Mining & metals 2021: Forces of transition and influencers of change

What's inside

The mining & metals industry is critical to the success of the world's transition towards net zero, both in reducing its own carbon footprint and providing the materials that will deliver a cleaner and more sustainable future

The mining & metals sector is enjoying renewed global macro-economic prominence, with the minerals and metals it produces—and, increasingly, recycles—being critical to the success of the world's energy transition toward a low-carbon future.

The resilience of the sector and of commodity prices throughout the COVID-19 pandemic, coupled with growing investor and consumer excitement about energy transition materials, has lured generalist investors toward the sector for the first time in years, turning the tide on the ESG concerns and lackluster returns that had previously worked against generalist investor sentiment.

The ESG agenda has undoubtedly been a major driver of change in recent times, and the expectations bar is continuously being raised by investors, governments, communities, consumers and other stakeholders. There is tremendous opportunity for industry players to embed an ESG and low-carbon culture—capturing both risks and opportunities—into their corporate strategies in order to build stakeholder trust, focus on ESG/low-carbon-compatible business lines and generate truly sustainable growth.

In the lead-up to COP-26, in this Insight series from the White & Case Global Mining & Metals team, we examine some of the major forces of transition in the global mining & metals sector, digging into those people, products, policies and institutions that are at the forefront of influencing change in our sector.

Taking ESG seriously: The crucial role of mining investors in the energy transition

Taking ESG matters seriously improves business performance; ESG best practice must become integral to the business and should be a "given" in any mining project.

As governments around the world are pursuing revised mining fiscal policies and more aggressive enforcement, investors need to prepare themselves for an active period of resource nationalism.

Investors are returning to mining & metals amid an almost unprecedented rally in the US capital markets that is taking place despite the continued economic challenges related to the COVID-19 pandemic

Key considerations around bribery and corruption risks, as the mining & metals sector is gaining critical momentum in the world's energy transition toward a low-carbon future.

A new wave of resource nationalism in the mining & metals industry

As governments around the world are pursuing revised mining fiscal policies and more aggressive enforcement, investors need to prepare themselves for an active period of resource nationalism.

Countries across the world are asserting new fiscal demands on investors in the mining sector

Analysts are predicting the advent of a new commodity super-cycle, powered by the economic recovery and the energy transition narrative. The mining & metals industry may be facing a renewed period of intense resource nationalism.

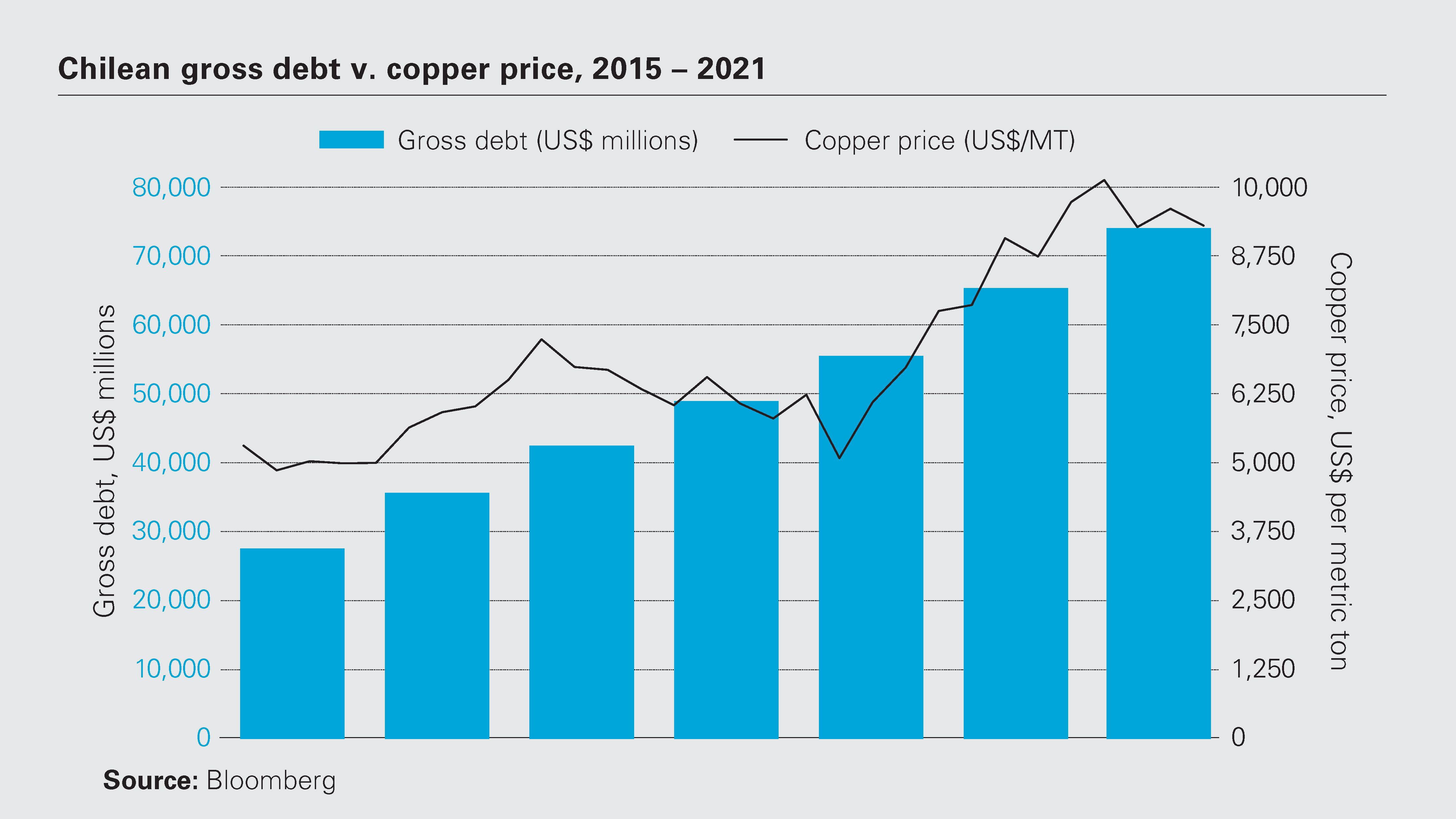

Facing gaping budget deficits in the wake of the COVID-19 pandemic, and stoked by soaring commodity prices, resource-rich countries are bound to demand more from investors in the sector. In fact, 2021 has already seen a flurry of proposed and actual fiscal measures, with governments around the world pursuing revised mining fiscal policies and more aggressive enforcement.

The factors supporting this trend show no sign of abating in the near term. For governments, the challenge will be to develop a sustainable fiscal regime that will help increase revenues when prices are high without discouraging investment in the sector, investors, for their part, need to prepare themselves for an active period of resource nationalism.

In Chile, investors could face a tax burden of 82 percent in royalties and taxes under the proposed bill on sales exceeding 12,000 tons annually of copper and 50,000 tons per year of lithium, up from 40.3 percent.

A predictable trend

The current trend is the result of the conjunction of two powerful factors.

The first factor is the upswing in commodity prices. Relative to most sectors, the mining industry has weathered the global economic downturn well. Commodity prices— especially copper, iron ore, silver and gold—have either remained high or increased dramatically.

The recession brought about by the pandemic drove gold prices to new heights, although the market has since softened. Industrial metals have been buoyed by government stimulus and deficit and infrastructure spending. Critically, the push for green energy and electrification has seen copper prices rise to their highest levels in years, while the demand for battery metals such as nickel, lithium and cobalt has surged.

The second powerful factor supporting the current trend is the fiscal crunch that many countries are facing. While governments typically respond to rising commodities prices with increased taxes, the case for increased taxation today is more pressing, as governments across the world have abandoned fiscal caution and spent freely to support their economies.

The result is predictable. With the prices of some commodities cyclically high, cash-strapped governments are bound to demand, in one way or another, a larger share of mineral wealth. The signs of an emerging wave of resource nationalism are already clear.

The challenge will be to craft sustainable fiscal policies that can move with the commodities cycle, grow the tax base with new projects and provide the certainty that the industry needs

Cashing in on copper

The copper-producing nations in Latin America are at the forefront of this trend. On May 6, 2021, Chile's Chamber of Deputies, the lower house of Congress, passed a bill to introduce a new royalty on copper and lithium sales.

Chile currently taxes most mining operations on a flat-fee basis, under agreements that are due to expire in 2023. The new bill proposes a 3 percent base rate royalty. For copper, a windfall profit tax would begin at marginal rates of 15 percent of sales priced at US$2 to US$2.5 per lb, rising to 75 percent of additional income on sales of more than US$4 per lb.

It is estimated that investors would face a tax burden of 82 percent in royalties and taxes under the proposed bill on sales exceeding 12,000 tons annually of copper and 50,000 tons per year of lithium, up from 40.3 percent.

According to the president of industry body Sonami, Diego Hernández, the new legislation would force 12 of the 15 biggest miners in Chile to operate at a loss. While the bill is yet to be approved in the Senate, some companies already appear to be reassessing their investment decisions.

For example, Lundin Mining, which operates one of the largest copper mines in Chile, is reportedly reconsidering its plans for a US$600 million expansion of its Candelaria mining complex in favor of a project in Argentina.

The Chilean developments have been echoed by other governments across the region. In June 2021, Peruvians elected the leader of the left-wing Free Peru party, Pedro Castillo, as president. As a candidate, Castillo endorsed plans to impose increased taxes on mining profits, drawing inspiration from Chile. Although Castillo said he did not intend to nationalize mining projects, he made clear that he would seek to tax mineral profits to fund social spending.

Some in the industry hope the new government will moderate its positions in office, but the global trend towards more aggressive fiscal policies is reason for caution.

0.75%

The US state of Nevada approved a proposal to add a 0.75 percent excise tax on gold and silver miners reporting gross revenue of between US$20 million and US$150 million

A raft of regulatory reforms

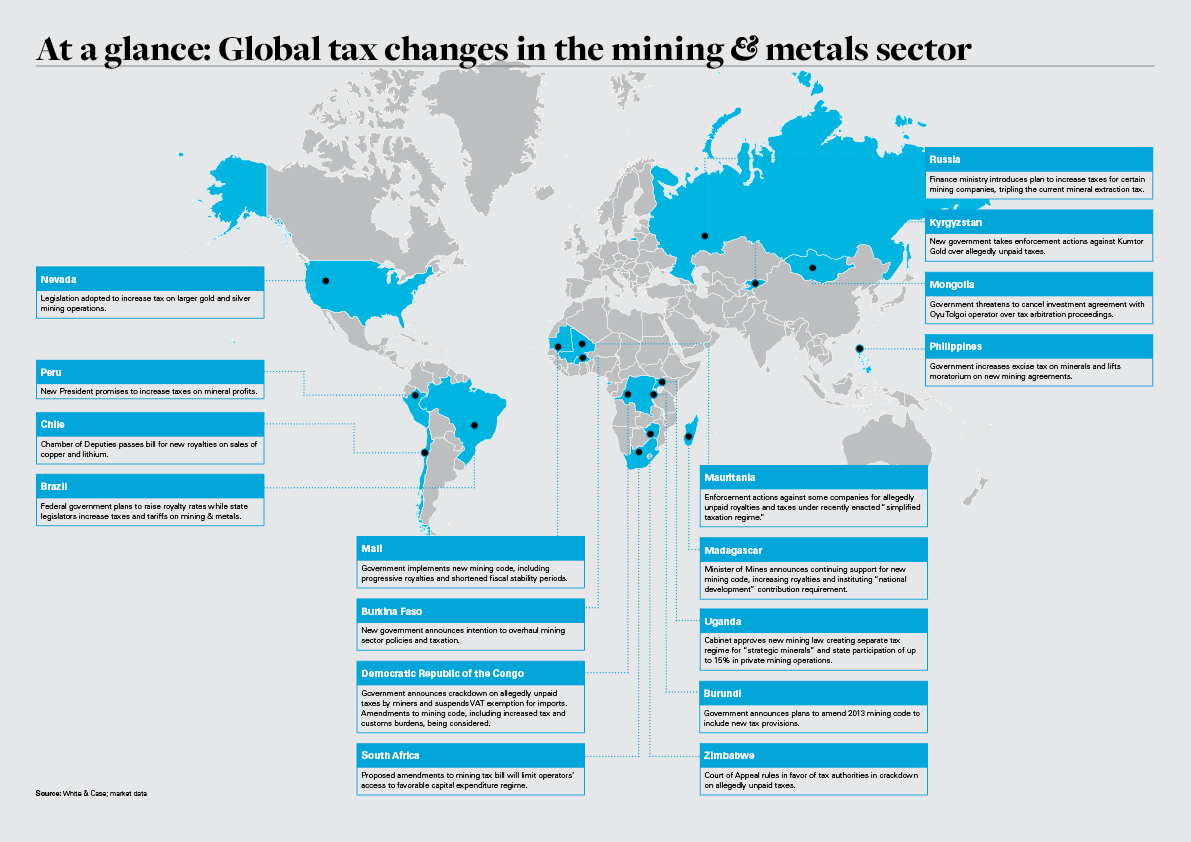

The trend is not limited to Latin America. From Burkina Faso to Zambia, and from Mongolia to the Philippines, countries across Africa and Asia-Pacific are asserting new fiscal demands on investors in the mining sector. These have taken the form of proposed windfall and profit taxes, higher excise taxes and stepped-up royalty rates, or simply more aggressive enforcement.

On May 13, 2021, Madagascar's mining minister, Fidiniavo Ravokatra, renewed his push for an overhaul of the country's mining code. Key proposed provisions include increased royalties—from 2 percent to 4 percent for base metals, gold and silver, and up to 8 percent for raw precious stones and raw fine gemstones—and the allocation of 20 percent of mining production to the state.

While the industry has been vocal in its opposition and the move was previously opposed by the presidency, the divergence between commodity prices and fiscal revenues is fueling the case for reform.

Many measures have been passed at a local level. In Brazil, while the federal government is considering raising taxes on the mining sector, in April 2021, the northern state of Pará instituted an increased tariff on iron ore, copper, manganese and nickel production.

The trend is not limited to emerging markets. On June 1, 2021, the US state of Nevada approved a proposal to add a 0.75 percent excise tax on gold and silver miners reporting gross revenue of between US$20 million and US$150 million, and a 1.1 percent tax on those grossing any higher.

In many jurisdictions, investors are also facing stepped-up enforcement of existing tax legislation. In May 2021, the Democratic Republic of the Congo announced it would clamp down on companies that it alleges have paid incorrect amounts of tax, demanding very large adjustments.

Meanwhile Kyrgyzstan's State Tax Service revived tax claims it had previously terminated against Centerra Gold for the period 2011 to 2017. A few weeks later, Kyrgyzstan took over Centerra's flagship Kumtor gold mine. Elsewhere, copper producer First Quantum Minerals is embroiled in international arbitration proceedings with both Zambia and Mauritania over disputed royalties and taxes.

4%

Madagascar proposed new provisions to the country's mining code, including an increase in royalties from two to four percent for base metals, gold and silver

Whether the legislative measures currently contemplated in Chile and elsewhere are ultimately adopted, the direction of travel is clear. Increased fiscal pressure on mining projects is bound to materialize in one form or another, whether through new taxes or the aggressive enforcement of existing ones.

While high commodity prices may initially cushion the impact on projects, governments need to achieve the right balance of increasing revenues without stifling investment. The challenge will be to craft sustainable fiscal policies that can move with the commodities cycle, grow the tax base with new projects and provide the certainty that the industry needs.

Sadly, there is a distinct possibility that, just as in previous cycles, some governments will fall prey to nationalist politics and overreach, threatening project economics and future investments.

In this environment, mining investors would be well advised to assess their positions. In particular, investors should carefully assess the contractual arrangements under which projects are being carried out.

Fiscal stability agreements will prove invaluable. These agreements are ordinarily enforceable through local courts or international arbitration and also provide useful leverage in negotiations with fiscal authorities.

In the current environment, projects that benefit from stability agreements are more attractive. Sponsors of new projects should put a premium on securing stability agreements, and operators of existing projects that benefit from such agreements should be extra-cautious not to allow them to lapse.

Beyond contractual protections, investors should also reassess project holding structures to ensure the best available investment treaty coverage for their foreign assets. Investment treaties provide broad protections to foreign investors, but not all treaties are created equal.

For example, some treaties carve out taxation measures, leaving investors with limited protection in the face of mounting fiscal pressure. Sophisticated investors increasingly plan their investment structures with a view to benefiting from optimum investment treaty protections. Many treaties do not include substance requirements, allowing investors to acquire protections through the simple addition of special purpose vehicles in their holding structures.

While "treaty planning" is generally permitted, it must ordinarily take place before adverse measures are adopted by host governments. With the signs of a new wave of resource nationalism already here, the time is now for investors to make sure that their house is in order.

Taha Wiheba (White & Case, Law Clerk, New York) contributed to the development of this publication.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: Chilean gross debt v. copper price, 2015 – 2021 (PDF)

View full image: Chilean gross debt v. copper price, 2015 – 2021 (PDF)

View full image: At a glance: Global tax changes in the mining & metals sector (PDF)

View full image: At a glance: Global tax changes in the mining & metals sector (PDF)