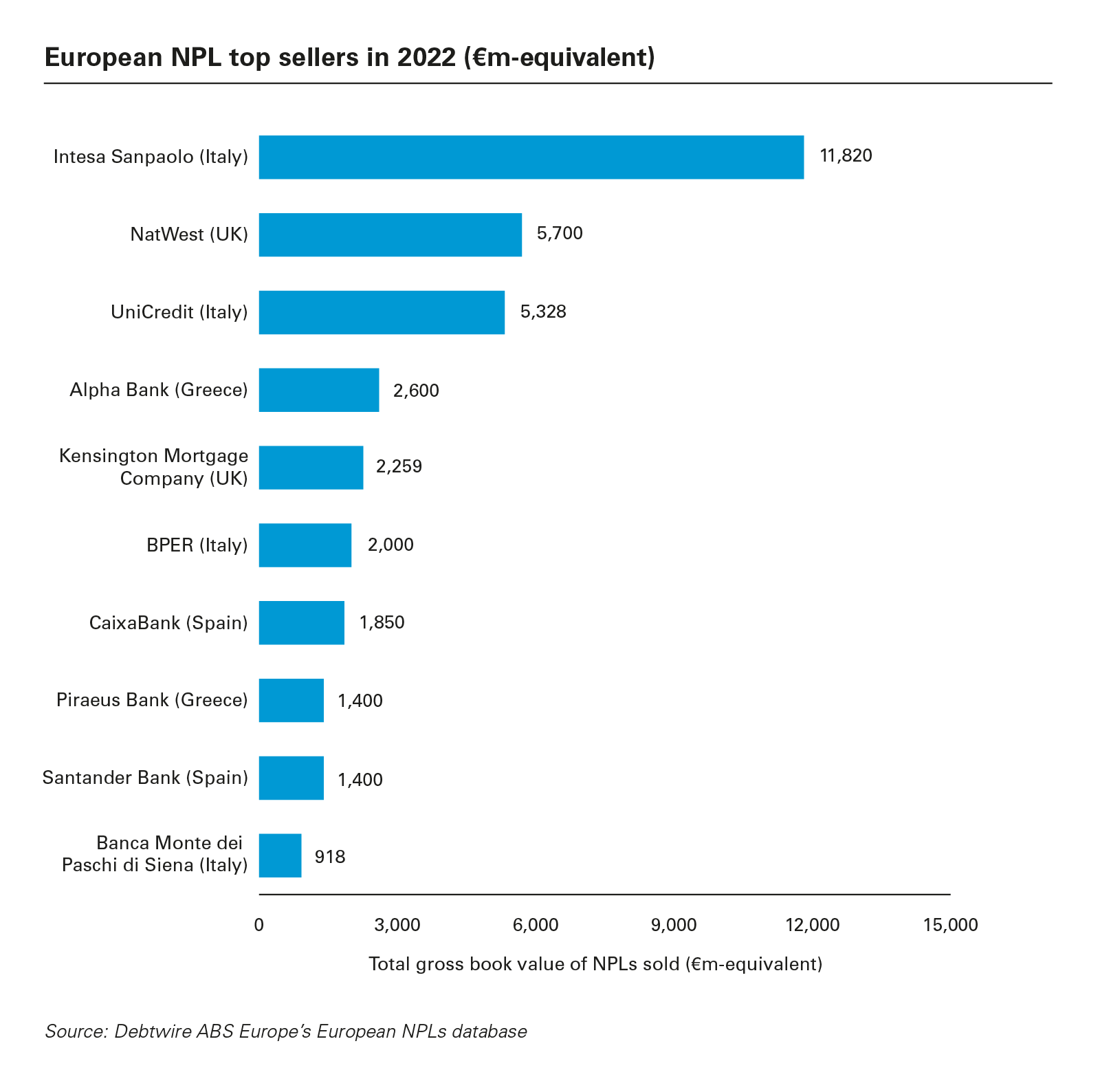

With Europe's banks continuing to shrink their stocks of NPLs, their need to dispose of these assets has naturally diminished. While NPL disposals continued in 2022, particularly in countries such as Italy and the UK, there is no doubt that the market was far quieter than in previous years.

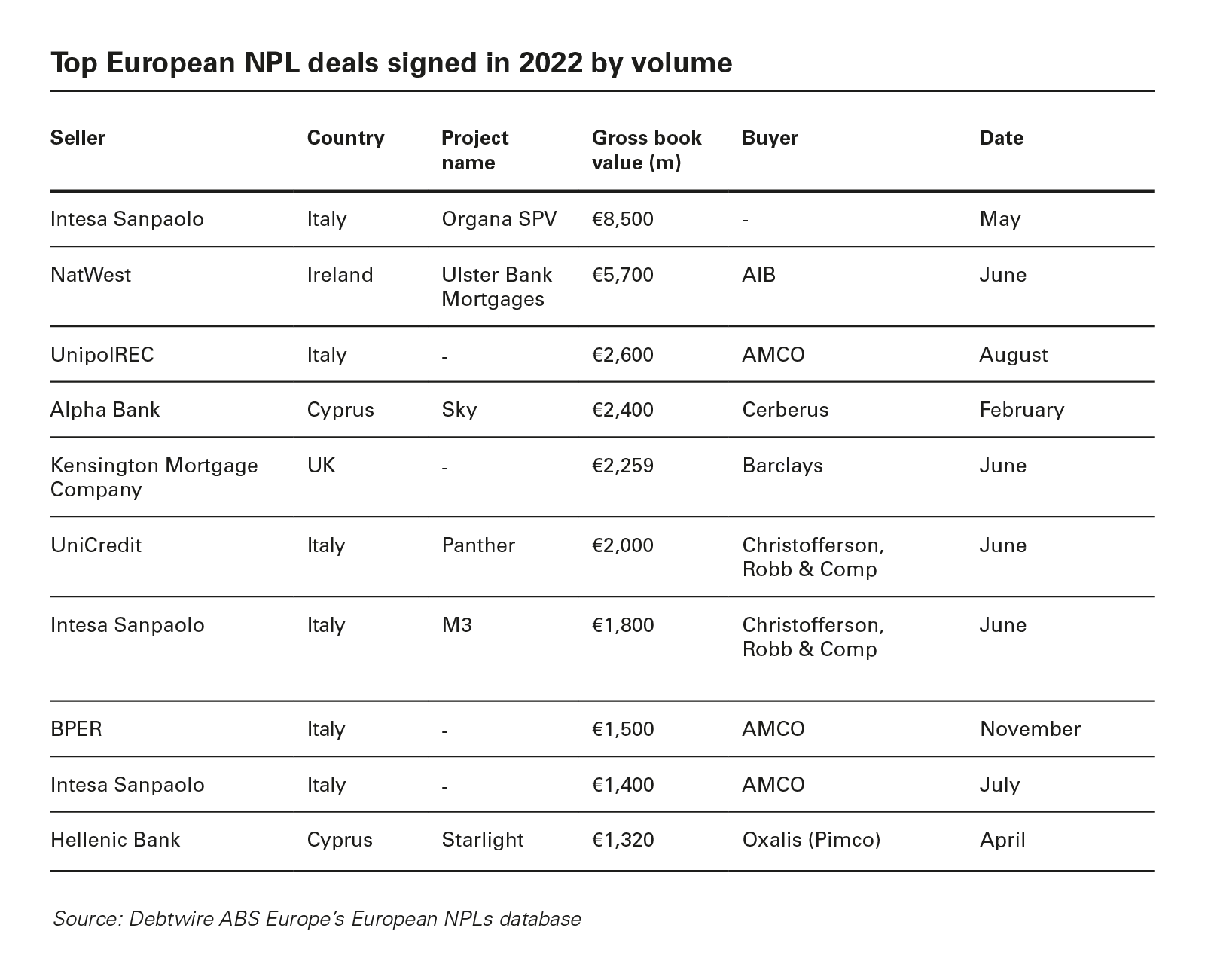

Analysis by Debtwire ABS Europe reveals that Europe's leading banks sold just under €49 billion worth of NPLs and non-core loans in 2022. That figure is significantly lower than the €100 billion of NPL sales recorded in 2021, let alone the peak of more than €200 billion seen in 2018.

For now at least, the primary market for NPLs looks flat at best, with preliminary analysis pointing to a further slowdown in sales in H1 2023. In the short term, a return to the volumes seen between 2015 and 2019, when sales topped €100 billion in four out of five years, seems unlikely.

One reason for the potential slowdown in Italian and Greek NPL securitisation is the withdrawal of state support for banks disposing of bad debts. In Italy, the government had secured a preliminary agreement with the European Union (EU) to renew its Garanzia Cartolarizzazione Sofferenze (GACS) initiative, a similar scheme to HAPS that expired in June 2022, but these plans were put on hold in May 2023. In Greece, the two-phase Hercules Asset Protection Scheme (HAPS), through which the government backed securitisations of banks' NPLs, came to an end last autumn.

However, on 8 July 2023, the Greek finance minister, Kostis Hatzidakis, noted in his address to the plenary session of the Hellenic Parliament during the debate on the government's policy statements that NPL management remains an important challenge and that "the Hercules programme will be used, so that within the framework of the rules set by the EU institutions, any outstanding issues will be addressed, for the benefit, ultimately, of the health of the banking system." Reportedly, the new Hercules programme will include three pending securitisations amounting to €3 billion.

Still, some deleveraging will continue, even if deals are smaller in scale. One possible driver is the EU's 'backstop' regulation, introduced in 2019, which requires banks to back NPLs with 100 per cent core equity within a set time period following their identification (from three to nine years depending on the type of loan). As more NPLs are impacted by this regulation, its significance as a driver of disposals will grow.

One nuance here is that the UK post-Brexit has distanced itself from this European regulation. In March 2023, the Bank of England announced that UK banks would no longer face the same deduction requirements on non-performing exposures. The change could even encourage UK banks to come into the market as NPL investors.

One impact of the changing dynamics of Europe's NPL market is that it has become less attractive to many of the private equity (PE) investors that were previously prominent buyers when banks deleveraged. The rising cost of capital has given many PE investors pause, particularly considering the time and resources required to extract value from NPL portfolios.

This is not to say PE has exited the buyer pool altogether. Last year's deals included high-profile transactions involving the likes of Bain Capital and Cerberus, for example. However, for PE firms lacking specialist servicing platforms, the economics of NPL investment are less compelling. As a result, their appetite to buy NPL portfolios has diminished, and some are even seeking to liquidate existing positions.

By contrast, many of the larger servicing companies remain acquisitive, as they pursue further growth, both as investors and as servicers. Their expertise and experience provide an edge in terms of evaluating new opportunities, as well as to extract more value through improved recovery rates. Firms such as Intrum, Kruk and Axactor account for a growing number of deals on the buyer side.

That said, servicing businesses aren't immune from rising capital costs, particularly as they face the need to refinance debt taken on to fund portfolio acquisition. In some cases, this debt is no longer rated as investment-grade. If NPL recoveries become more difficult in light of the current economic backdrop, the pressure on these firms will increase, impacting their ability to make more acquisitions.

More broadly, these factors are also likely to play into ongoing consolidation in the servicing market, which a handful of large firms now dominate. Banks have continued to spin out their servicing units, even where they have chosen to retain NPLs, and smaller-scale players are increasingly rare.

Many of these themes are also relevant to the secondary market for NPLs, which already accounts for a larger share of overall dealmaking as bank disposals moderate.

Where, for example, PE firms are seeking to exit existing positions, they must find secondary buyers for their NPLs. For larger players looking to deleverage in order to assuage the concerns of the bond market, disposals on the secondary market are one possible strategy. Larger servicing companies are increasingly seeking new strategic solutions for their NPL portfolio investments in order to achieve their deleveraging objectives and improve their financial ratios. Such solutions include the securitisation of back books and the formation of capital partnerships or co-operation agreements for the securitisation of front books. In addition to being a core balance sheet management tool, such securitisation transactions enable the debt collection firms to continue servicing the securitised NPL portfolios.

A related trend is the growing interest in dividing parts of the portfolio for sale to specialist acquirers. Where portfolios were acquired from banks by way of NPL securitisation, this requires taking out single loans or parts of the portfolio from the securitised portfolios. PE investors may no longer be so keen on exposure to NPLs as an asset class in their own right, but a firm with specialist expertise in, say, real estate or the consumer sector, may be interested in buying loans that relate specifically to their area of interest.

Other buyers may also be in this market. For example, Intrum's 2022 sale of Tethys, a portfolio of NPLs relating to Greece's hospitality sector, saw it agree a deal with a consortium of investors including an Israeli hotels company.

These sales of small portfolios, where debt collection firms have organised the NPLs around a particular sectoral or thematic opportunity, conducted some remedial work and built a data room, effectively offer a curated opportunity for specialist buyers. Deals may even include the disposal of single-name debt positions in certain sectors.

Separately, there is also an ebb and flow to NPL transactions. As buyers work through large deals done in the past, they naturally reach the point where a small sub-scale rump of NPLs remains—debt raised to finance the deal may even have been repaid. At that stage, it makes sense to sell to a more specialist investor.

Inevitably, however, buyer demand on the secondary market will be impacted by the performance of NPL portfolios. Here, the data is encouraging—analysis by Morningstar and DBRS suggests NPL transactions that have taken place since the outbreak of the COVID-19 pandemic have performed strongly, with recoveries proceeding at a better rate than expected.

Still, as economic headwinds strengthen, particularly in consumer-facing sectors, such progress may be difficult to maintain. That has the potential to act as a brake on secondary NPL sales.

One factor that certainly supports deals in both the primary and the secondary market is the significant improvement in data quality in the NPL sector. For banks, the regulatory requirements around data management have increased drastically in recent years—NPLs coming on to the market for the first time are therefore backed with much clearer documentation.

Visibility improves

One factor that certainly supports deals in both the primary and the secondary market is the significant improvement in data quality in the NPL sector. For banks, the regulatory requirements around data management have increased drastically in recent years—NPLs coming on to the market for the first time are therefore backed with much clearer documentation. Errors have been eliminated and information gaps closed.

Similarly, secondary buyers are benefitting from the huge amount of work done by debt servicers—both independents and PE-captive platforms—to clean up portfolio data. As they have serviced these loans, they have built substantial data rooms that provide a consistent and reliable source of information.

Such data provides buyers with far greater visibility of potential purchases. Investors with specialist data analytics tools are increasingly using this expertise to secure an edge in the market, generating actionable insight around pricing and potential recovery rates.

Technological advances will provide further opportunities in this regard. Early adopters of machine learning and artificial intelligence tools in the NPL sector claim to have reduced costs by 90 per cent and increased efficiency 20 times over.

Reperforming loans increase

There is another driver of NPL activity that should not be discounted. In some markets, NPL investors report growing numbers of rehabilitated accounts—loans that are once again performing, with borrowers' payments back on schedule. This debt can be put up for sale, with banks often keen to acquire the potentially profitable customer relationship that comes with it.

Regulatory constraints are a factor here—in most markets, regulators do not allow the sale of a rehabilitated loan back to the original lender. Nevertheless, investors are often keen to sell such loans, both to secure a return and to free up resources to focus on their core activity of managing NPLs. Banks looking to grow the customer base provide a potential buyer pool.

The extent to which reperforming loan sales will accelerate is not clear. Slowing economic growth may be an obstacle to rehabilitation—some loans may even slip back into NPL status—but this theme is attracting interest in several markets. Greek businesses, for example, are now performing far more strongly than during the period when many NPL sales were concluded.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: NPL volumes in Europe at end-2022 (€bn-equivalent) (PDF)

View full image: NPL volumes in Europe at end-2022 (€bn-equivalent) (PDF)

View full image: European NPL top sellers in 2022 (€m-equivalent) (PDF)

View full image: European NPL top sellers in 2022 (€m-equivalent) (PDF)

View full image: Top European NPL deals signed in 2022 by volume (PDF)

View full image: Top European NPL deals signed in 2022 by volume (PDF)