Our Public Takeover Report provides an overview of trends and legal developments relating to public takeovers in Germany in 2025.

In this issue:

- The Most Significant Public Takeovers in 2025

- Aftermath of 2024 Public Takeover Activities in 2025

- Review of the major delisting proceedings and other acquisition offers in 2025

- Key figures of the takeover market in 2025

- Prohibitions and Exemptions

- Key aspects of the takeover transactions

- Adjustments to the legal framework in takeover law

- Stock Price and Valuation – New Developments

- Judgments relevant for takeovers in 2025

- Outlook

Compared to the previous year, 2025 was a relatively quiet year in the market for public takeovers, with only 20 proceedings, whereas 32 proceedings were recorded in 2024. The German stock market's very strong performance, despite weak economic data, resulted in increased caution among potential bidders. The widely noted takeover of Commerzbank by UniCredit, initially announced in September 2024, has once again attracted public attention following the announcement of an exchange offer on March 16, 2026.

Notwithstanding the overall weakness in the market, it remains worthwhile to examine the particular characteristics of public takeovers in 2025 as well as the most recent legal developments.

The Most Significant Public Takeovers in 2025

Zalando acquires About You

The public M&A year began with the publication of Zalando's takeover bid for About You; the transaction was prepared with the signing of a business combination agreement in December 2024. Through the acquisition, Zalando seeks to unlock substantial value creation opportunities and is particularly focused on About You's corporate client segment as well as its slightly younger target audience, with the objective of further expanding Zalando's customer base. On November 6, 2025, it was announced that the statutory squeeze-out of About You had become effective and, at the same time, the listing of About You shares on the regulated market (Prime Standard) had been terminated. White & Case advised About You on both the public tender offer and the statutory squeeze-out.

Takeover battle for ProSiebenSat.1

The takeover process that arguably garnered the most public attention in 2025 was the bidding contest for ProSiebenSat.1. Italian MediaForEurope Holding (MFE), which already held approximately 30% of ProSiebenSat.1's share capital at the time of the offer document's publication, engaged in a competitive bidding process with its Czech rival, PPF, which held 15.7% of the company. PPF submitted a partial tender offer to ProSiebenSat.1 shareholders at EUR 7.00 per share, prompting MFE to enhance its own mixed cash and exchange offer from EUR 4.48 plus 0.4 MFE shares to the original cash consideration plus 1.3 MFE shares. PPF's offer was structured to acquire a 29.99% stake, and thus not to acquire a controlling interest. Ultimately, PPF decided not to pursue its plan further and sold its 15.7% stake in ProSiebenSat.1 to MFE. As a result, MFE was able to increase its stake in ProSiebenSat.1 to 75.6% during the extended acceptance period, which ran until early September 2025.

MFE's holding company has announced plans to establish a pan-European media network to compete with international players such as Netflix.

JD.com acquires Ceconomy

The acquisition of Ceconomy, the parent company of MediaMarkt and Saturn, by the Chinese conglomerate JD.com represented the largest transaction by volume in 2025, with a deal value of EUR 2.253 billion. The transaction was subject to considerable public debate and was even under discussion in the German parliament (Bundestag) in January 2026. A parliamentary inquiry questioned whether the Federal Cartel Office combats global cartels with a German nexus and whether the potential displacement of German electrical and electronics manufacturers—such as Miele, Bosch, Liebherr, Siemens, Rowenta, and Loewe—was considered during JD.com's acquisition planning. Additionally, members of parliament wanted to know whether the Directorate-General for Competition of the European Commission was involved in the review of this transaction. White & Case advised JP Morgan, acting as Ceconomy's financial advisor, on the transaction.

Ceconomy announced in early December 2025 that JD.com had secured a total shareholding of 82.5% in Ceconomy as result of the public tender offer. As of early April, completion of the transaction remained subject to foreign direct investment approvals and clearance under the EU Regulation on foreign subsidies distorting the internal market (Foreign Subsidies Regulation, "FSR"). Antitrust approvals had already been obtained at that time. According to JD.com, the acquisition is intended to support the expansion of its omnichannel service platform and retail expertise, which will be leveraged to benefit the Ceconomy Group. Ceconomy is expected to be delisted in the second quarter of 2026.

BioNTech Acquires CureVac via an Exchange Offer

A notable takeover between two German companies occurred outside the scope of the German public takeover market. In December 2025, BioNTech announced its acquisition of CureVac, a company based in Tübingen, following the successful completion of an exchange offer. In total, 86.75% of CureVac's shares were exchanged for BioNTech shares. As both companies are listed exclusively in the United States on Nasdaq, the rules governing the acquisition of listed companies in Germany did not apply to this transaction. White & Case acted as legal advisor to Berenberg, which served as the exchange agent for the transaction.

Aftermath of 2024 Public Takeover Activities in 2025

Several takeover proceedings from 2024 were successfully concluded in 2025.

ADNOC / Covestro

The acquisition of Covestro by the Abu Dhabi National Oil Company (ADNOC), based in the United Arab Emirates, also attracted significant public attention in 2025. As part of the acquisition in October 2024, ADNOC had acquired nearly 70% of the voting rights. At the end of July 2025, the European Commission initiated an in-depth review of the planned acquisition under the Foreign Subsidies Regulation, ultimately granting conditional approval in November 2025. In early January 2026, it was announced that ADNOC had increased its shareholding to 95.1% of Covestro's shares. At the forthcoming Covestro Annual General Meeting in April 2026, it is anticipated that a resolution will be adopted to exclude minority shareholders by way of a squeeze-out.

Will UniCredit acquire Commerzbank?

In 2025, the Italian UniCredit's efforts to acquire Commerzbank continued to be a topic of discussion in the market. On March 16, 2026, UniCredit published the principal terms of its proposed takeover offer to the shareholders of Commerzbank. Since UniCredit's acquisition of approximately 20% of Commerzbank's shares in September 2024, the German government, Commerzbank, and employee representatives had initially expressed clear opposition to a potential takeover by UniCredit. Nevertheless, UniCredit initiated a shareholder control procedure, which received a favorable decision from the European Central Bank in March 2025. In April 2025, the Federal Cartel Office approved UniCredit's increase of its stake in Commerzbank to 29.99% and confirmed that the transaction did not require notification to the European Commission, as the acquisition of up to 29.99% of the shares did not yet constitute "control" within the meaning of the EU Merger Regulation. By the end of July 2025, UniCredit announced that it had increased its holding to 29.26% through shares and financial instruments.

In response, during the second half of 2025, Commerzbank implemented additional measures to make a takeover more challenging. Notably, the bank launched the largest share buyback program in its history, acquiring over 4% of its own shares in 2025, with a further share buyback program scheduled for 2026. The bank also undertook internal efficiency measures. These actions, together with robust annual results, led to a significant increase in Commerzbank's share price—more than doubling since January 2025—thereby substantially raising the cost of any potential takeover.

The Federal Republic of Germany continues to hold a stake of more than 10%; BlackRock holds more than 5%, and other institutional investors hold approximately 33%.

On March 16, 2026, UniCredit announced a voluntary public takeover offer, which is to be structured as an exchange offer. Pursuant to the terms of the offer, Commerzbank shareholders would receive 0.485 new UniCredit shares for each Commerzbank share tendered, equating to a takeover price of approximately EUR 30.80 per share, which represents the statutory minimum price. With this low-ball offer, UniCredit seeks to surpass the 30% control threshold under takeover law and to initiate discussions with Commerzbank's management. Following the publication of the principal terms of the takeover offer, Commerzbank stated only that the offer had not been coordinated with the bank. Both the German government and union representatives have reiterated their opposition to a takeover of Commerzbank.

Review of the major delisting proceedings and other acquisition offers in 2025

In 2025, seven out of the twenty offers published under the German Securities Acquisition and Takeover Act (Wertpapiererwerbs- und Übernahmegesetz, WpÜG) were aimed to delist the respective target companies. By May of that year, three major companies—Metro, Biotest, and CompuGroup Medical—had withdrawn their shares from trading on the regulated market.

Metro

Metro's principal shareholder, EP Global Commerce—which is majority-owned by Czech investor Daniel Křetínský and held a 49.99% interest in Metro's share capital as of early 2025—submitted a delisting offer to Metro shareholders to enable the implementation of a necessary transformation process at Metro. According to EP Global Commerce, such a process could not be effectively carried out under the constraints imposed by the expectations of the capital markets. The delisting offer had a transaction volume of EUR 974 million.

Biotest

Grifols, a Spanish healthcare company, published a similar rationale in its delisting offer to Biotest shareholders. Grifols and Biotest were in agreement that the public capital markets were no longer an appropriate environment for the pursuit of Biotest's future strategic objectives. Grifols had acquired a stake in Biotest in 2021, and Biotest's shares were delisted from the Frankfurt Stock Exchange in early July 2025. The total market value at the time of the delisting offer was EUR 677 million.

CompuGroup Medical

In contrast, private equity investor CVC completed its takeover offer for CompuGroup Medical in December 2024. The company's stock exchange listing was subsequently discontinued in June 2025, following the successful implementation of a delisting offer with a transaction volume of EUR 895 million (excluding non-acceptance agreements). In its delisting offer, CVC cited anticipated cost savings resulting from the termination of the stock exchange listing, as well as the availability of sufficient alternative sources of financing.

Francotyp-Postalia

Finally, it is noteworthy to mention a delisting offer of minor transaction volume, in which Francotyp-Postalia Holding acted as both the bidder and the target company. Subsequently, certain individual shareholders published a partial acquisition offer, contending that the delisting offer was inappropriate for various reasons. Notwithstanding the objections raised by these shareholders, the listing of Francotyp-Postalia shares was discontinued on August 28, 2025.

United Internet / 1&1

In contrast, United Internet has indicated its intention to maintain the stock market listing of 1&1 shares for the time being, while further increasing its stake in 1&1 through a partial tender offer. By April 2025, United Internet had already surpassed the 80% ownership threshold in 1&1 by accepting off-market offers. In pursuit of a higher shareholding, United Internet launched a public partial offer with a transaction volume of EUR 306 million. According to United Internet, this offer provided all 1&1 shareholders an attractive opportunity to achieve liquidity at a significant premium. As a result of the partial tender offer, United Internet increased its stake to 85.1% of the share capital. It is also notable that Ralph Dommermuth serves as CEO of both the bidder and the target company.

Key figures of the takeover market in 2025

View full image

View full image

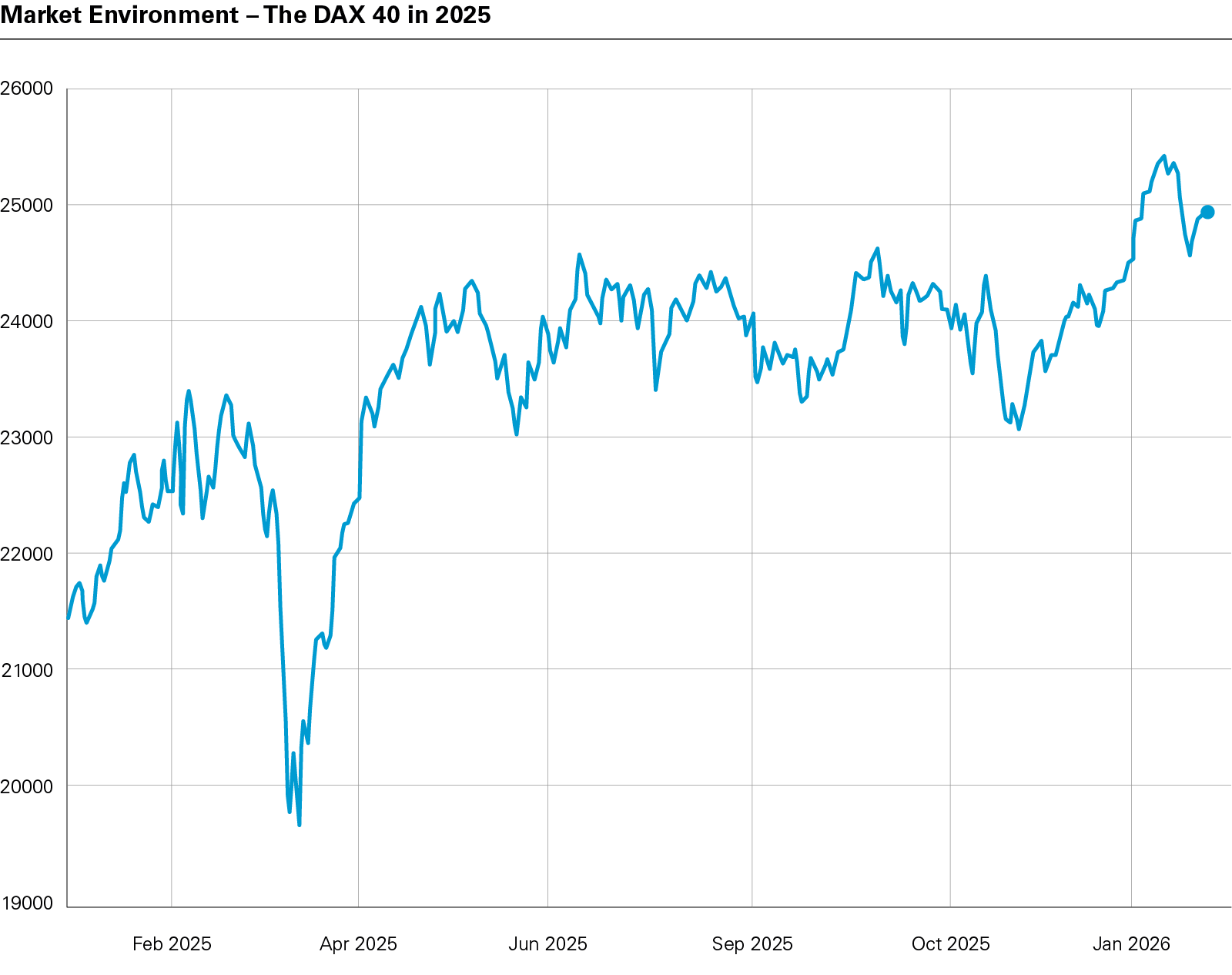

In 2025, the DAX 40 index increased by more than 4,500 points (opening at 19,923.07 on January 2, 2025, and closing at 24,490.41 on December 30, 2025), representing a gain of over 20%, mirroring the performance of the previous year. Nevertheless, investor sentiment was tested by significant market volatility, with a spread of 6,281 points between the year's high and low.

Type of Offer

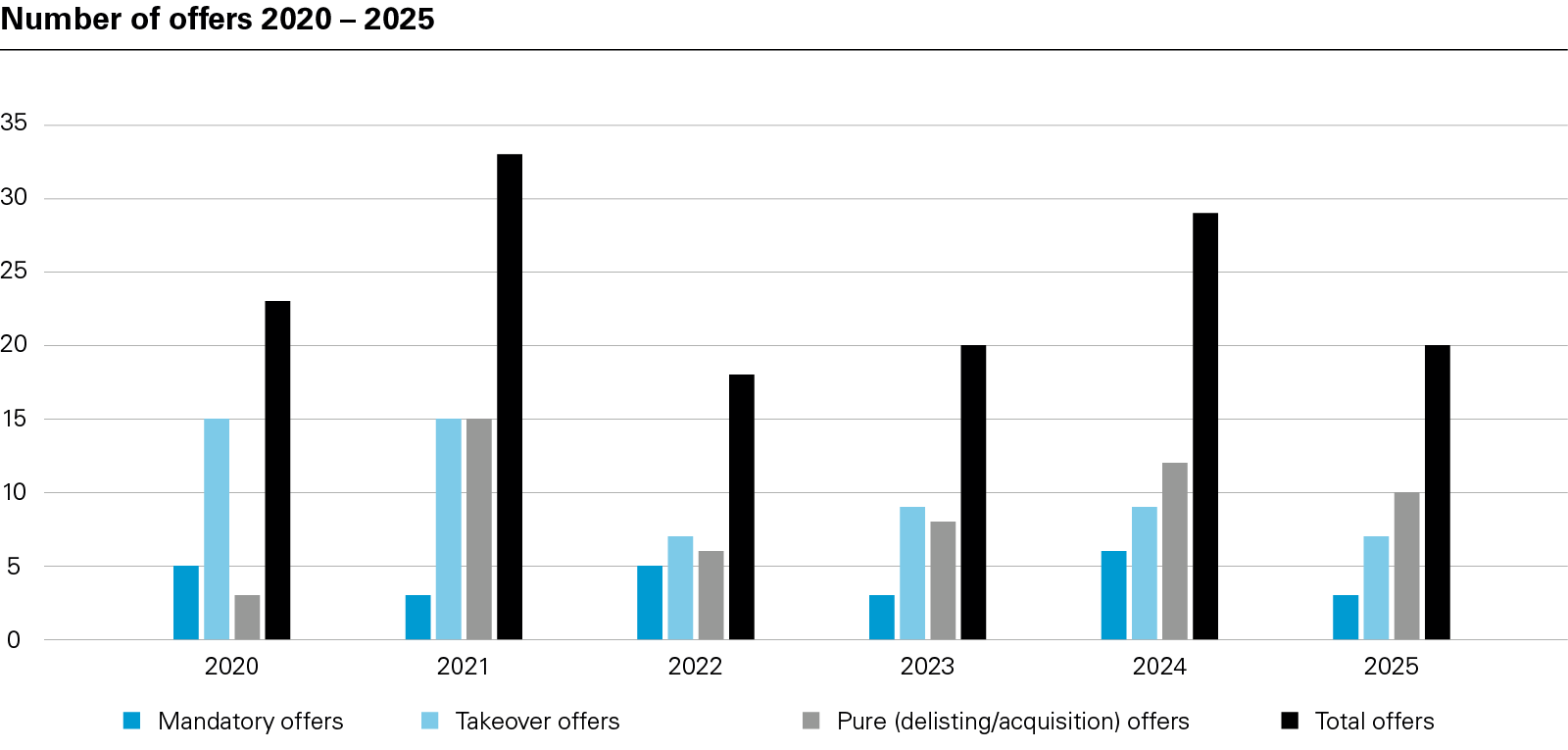

Following a surge in public takeover transactions in 2024—when the total number rose by more than one-third compared to the prior year (32 transactions in 2024 versus 20 in 2023)—the number of transactions in 2025 declined to the 2023 level, with a total of 20 transactions. Takeover proceedings involving high transaction volumes remained rare in 2025. Specifically, the following were published:

- Seven voluntary takeover bids, one of which was combined with a delisting offer;

- Three mandatory offers;

- Three partial acquisition offers within the meaning of section 19 of the WpÜG, each aimed at acquiring a defined maximum number of shares; and

- seven delisting offers (including the combined takeover and delisting offer by Leonardo Art Holdings to the shareholders of artnet).

View full image

View full image

In addition to the total number of transactions, the proportion of delisting offers among the total number of offers regulated under the WpÜG declined to 35% in 2025 (2024: 16 delisting offers, or 50% of all WpÜG-regulated offers). It remains to be seen whether this development marks a lasting shift away from the "delisting trend" observed in recent years.

Bidder Structure

Examining the bidder structure in 2025, the declining significance of private equity investors is particularly notable. By contrast, the role of strategic investors increased markedly compared to previous years: all public takeovers with transaction volumes exceeding EUR 500 million were executed by strategic investors. These included takeover bids such as Zalando/About You, JD.com/Ceconomy, the competing bids for ProSiebenSat.1, and the delisting offers by Grifols for Biotest and EP Global Commerce for Metro. The only exceptions were Warburg Pincus's takeover bid for PSI Software and the delisting of CompuGroup by CVC Capital Partners.

Transaction Volumes

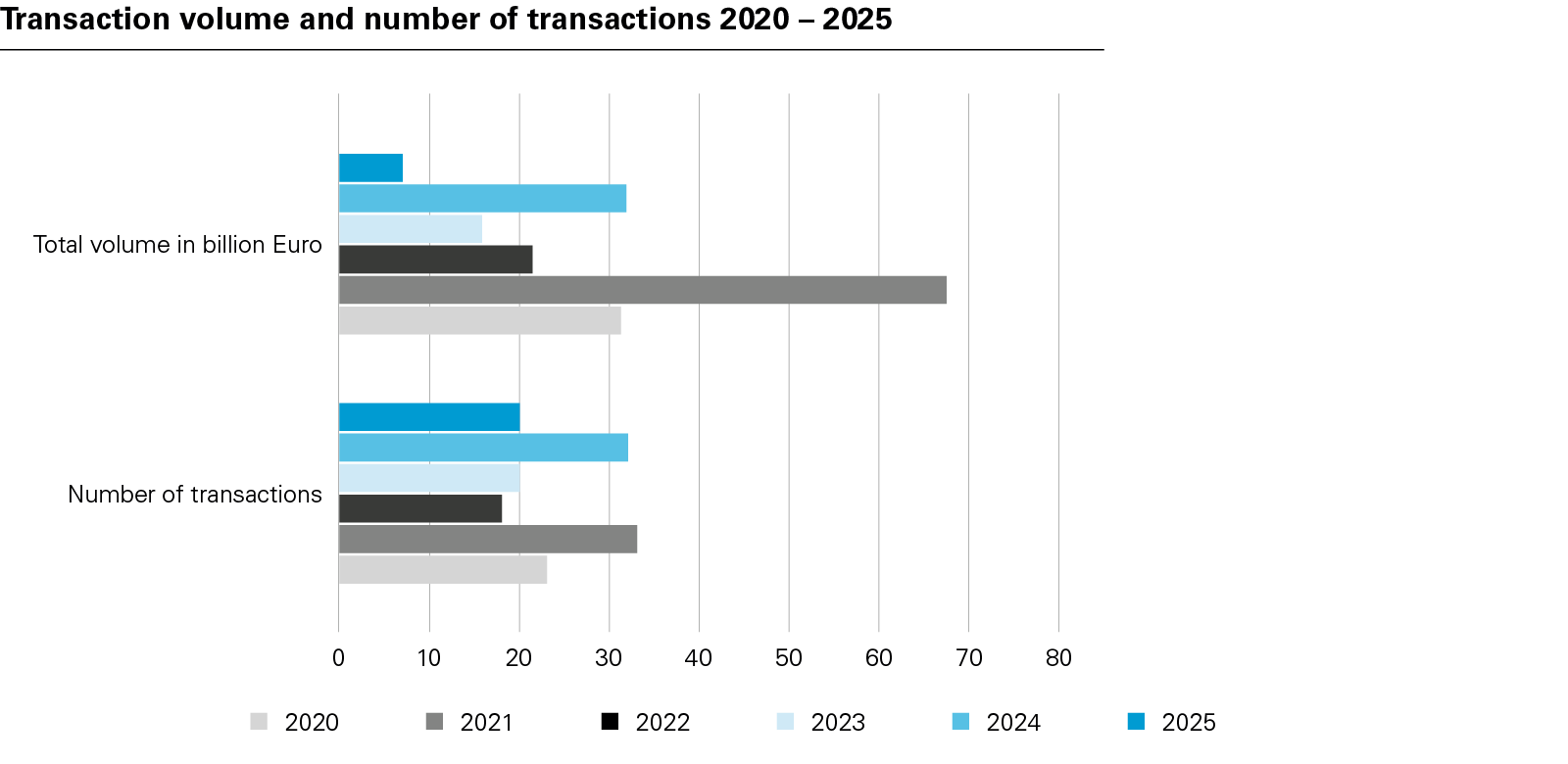

The total volume of public takeover transactions in Germany - calculated based on the maximum consideration payable, including transaction costs but excluding non-tender agreements - declined sharply in 2025 to just EUR 8.79 billion, compared to EUR 31.78 billion in the previous year (2024), representing a decrease of approximately 76%. When factoring in non-tender agreements secured by depositary lock-up agreements, which further reduce the effective transaction volume, the total for 2025 is effectively halved to EUR 4.3 billion. Accordingly, 2025 marks the lowest total transaction volume observed in recent years by far.

View full image

View full image

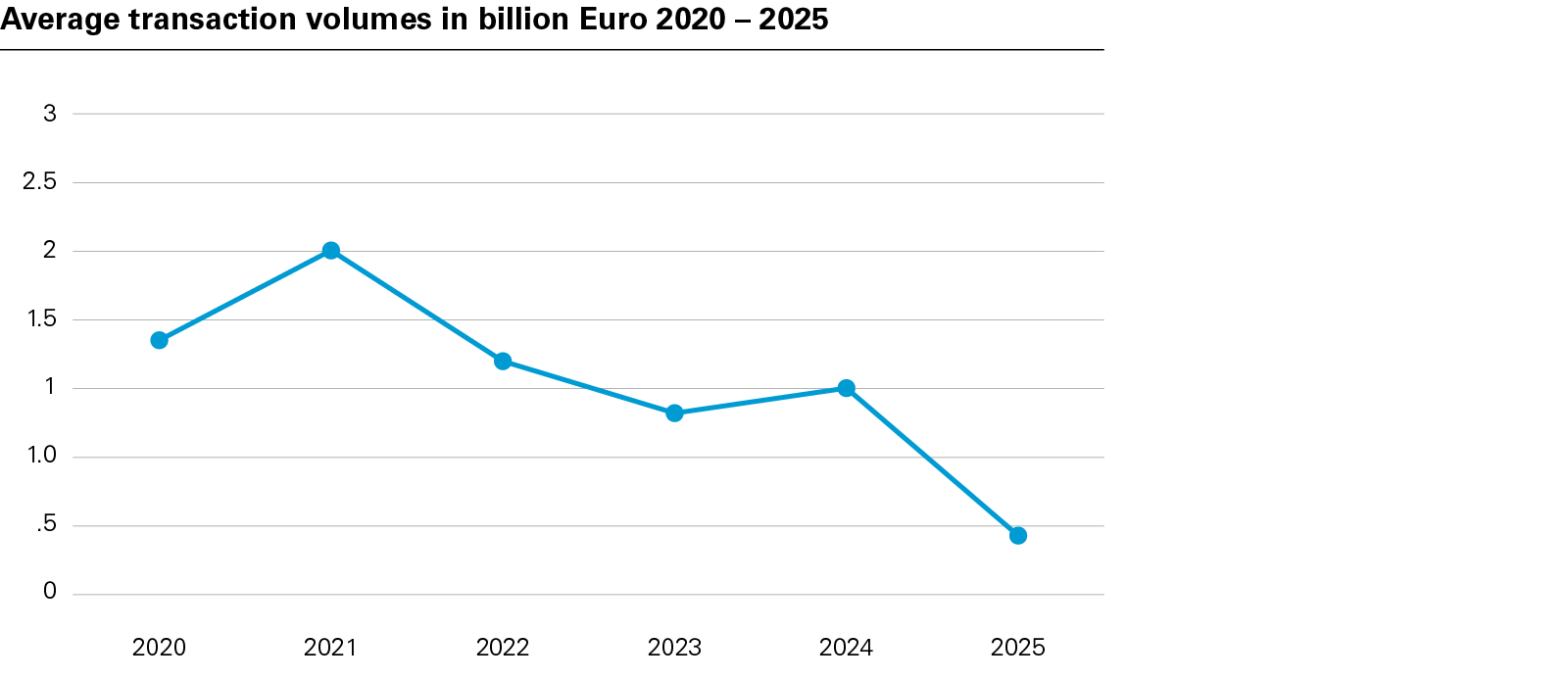

With the takeover bids for Ceconomy (approximately EUR 2.25 billion) and About You Holding (approximately EUR 1.16 billion), only two transactions in 2025 exceeded the EUR 1 billion threshold. These two offers alone, with a combined volume of approximately EUR 3.41 billion, represented nearly 45% of the total transaction volume for the year. The average transaction volume in 2025 was approximately EUR 380 million, which is significantly lower than the average observed over the past five years.

View full image

View full image

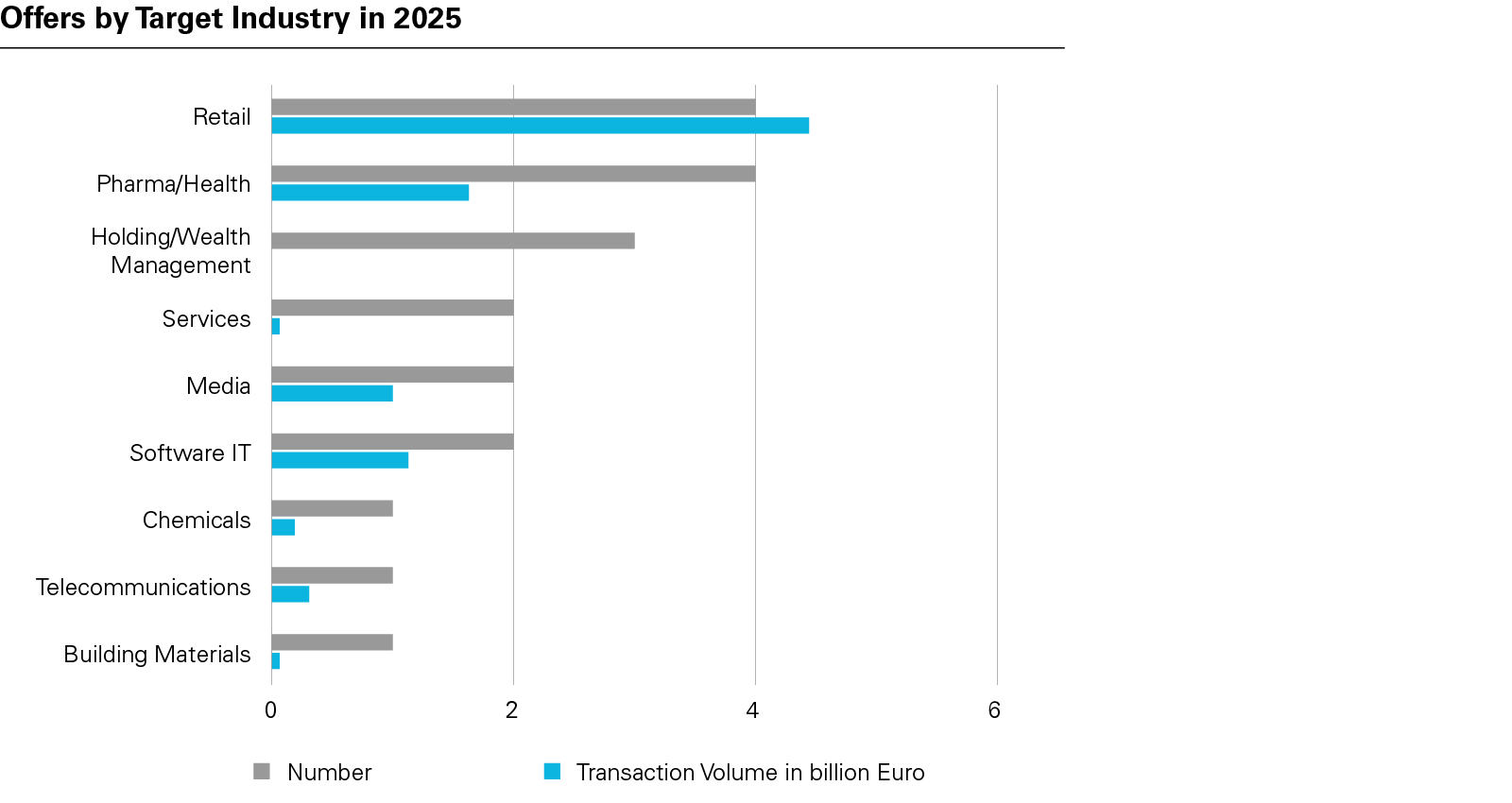

Industry Focus of Target Companies

At first glance, there was no distinct sector focus in 2025; target companies were drawn from a broad range of industries, including software/IT, private equity, retail, services, pharmaceuticals, art, specialty chemicals, building materials, telecommunications, and media. However, an analysis of transaction volumes reveals a clear emphasis on target companies in the pharmaceuticals/healthcare and retail sectors.

The pharmaceuticals/healthcare sector, including private equity firms specializing in healthcare, was particularly popular with investors. Two offers targeted companies operating directly in the healthcare sector (Biotest and Pharma SGP Holding), while two additional offers involved private equity firms with a healthcare focus (Leo International Precision Health and CompuGroup Medical). As a result, 20% of all transactions in 2025 involved target companies in the pharmaceuticals/healthcare sector, with a combined transaction volume of approximately EUR 1.63 billion.

View full image

View full image

Another focus was evident in the retail sector, particularly in terms of the number of offers, which likewise totaled four (20%). This sectoral focus is even more evident when considering transaction volume: transactions in the retail sector - including the two billion-euro offers for Ceconomy and About You Holding - amounted to approximately EUR 4.44 billion, representing well over half of the total transaction volume in 2025.

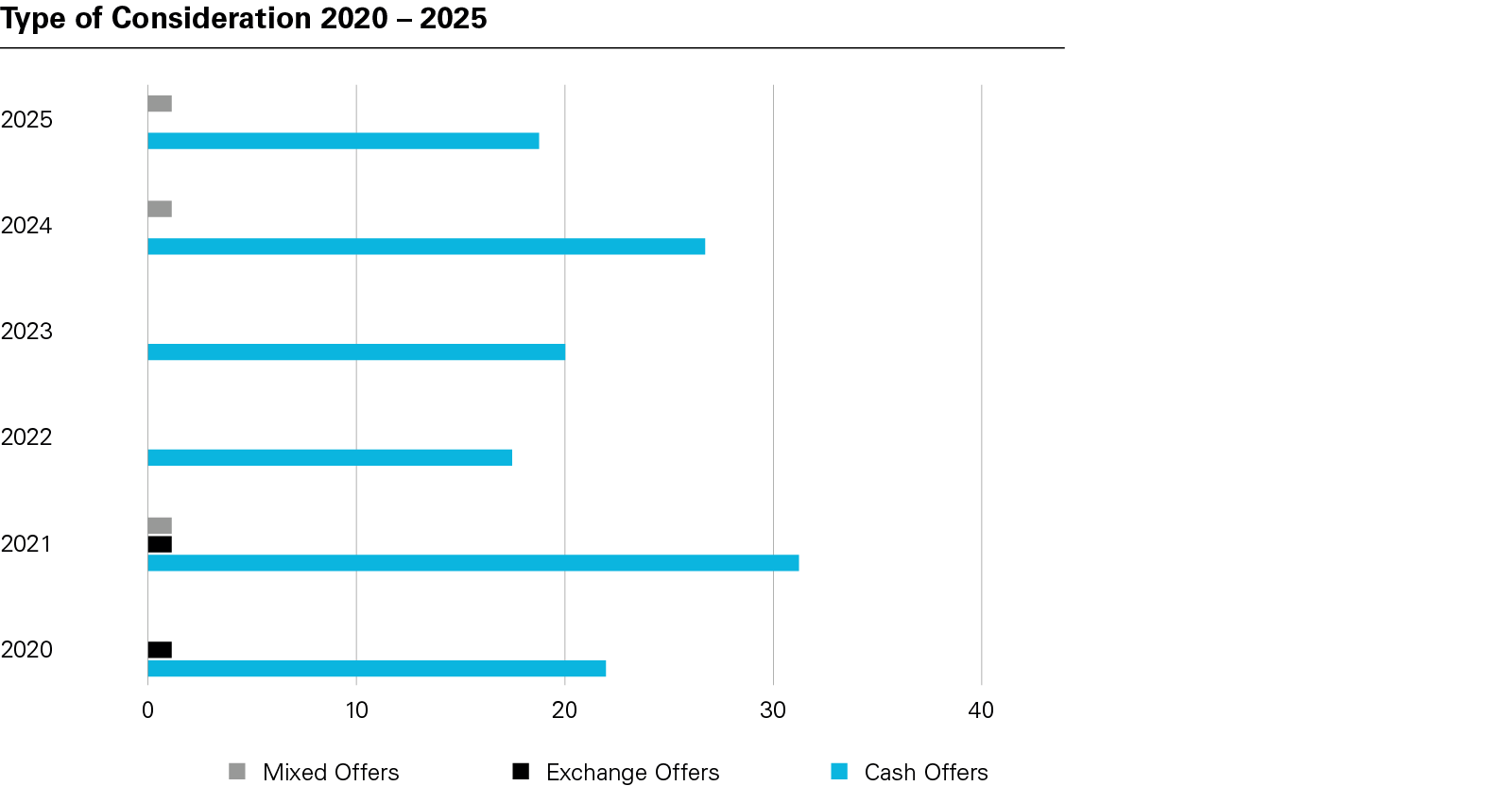

Consideration

In 2025, cash offers continued to predominate, constituting 95% of all transactions (19 out of 20).

View full image

View full image

Consistent with the preceding three years, there was not a single pure exchange offer. The only transaction involving mixed consideration was the takeover bid by the Italian company MFE for ProSiebenSat.1.

Are bidders still paying premiums in the current environment?

As in previous years, only a limited number of bidders offered attractive premiums over the relevant stock market prices used to calculate the offer price1 with the intention of making their offers more appealing to the target company's shareholders. The highest premiums over the average stock market price determined by BaFin continued to be paid in voluntary takeover bids; by contrast, premiums remained the exception in mandatory and acquisition offers.

Voluntary Takeover Offers

- Zalando paid the highest premium to About You shareholders, offering 107% above the three-month average price; however, this premium corresponded to the highest pre-acquisition price paid or agreed upon within the meaning of section 4 of the WpÜG Offer Regulation.

- Similarly, JD.com's takeover offer for Ceconomy shareholders included a premium of 33.7% over the three-month average price.

- Warburg Pincus paid a premium of 62.2% over the relevant average price to PSI Software shareholders.

- In the competing bid for ProSiebenSat.1, PPF offered a premium of 21.11% compared to the initial offer from the Italian bidder MFE, who initially attempted to acquire ProSiebenSat.1 shares without offering a relevant premium. Ultimately, MFE increased its offer consideration and paid a premium of 49.9% over the volume-weighted average stock price for the last three months.

Delisting Offers

- Historically, delisting offers have not typically included premiums. Notable exceptions in 2025 included:

- The acquisition of Metro AG by EP Global Commerce, where common shareholders received a premium of 23.38% over the six-month average share price.

- The delisting of CompuGroup Medical by CVC Capital Partners, which included a premium of 5.6% pursuant to section 5 of the WpÜG Offer Regulation.

- The delisting of Biotest AG by Grifols, where common shareholders received a premium of 5.2%.

Mandatory Offers

The pricing of the three mandatory offers published in 2025 was determined by specific circumstances in each case:

- Obotritia Capital's mandatory offer for Readcrest Capital was based on the acquisition of control following a capital increase in kind after a capital reduction, which significantly influenced the offer price.

- Apeiron Investment Group's mandatory offer for Heidelberger Beteiligungsholding was published at the determined average price without a premium, resulting in only 1.63% of the share capital being tendered.

- In the case of the offer by the Taiwanese bidders for Leo International Precision Health, a company valuation was required due to insufficient trading volume. The resulting premium of 12.7% over the determined enterprise value corresponded to the highest pre-acquisition price paid.

Prohibitions and Exemptions

Prohibition of an Offer

In 2025, BaFin issued one prohibition on an offer. However, it was not the publication of an offer document that was prohibited. Instead, by way of a prohibition notice dated June 11, 2025, BaFin prohibited the purchase offer by CAUSA Verwaltungs GmbH to the shareholders of Mutares, which had been published in the Federal Gazette on May 23, 2025. The bidder had failed to submit an offer document containing the required information to BaFin for approval, and the prohibition was therefore based on section 15 para. 1 no. 1 section 3 WpÜG. The circumstances of the case appear somewhat unusual, as the bidder's intention was likely only to invite offers. Nevertheless, section 17 WpÜG expressly prohibits even such so-called "invitatio ad offerendum."

Exemptions from the Obligation to Make an Offer

In 2025, BaFin granted exemptions from the obligation to publish and submit an offer pursuant to section 37 WpÜG in seven cases.

Two of these exemption notices related to the Westwing Group's share buyback program and the subsequent cancellation of shares by the target company. The exemptions were granted on the basis of section 9, sentence 1, no. 5 of the WpÜG Offer Regulation (WpÜG-Angebotsverordnung, WpÜG-AngebVO), which is designed to ensure that an offer is not required solely because a shareholder acquires control within the meaning of section 35 WpÜG without any action on their part. In the first case, the acquisition of control by the applicant, Rocket Internet, would have resulted from the reduction of Westwing Group's share capital following the cancellation of treasury shares; at the time of the application, Rocket Internet held 29.95% of the target company's share capital and voting rights. The second exemption was granted in favor of Global Founders and two other applicants, who, as the direct or indirect parent companies of Rocket Internet, were attributed voting rights in Westwing Group pursuant to section 30 para. 1 sentence 1 no. 1 sentence 3 in conjunction with section 2 para. 6 WpÜG and section 290 of the German Commercial Code (HGB).

Two additional exemptions relating to the target companies About You and OHB were granted pursuant to section 36 No. 3 of the WpÜG, as control was acquired, at least in part, through an intra-group restructuring.

In the case of Helvetia Holding's acquisition of control over OVB Holding Köln, the exemption was granted under section 37 para. 1 alternative 2, para. 2 of the WpÜG in conjunction with section 9 sentence 2 no. 3 of the WpÜG-AngebVO. This was because the bidder indirectly acquired control of the target company through the acquisition of control elsewhere, and the book value of the company's interest in the target company was less than 20% of the company's total book assets.

Two further decisions addressed restructuring cases within the meaning of section 9 sentence 1 no. 3 of the WpÜG-AngebVO.

Key aspects of the takeover transactions

Structure of the Conditions

As a general rule, both the bidder and the target company are interested in the success of the takeover offer and prefer not to make the offer subject to conditions that are not legally required. As a rule, the only legally required conditions are regulatory approvals under antitrust and foreign trade laws, as well as under the Foreign Subsidies Regulation. In practice, for voluntary takeover offers, the bidder and the target company negotiate the principal terms of the takeover - including any conditions - within the framework of a Business Combination Agreement or Investment Agreement, which are subsequently reflected in the offer document.

Currently, very few bidders include a minimum acceptance threshold as a condition; instead, they generally secure a minimum stake in advance through shareholder agreements. An exception was Warburg Pincus's takeover offer for PSI Software, which included a minimum acceptance threshold of 50%, a threshold that was successfully exceeded. In the case of H&R Holding's offer to acquire shares from the shareholders of H&R—which ultimately resulted in the sale of shares to the controlling shareholder of the target company—the bidder waived the originally contemplated minimum acceptance threshold of 85% during the acceptance period.

Only two of the partial takeover offers included so-called Material Adverse Change (MAC) conditions: Both PPF's partial offer for ProSiebenSat.1 and United Internet's partial offer for 1&1 made the offer conditional on the DAX or SDAX index value; in addition, United Internet's offer included a minimum EBITDA requirement for the 1&1 Group as a further condition.

Statements by the Target Company

In both takeover and delisting offers, the bidder and the target company customarily agree on the principal terms of the transaction in advance. Nearly all delisting and takeover offers in 2025 were prepared on the basis of an investor or delisting agreement. Only the special case of the delisting offer regarding Francotyp-Postalia (where the bidder and target company were the same entity) was not accompanied by a corresponding preliminary agreement.

As a result, management's support for the offer is generally secured prior to its public announcement, and the statements issued pursuant to section 27 WpÜG typically include a positive recommendation to shareholders to accept the offer. The only exception was the takeover of ProSiebenSat.1, where, at the time of issuing its statement on the initial offer by the Italian company MFE, management was already aware that a competing partial offer by the Czech competitor PPF was based on a higher valuation. Accordingly, the consideration in MFE's initial offer was deemed inadequate. After the offer price was increased, the Management Board and Supervisory Board subsequently recommended acceptance of the MFE offer in an additional statement.

In three cases in 2025, statements from the works councils were published alongside the target company's statement - specifically, from the works councils of About You, Biotest, and Metro - in which expectations and concerns were expressed in each instance.

As in previous years, fairness opinions are typically obtained by the management of the target company, particularly in the context of voluntary takeover offers. The only exception was the voluntary takeover offer by Obotritia Capital for Readcrest Capital, as this involved a restructuring with a capital reduction followed by a capital increase in kind. Other instances where a fairness opinion was not obtained pertained to mandatory, acquisition, and delisting offers.

Transaction Financing

With regard to the financing of transactions by the bidders, two instruments in particular emerged as market-defining in 2025.

Bank loans: 13 out of 20 transactions were at least partially financed through one or more bank loans (2024: 13 out of 32 transactions), typically in the form of syndicated loans involving multiple financial institutions. By contrast, the percentage of transactions financed at least in part by the bidders' shareholders declined significantly in 2025, with seven out of 20 transactions compared to the previous year (2024: 16 out of 32 transactions).

Non-Tender Agreements: Comprehensive non-tender agreements are increasingly becoming the market standard. These are typically accompanied by corresponding account freeze agreements or freeze instructions issued to the custodian banks of the affected shareholders, as well as contractual penalties in the event of a breach. In this way, the actual financing requirement was reduced in 11 of the 20 transactions in 2025 (2024: 11 of 32 transactions). BaFin now accepts that no financing measures need to be demonstrated for shares that cannot be accepted due to a non-tender agreement and secured by a blocked securities account.

Financing from own funds: In 2025 as well, offers from private equity investors in particular were regularly secured by intra-group equity financing commitments. In nine of the 20 transactions, the bidders also relied in part on their own liquid funds (2024: 11 of 32 transactions).

Adjustments to the legal framework in takeover law

Location Promotion Act: Restructuring of the delisting regime and simplifications to prospectus requirements

The Future Financing Act II (ZuFinG II), which was submitted to the Bundestag by the previous "traffic light" coalition government, was not enacted due to the principle of discontinuity following the federal elections in February 2025, as the legislative process had not been completed. However, key elements of ZuFinG II were subsequently incorporated by the new federal government into the Location Promotion Act (Standortförderungsgesetz /StoFöG), which was published in the Federal Law Gazette on February 9, 2026. From the perspective of takeover law, the amendments to the delisting regime and prospectus requirements are of particular significance.

Delisting of Issuers in the SME Growth Market

The delisting regime has been revised, with a particular focus on issuers listed on SME growth markets.

This revision was prompted by an empirical study commissioned by the Federal Ministry of Finance in 2022, which examined the effects of delisting announcements on share prices before and after the introduction of the delisting regulation in 2015. The study found that, prior to the legislative amendment, the announcement of a delisting resulted in a statistically significant decline in share prices, leading to a loss of value for investors who might otherwise have sold their shares at a higher market price before the announcement. Since the legislative change, however, no statistically significant negative effects on investors have been observed in cases of delistings from the regulated market. Similarly, in cases of downlistings from the regulated market to the over-the-counter market, no significant negative abnormal returns were observed, regardless of the regulatory framework. In contrast, for delistings from the over-the-counter market - where section 39 of the Stock Exchange Act (Börsengesetz, BörsG) does not apply - statistically significant negative effects continue to be observed: the announcement of a delisting in this context leads to a measurable loss of value for investors in the form of negative abnormal returns.

Based on these findings, the legislature has exempted downlistings from the regulated market to the SME Growth Market - which is subject to specific regulatory requirements - from the delisting regulation. At the same time, delistings from the SME Growth Market are now included within the protective scope of the delisting regulation under section 39 BörsG.

Under the revised section 39 paras. 2 and 3 of the BörsG, a transition from the regulated market to an SME growth segment - such as the Scale segment of the Frankfurt Stock Exchange - is permitted without the need to conduct a delisting tender offer, provided that the securities remain listed on an SME growth market (section 39 para. 2, sentence 2, no. 3 BörsG). The legislature justifies this amendment by referencing the comparable regulatory standards between SME growth markets and the regulated market.

As a result, stand-alone delistings from an SME growth market are now treated in the same manner as delistings from regulated markets: pursuant to section 39 paras. 2 through 6 BörsG, these generally require a tender offer reviewed by BaFin, which enables investors to exit in exchange for appropriate compensation (section 48a para. 1b BörsG). The only exception to this requirement is in cases of so-called "uplisting", where an application for admission of the securities to trading on the regulated market is filed simultaneously.

Requirements for consideration in delisting offers and judicial review

Pursuant to the revised version of section 39 para.3 sentence 3 BörsG, the market price is not decisive if "special circumstances" have influenced it during the relevant six-month period to such an extent that it is unreasonably low for the purpose of determining the consideration. In such cases, the bidder is required to pay a higher consideration reflecting the value determined on the basis of a valuation of the issuer.

Furthermore, Section 39 para. 3 sentence 7 BörsG, as amended, provides for the review of the amount of the consideration in the context of the delisting offer in accordance with the provisions of the Act on Appraisal Proceedings (Spruchverfahrensgesetz, SpruchG). Section 1 of the SpruchG has been amended with a corresponding paragraph 8; in return, the previous legal protection under the Capital Markets Model Case Act (Kapitalanleger-Musterverfahrensgesetz - KapMuG) has been abolished. According to the legislature's intent, this amendment is intended to ensure that the delisting can be carried out regardless of any disputes regarding the adequacy of the consideration.

With regard to exchange offers - which are rare in practice and in which shares are offered instead of cash consideration - the new provisions on the prospectus requirement in prospectus law are also of interest. As of June 5, 2026, prospectus-free offerings of securities (particularly shares and bonds) with a total volume of up to EUR 12 million (previously EUR 8 million) within a 12-month period will be permitted.

Listing Act – New Rules on Ad Hoc Disclosure of Interim Steps in M&A Transactions

The amendments to the ad hoc disclosure obligations in the Market Abuse Regulation (MAR) introduced by the EU Listing Act and the Delegated Act published by the European Commission in December 2025, including its Annex, provide significant clarifications regarding ad hoc obligations in protracted processes; the Delegated Regulation is expected to enter into force in the first half of 2026.

The preparation for the takeover of a listed company - typically involving several intermediate steps - often constitutes a "protracted process" within the meaning of insider trading law and ad hoc disclosure requirements under the MAR. As a result, these amendments are also relevant for takeover law. Under the previous legal framework, such intermediate steps were generally considered inside information - regardless of whether the final event was already reasonably likely and thus typically triggered a disclosure obligation for both the bidder and the target company. Compliance with the MAR's requirements primarily concerns the target company. However, for listed bidders, the question frequently arises as to when the decision to make an offer must be disclosed pursuant to section 10 of the WpÜG, and how this obligation interacts with the disclosure requirements under the MAR, including any preceding intermediate steps.

For protracted processes, the MAR as amended by the Listing Act now provides that the obligation to immediately disclose inside information no longer applies to intermediate steps (and, accordingly, the need for self-exemption to justify deferral is eliminated). Instead, only the respective final event must be disclosed (Art. 17 para. 1 subpara. 1 sentences 2 and 3 MAR, as amended). This new regulation will take effect on June 5, 2026. The Delegated Regulation implementing the Listing Act now includes a non-exhaustive list of typical protracted processes and specifies the relevant disclosure date for each. However, contrary to ESMA's initial proposal during the consultation process, the list does not address public takeovers. Since the list of "end events" in the Delegated Regulation is expressly non-exhaustive, issuers remain responsible for independently determining and documenting the relevant end event of a transaction in order to demonstrate compliance with the ad hoc disclosure obligation to BaFin in individual cases.

Development of the Regulatory Framework

Foreign Subsidies Regulation – EU Commission Publishes Guidelines

Since the Foreign Subsidies Regulation (FSR) entered into force on July 12, 2023, companies are required to notify the European Commission of mergers if the acquired company, one of the merging parties, or the joint venture generates EU turnover of at least EUR 500 million, and if the parties have received foreign financial subsidies exceeding EUR 50 million within the past three years.

On January 13, 2026, the European Commission published supplementary guidelines on the FSR. While these guidelines do not have the force of law, they reflect the Commission's enforcement practice and provide guidance to companies. In particular, the guidelines clarify the following key aspects of the FSR:

- The criteria for determining whether there is a distortion of competition in the internal market;

- Whether a distortion of competition may be justified by the positive effects of subsidies granted by third countries;

- The circumstances under which the Commission may exercise its "call-in" right to require notification of a merger or the reporting of a third-country financial subsidy in the context of a public procurement procedure, even if such notification or reporting would not otherwise be required.

The guidelines also contain illustrative examples of the main categories of distortions, such as those relating to the distortion of competition through the acquisition of other companies.

In 2025, approval under state aid control law was only sought in the JD.com/Ceconomy acquisition. The FSR procedure in the ADNOC/Covestro case was successfully concluded in 2025.

EU Screening Regulation – EU Revises Legal Framework for Foreign Direct Investment Screening

Regulation (EU) 2019/452 ("EU Screening Regulation") has been in force since October 2020 as a cooperation mechanism, allowing Member States and the European Commission to identify cross-border risks to security and public order arising from foreign investments and to exchange information on such transactions. Under this mechanism, the Member State conducting the review forwards information on the relevant transaction to other Member States and the Commission, which may submit comments or a non-binding opinion within specified timeframes.

An initial proposal to reform the EU Screening Regulation was published in 2024, and the so-called trilogue negotiations commenced in July 2025. On December 11, 2025, the Council of the European Union and the European Parliament reached a provisional political agreement. To promote greater uniformity across the EU, all Member States will be required to conduct targeted screening in clearly defined areas. The minimum scope of screening will include:

- Dual-use items and military goods;

- Particularly critical technologies, such as artificial intelligence (as defined in the Artificial Intelligence Regulation, with a focus on general-purpose AI relevant to space or defense), quantum technologies, and semiconductors;

- Critical raw materials;

- Critical facilities in the energy, transport, and digital infrastructure sectors, based on a risk-based assessment by the Member State where the EU target is located;

- Election infrastructure (e.g., voter databases, voting systems, election management systems); and

- A limited list of financial system entities, restricted to central counterparties, central securities depositories, market operators, payment system operators (excluding central banks), and systemically important institutions.

Under the agreement, each Member State retains exclusive competence over investment screening procedures. At the same time, transparency and coordination between national authorities and the Commission are enhanced. Where other Member States or the European Commission have submitted comments or opinions, the reviewing Member State must explain the extent to which these have been taken into account. The provisional agreement must now be approved by the Council and the Parliament before it is formally adopted. The new rules will apply 18 months after the regulation enters into force.

In 2025, investment control clearance procedures were conducted in the Warburg Pincus/PSI Software, JD.com/Ceconomy, and Carlyle/SNP Schneider-Neureither & Partner transactions.

Stock Price and Valuation – New Developments

Sometimes, even before the conclusion of a takeover proceeding, there may be an intention to implement further integration measures, such as entering into a control (and profit transfer) agreement (Beherrschungs- und Gewinnabführungsvertrag, BGAV) or a squeeze-out of the remaining minority shareholders. In such cases, shareholders are entitled to receive appropriate compensation.

Shareholders may seek a judicial review of the compensation amount. This raises the issue of whether, and to what extent, the stock market price determines the compensation amount, or whether a fundamental valuation must be conducted. Traditionally, the enterprise value has been determined in accordance with established case law using a business valuation based on the IDW S1 standard, with the stock market price serving only as a lower threshold.

However, in February 2023, the Federal Court of Justice (BGH) recognized for the first time that the stock market price is a fully valid valuation method that can replace the income value method for determining the adequacy of both the compensation and the settlement payment in the context of a domination and profit and loss transfer agreement (BGAV). Accordingly, reliance on a company's stock market price is an appropriate method for estimating the enterprise and equity value of an outside shareholder under section 305 of the German Stock Corporation Act (AktG). Moreover, the market value of a company is generally suitable for adequately reflecting both its historical earnings performance and its future earnings prospects in individual cases, and may therefore also serve as the basis for determining the compensation payment pursuant to section 304 para. 2 sentence 1 AktG (BGH, Decision of February 21, 2023, Ref. No. II ZB 12/21, and Decision of January 31, 2024, Ref. No. II ZB 5/22).

Following these decisions, both the Higher Regional Court of Karlsruhe (decision of April 16, 2024, Case No. 12 W 27/23) and the Higher Regional Court of Frankfurt (decision of February 9, 2024, Case No. 21 W 129/22) similarly ruled on the determination of appropriate compensation in squeeze-out cases.

In response to this case law and the resulting practice, the Institute of Public Auditors in Germany (IDW) published the new "IDW Standard S 17 – Assessment of the Appropriateness of Stock Market Price-Based Compensation" on January 8, 2026. This standard sets out the principles by which auditors—without prejudice to their own professional judgment—assess the appropriateness of stock price-based compensation in light of the full economic ("true") value of the shares in the context of appropriateness reviews under stock corporation or transformation law. The standard applies to valuation dates after its publication. IDW S 17 defines economic assessment criteria and procedures; based on these, the auditor conducts an overall assessment of appropriateness with regard to the "true" value. Key criteria under the new standard include shareholder structure, liquidity, market coverage, the scope of reporting, the company's circumstances as of the valuation date (the date of the general meeting resolution), and any obvious indications of external price manipulation. Auditors are to use these criteria in a "traffic-light" system; if at least one criterion is rated yellow, a determination of the objectified enterprise value according to IDW Standard S 1 is also required.

The importance of the stock market price in determining compensation payments has thus been reinforced not only by recent case law but also by the Location Promotion Act and the new IDW Standard S 17. Nevertheless, IDW Standard S 17 has been subject to justified criticism for interpreting the fundamental recognition of the stock market price as an independent valuation method - as now required by the highest court's case law - in a somewhat restrictive manner in practice.

Judgments relevant for takeovers in 2025

ECJ rules on the attribution of voting rights in cases of concerted action without an agreement (acting in concert)

In its order of October 22, 2024 (Case No. II ZR 193/22), the Federal Court of Justice (BGH) referred the following question to the European Court of Justice (ECJ) regarding the disclosure obligation for voting rights in cases of concerted action without a prior "agreement": Should Article 3(1a), fourth subparagraph, point (iii) of Directive 2004/109/EC (the Transparency Directive) be interpreted as precluding section 34 para. 2 first sentence, case 2 of the German Securities Trading Act (Wertpapierhandelsgesetz, WpHG), which does not require an agreement between the party subject to the notification requirement and the third party for the attribution of voting rights, but instead allows for attribution based on coordinated conduct in any other manner, as established by factual circumstances?

Although the BGH case involving Valora Effekten AG concerned a small company, the referral to the ECJ raised the question of whether the BGH would reconsider its previous position on "voting in any other manner" when assessing potential acting in concert. This issue is particularly relevant in the context of "collaborative engagement" by investors on ESG matters, which may, in individual cases, constitute "acting in concert." The BaFin issued guidelines on this topic in March 2023.

Under takeover law, it is undisputed that voting "in any other manner" is sufficient for the attribution of voting rights. However, with respect to section 34 para. 2 WpHG, there has been debate as to whether this provision complies with the Directive, especially since it allows for the attribution of voting rights even in the absence of an "agreement," based on a "vote by other means," which goes beyond the requirements of Article 10 (a) of the Transparency Directive. The core issue is whether the broad national provision falls within the exception set out in Article 3 (1a) fourth subparagraph point (iii) of the Transparency Directive, which permits stricter national rules only if they relate to takeover bids, mergers, or other transactions affecting the ownership structure or control of companies and are supervised by authorities under the Takeover Directive.

The ECJ, in its judgment of February 12, 2026 (Case C-864/24), has now ruled that the attribution of voting rights without the existence of an explicit agreement is impermissible. The exception in the WpHG for attribution of voting rights based on "voting in any other manner" must therefore be interpreted narrowly. As a result, the previously assumed alignment of legal consequences for agreements "in any other manner" under the WpHG and takeover law has been restricted by the ECJ at the level of securities trading law. Consequently, the prevailing view is now that the WpHG notification obligation exists independently of a takeover and applies only to explicit agreements between shareholders entitled to vote; thus, mere factual circumstances are not sufficient to establish acting in concert with the consequence of the attribution of voting rights.

Statute of limitations on claims for additional payments under Section 31 para. 6 of the German Takeover Act (WpÜG) – Stada case

Decision of the Frankfurt Higher Regional Court from November 2025

In November 2025, the Frankfurt Higher Regional Court published its appeal decision in the Stada case. The subject of the proceedings was the possible statute of limitations on the claims of plaintiff shareholders in connection with an agreement reached with Elliott following the Stada takeover by private equity investors Bain and Cinven in 2017. We reported on the previous decision by the Regional Court in our Public Takeovers 2024 update.

The legal dispute stems from an irrevocable commitment that the bidders had agreed upon with the hedge fund Elliott after reaching the - previously reduced - acceptance threshold of 63% within the statutory extended acceptance period. Under this commitment, Elliott agreed to approve a profit transfer and control agreement at the Stada Annual General Meeting, provided that the compensation for the remaining shareholders was set at a minimum of EUR 74.40 per share. By contrast, shareholders who had accepted the public takeover offer received only EUR 66.25 per share.

This raised the question for shareholders who received the lower consideration under the takeover offer as to whether they were entitled to an additional payment based on the principle of equal treatment under the WpÜG. In May 2023, the Federal Court of Justice (BGH) held that such an irrevocable commitment constitutes an agreement within the meaning of section 31 para. 5 WpÜG and affirmed the plaintiffs' entitlement to an additional payment.

In its judgment of April 10, 2024 (Case Nos. 3-05 O 532/23 and 3-05 O 572/23), the Frankfurt am Main Regional Court held that the statute of limitations for additional payment claims by other shareholders did not begin to run until 2023, due to the absence of prior knowledge of the relevant facts. As a result, the claims against the bidders were not time-barred. The Regional Court found that the statute of limitations did not commence with the publication of press releases by the bidders and Elliott, but only in May 2023, when the Federal Court of Justice's decision was announced. The press releases did not disclose that a legally binding agreement had been concluded. Accordingly, the remaining shareholders lacked the requisite knowledge or obligation to know of an agreement within the meaning of section 31 para. 6 WpÜG. The publication of the first-instance judgment in a legal journal also did not create an obligation to know the facts giving rise to the claims.

In its judgment of December 28, 2025 (Case No. 26 U 14/25), the Frankfurt Higher Regional Court upheld the Regional Court's decision. The appeal was successful only to a limited extent with respect to the accrual of interest: the obligation to pay interest begins only from the day following the date on which the case became pending. A petition for review was not granted. An appeal against the denial of leave to appeal has been filed, but a decision on this has not yet been rendered.

Outlook

With the acquisition of Klöckner & Co by Worthington Steel (with a transaction volume exceeding €2 billion), the public takeover market has started 2026 with a major transaction. However, it appears unlikely that this will signal a broader trend, given the current stock market environment. The new conflict in the Middle East has further unsettled capital markets, and it remains uncertain how the market for acquisitions of publicly listed companies will develop over the course of 2026. Conversely, the underperformance of certain companies' stock prices may make them attractive acquisition targets for growth-oriented bidders.

The takeover bid by UniCredit for Commerzbank, announced in March 2026 and characterized as hostile, has generated significant discussions. Whether UniCredit's proposed merger of these two major players in the banking sector will ultimately be realized remains to be seen.

1 Pursuant to section 5 of the WpÜG Offer Regulation, the offer price must be at least equal to the weighted average domestic stock market price of the target company's shares during the last three months (or six months in the case of delisting offers) prior to the publication of the decision to make the offer. Pursuant to section 4 of the WpÜG Offer Regulation, the offer price must be at least equal to the value of the highest consideration granted by the bidder, persons acting in concert with the bidder within the meaning of Section 2(5) of the WpÜG, or their subsidiaries for the acquisition of the target company's shares within the six months preceding the publication of the offer document.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2026 White & Case LLP