European non-performing loan trends in a post-COVID-19 world

Foreword

While the overall European non-performing loan (NPL) market has been in decline since its peak in 2018, the ongoing impact of COVID-19 may soon change things.

It has been a tough year for European business and consumers, as waves of COVID-19 lockdown restrictions took their toll. Entire sectors were effectively shut down, with many surviving on government support and employee furlough programmes, as well as tapping liquidity markets and taking advantage of any debt relief measures on offer.

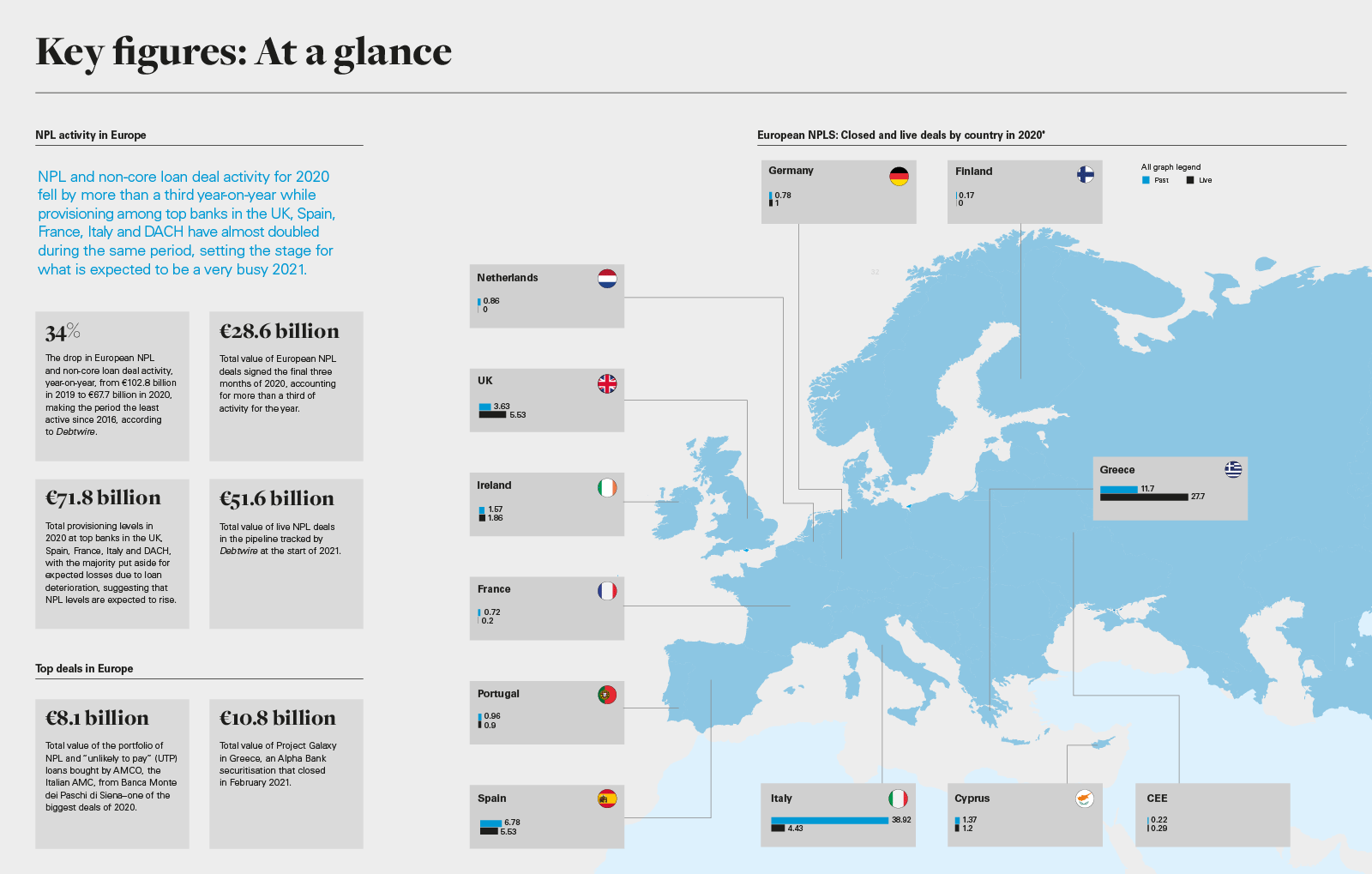

Travel restrictions and economic uncertainty also impacted the NPL market. Though activity shut down in the second quarter of 2020, the final quarter saw a partial recovery, with deals worth €28.6 billion signed in Q4 2020 alone. However, price gaps continued to impact some deals. The first month of 2021 saw deals close that were worth €3.3 billion, as some deals paused due to lockdown conditions managed to compete. Looking to the rest of 2021, Greek NPL deals are keeping the NPL pipeline filled.

The impact of COVID-19 on loan quality has yet to be felt. Many companies have managed to avoid slipping into insolvency thus far, whether through government stimulus measures or agreements with lenders, but once those measures wind down and lenders reassess the creditworthiness of their borrowers, that is likely to change. Provisioning levels at top European banks in the UK, Spain, France, Italy and DACH reflect this reality, almost doubling year-on-year from 2019 to 2020, according to Debtwire.

Governments across Europe recognise the challenge they are facing. A spike in NPLs among lenders could spell trouble for those same lenders, prompting the EU to consider regulatory options that will help smooth the process. Standardised templates, securitisation and boosting secondary NPL trading are all on the cards, as regulatory bodies and lenders take a proactive stance to prepare for a potentially rocky road ahead. Taking these steps also opens the door to more buyers entering the market—including some that were once active but may have stepped aside as things cooled, including PE firms, banks and other debt servicers. It may also encourage partnerships to invest in NPL portfolios, which may also drive the speed of portfolio disposals in the coming year.

New market opportunities in sight?

At a regional level, Italy and Greece remain NPL hotspots, as the securitisation of NPL portfolios coupled with state-backed guarantee schemes continue to help reduce NPL stocks among banks. But other markets are now showing signs of activity, and investors are watching very closely.

In Spain, moratoria on mortgage and non-mortgage debts are set to expire, prompting many Spanish banks to prepare for an uptick in NPL stocks—the four top banks in the country put aside provisions of €22 billion in 2020, up from €15 billion in 2019.

Many expected UK banks to move quickly in the event of an expected rise in NPLs, given the high economic fallout of multiple lockdowns. Top UK bank provisions rocketed by 3.1x year-on-year, to €21.2 billion, as banks braced for loan losses.

Ireland, France, Portugal and even typically cautious Germany (where SME loans are expected to be the largest source of NPL stock rise) are all on the radar for investors. But the degree of rise in problem loans still has a large degree of variability, with the speed of economic recovery and the end of huge levels of government support still unclear.

COVID-19 and the state of the European NPL market

Early in 2020, as the pandemic took hold, the European NPL market went into lockdown along with the rest of the economy—but as the market opened up in the second half of the year, NPL sellers jumped back in, setting the stage for a busier 2021.

NPL and non-core loan deal activity for 2020 fell by more than a third year-on-year while provisioning among top banks in the UK, Spain, France, Italy and DACH have almost doubled during the same period, setting the stage for what is expected to be a very busy 2021.

Regional spotlight: NPLs in France, Germany, Spain, UK & Ireland

Opportunities for NPL investors are presenting themselves in European jurisdictions outside of the largest markets: Italy and Greece. Here is an assessment of markets where new opportunities for NPL deal flow are emerging.

Where will the European NPL market go from here? A lot depends on vaccine rollouts and the end of debt relief measures. For many, that will be their first chance to assess the damage and plan ahead.

Where will the European NPL market go from here? A lot depends on vaccine rollouts and the end of debt relief measures. For many, that will be their first chance to assess the damage and plan ahead.

In a poll of audience members watching Fitch Ratings' Credit Outlook conference, held in January 2021, nearly 70 per cent said they expected a rise in European NPL sales in the year ahead, driven by capital management in banks holding the loans as well as non-bank financial institutions improving their handling of NPLs.

While a rise in NPLs is likely on the cards, the scale and timing of such developments remain largely unknown. Government-led relief measures have made it almost impossible to assess how some businesses have performed during the pandemic.

And as the EU's Economic Governance Support Unit pointed out in its analysis of the EU's regulatory and supervisory response to addressing NPLs, published in February 2021, the situation for lenders is not particularly transparent: "The COVID-19 crisis and the policy reactions to avert its damaging economic and social effects have exposed banks to further deterioration of their assets. Effects on banks' balance sheets are yet to be felt and quantified."

Then there are other unknowns to consider. For example, the current economic situation is not the result of a "credit crunch." The impact of COVID-19 was sudden and has lasted longer than many anticipated, but liquidity has not necessarily been an issue. Lending paused in the second quarter of 2020, as did virtually everything, but activity picked up significantly in the second-half of the year. Interest rates remain low and, by and large, companies needing to address any debt repayment concerns have had the opportunity to do so.

Post-COVID-19, many businesses that were forced to close their doors for the duration will also remain viable—albeit with weakened balance sheets—and their recovery is entirely possible. Sectors hit particularly hard by the pandemic, from leisure and hospitality to airlines, are likely to struggle more than most, but even they will see recovery once the public is free to take advantage.

At the same time, consumer habits and preferences may have been changed entirely by this experience, to say nothing of people's work habits, and time will tell how this plays out. Many supply chains will also have been altered and may not return to pre-COVID-19 levels, changing the business landscape significantly.

What all of these unknowns mean for the future of NPLs is not yet clear. But the resurgent waves of COVID-19 across Europe, coupled with delays in vaccine deliveries and rollouts, suggest that European NPL volumes are likely to increase in the months ahead, as businesses are forced to make increasingly tough decisions about their future. Increases in bank provisioning certainly points to an uptick in NPL activity. As such, borrowers, lenders and investors alike will need to keep a close eye on how the story plays out once the dust begins to settle.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image 'Key figures: At a glance' PDF

View full image 'Key figures: At a glance' PDF