At the leading hedge: Europe’s metal recycling and hydrogen push

Europe is turning towards metals recycling as a core component of an industrial hedging strategy around decarbonisation, reshaping its energy security in the process.

9 min read

Solar panels, wind turbines, heat pumps and batteries are all made of metal and—unlike a barrel of oil or ton of coal—metals can be recycled. Countries heavily dependent on imports of crucial decarbonisation minerals are seeking as many sources of supply as possible, and while hedging behaviour is not new in the world of energy security, it is increasingly important for mining & metals markets.

Hedging behaviour is nothing new in the world of energy security, but increasingly important for mining & metals markets. Countries heavily dependent on imports of minerals, metals, and crucial decarbonisation inputs are now seeking as many sources of supply as possible while onshoring more refining and production to minimise the harm of potential interruptions in supply. Solar panels, wind turbines, heat pumps and batteries are made of metal and, unlike a barrel of oil or ton of coal, metals can be recycled. Europe is turning towards metals recycling as a core component of an industrial hedging strategy around decarbonisation, reshaping its energy security in the process.

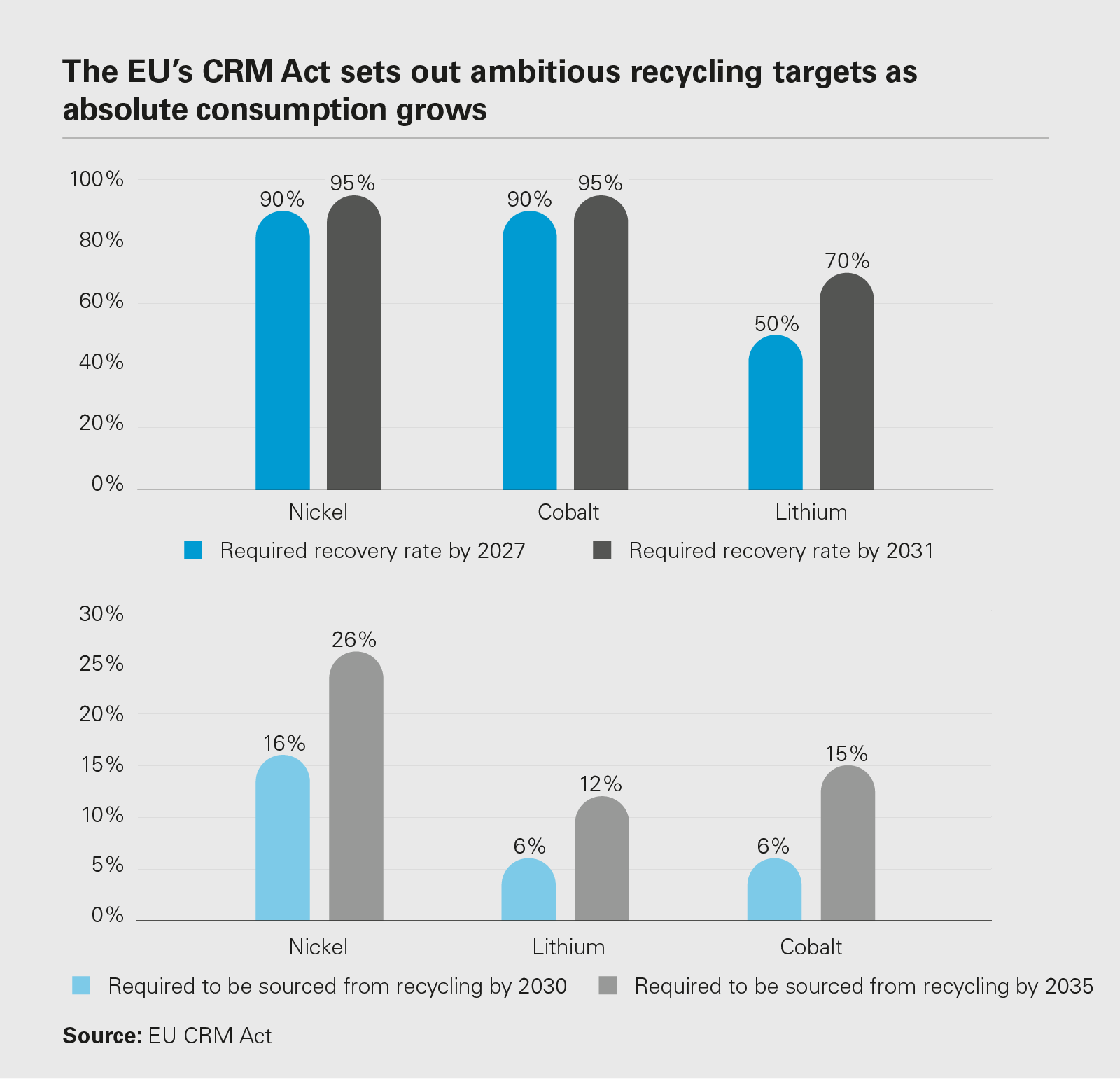

The European Commission's Critical Raw Materials Act (CRM) sets out an ambitious recycling agenda to counter the bloc's over-dependence on supplies of raw and refined strategic materials from China. Specifically, the CRM sets aggressive targets to increase domestic mining, refining and metals production capacities by 2030 to protect energy security. EU projects must account for:

- 10 per cent of annual consumption of extraction

- 40 per cent of annual consumption of processed materials

- 15 per cent of all recycled materials consumed

- And no more than 65 per cent of the EU's annual consumption of any strategic raw material at any stage of production can come from a single third country

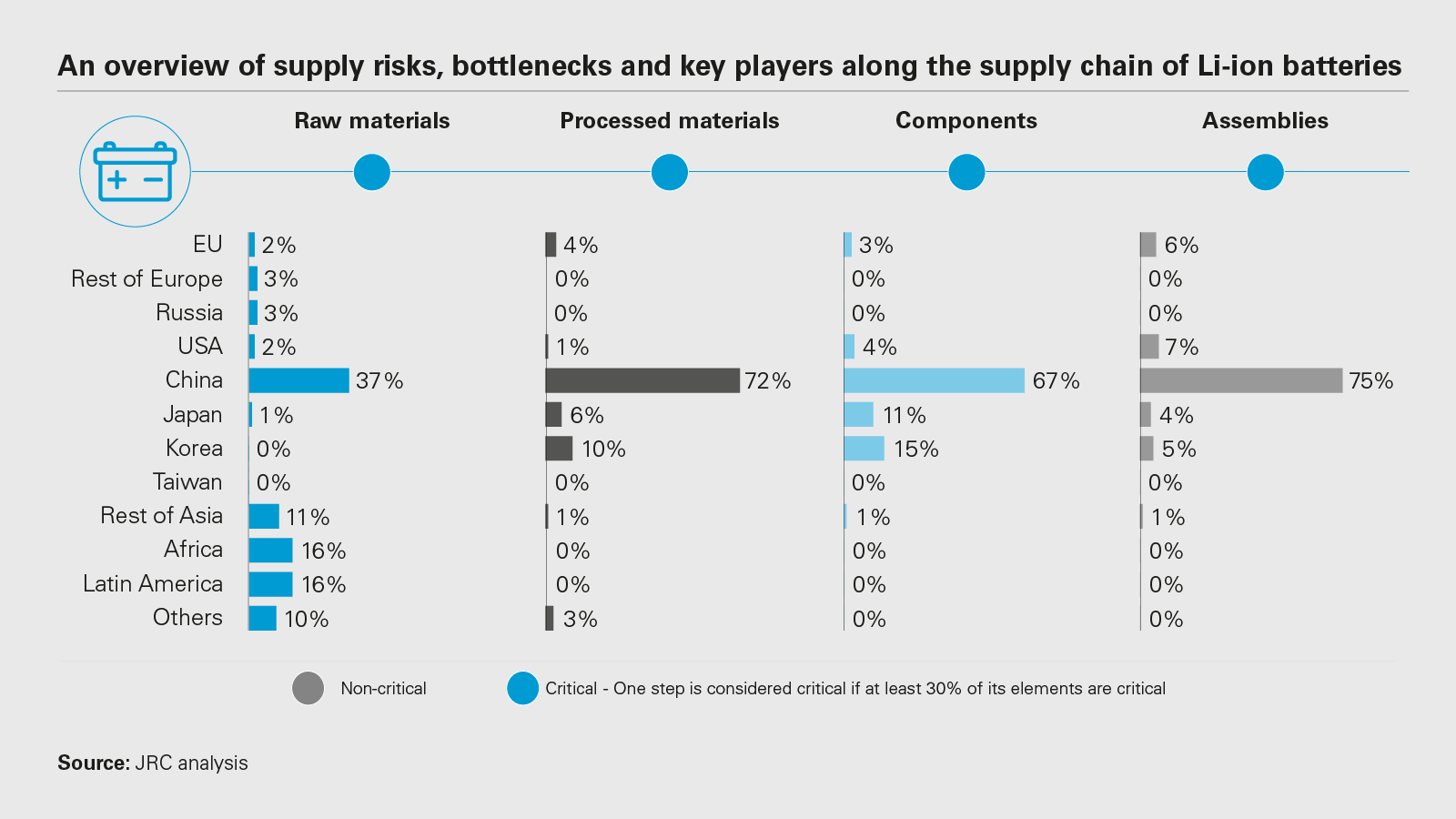

View full image: An overview of supply risks, bottlenecks and key players along the supply chain of Li-ion batteries (PDF)

View full image: An overview of supply risks, bottlenecks and key players along the supply chain of Li-ion batteries (PDF)

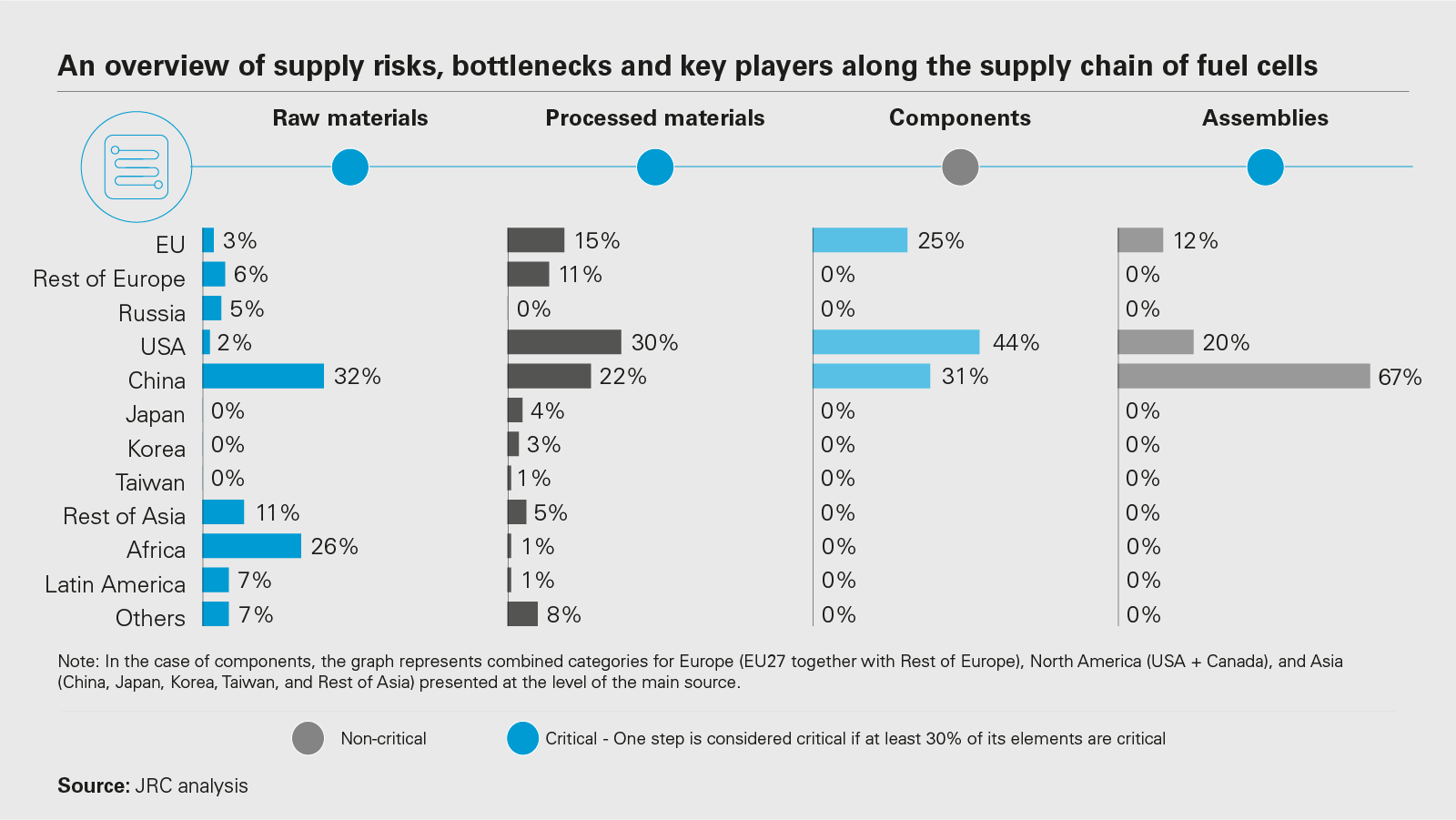

View full image: An overview of supply risks, bottlenecks and key players along the supply chain of fuel cells (PDF)

View full image: An overview of supply risks, bottlenecks and key players along the supply chain of fuel cells (PDF)

Building a market for metals recycling

17.5GW per year

Electrolyser manufacturing capacity of 17.5GW per year is required to achieve annual production of 10 million tons of renewable hydrogen by 2030.

A Joint Declaration committing to increase electrolyser manufacturing capacity ten-fold to 17.5GW per year to meet achieve annual production of 10 million tons of renewable hydrogen by 2030.

The CRM builds on existing standards already shaping investment plans among auto and battery makers. Companies will be required to report their products' entire carbon footprint from mining to production and recycling as early as July 2024, with the eventual aim of setting an EU-wide maximum CO2 limit for each battery produced.

As the regulatory regime mandating recycling expands, so do market incentives to onshore supply chains within Europe. The European Battery Alliance counts more than 35 lithium-ion battery recycling projects underway or in planning, with multiple projects expected to be operational before 2025. Innovative companies such as Vulcan Energy are exploring joint projects utilising geothermal energy production as a means of extracting lithium from brine, then feeding that lithium into a sorption plant and then into a lithium processing plant to ultimately produce lithium hydroxide. The lithium produced will have a negative carbon footprint.

Continuing rollouts of solar PV, wind and battery storage projects across Europe—coupled with regulatory change and concerns around European supply chain and energy security—could also boost manufacturing projects for the key components of these renewable power projects, and further stimulate local demand for raw metals, including from recycled sources. Currently, outside the wind turbine sector, European manufacturing capacity for renewable energy components is limited, and where it does exist, continues to depend on imported components and systems from a limited range of producers, with expansions in manufacturing capacity facing constraints due to complex permitting requirements and shortages of supporting systems. Onshoring or 'friendshoring' production of vital components and systems is part and parcel of ongoing policy initiatives across the EU to localise socially and strategically sensitive supply chains.

View full image: The EU's CRM Act sets out ambitious recycling targets as absolute consumption grows (PDF)

View full image: The EU's CRM Act sets out ambitious recycling targets as absolute consumption grows (PDF)

Rebuilding industrial value chains requires minerals. Historically, supply hedging has meant seeking new sources of supply from which to import energy or other crucial commodities. We are seeing this play out in Europe where national export credit agencies (ECAs) and development finance institutions (DFIs) are looking for mining projects in Africa to expand the supply of copper, nickel, cobalt, lithium and high-grade iron ore needed to meet the demand generated by the energy transition. Reforming permitting processes for mining projects in Europe has also received support. The CRM includes a provision allowing projects deemed strategic to receive permits within two years, a timeline comparable with more competitive mining jurisdictions such as Australia and Canada.

The UK is also in on the act. As part of the UK's national Critical Minerals Strategy announced last year, the British Geological Survey published an initial report for prospective finds on 18 April 2023. Exploration works at specific sites are expected to follow in the year ahead to determine the viability of projects. Efforts to restart projects such as Tungsten West's Hemerdon tungsten and tin mine, and similar projects that have stalled continue. Though the UK has not announced a large package of subsidies, efforts are being made to coordinate policies, R&D and knowledge sharing, and investment with Canada and Australia.

What is novel about these initiatives is that onshoring and friendshoring are being coupled with recycling to provide an additional hedge against supply shocks. Recycling allows countries with limited domestic resources and comparatively high standards for ESG or similar requirements to reduce pressure on upstream investments. Circular economies mitigate security risks, especially in Europe where energy security has become far more salient in the past two years.

The relatively short average design life of 20 to 30 years for a wind turbine or solar PV panel, and a considerably shorter life for a battery energy storage system, means that increased deployment of renewable technologies not only creates an increased demand for metals and potential local manufacturing. It also creates another steady and growing stream of locally available feedstock for metal recycling projects in Europe.

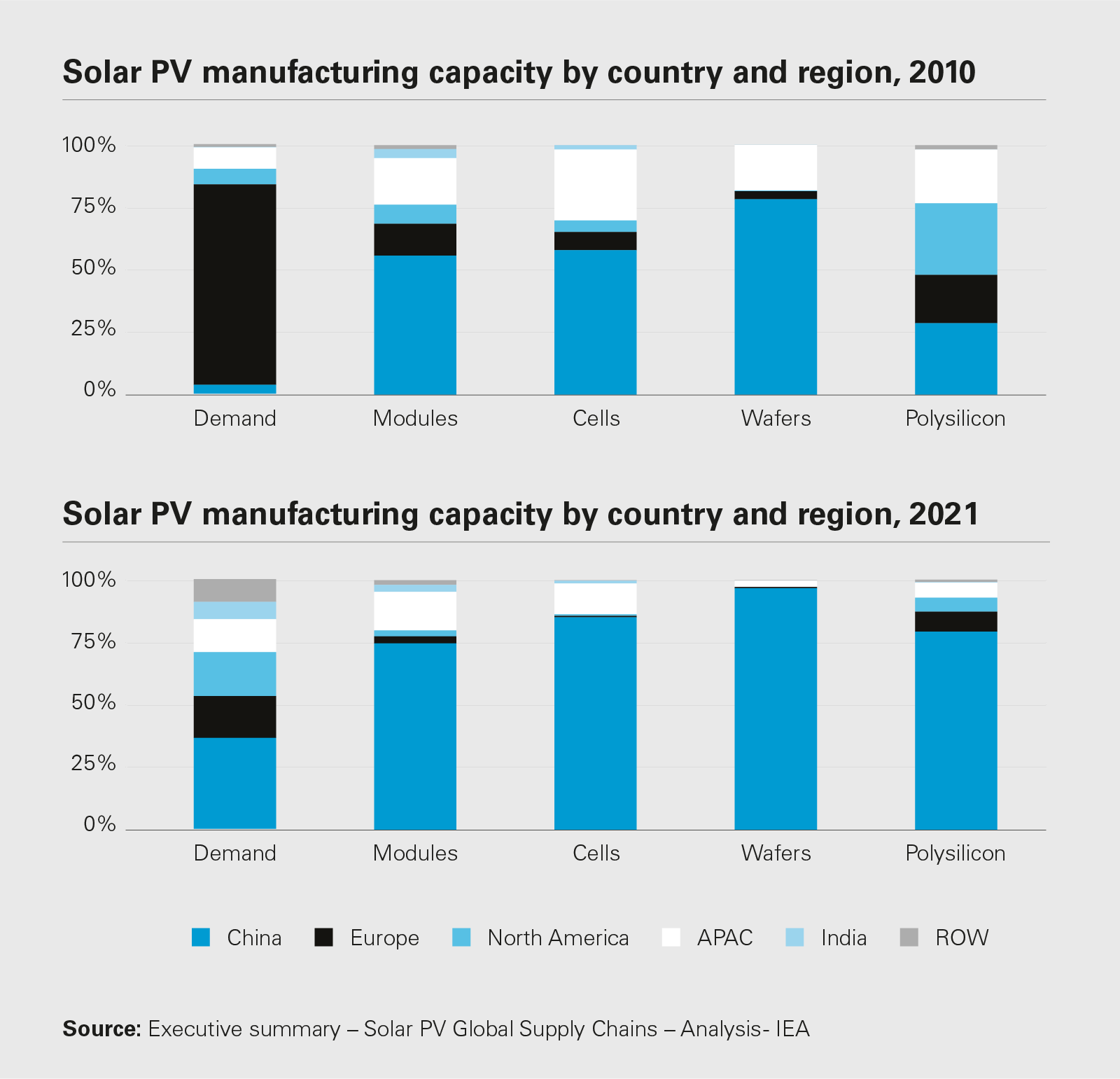

View full image: Solar PV manufacturing capacity by country and region, 2010 (PDF)

View full image: Solar PV manufacturing capacity by country and region, 2010 (PDF)

Hydrogen and recycling

Onshoring and friendshoring are being coupled with recycling to provide an additional hedge against supply shocks allowing countries with limited domestic resources and comparatively high ESG standards to reduce pressure on upstream investments

Metal recycling provides an opportunity to help meet rising demand for metals, while creating a more circular and resilient European based metal supply chain

The implications for recycling go beyond batteries to include broader industrial supply chains consuming metals of all kinds. The passage of the Inflation Reduction Act has added an additional urgency for metals end-users and metallurgical firms in Europe that are worried they may be left behind in the race to commercialise hydrogen at scale and reduce emissions from metals production that account for roughly ten per cent of global CO2 emissions in any given year.

The EU currently leads the market for hydrogen electrolyser components and assembly, and is well placed to contribute to the roll out of hydrogen powered industrial processes, both in Europe and globally. On 5 May 2022, European Commissioner for the Internal Market Thierry Breton met with 20 CEOs from electrolyser manufacturers to sign a Joint Declaration committing to increase electrolyser manufacturing capacity ten-fold to 17.5GW per year to achieve annual production of 10 million tons of renewable hydrogen by 2030. Metal Focus estimates that PGM demand from the hydrogen sector will eclipse 100,000 oz in 2023, effectively doubling demand from last year. When scrap metals are recycled, they typically go through several stages: Metals are first separated; then crushed and placed into bales, shredded, chemically decoated, melted down; and then recast. Each stage of the process is energy-intensive, and melting and casting normally drive most emissions from the use of coking coal or natural gas to heat or power furnaces. Replacing coking coal and natural gas with green hydrogen would considerably lower the CO2 emissions generated during the metal recycling process, giving recycled metals an additional advantage in carbon regulated markets.

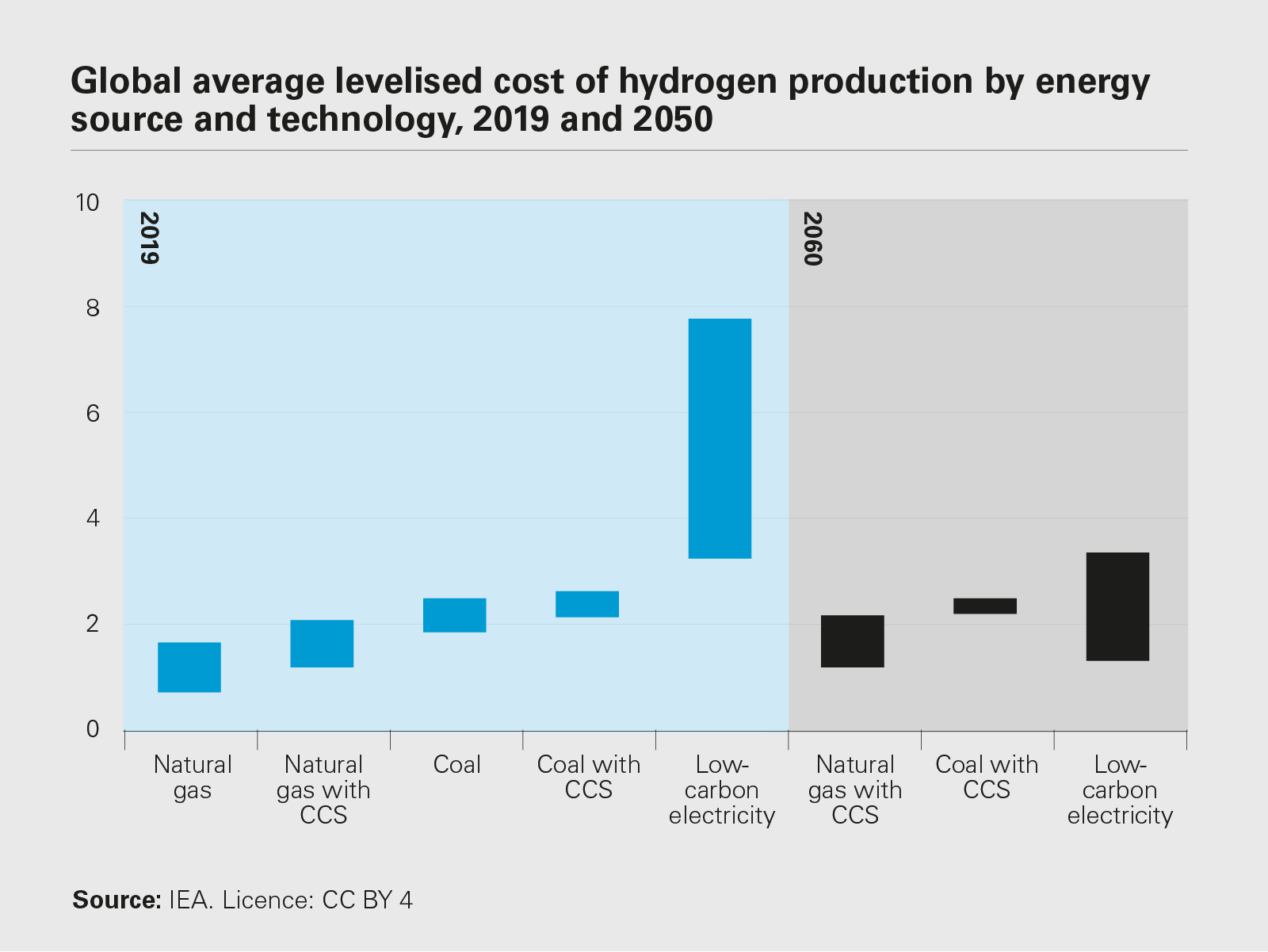

Cost competitiveness against natural gas remains the sticking point for green hydrogen as a feedstock or power source for milling and recycling operations. Estimates of levelised costs for green hydrogen production typically range from USD$3 to US$7 per kg, whereas natural gas is typically just US$0.70 to US$1.20 per kg. The cost of acquiring and installing electrolysers and the cost of renewable electricity required to create green hydrogen are the main culprits for green hydrogen's higher cost base. But they are expected to fall in time, boosted by the relative increase in natural gas prices since 2021.

56 per cent of steel in the EU is already made from scrap, 51 per cent of aluminium is made from recycled materials, and roughly 50 per cent of copper is recycled as well. Figures for nickel depend on its end-use, but are comparable. Mandating an increase in the use of recycled content for all types of metals as well as batteries will create new opportunities to shape circular supply chains that reduce producers' exposure to external inputs, give them greater control over their Scope 2 and 3 emissions, and allow them to meet more rigorous ESG targets.

Recycling and green metals production are also affecting competition law. The European Commission took Hydro's takeover of Polish recycler Alumetal into an in-depth Phase II review because of concerns that the deal could have a negative impact on the competitive landscape for green aluminium products for European automotive customers. The Commission made particular note of Alumetal's importance as a competitive force with strong growth potential for the supply of advanced foundry alloys made from recycled aluminium, a crucial input to produce vehicles that are more fuel-efficient and emit less. Antitrust analyses now must take account of the green credentials and lower emissions of recycled metals.

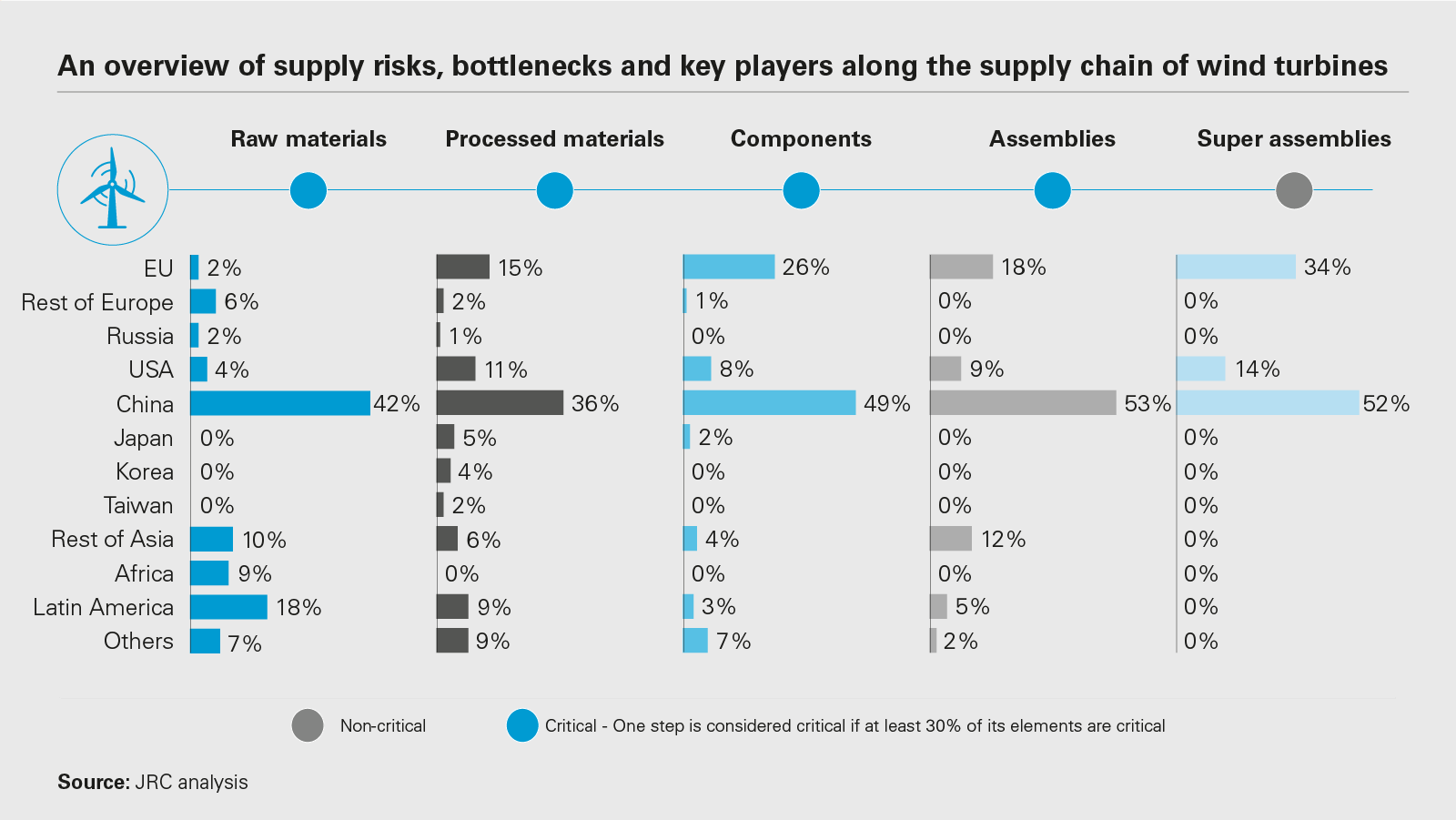

View full image: An overview of supply risks, bottlenecks and key players along the supply chain of wind turbines (PDF)

View full image: An overview of supply risks, bottlenecks and key players along the supply chain of wind turbines (PDF)

View full image: Global average levelised cost of hydrogen production by energy source and technology, 2019 and 2050 (PDF)

View full image: Global average levelised cost of hydrogen production by energy source and technology, 2019 and 2050 (PDF)

Going for platinum

Meeting the steep demands of decarbonisation and improving Europe's supply chain and energy security will require increases in the consumption of critical minerals. Just as batteries and electrified vehicles require large volumes of nickel, copper, cobalt, and lithium, hydrogen electrolysers require graphite, zirconium, platinum, strontium, gold-plated copper, and the incredibly rare metal iridium. Wind turbines also require material quantities of steel, copper, zinc, nickel and rare earths. Solar PV panels are also currently a significant consumer of global silver production. Metal recycling provides an opportunity to help meet this rising demand for metals, while creating a more circular and resilient European based metal supply chain.

The challenges posed by energy security amid decarbonisation are not fundamentally different to supply chain considerations forged during the fossil fuel era. Faced with rising demand for metals, one has three options: Find more supply; consume less; or substitute existing demand. European governments, miners, metals firms and manufacturers are now figuring out how to do all three—and quickly.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2023 White & Case LLP