Mining & metals 2021: Forces of transition and influencers of change

What's inside

The mining & metals industry is critical to the success of the world's transition towards net zero, both in reducing its own carbon footprint and providing the materials that will deliver a cleaner and more sustainable future

The mining & metals sector is enjoying renewed global macro-economic prominence, with the minerals and metals it produces—and, increasingly, recycles—being critical to the success of the world's energy transition toward a low-carbon future.

The resilience of the sector and of commodity prices throughout the COVID-19 pandemic, coupled with growing investor and consumer excitement about energy transition materials, has lured generalist investors toward the sector for the first time in years, turning the tide on the ESG concerns and lackluster returns that had previously worked against generalist investor sentiment.

The ESG agenda has undoubtedly been a major driver of change in recent times, and the expectations bar is continuously being raised by investors, governments, communities, consumers and other stakeholders. There is tremendous opportunity for industry players to embed an ESG and low-carbon culture—capturing both risks and opportunities—into their corporate strategies in order to build stakeholder trust, focus on ESG/low-carbon-compatible business lines and generate truly sustainable growth.

In the lead-up to COP-26, in this Insight series from the White & Case Global Mining & Metals team, we examine some of the major forces of transition in the global mining & metals sector, digging into those people, products, policies and institutions that are at the forefront of influencing change in our sector.

Taking ESG seriously: The crucial role of mining investors in the energy transition

Taking ESG matters seriously improves business performance; ESG best practice must become integral to the business and should be a "given" in any mining project.

As governments around the world are pursuing revised mining fiscal policies and more aggressive enforcement, investors need to prepare themselves for an active period of resource nationalism.

Investors are returning to mining & metals amid an almost unprecedented rally in the US capital markets that is taking place despite the continued economic challenges related to the COVID-19 pandemic

Key considerations around bribery and corruption risks, as the mining & metals sector is gaining critical momentum in the world's energy transition toward a low-carbon future.

EVs are expected to account for at least 7 percent of the global road vehicle fleet in 2030

Platinum group metals (PGMs) have been the main contributor to a major uplift in Southern African mining production in 2021—the biggest bounce in six years after disruption caused by the pandemic and a significant production decrease in 2020.

The recovery coincides with the transition by automotive manufacturers from combustion engines to electric vehicles. It may have been expected that this would risk the loss of a powerful driver of demand for the Southern African PGM. But in a reversal of fortunes, PGMs are helping to ensure that the region remains relevant and is contributing to the global clean and green transition.

Along with a price boom, there seems to be a new wave of investment interest in PGMs, but this relies, to a large extent, on demand-side stability.

Demand drivers and supply constraints

Among the rarest metals on earth, PGMs, which include platinum, palladium, rhodium, ruthenium, iridium and osmium, are well known for their catalytic properties. This makes them resistant to corrosion, wear and tarnish, and gives them excellent high-temperature characteristics, high mechanical strength, good ductility and stable electrical properties.

A significant driving force behind the PGM boom is the automotive sector. With 78 million cars being produced in 2020, the need for autocatalysts and the PGMs used to make them is significant. The more stringent emissions regulations that have been put in place in Europe, China and India—driving the increase in the use of autocatalysts in vehicles—have started to impact the subsequent demand for PGMs.

Ultimately, the expected growth in battery electric vehicles (EVs), which do not use autocatalysts, may result in some reduction in demand for PGMs. However, this transition will take time and, during the transition phase, combustion engine vehicle emissions are expected to become even more heavily regulated by governments worldwide.

Approximately three million EVs were sold in 2020, representing less than 5 percent of global sales. EVs are expected to account for at least 7 percent of the global road vehicle fleet in 2030, showing continuing strong demand in more traditional modes of transport.

While current demand hinges on autocatalysts, PGMs are making rapid progress in the new end-use sectors of the hydrogen economy: fuel cells; lithium batteries; low-loss computing; and food technology.

Their particular combination of chemical and physical properties makes PGMs valuable to the end-market for a range of industrial, medical and electronic applications —not just for investment but for real, functional use. In many of their applications, substitutes for PGMs are either not feasible or are considered to be inferior in performance. As such, demand for PGMs is expected to continue even as prices rise.

Fuel cell technologies are also becoming increasingly prominent across many sectors, including transport, as part of the global push to improve air quality and reduce global warming. Additionally, the anticipated growth in demand for electrolysis capacity to produce green hydrogen presents significant demand potential in the longer term. Together with the use of platinum in automotive fuel cells, PGMs will play a key role in the hydrogen economy and therefore contribute to the energy transition process.

With environmental stewardship identified as one of the main sources of sustained demand, PGMs will form a significant part of the conversation as green energy metals of the future at the UN Climate Change Conference in November, alongside lithium, cobalt and copper.

Despite this increased demand, there are considerable factors that are limiting PGM supply. While new projects have been announced and will hopefully come online, the process is slow and the funding environment risk-averse, even amid soaring commodity prices. According to the World Platinum Investment Council, 2021 will be the third consecutive year with a deficit in supply. Supply is projected to be broadly flat for the next three to four years, resulting in continued expectations around buoyant pricing.

In addition, Johnson Matthey's latest PGMs Market Report notes that the palladium and rhodium markets will remain in deficit, despite all-time-high prices being recorded, with palladium climbing above US$3,000 per ounce and rhodium repeatedly surging to US$30,000 earlier this year.

According to the report, mining alone will not produce enough supply of PGMs to meet demand— approximately 25 percent of supply is from recycled materials— which may in turn drive prices even higher.

US$3,000

Price for palladium climbed above US$3,000 per ounce earlier in 2021

Implications for the Southern Africa mining sector

This growth has significant implications for the Southern Africa mining sector, which accounts for more than 60 percent of world PGM production. Russia produces a further 26 percent, and most of the rest comes from Canada and the US.

In particular, South Africa produces more than 80 percent of the world's platinum, more than 30 percent of the world's palladium (Russia accounts for about 45 percent) and approximately 80 percent of the world's rhodium.

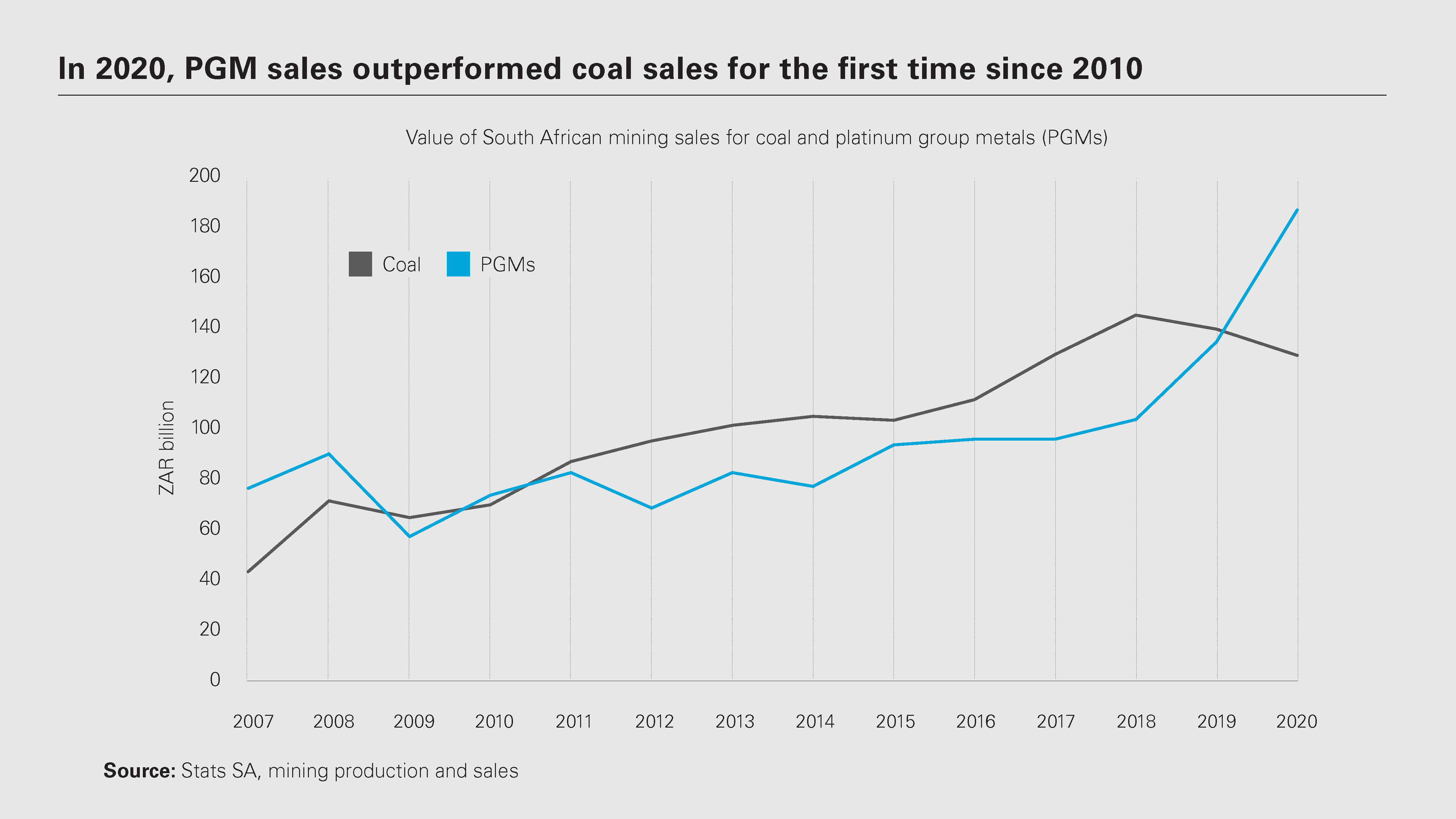

For the first time since 2010, PGMs overtook coal as the most significant contributor to mining-industry revenue in South Africa, reaching ZAR 190 billion last year. Their performance continues to surge in 2021.

Mineral sales for March 2021 in South Africa reached a record ZAR 75 billion, with 41 percent of that generated by PGMs according to the latest data, while platinum supply for Zimbabwe in Q1 2021 showed 11 percent growth compared to the same period in 2020. Additionally, the Zimbabwe Statistics Agency reported that PGM exports for March 2021 increased by 202 percent to US$168.9 million—their highest export earning since 2009.

This uptick has translated into real opportunities for Southern African PGM miners, especially those that have been highly acquisitive during the last two years and focused on geographic diversification. While recycling from secondary markets is an attractive alternative, platinum producer Implats has suggested there will be a shift back to the South African production base, which will enable the PGM majors to capitalize on continuing strong demand.

Helping to drive this demand are new products such as PGM exchange-traded funds or novel investment products such as Norilsk's Global Palladium Fund, showing how investors are looking for different ways to obtain PGMs' physical and derivative exposure.

All of these conditions, together with the push toward a hydrogen economy, make for a positive and exciting outlook for a sector that might otherwise have struggled to find its place amid the expected rise of EVs. With automotive manufacturers and other end-users of PGMs being increasingly focused on the ESG performance of their entire supply chains, and debt and equity investors continuously raising the bar in the ESG realm too, the sector is well positioned to capture future investment, especially as the global economic recovery gathers pace.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: In 2020, PGM sales outperformed coal sales for the first time since 2010 (PDF)

View full image: In 2020, PGM sales outperformed coal sales for the first time since 2010 (PDF)