Making the trading system work for Africa

The African Continental Free Trade Area could trigger a new era in intra-African trade.

By Mukund Dhar, Africa Interest Group Leader

As our last edition of Africa Focus was published in September 2020 in the midst of the COVID-19 pandemic, some progress had been made on the development, trial and authorization of COVID-19 vaccines. However, there was no assurance of efficacy or effectiveness, and there was profound uncertainty in our personal and professional lives, with unprecedented upheaval in the global economy.

This spring 2021 issue comes to you in a changed environment: Multiple vaccines have been approved; millions of vaccine doses are being manufactured and administered every day; and a return to normality feels no longer like a matter of hope, but of time. Therefore, while uncertainty in our lives and disruption in the global economy continues, we can perhaps permit ourselves to review the business and legal environment in Africa with a renewed sense of cautious optimism and against the backdrop of groundbreaking changes that raise important issues for companies and financial institutions doing business in Africa.

Nearly the entire African continent is involved with the African Continental Free Trade Area (AfCFTA), a single trade and investment market with a combined GDP of close to US$3.4 trillion. Trading under these new arrangements started on January 1, 2021. At the same time, development finance institutions have mounted a robust response to the COVID-19 pandemic by harnessing support from international investors and aggressively funding infrastructure and development. Several sectors of Africa’s economy continue to offer private equity and venture capital investment opportunities, while multilateral development banks are successfully supporting post-COVID recovery and growth in key African sectors. Meanwhile, innovative technologies and new approaches to decommissioning mining assets are transforming Africa’s mining industry and enabling sustainable exits.

This sixth edition of Africa Focus begins with "Making the trading system work for Africa," which explains how AfCTA's plan for virtually all African nations to open their markets to each other may have arrived at exactly the right time to spark change. "African development finance institutions" discusses how African DFIs are achieving positive impacts by funding recovery responses, leading the way with sustainable lending and attracting commercial lenders to African markets.

The article "Private equity in Africa: Trends and opportunities in 2021" highlights several industries in Africa that remain attractive private equity and venture capital destinations, particularly for those focused on long-term investments, and "Ensuring sustainable exits from African mining" discusses how mining companies can improve the ways they decommission and close their operations as well as factors that mining companies, regulators and other stakeholders can consider when formulating rules to reflect environmental, social and governance principles.

In "European multilateral development banks in sub-Saharan Africa," we examine how multilateral development banks, including the European Investment Bank, the European Bank for Reconstruction and Development and others, are collaborating with other key stakeholders and acting as catalysts for growth.

Finally, in "African mining 4.0: An innovative sunrise for African miners," we discuss how new transformative technologies, rapidly becoming available to the mining industry, are ushering in a new era of increased productivity, efficiency, safety and growth for miners.

We welcome your suggestions for any topics to review in our upcoming issues. For now, we hope this issue of Africa Focus helps you navigate the rapidly changing business landscape and explore current opportunities for doing business and investing in Africa.

The African Continental Free Trade Area could trigger a new era in intra-African trade.

Rising to challenges, funding a recovery response and leading the way to sustainable lending.

Despite challenges, Africa remains an attractive PE and VC investment destination.

The development of mine decommissioning and closure laws.

Supporting post-COVID recovery and growth in key sectors.

Transformative technologies are ushering in a new era of efficiency, safety and growth.

Despite challenges, Africa remains an attractive PE and VC investment destination

Subscribe to receive Africa Focus

World in Transition

Our views on changing dynamics in energy, ESG, finance, globalization and US policy.

Iman Algubari (White & Case, Trainee Solicitor, London) contributed to the development of this publication.

One factor contributing to PE’s resilience in Africa in 2020 is a focus on investing in businesses that provide “essential” or “emergency services.”

The global economic downturn following the outbreak of COVID-19 slowed private equity (PE) and venture capital (VC) activity across emerging economies. The COVID-19 crisis particularly affected the short-term and medium-term growth prospects of funds' portfolio companies, which are generally experiencing negative impacts on revenues, costs and profitability.1 For example, a September 2020 analysis by the International Finance Corporation (IFC) highlights the impact of the economic shock caused by COVID-19 on growth PE funds (which invest in comparatively more mature businesses than VC funds).

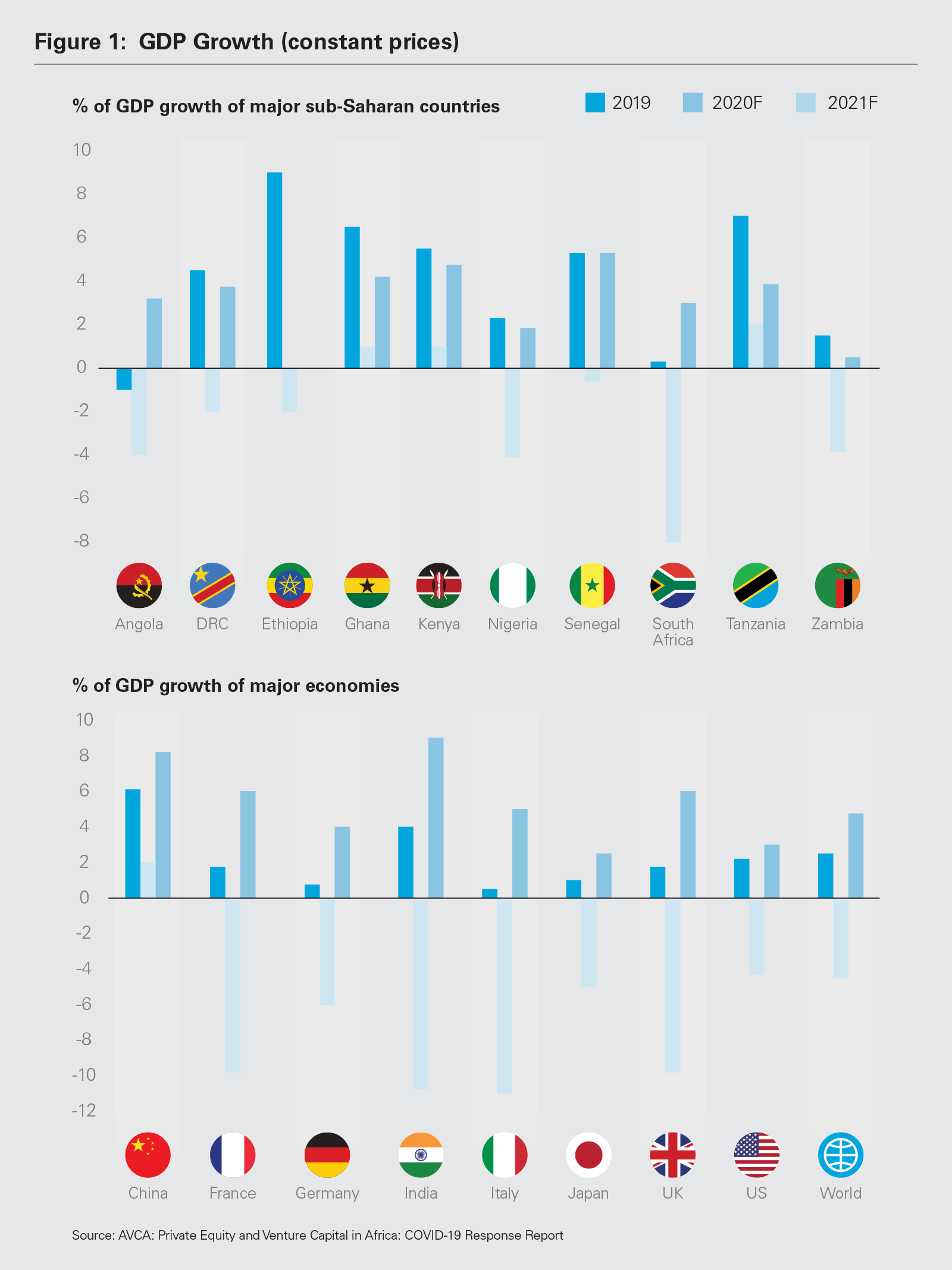

Although the African continent was relatively less affected by the virus than other parts of the world (with the notable exception of South Africa and parts of North Africa), many trends that affected PE and VC activity throughout emerging markets impacted by the pandemic were mirrored in Africa in 2020 (See Figure 1).

One factor that has mitigated the pandemic's impact on PE and VC activity in Africa is the composition of the limited partner (LP) base of PE and VC firms operating on the continent, where development finance institutions (DFIs) continue to play a significant role.2 DFIs' long-term focus and mandate for countercyclical investments often shield them from short-term shocks. While this support continues, there is an opportunity for fund managers to take advantage of the opportunities DFIs can offer, such as connecting fund managers and governments to fill funding and capacity gaps, facilitating due diligence processes and mobilizing local capital.

Overall, GDP growth on the African continent, supported by factors such as the LP base of Africa-focused PE and VC firms, may be contributing to PE's continuing investment appetite. The African Private Equity and Venture Capital Association (AVCA) reports that the total value of African PE deals in H1 2020 remained constant at US$0.7 billion3 (the same as H1 20194). With H2 data soon to be released, the full impact of COVID-19 on deal-making activity will soon be seen.

One factor contributing to PE's resilience in Africa in 2020 is a focus on investing in businesses that provide "essential" or "emergency services," including healthcare, food production, energy and education sectors, which continued to operate during lockdowns.5 This trend is likely to continue in 2021.

Africa's healthcare sector experienced significant growth and will likely remain a key focus in 2021, due to a demand for investment in affordable healthcare. According to AVCA, the healthcare sector accounted for the largest share of PE deals by value in H1 2020 (24 percent).6 This is a marked increase from H1 2018, when just 4 percent of total deal value flowed to the sector.7 Healthcare is attractive to PE investors for a number of reasons, including a high internal rate of return (IRR) and favorable exit opportunities. The IFC estimates that healthcare investments in Africa deliver a 9.6 percent investment-level gross IRR—the fourth-highest return after telecommunications, IT and consumer staples. Investments in healthcare also align with societal impact, a key PE goal in Africa.

African financial technology (fintech) is another sector that historically attracted PE investment and will likely continue in 2021. In 2019, more than 40 percent of total investments in Africa went to this sector, with financial inclusion remaining a main driver, attracting 54.5 percent of total investments.8 Technology deals increased notably by volume and value, rising from 8 percent and 7 percent, respectively, in H1 2019 to 17 percent and 16 percent in H1 2020.9 The acquisition of Paystack, a Lagos-based payments company, by the online payments provider Stripe is an example of the success of African fintech.10 Mobile services and technologies already comprise a large proportion of Africa's GDP, with an added value of US$155 billion (9 percent of the total), and is expected to rise to US$184 billion by 2025.11 While fintech such as e-commerce is expected to attract a significant proportion of new investments, a number of other fintech-enabled verticals are poised for growth in 2021, including enterprise software and cloud computing, health, education and renewable energy technologies.

Infrastructure activity also remains strong in Africa, with a large number of deals completed in recent years in both the traditional and renewable energy sectors. Renewable energy is one of the fastest-growing segments in many African countries in terms of both demand and volume of public and private investment. Solving persistent, high demands for energy solutions—on a continent where 600 million people lack access to electricity—will continue to be a focus in 2021 and beyond. The International Energy Agency estimates that investments must increase four-fold to US$120 billion annually to close the energy gap by 2040. In addition, the declining costs of renewables, particularly solar energy, is driving investments with a rising proportion from PE. ARCH Emerging Markets Partners' investment into CrossBoundary Energy, which will be used to scale CrossBoundary Energy's commercial and solar services, is an example of this trend (with further investment expected into CrossBoundary Energy expected in 2021). PE's focus on impact investing and meeting the UN's social development goals aligns with continued investment into renewable energy companies.

VC activity in Africa has grown significantly over the past two decades, becoming a more recognizable investment space. This trend will likely continue in 2021.

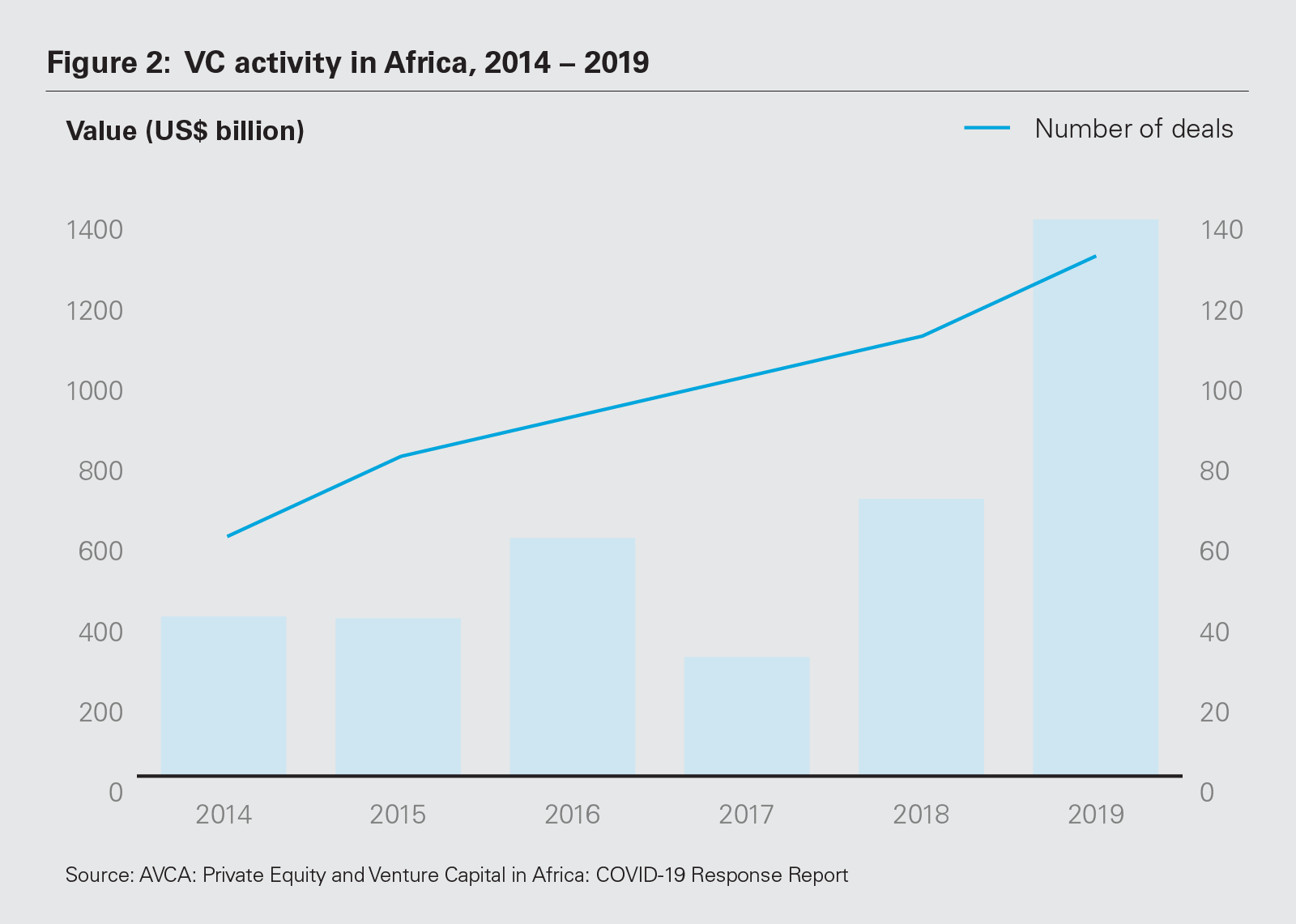

The world's second fastest-growing region, Africa experienced 4.6 percent average annual GDP growth from 2000 to 2016.12 This robust economic backdrop has been a crucial driver of Africa's VC industry, creating a positive economic environment to catalyze innovation, entrepreneurship and investment. According to AVCA, the total number and value of VC deals reported on the continent reached a six-year record high in 2019, and the value of VC deals reported in Africa reached US$1.4 billion in 2019, a record high.13 (See Figure 2).

PE and VC funding developed progressively in Africa supported by a 1.2 billion-person market, an expansive middle class consumer base and the world's largest free-trade area.14

In some regions, growth was facilitated by efforts to build a more supportive legislative framework for startups. In Francophone Africa, Tunisia and Senegal passed Startup Acts to create a better local environment for innovation and entrepreneurship.15 Although fintech dominates Africa's startup scene, entrepreneurship has also exploded within the utilities, logistics & transportation, e-commerce, healthcare and agribusiness sectors. In 2019, Nigeria attracted a record high of US$747 million in tech VC investment (37 percent of all funding), while Egypt reached number three both in terms of deal count (+147 percent year-over-year) and deal volume (+215 percent year-over-year). The regional landscape has now been redrawn, with 85 percent of total funding (US$1.7 billion) flowing to Nigeria, South Africa, Egypt and Kenya.16

Despite the impact of the COVID-19 pandemic on the global economy, VC firms continued investing in Africa during 2020. Examples include pre-seed investments of US$1 million into Okra by TLcom Capital17 and Autocheck Africa, completing a pre-seed round of US$3.4 million co-led by TLcom Capital and 4DX Ventures.18 PE firms from the APAC region are also becoming more active on the continent, evidenced by Opay, an Africa-focused mobile payments startup owned by Chinese investors, raising US$50 million in a Series A round from investors including Sequoia China.19 Transsion, China's dominant mobile phone device creator in Africa, partnered with Kenya's Wapi Capital to fund early-stage African fintech startups.20 These early-stage investments may act as a signal to broader groups of global investors, attracting attention and increasing deal-making activity in 2021.

US$3.8 billion

PE fundraising in 2019

(AVCA: Private Equity and Venture Capital in Africa)

After suffering a dip in 2016 and 2017, PE fundraising started to recover in 2018, with the total value of fundraisings reaching US$3.8 billion in 2019.21 However, the COVID-19 pandemic has raised challenges, including a disruption in the continent's fundraising efforts. 49 percent of GP respondents surveyed by AVCA expected the COVID-19 crisis to affect their fundraising timeline, and 29 percent expected it to impact their fundraising target.22 Any upcoming fundraisings may continue the ongoing trend of having DFIs as cornerstone LPs in the short- to medium-term. Despite these challenges, longer-term fundamentals continue to attract investors to the region, and capital raising continues, particularly where existing GP-LP relationships are in place. In July 2020, CDC Group Plc and Finnfund announced a combined commitment of US$70 million to AfricInvest Fund IV to anchor the fund's first close at US$202 million; and CDC committed US$100 million to Helios Investment Partners' fourth fund.23

In addition to the traditional fundraising methods, PE funds and their investee companies also continue to innovate and explore different options to raise funds and finance projects.

Permanent capital vehicles (PCVs) offer advantages that attract interest from PE firms focused on investing in Africa. One attractive feature of PCVs is a longer fund life that enables PE firms to hold assets for a longer time and ride out short-term volatilities. Managers also do not have to return to the market on a regular basis to raise successor funds. In addition, PCVs align with the longer hold period for African portfolio companies. One recent example is the December 2020 combination between Helios and Fairfax Africa Holdings, which provided Helios with long-term shareholders in a PCV.24

Blended finance is another fundraising avenue that rose to prominence in 2020. Blended finance is one important way that assets like sustainable infrastructure can be made "investable" by large-scale, mainstream capital in emerging markets. Investor risks can be allayed by the use of catalytic funding, such as grants from public and philanthropic sources, to mobilize additional private sector investment.

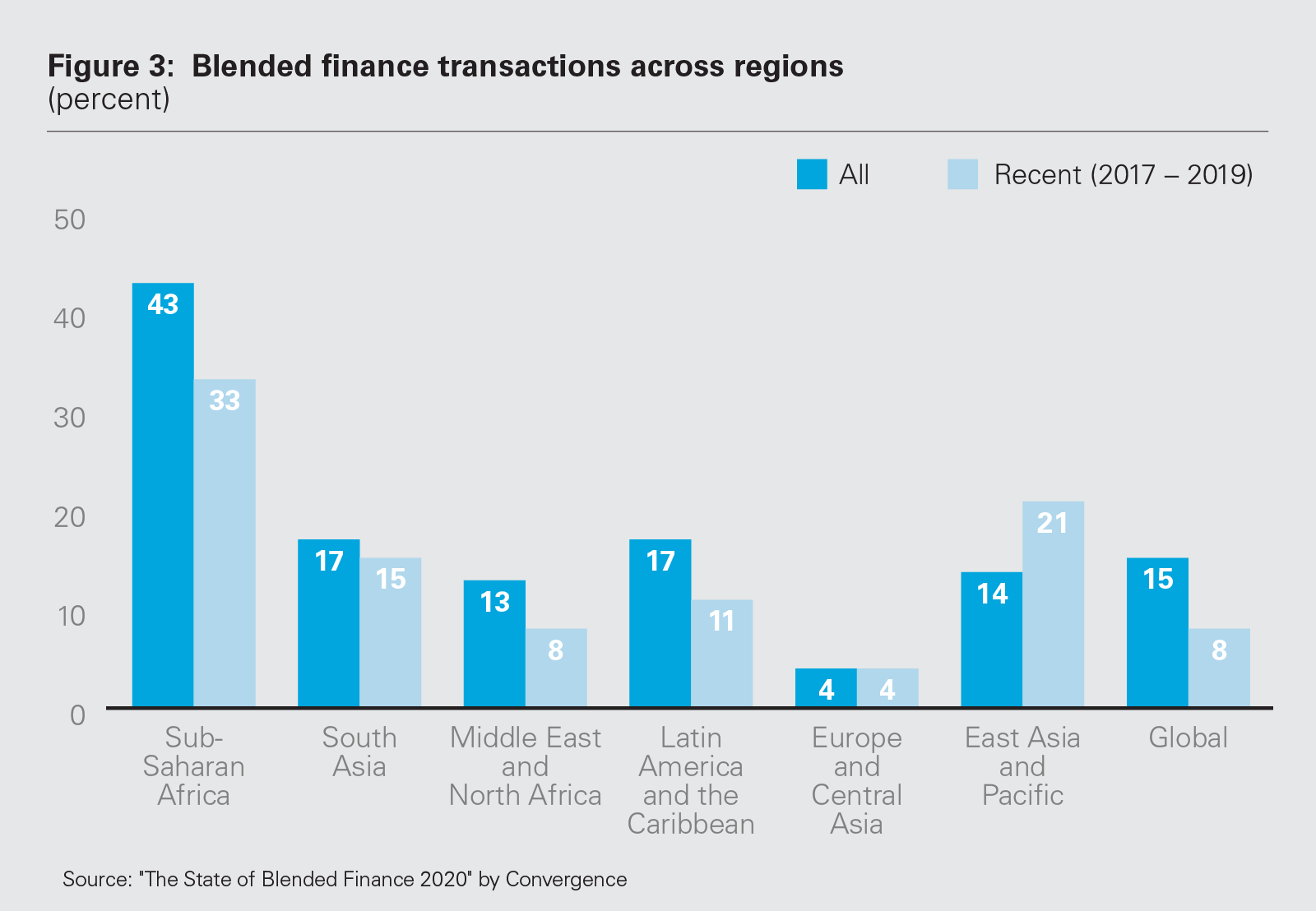

Sub-Saharan Africa has been the most targeted region for blended finance transactions to date, representing 33 percent of blended finance transactions launched in 2017 – 2019, and 43 percent of the market historically.25 (See Figure 3) The exit of CrossBoundary Energy I (CBE1) at a 15 percent net IRR to investors following ARCH Emerging Partners' investment into CrossBoundary Energy is a powerful demonstration of the potential of blended finance to unlock new and impactful asset classes. CBE1 closed in 2015 as Africa's first dedicated fund for commercial & industrial solar, and served as a prototype for a new blended finance approach to renewables in Africa. USAID's Power Africa initiative contributed US$1.3 million in the form of a repayable grant to attract additional private investors to the fund. At the close of the transaction, the leverage of matching private capital was more than 30 times.26 It is clear that blended financing has become increasingly attractive to the private sector, which has been demonstrating a growing interest in responsible investment strategies and ESG investment.

Another expansion approach being explored by PE in Africa is entering into advisory contracts, pursuant to which a PE firm manages assets held by an investment manager. This provides the investment manager with PE asset management expertise, and allows PE firms to demonstrate their value creation and value realization capabilities. For example, Ethos Private Equity, a traditionally South Africa–focused firm, extended its pan-African reach through four of these initiatives, which resulted in Ethos managing assets in countries such as Egypt and Morocco.27

43%

of blended finance transactions in sub-Saharan Africa to date(Convergence, "The State of Blended Finance 2020")

Africa's exit environment has been a consistent challenge for PE funds. In surveys conducted even before the onset of COVID-19, LPs identified limited exit opportunities as a key challenge, and Africa recorded a small number of exists in 2019 (only 43 exits, down from a peak of 52 in 2017).28 Trade buyers account for almost half of PE exits, and the share of secondary exits was in decline. Initial public offerings (IPOs) remain rare as an exit route.

Africa's exit problems are largely due to a lack of liquidity, which leaves PE funds without consistent, reliable exit options. However, despite Africa's historic exit issues and the further disruptive impact of COVID-19, an AVCA survey shows that LPs are optimistic about major aspects of the exit environment, with approximately 85 percent of respondents expecting exits to both trade buyers and PE or other financial buyers to increase over the following three-to-five years, while 52 percent expect the same of IPOs and capital markets.29 LPs clearly see Africa as an attractive medium- to long-term opportunity, with more than 90 percent believing returns in Africa will be similar to or better than those in other emerging markets over the next decade.30

Overall, Africa remains an attractive PE and VC investment destination, relative to other emerging markets, with significant growth expected.

Although the impact of the ever-evolving pandemic on investments in Africa is unclear, the long-term outlook for PE in Africa appears bright. Current economic challenges will require agility from PE and VC funds—for example, through innovative fundraising efforts. But stretched government finances and a challenging macro-environment may also represent enticing opportunities for PE investors in healthcare, fintech, renewables and other sectors in 2021.

1 IFC, Impacts of the COVID-19 Crisis on Private Equity Funds in Emerging Markets

2 AVCA: Private Equity and Venture Capital in Africa: COVID-19 Response Report

3 AVCA 2020 H1 African Private Equity Data Tracker report

4 Id.

5 Private Equity International – Africa Mapping out the continent’s hotspots

6 AVCA 2020 H1 African Private Equity Data Tracker report

7 Id.

8 2019 Africa Tech Venture Capital Report by Partech Africa Team

9 AVCA: Private Equity and Venture Capital in Africa: COVID-19 Response Report

10 https://www.ft.com/content/beb9a517-ea27-4d52-8544-43c8fdfa2f1d

11 AVCA 2020 H1 African Private Equity Data Tracker report

12 https://www.odi.org/events/4592-africas-economic-growth-new-global-context

13 AVCA Venture Capital in Africa: Mapping Africa's Start-Up Investment Landscape

14 https://www.worldbank.org/en/region/afr/overview

15 https://www.privateequityinternational.com/the-rise-of-venture-capital/

16 2019 Africa Tech Venture Capital Report by Partech Africa Team

17 https://techpoint.africa/2020/04/27/okra-raises-1m-pre-seed-investment/

18 https://techpoint.africa/2020/11/18/autochek-raises-3-4m-pre-seed/

19 https://www.atlanticcouncil.org/blogs/africasource/africas-venture-space-attracts-global-interest/

20 https://techcrunch.com/2019/08/15/chinas-transsion-and-kenyas-wapi-capital-partner-on-africa-fund/

21 AVCA: Private Equity and Venture Capital in Africa: COVID-19 Response Report

22 Id.

23 Private Equity International – Africa Mapping out the continent’s hotspots

24 https://www.globenewswire.com/news-release/2020/07/10/2060633/0/en/Proposed-Strategic-Transaction-Between-Helios-Holdings-Limited-and-Fairfax-Africa-Holdings-Corporation.html

25 The State of Blended Finance 2020 by Convergence

26 https://aithority.com/technology/energy-management/crossboundary-energy-fully-exits-first-fund-at-15-net-irr-raises-40-million/

27 https://www.ethos.co.za/communications/ethos-secures-advisory-contract-for-ninety-ones-africa-private-equity-funds-bolstering-its-pan-african-platform/

28 AVCA: Private Equity and Venture Capital in Africa: COVID-19 Response Report

29 Private Equity International – Africa Mapping out the continent’s hotspots

30 Id.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP

View full image 'Figure 1: GDP Growth (constant prices)' (PDF)

View full image 'Figure 1: GDP Growth (constant prices)' (PDF)

View full image 'Figure 2: VC activity in Africa, 2014 – 2019' (PDF)

View full image 'Figure 2: VC activity in Africa, 2014 – 2019' (PDF)

View full image 'Figure 3: Blended finance transactions across regions (percent)' (PDF)

View full image 'Figure 3: Blended finance transactions across regions (percent)' (PDF)