Winning the AML Intelligence War with Public Private Partnerships

Key considerations for banks engaging with governments and peer institutions to improve financial crime compliance systems

Key considerations for banks engaging with governments and peer institutions to improve financial crime compliance systems

Challenges and opportunities in the US, UK and Europe

It has been a period rife with notable shifts on the global stage; a new administration in the US, the end of the Brexit transition period and the reaching of key milestones in the discontinuation of LIBOR, to name but a few. This section provides an overview of recent developments in some key regulatory hot topics

Key considerations for banks engaging with governments and peer institutions to improve financial crime compliance systems

Every year, banks spend billions of dollars on core financial crime compliance systems and are filing more suspicious activity reports (SARs) than ever. Despite these process improvements, the global anti-money laundering (AML) regime does not appear to be substantially more effective. Innovative public-private partnerships (PPPs) have demonstrated some success in meeting government objectives, but is the system manifestly better for banks? We explore key considerations for banks engaging with their governments and their peers in AML PPPs, with a particular focus on the UK, the US and Germany.

The global AML regime is decades old, built on international standards, national legislation and multibillion-dollar enforcement actions. Yet, for all of those efforts, questions still remain as to the effectiveness of SARs—one of the keystone initiatives of the global AML regime.1

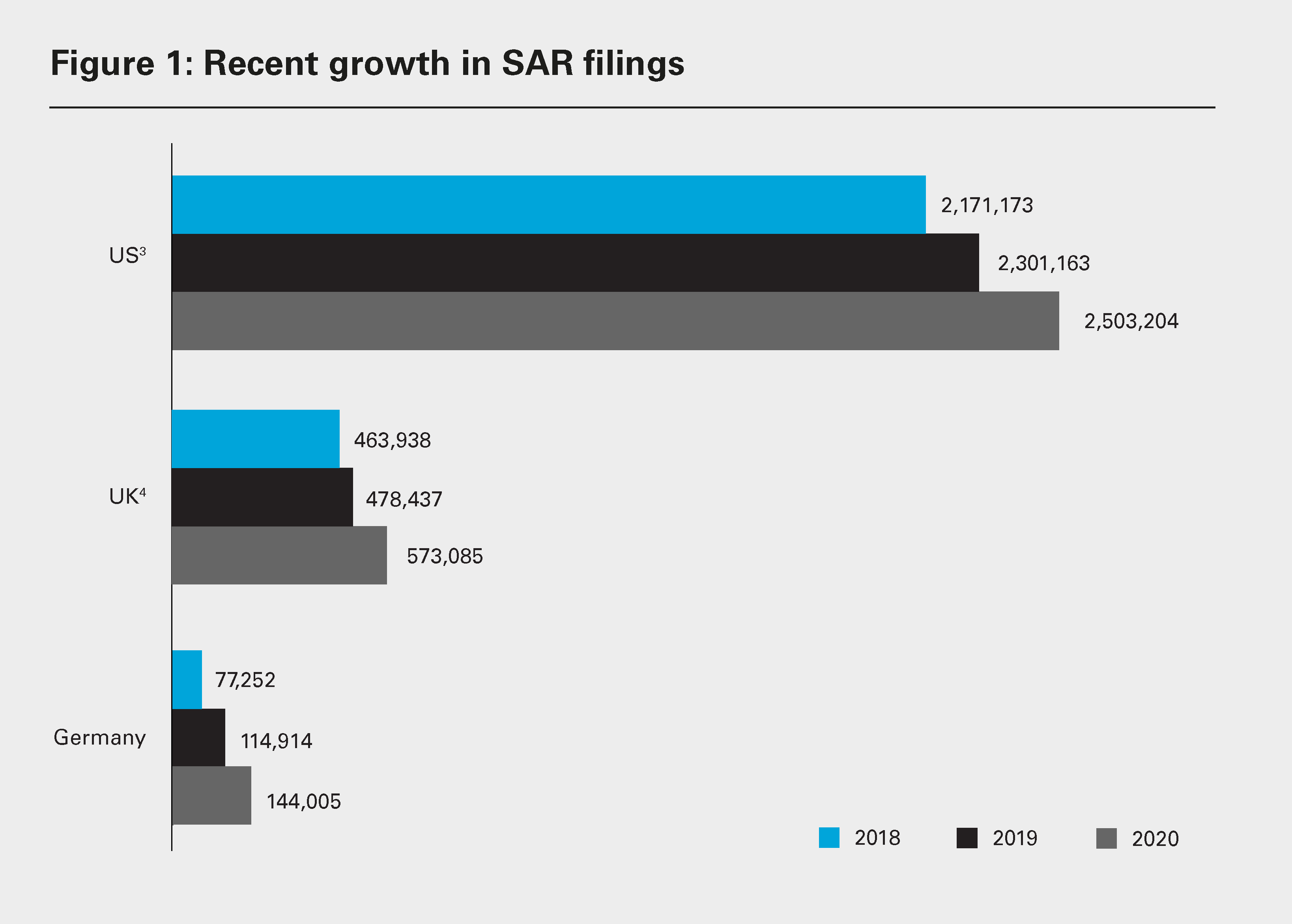

Financial institutions and other reporting entities collectively spend many billions of dollars annually to produce millions of SARs.2 In addition, the number of SARs filed has increased significantly each year. For example, Figure 1 shows how SAR filings in the UK, the US and Germany have grown over the last three years.

At the same time, surveys of past and present heads of national financial intelligence units (FIUs) indicate that only a relatively small handful of SARs are of immediate value to law enforcement.5

Of course, a report that is not of immediate value could still become valuable in the future, as investigations often develop over the course of many months and years. Moreover, some FIUs data mine all of their SARs to uncover trends and typologies or to develop new insights into networks that are only made clear after the SAR is placed in context. Still, this low return on investment is frustrating to both governments and reporting institutions and has driven a wave of reform designed to improve the usefulness or effectiveness of SAR reporting.

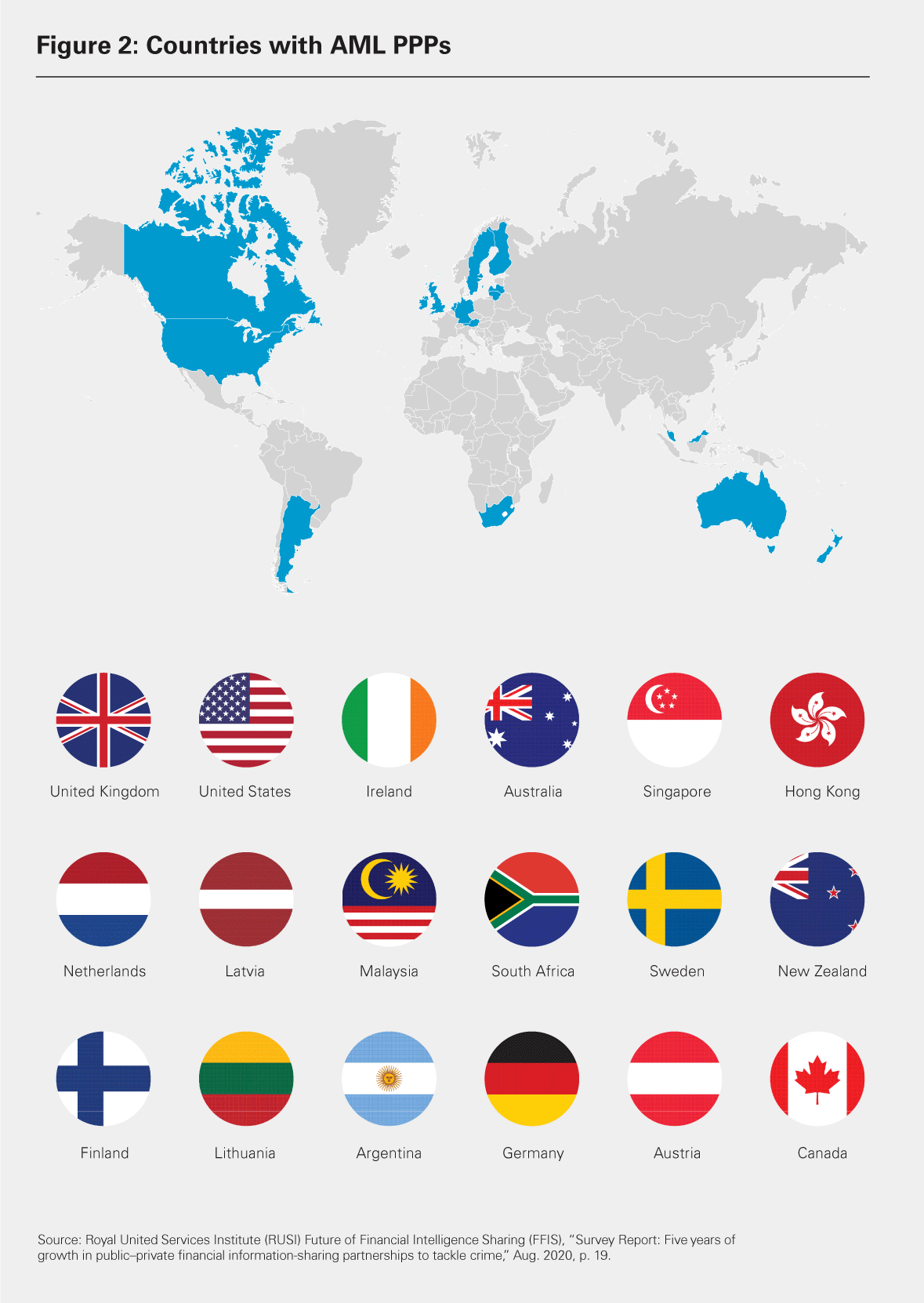

As of June 2020, at least 18 countries have developed PPPs (See Figure 2).

Some benefits from PPPs include:

Here are examples of current PPPs in the UK, the US and Germany.

While informal dialogue between law enforcement agencies and financial agencies has nearly always existed in many jurisdictions, a structured approach to that dialogue is a relatively recent innovation that was pioneered in the UK with the Joint Money Laundering Intelligence Taskforce (JMLIT). The JMLIT, created in 2015, now comprises of the following:

Since its inception, JMLIT has supported and developed more than 750 law enforcement investigations, which directly contributed to more than 210 arrests and the seizure or restraint of more than £56 million. JMLIT private sector members have identified more than 5,000 suspect accounts linked to money laundering activity and commenced more than 3,500 of their own internal investigations.7

Beyond these statistics, the 2018 UK Financial Action Task Force (FATF) mutual evaluation report gave two specific examples of JMLIT's success. These examples focus on terrorism financing matters and relate to the two terrorist attacks on London in 2017. JMLIT's assistance allowed law enforcement to rapidly obtain a full financial picture of the attackers and in relation to one of the attacks establish that there was no broader network beyond the three attackers.8 FATF also noted that one request by law enforcement agencies through JMLIT can obtain information from multiple financial institutions, which is very efficient for them in terms of developing a comprehensive intelligence picture. SARs that follow such a request are considered to be of a very high standard.

JMLIT sits within the National Economic Crime Centre (NECC) which coordinates and tasks the UK's response to economic crime and is intended to harness intelligence and capabilities from across the public and private sectors to tackle economic crime in the most effective way. The NECC launched in October 2018 and includes various law enforcement agencies and the Home Office. As the NECC evolves, it will build wider partnerships with the private sector.

In December 2017, the US Department of the Treasury's Financial Crimes Enforcement Network (FinCEN) formalized its PPP, the FinCEN Exchange.9 FinCEN, in close coordination with law enforcement, convenes regular briefings with financial institutions to exchange information on priority illicit finance threats, including targeted information and broader typologies. Its goal is to enable financial institutions to better identify risks and focus on high priority issues and to help FinCEN and law enforcement receive critical information supporting their efforts to disrupt money laundering and other financial crimes. It is a voluntary, invitation-based program, where participating financial institutions are selected based on their relevance to the topic of that particular exchange. The FinCEN Exchange grew out of more than a dozen special briefings since 2015 in five cities with more than 40 financial institutions and multiple law enforcement agencies that helped the public sector map out and target weapons proliferators, sophisticated global money laundering operations, human trafficking and smuggling rings, corruption, trade-based money laundering networks and other illicit actors.

More than 40

financial institutions are in the UK JMLIT

Germany established a PPP in September 2019 in order to intensify cooperation between the authorities and private sector institutions involved in preventing and combating money laundering. Germany's Anti Financial Crime Alliance (AFCA) aims to facilitate an intensive and lasting exchange of information from the public and private sectors to jointly identify new trends and developments and optimize potential for the reporting of suspected money laundering. To date, this national form of cooperation is unique in the field of financial crime in Germany.

The AFCA's Board, composed of an equal number of public sector representatives and private sector reporting entities, is responsible for AFCA's overall strategic orientation. AFCA's structure follows a partnership-based approach with equal input from all participants, allowing for strategic exchanges related to problems and issues between government institutions and the private sector. During AFCA's first year of work, the number of members has more than doubled to 36, including members from both inside and outside the financial sector. The Management Office incorporated in the German FIU is the main interface between the various participants, users and the AFCA Board. The operational core is formed of working groups, which meet regularly, have clear time limits and are demarcated by their subject matter. Initially, two working groups were set up:

In addition to these initial working groups, three more subject matter focused working groups have been set up in the course of 2020 covering: (1) Money laundering in the real estate sector, (2) tax offenses and (3) gambling.

In late 2020, AFCA has also established an expert panel which consists of high-ranking representatives from the public and private sector as well as a legal expert from the academic community. The expert panel will advise the Board regarding the strategic objectives of the AFCA, as well as analyzing and evaluating the results of the working groups.

Despite continuous progress, AFCA is not yet able to stand in comparison with similar initiatives in other countries, such as the JMLIT. One key obstacle in its work is the lack of a framework that would allow all AFCA members to exchange detailed information of individual transactions without risking violations of data protection requirements. This conflict of interest between data protection concerns and money laundering prevention ultimately has to be resolved by the legislator.

The advent of AML PPPs appear to have successfully achieved many government objectives, but do PPPs similarly benefit private sector participants, particularly multinational banks that may be involved in several national PPPs? Are AML PPPs also meeting banks' objectives, or do they simply create another additional obligation for banks?

To date, many banks have willingly participated in AML PPPs.10 Typically, in addition to altruistic reasons, they seek to:

We have also heard from many bank executives that if banks are required to maintain expensive AML systems to identify and report suspicious activities, they want to know that those reports at least have some value to law enforcement and other stakeholders. Whatever the objectives pursued by bank participants in a PPP, for the PPP to be a long-term success, those objectives must be pursued as diligently as any of the government's objectives.

Through a PPP, government authorities can provide more detailed typologies—or even details of specific organized crime groups and their members—that would otherwise compromise investigations, if that information were released more broadly. This allows banks to leverage the rich pools of data to which they have access with greater focus and intention, building and reporting connections that might not otherwise be suspicious. The return on investment for PPP-driven SAR investigations is also significantly higher than for self-generated SAR investigations. In the latter circumstance, once the SAR is filed, it may often feel as if the SAR was submitted directly into a black hole, with little acknowledgement that the SAR exists, let alone is useful. However, because of the involvement of the PPP, a bank that files PPP-driven SARs knows that the government is immediately interested in such information and often will take action on the information filed by the bank.

For all of the attention placed on information-sharing, many of the national-level PPPs share some significant deficiencies in cross-border information-sharing. For example, very few of the national-level PPPs coordinate with their foreign peers. This a major weakness when considering the cross-border nature of many of the topics addressed by PPPs, such as terrorism finance, narcotics trafficking, modern slavery and other transnational crimes. Moreover, the different priorities pursued between the national-level PPPs can diffuse the focus of multi-national banks that may be engaged in several different PPPs at the same time, undercutting potential improvements to AML compliance efficiency.

Similarly, national-level PPPs often impose confidentiality requirements or non-disclosure agreements – along with strict SAR confidentiality requirements – that in some jurisdictions may limit a bank's ability to share information across its enterprise, particularly with foreign branches, subsidiaries or affiliates. This may limit a multi-national bank's ability to exploit all of its data, see different aspects of cross-border relationships, derive more meaningful AML typologies that are specific to that bank and manage enterprise-wide risks.

Ideally, a bank's involvement in a PPP could result in efficiencies in its AML investigatory and reporting function. The PPP would set priorities for the bank, which would enable the bank to shift resources from lower-priority efforts to higher, more valuable, priorities. Unfortunately, to date, AML supervisors have generally not authorized such re-prioritization of resources, and participating in a PPP is an additional expense for many banks. To participate in a PPP, a bank would generally commit to engage in deeper, retrospective analyses of its account and transaction base and potentially promulgate bespoke rules for its transaction monitoring systems, all of which would be in addition to the bank's business as usual AML compliance function to meet its baseline regulatory requirements.

In theory, a bank engaged in a PPP would be able to use such involvement to boost its credentials as a responsible corporate citizen (and improve its environmental, social and governance (ESG) ratings). However, the nature of PPPs is to share information with and from the government that is otherwise sensitive or confidential. As a result, a bank may be extremely restricted as to what it can disclose about its activities in support of the PPP. Without concrete details it can point to, a bank's involvement in a PPP is esoteric and does not easily translate to a reputational asset.

Banks, particularly those with the highest public profiles, will continue to be willing participants in PPPs in the near- to mid-term. However, if PPPs become one-sided, only providing tangible benefits to the public sector, voluntary participation by banks and other financial institutions may wane.

Fortunately for all concerned, a number of initiatives are underway to improve the effectiveness of PPPs particularly and for the global AML regime generally.

Government initiatives—including implementation of even more innovative approaches to PPPs and new laws and regulations that further break down barriers to collaboration—hold great promise for financial institutions. Banks can also take a number of steps to ensure that their participation in PPPs returns the greatest value.

Europol's Financial Intelligence PPP (EFIPP)

While not specifically designed to address concerns of competing priorities among national-level PPPs, the PPP created by Europol demonstrates the advantages of a multi-national PPP. EFIPP is constituted of:

EFIPP has developed detailed typologies, including geographical indicators, on a wide range of topics, including organized crime, criminal and money laundering trends, financial flows related to "laundromats," virtual currencies, terrorism financing, tax fraud and COVID-19 related fraud.11 Of additional note, an EFIPPP working group has conducted a mapping exercise on legal gateways to share information within a financial institution (intra-group), between EU member states and countries with equivalent personal data-protection rules, and with countries with non-equivalent personal data-protection rules.12

Enterprise-wide SAR sharing

US regulators have allowed branches and subsidiaries of certain non-US financial institutions to share SARs generated in the US with their non-US parent or head office.13 However, it was only after the passage of the January 2021 Anti-Money Laundering Act that US-headquartered financial institutions had an opportunity to share SAR information with their overseas affiliates through a required pilot program.14 To further encourage information-sharing, this Act also granted SARs filed under non-US regimes the same confidential status as if the SAR had been filed in the US.15

The UK has made an effort in recent years to facilitate SAR information sharing between UK regulated entities. The Criminal Finances Act 2017 introduced a mechanism16 by which regulated banks and financial institutions can share information about suspected money laundering in conjunction with the UK FIU. This allows for the submission of joint disclosure reports (referred to as "super SARs"), with the aim of providing a fuller picture of the suspected activity to enforcement agencies. This significantly broadened the permissible disclosure regime in the UK, which primarily focused on intra-group disclosure.17

Similarly, Germany has implemented certain exceptions to the prohibition on disclosure of information in SAR filings, which are intended to facilitate the exchange of information with government agencies and other obliged parties for the purpose of preventing money laundering or terrorism financing. Information sharing is allowed between obliged parties of the same group,18 including between parent companies and their third country subsidiaries, provided that the parent has implemented group-wide money laundering prevention measures.19 In addition, obliged parties may, under certain conditions, share information with other EU or third country obliged parties, provided they are involved with the same contracting party or the same transaction.20 This is to enable the obliged parties to better assess risks, identify suspicious behavior and intervene in suspicious conduct before a money laundering risk materializes.

Co-location of analysts

Australia and the Netherlands have developed interesting approaches to the PPP model, whereby analysts from the public and private sector work together on a daily basis. This model is expected to allow the participants to develop a stronger shared understanding of the threats posed by money laundering, terrorism financing and serious financial crime. Co-location also has tactical advantages, as it allows more agile collaboration among participants on time-sensitive cases. With such a tactical focus, this model also allows for more contemporaneous and more detailed feedback on specific SARs as they relate to current cases.

Prioritization of AML resources

In the last year, a movement has grown in the US to prioritize effort in AML compliance, culminating in the passage of the Anti-Money Laundering Act, which requires the US government to identify national-level AML priorities that financial institutions must incorporate into their AML compliance programs.21 While these priorities and their implementation must still be fleshed out through regulations, the expectation appears to be that financial institutions prioritize their limited resources on the national-level priorities.22 To be at all effective, these priorities would also have to extend to how FinCEN Exchange (the US PPP) engagements are organized. Many financial institutions may find engagement in the FinCEN Exchange even more valuable, because the integration of priorities at a more tactical level will give even greater clarity as to where the financial institutions should prioritize their efforts and resources.

Even if a bank is not able to avail itself of the initiatives described above, there are several actions it can take to better leverage the capabilities of a PPP to meet its AML compliance objectives:

1 Note that the requirement can also be referred to as a suspicious transaction report, but we focus on the slightly broader obligation to report suspicious activities.

2 See: British Banker’s Association, "Response to Cutting Red Tape Review: Effectiveness of the UK’s AML regime," Jun. 21, 2018, and Bank Policy Institute, "Getting to Effectiveness – Report on U.S. Financial Institution Resources Devoted to BSA/AML & Sanctions Compliance," Oct. 29, 2018.

3 Per annual reports on SAR filings produced by the National Crime Agency, the UK’s FIU. The reporting year runs from April to March each year.

4 FinCEN, "SAR Statistics," filings for all industries, reviewed on Jun. 7, 2021.

5 See, Nick J. Maxwell and David Artingstall, Occasional Paper, "The Role of Financial Information-Sharing Partnerships in the Disruption of Crime," Royal United Services Institute for Defence and Security Studies, Oct. 2017, p. vi; see also for example the 2019 annual report of the German FIU, p. 20, according to which only approx. one third of all SARs were disseminated to law enforcement authorities (compared to 58% in 2018)

6 Royal United Services Institute (RUSI) Future of Financial Intelligence Sharing (FFIS), "Survey Report: Five years of growth in public–private financial information-sharing partnerships to tackle crime," Aug. 2020, p. 19.

7 Royal United Services Institute ("RUSI") Future of Financial Intelligence Sharing ("FFIS"), "Survey Report: Five years of growth in public–private financial information-sharing partnerships to tackle crime," Aug. 2020, p. 19.

8 See, Financial Action Task Force, "Anti-money laundering and counter-terrorist financing measures: United Kingdom Mutual Evaluation Report," Dec. 2018, p. 92.

9 The National Defense Authorization Act of FY 2021, which was enacted in January 2021, codified the FinCEN Exchange in law at Section 6103.

10 While involvement in PPPs is generally voluntary, not every bank or financial institution may be given the opportunity to participate. Many PPPs only permit a relatively small number of financial institutions to participate, to keep costs low and protect the confidentiality of any information that is shared.

11 RUSI, p. 80.

12 RUSI, p. 81.

13 FinCEN, Board of Governors of the Federal Reserve System, Federal Deposit Insurance Corporation, Office of the Comptroller of the Currency, and Office of Thrift Supervision, "Interagency Guidance on Sharing Suspicious Activity Reports with Head Offices and Controlling Companies," Jan. 20, 2006.

14 P.L. 116-283 § 6212.

15 P.L. 116-283 § 6109.

16 Section 11 of the Criminal Finances Act 2017 amended the Proceeds of Crime Act 2002 by inserting Sections 339ZB – 339ZG. See, White & Case LLP, "The Making of a Super-SAR: A Case Study," Feb. 1, 2018, and Home Office Circular: Criminal Finances Act 2017, "Money Laundering: Sharing of Information within the Regulated Sector."

17 Per sections 333B-333D of the Proceeds of Crime Act 2002.

18 Sec. 47 (2) no. 2 German Money Laundering Act (Geldwäschegesetz, GwG).

19 Sec. 47 (2) no. 3 GwG.

20 Sec. 47 (2) no. 5 GwG.

21 P.L. 116-283 § 6101.

22 On June 30, 2021, FinCEN released its priorities, which include corruption; cybercrime, including relevant cybersecurity and virtual currency considerations; foreign and domestic terrorist financing; fraud; transnational criminal organization activity; drug trafficking organization activity; human trafficking and human smuggling; and proliferation financing. FinCEN, "Anti-Money Laundering and Countering the Financing of Terrorism National Priorities," June 30, 2021.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP

View full image: Figure 1: Recent growth in SAR filings (PDF)

View full image: Figure 1: Recent growth in SAR filings (PDF)

View full image: Countries with AML PPPs (PDF)

View full image: Countries with AML PPPs (PDF)