Cybersecurity: Legal implications and risk management

What's inside

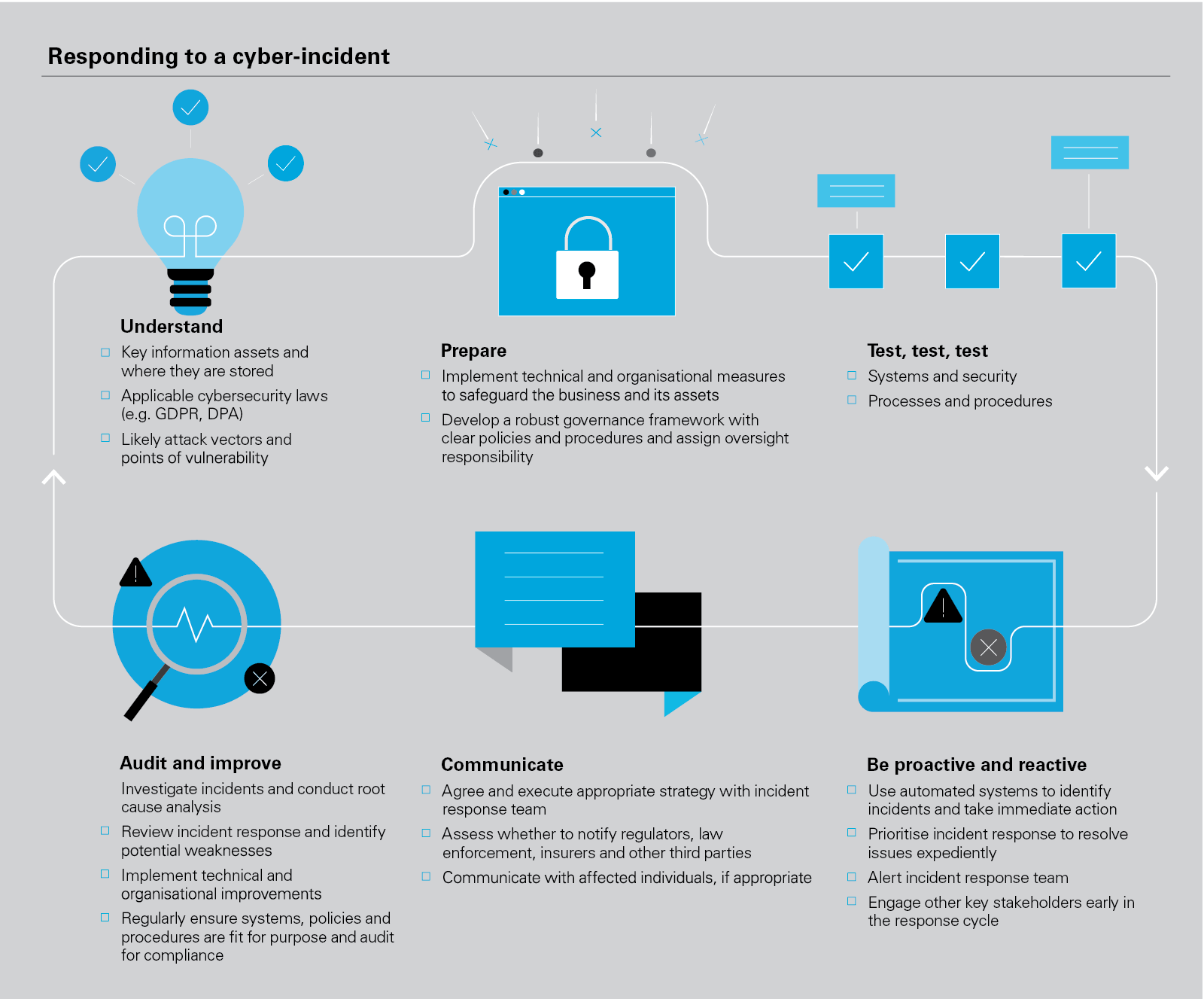

In an increasingly interconnected world, cyber risk is firmly at the top of the boardroom agenda, and having an effective data breach response programme is no longer optional.

Cybersecurity crisis management

The internet knows no borders, neither do we. Our global team of cybersecurity response experts work across borders, combining data protection, privacy, regulatory, white collar and litigation expertise in order to deliver seamless crisis management and legal advice, whenever and wherever needed.

The digitalization and free flow of information has transformed global business. However, with increased opportunities have come new and increased risks, together with complex legislative regimes that can vary significantly by jurisdiction, and are constantly evolving. Even the most conscientious company can become the victim of a cybersecurity incident, such as the stealing of client or company information, or a ransomware attack. We work with a wide range of multinational companies to manage their cybersecurity risks, developing rapid response plans, providing time-critical crisis management advice, and working with clients to manage any resulting legal issues that may arise.

Key issues

Why?

Reputation

Fines

Breach of contract

M&A due diligence

Insurance

Proprietary information

Litigation

Criminal offences

Negligence

Be prepared

Risk Assessment

Key Information

Assets

Key Systems

Threat Analysis

Security Measures

Toolkit

Scripts

Internal and

External

Communications

Employee contacts

Response Plan

Live Training

Business Continuity Plan

Key considerations

Customer/individual rights

Requests for data

Data Protection Authority Complaints

Group litigation orders

Resolution mechanisms

B2B relationships

Contractual obligations

Contractual liability

Tort

Reputationmanagement

Media strategy

Customer interaction

Employee engagement

Commercial

Proprietary

Information/Trade Secrets

System Disruption

Regulatory issues

Data Protection Authority

Financial Regulators

Market authorities

Other regulators

Privacy & data protection

Jurisdictions involved

Reporting obligations

individuals

authorities

Evidence

Law Enforcement Involvement

Legal Privilege

Preservation of Evidence

Response

Crisis Team

Legal (internal and external)

IT/IT Forensics

PR

Regulatory

DPO

Executive committee

HR

Vendor manager

Key Actions

Work with forensic investigators to:

Identify and contain breach

Gather/preserve evidence

Maximise legal privilege coverage

Contact crisis team

Bring in external partners

Identify key risks and priorities based on nature of breach

Assess notification requirements

Communications

Regulatory notifications

Articles

2025

Reform to the UK’s cybersecurity regime incoming

Changes are coming to the UK’s cybersecurity legal landscape. The new Cyber Security and Resilience (Network and Information Systems) Bill aims to expand legal requirements to more sectors, tighten incident reporting rules, give the Government stronger powers to tackle cyber threats, and ramp up fines for serious breaches.

Member States were required to implement the NIS 2 Directive ("NIS 2") into national law by 17 October 2024. One year on, many EU Member States have failed to meet the transposition deadline, creating confusion and increasing compliance complexity for organisations across the EU.

Cyber Resilience Act: The clock is ticking for compliance

The Cyber Resilience Act (the "CRA") entered into force on 10 December 2024 and applies in full from 11 December 2027. Manufacturers of in-scope products should start the compliance journey as soon as possible to avoid impacts to the product development cycle and non-compliance risk exposure.

Navigating NIS 2: Mastering Compliance and Risk in a Fragmented Cybersecurity Landscape

White & Case Partners John Timmons and Clara Hainsdorf explore the key issues for organizations grappling with NIS 2 compliance in light of the complex implementation landscape.

Ransomware Payments: New legislative proposals in the UK

On 14 January 2025, the Home Office opened a public consultation (the "Consultation") on proposals seeking to address the growing threat and impact of ransomware in the UK.

NYDFS Releases Artificial Intelligence Cybersecurity Guidance For Covered Entities

On October 16, 2024, the New York State Department of Financial Services (the "DFS"), under its Cybersecurity Regulation—23 NYCRR Part 500—issued a memorandum providing guidance on the risks posed by artificial intelligence ("Guidance Memo").

SEC Will Prioritize AI, Cybersecurity, and Crypto in its 2025 Examination Priorities

On October 21, 2024, the US Securities and Exchange Commission ("SEC") Division of Examinations ("Examination Division") announced its 2025 Examination Priorities ("Report").Investment advisers and broker-dealers should ensure that policies, procedures and surveillance efforts related to these priorities address concerns outlined in the Report.

SEC Enforcement Heats up on Key Public Company Topics: Cyber Disclosure, Director Independence and Regulation FD

The U.S. Securities and Exchange Commission's ("SEC") Division of Enforcement has recently brought a spate of enforcement actions relating to key topics for public companies. These include enforcement actions related to cybersecurity incident disclosure, director independence and Regulation Fair Disclosure ("Reg FD") violations, which are described below, and actions based on Section 13 and 16 beneficial ownership filings, as discussed in our prior alert.

Judge Rejects SEC’s Aggressive Approach to Cybersecurity Enforcement

On July 18, 2024, a New York federal judge dismissed most of the US Securities and Exchange Commission's ("SEC") claims against SolarWinds Corp. ("SolarWinds" or the "Company") and its Chief Information Security Officer ("CISO"), Timothy G. Brown, in connection with the Company's cybersecurity practice.

SEC’s Corp Fin Director Issues Statement on Cybersecurity Incident Disclosures

On May 21, 2024, the SEC's Director of the Division of Corporation Finance issued a statement on cybersecurity incident disclosures in light of the SEC's new cybersecurity disclosure rules. Our summary of this statement and key take-aways from White & Case's survey of cybersecurity disclosures is below.

The SEC’s Charges Against SolarWinds and its Chief Information Security Officer Provide Important Cybersecurity Lessons for Public Companies

On October 30, 2023, the US Securities and Exchange Commission ("SEC") announced that it filed charges against SolarWinds Corp. ("SolarWinds" or the "Company") and its Chief Information Security Officer ("CISO") in connection with the SEC Division of Enforcement's ("Enforcement Division") investigation of a cyberattack.

On July 26, 2023, the Securities and Exchange Commission ("SEC"), in a 3-2 vote, adopted rules that will require public companies to make prescribed cybersecurity disclosures.

Shaping the future of digital and cybersecurity governance

In this brief three-minute video, London-based partner Lawson Caisley, Chair of White & Case's Global Cyber Risk Committee, shares his insights on governing cyber risk at the corporate level and some of the challenges of cyber risk management in the boardroom. Filmed at the Digital Directors Network (DDN) Domino 2023 conference on digital and cybersecurity governance.

In this short three-minute video, Washington, DC–based partner F. Paul Pittman discusses the implications of the proposed new SEC rules on cybersecurity governance and what corporate boards can do now. Filmed at the Digital Directors Network (DDN) Domino 2023 conference on digital and cybersecurity governance.

The potential for cybersecurity threats and attacks looms large and the technology companies developing new products and services play a constant game of cat-and-mouse with hackers and cybercriminals for control of cyberspace. Here are six points to consider when analyzing cybersecurity risks and protections.

Directors face personal liability over cybersecurity failures

In an article for The Times, White & Case partner Lawson Caisley discusses why it could become increasingly common for UK directors to "face personal liability and regulatory censure as a result of their company suffering or mishandling a cyberbreach".

Director liability for cyber breaches: transatlantic warning signs?

Two legal cases in the US in the past month suggest that regulators and prosecutors are becoming more determined to take personal action against directors and senior executives who fail to deal adequately with cyber security breaches.

On March 9, 2022, the Securities and Exchange Commission ("SEC") proposed rules that would require public companies to make prescribed cybersecurity disclosures.

In The Legal 500's newly released In-House Lawyer Magazine a group of White & Case lawyers has contributed a legal briefing on trends in German commercial litigation.

AAA plc & ors v Persons Unknown: Cyber Activism or Blackmail?

In recent years, demands for payments in cryptocurrencies have become the ransom of choice for cyber extortionists and other online frauds. As a result, the English Court's powers are increasingly being called upon.

Ninth Circuit Decision Highlights Importance of Updating Risk Factors to Address Material Developments, including those relating to Cybersecurity Risks.

Cybersecurity Enforcement: New York Department of Financial Services issues first penalty under Cybersecurity Regulation

Consistent with its increasing activity in the cybersecurity enforcement space, in March 2021, the NYDFS issued its first penalty under the Cybersecurity Regulation. This client alert explores the settlement and offers takeaways on the areas of focus by the NYDFS in enforcement actions under the Cybersecurity Regulation.

Compensating non-material damages based on Article 82 GDPR

Is a data subject entitled to compensation from a controller or processor if the data subject's GDPR rights have been infringed, even if they have not suffered any kind of material damage?

Cybersecurity Risk: Top 5 strategies to build resilience

The fourth webinar in our 2020 Autumn Webinar Series covered crucial steps you should be taking to protect against cybersecurity threats and what you should do when disaster strikes.

Before the Dust Settles: The California Privacy Rights Act Ballot Initiative Modifies and Expands California Privacy Law

Hot on the heels of the California Attorney General's rulemaking process for the California Consumer Privacy Act ("CCPA"), California voters have passed a ballot initiative to expand and create new privacy rights for consumers.

UK law enforcement can now obtain an order against a person in or operating in the US for the production of or access to electronic data under a new ‘landmark’ US-UK data sharing agreement.

The COVID-19 crisis has exposed many companies to more cyber threats. Tim Hickman and John Timmons discuss what businesses need to do should a major incident occur.

Trending: Legal protection for cryptoasset stakeholders

Recent decisions in Singapore and New Zealand confirm that the courts are prepared to act to provide greater certainty and support to stakeholders in cryptoassets.

Recovering the ransom: High Court confirms Bitcoin status as property

The High Court has determined that Bitcoin (and other similar cryptocurrencies) can be considered property under English law, and could be the subject of a proprietary injunction. The Court granted the injunction to assist an insurance company to recover Bitcoin that it had transferred in order to satisfy a malware ransom demand.

Navigating Privacy and Cyber Incident Notification and Disclosure Requirements

Organisations are facing increasing uncertainty in assessing global notification and disclosure obligations and making a determination of whether to notify or disclose a privacy violation or security incident in today's complex regulatory environment. This article offers six steps companies should consider when navigating this complex process.

Proposal on the Application of the NIS Regulations post-Brexit

This article examines the impact of the UK Network and Information Systems Regulations 2018 (SI 2018/506) (NIS Regulations) on organisations post Brexit and their obligations under applicable cybersecurity law.

Consistent with its increasing activity in the cybersecurity enforcement space, in March 2021, the NYDFS issued its first penalty under the Cybersecurity Regulation. This client alert explores the settlement and offers takeaways on the areas of focus by the NYDFS in enforcement actions under the Cybersecurity Regulation.

On March 3, 2021, the New York State Department of Financial Services ("NYDFS") announced that mortgage lender, Residential Mortgage Services, Inc. ("RMS") will pay a penalty of $1.5 million to the State to settle violations of NYDFS Cybersecurity Regulation, 23 NYCRR 500 ("Cybersecurity Regulation").1 Although, the NYDFS commenced its first enforcement action in July 2020 against insurer First American Title Insurance Company, this appears to represent the first penalty issued by the NYDFS under the Cybersecurity Regulation and the second reported enforcement action.

As we have set forth in our previous client alerts,2 NYDFS's Cybersecurity Regulation establishes numerous specific administrative and technical security requirements for covered entities to adopt and implement. The violations here stem from failures by RMS to disclose a 2019 data breach and to conduct required Cybersecurity Risk Assessments. Importantly, the violations were uncovered during a routine compliance examination between March and August 2020, providing notice to covered entities that the NYDFS will be proactive in its efforts to ensure compliance with the Cybersecurity Regulation. The NYDFS settlement continues a trend among regulators and lawmakers to focus on cybersecurity enforcement and establishing defined standards for compliance.

The NYDFS Examination and Discovery of the 2019 Data Breach

On March 30, 2020, NYDFS commenced a routine safety and soundness examination of RMS for the period between January 2017 and December 2019, which included an assessment of RMS’s compliance with the Cybersecurity Regulation. During the course of the examination, RMS disclosed that it had suffered a data breach 18 months earlier, in March 2019, and that it had not conducted an in-depth investigation of the incident nor disclosed the event’s occurrence to NYDFS or other state agencies.

The breach originated from a phishing email sent to an RMS employee. As a mortgage lender licensed in over 20 states, RMS collects sensitive personal information from customers applying for mortgage loans, including social security and bank account numbers. On March 5, 2019, an employee who collects a "substantial amount" of this data received a phishing email that appeared to come from a business partner. The employee followed a malicious link in the email to a website where she provided her email credentials. Although RMS maintained multi-factor authentication to protect company email accounts, the employee approved several remote login attempts to her email account, thereby granting the intruder access. The following day, on March 6, the employee notified RMS’s IT staff of the incident. The IT team traced the breach to an IP address in South Africa and blocked the unauthorized access to the email account. RMS did not investigate the matter further.

According to NYDFS, RMS failed to "(1) identify whether Employee’s mailbox contained private consumer data during the breach, (2) identify which consumers were impacted, and (3) apply the applicable state notice requirements triggered by the breach." Its failure to investigate the incident until prompted by NYDFS and its failure to disclose the breach for 18 months were both in violation of the Cybersecurity Regulation.

In its examination, NYDFS further discovered that RMS was in violation of the requirement under the Cybersecurity Regulation to maintain and conduct comprehensive cybersecurity risk assessments. Under the Cybersecurity Regulation, licensees must "identify and evaluate periodically vulnerability to cybersecurity risks and threats . . ." and design a cybersecurity program to mitigate those threats and risks. Finally, the NYDFS noted that RMS’s violations meant that it had also inaccurately certified its compliance with the Cybersecurity Regulation in its annual filing.

Following NYDFS's investigation, in fall 2020, RMS launched its own internal investigation into the data breach. RMS reviewed the sensitive personal information collected in the employee’s compromised emails, identified data that could have been accessed by the intruder, and subsequently notified the customers impacted by the breach along with the appropriate state agencies. Despite the initial delay in reporting the breach, NYDFS applauded RMS’s cooperation throughout its examination and investigation. The NYDFS did not disclose the number of customers whose data were impacted by the breach. Notably, however, the Massachusetts State Attorney General’s data breach report indicates 127 residents of Massachusetts were affected and had social security numbers, driver’s licenses, and credit numbers breached.

NYDFS Settlement Terms

On March 3, 2021, NYDFS announced a settlement with RMS to resolve the violations of the Cybersecurity Regulation. The settlement included both a civil penalty and a number of other remedial provisions.

First, RMS must pay a penalty of $1.5 million to NYDFS. NYDFS based this penalty upon, "the extent to which the entity has cooperated with the Department in the investigation of such conduct, the financial resources and good faith of the entity, the gravity of the violation, and such other matters as justice and the public interest may require."

Second, RMS agreed to devote additional resources to bolstering its cybersecurity. The Consent Order requires that RMS submit a Cyber Security Incident Response Plan to NYDFS within 90 days. This comprehensive plan must set out incident response plans and procedures, define roles and responsibilities for decision-making throughout the organization, and account for reporting and documenting any cybersecurity incidents, among other things.

Third, the Consent Order further requires that RMS submit a Cybersecurity Risk Assessment to the NYDFS within 90 days. RMS is required to update the Risk Assessment to account for any changes in RMS Information Systems and evolving risks and threats. Additionally, the Risk Assessment must include written descriptions of the criteria used to evaluate risks and to assess the integrity of current controls in place.

Finally, the Consent Order requires that RMS submit materials to the NYDFS relating to Training and Monitoring. Specifically, RMS must submit its most recent and updated cybersecurity awareness training for staff. It must also submit its policies for monitoring Authorized User activity and for detecting unauthorized access by Authorized Users to Nonpublic Information.

Implications

The $1.5 million penalty imposed by the NYDFS puts covered entities on notice that the NYDFS Superintendent’s enforcement actions will carry significant weight. While the lack of information regarding the number of impacted individuals here limits what we can predict concerning how the NYDFS might approach settlements and fines in other actions, the settlement nevertheless provides several useful takeaways.

The RMS enforcement action stemmed from a routine examination of the covered entity's compliance with the Cybersecurity Regulation, suggesting that the NYDFS will be proactive in its compliance assessment and enforcement efforts.

Consistent with the First American Title Insurance Enforcement Action, the RMS enforcement action involved a failure to conduct a periodic risk assessment. In addition, the companies failed to adequately investigate a known incident (RMS) or address a known vulnerability (First American Title Insurance) over an extended period. As such, regulated entities should be proactive in complying with the Cybersecurity Regulations and ensure that any efforts to do so are clearly documented.

The RMS settlement also suggests an emphasis by NYDFS on the general importance of the disclosure requirement. Companies should take care to establish a cybersecurity incident response plan, which includes a conscientious consideration of the disclosure of cybersecurity incidents and events to the NYDFS and affected consumers alike.

The Consent Order makes clear the importance of cooperation with NYDFS in the event of an investigation. The Department emphasized its appreciation for RMS's willingness to cooperate and commitment to remedying its cybersecurity deficiencies, which may have mitigated RMS's penalty.

The recent enforcement actions taken by NYDFS should remind covered entities to take the necessary steps to ensure active and continued compliance with Cybersecurity Regulations. Filing a certification cannot be an empty gesture, as the NYDFS has demonstrated it will conduct the appropriate due diligence to ensure covered entities’ annual certifications are accurate. And where violations are discovered, NYDFS will expect covered entities to rectify them and redress any outstanding harms to individuals.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.