European non-performing loan trends in a post-COVID-19 world

Foreword

While the overall European non-performing loan (NPL) market has been in decline since its peak in 2018, the ongoing impact of COVID-19 may soon change things.

It has been a tough year for European business and consumers, as waves of COVID-19 lockdown restrictions took their toll. Entire sectors were effectively shut down, with many surviving on government support and employee furlough programmes, as well as tapping liquidity markets and taking advantage of any debt relief measures on offer.

Travel restrictions and economic uncertainty also impacted the NPL market. Though activity shut down in the second quarter of 2020, the final quarter saw a partial recovery, with deals worth €28.6 billion signed in Q4 2020 alone. However, price gaps continued to impact some deals. The first month of 2021 saw deals close that were worth €3.3 billion, as some deals paused due to lockdown conditions managed to compete. Looking to the rest of 2021, Greek NPL deals are keeping the NPL pipeline filled.

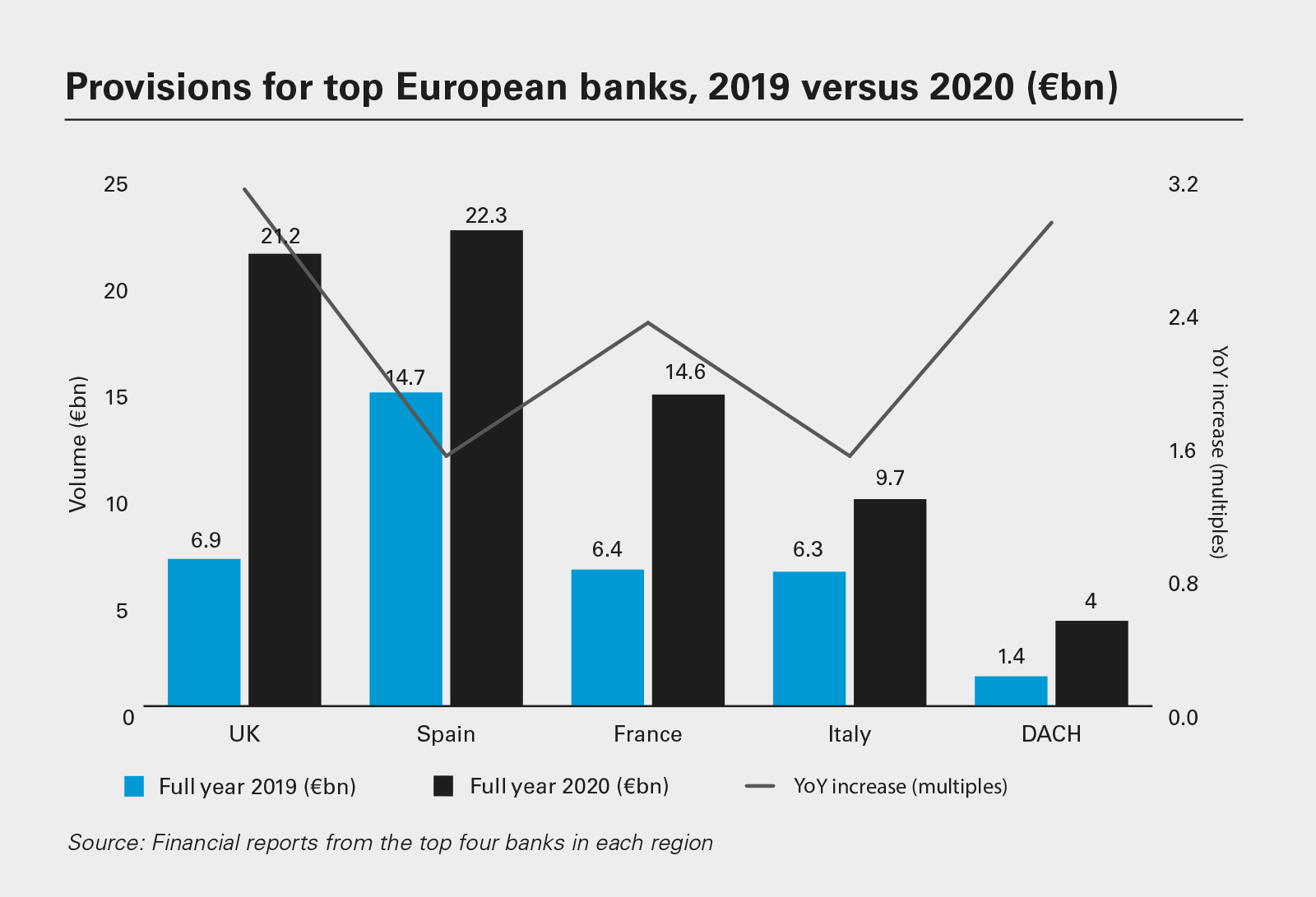

The impact of COVID-19 on loan quality has yet to be felt. Many companies have managed to avoid slipping into insolvency thus far, whether through government stimulus measures or agreements with lenders, but once those measures wind down and lenders reassess the creditworthiness of their borrowers, that is likely to change. Provisioning levels at top European banks in the UK, Spain, France, Italy and DACH reflect this reality, almost doubling year-on-year from 2019 to 2020, according to Debtwire.

Governments across Europe recognise the challenge they are facing. A spike in NPLs among lenders could spell trouble for those same lenders, prompting the EU to consider regulatory options that will help smooth the process. Standardised templates, securitisation and boosting secondary NPL trading are all on the cards, as regulatory bodies and lenders take a proactive stance to prepare for a potentially rocky road ahead. Taking these steps also opens the door to more buyers entering the market—including some that were once active but may have stepped aside as things cooled, including PE firms, banks and other debt servicers. It may also encourage partnerships to invest in NPL portfolios, which may also drive the speed of portfolio disposals in the coming year.

New market opportunities in sight?

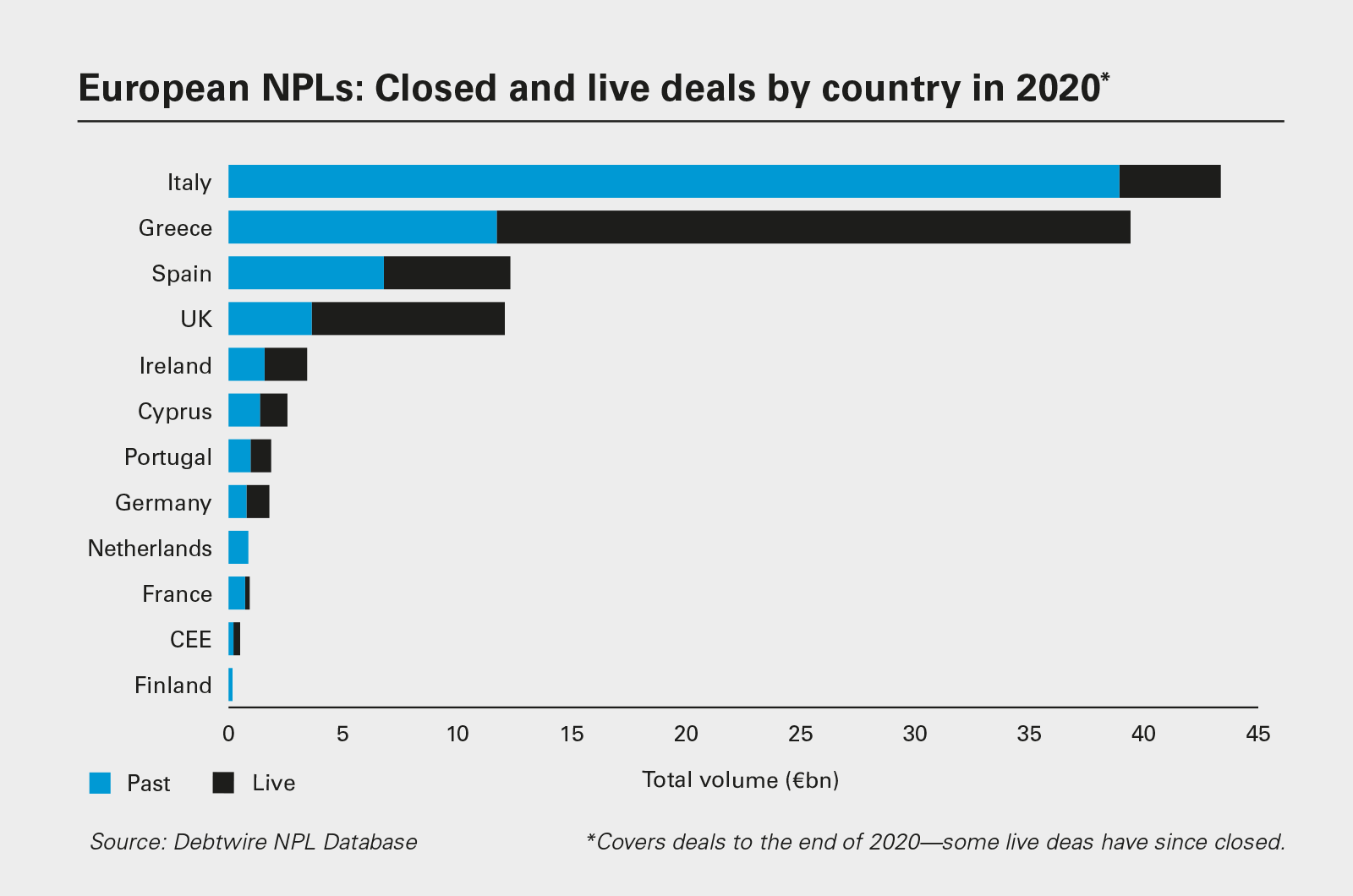

At a regional level, Italy and Greece remain NPL hotspots, as the securitisation of NPL portfolios coupled with state-backed guarantee schemes continue to help reduce NPL stocks among banks. But other markets are now showing signs of activity, and investors are watching very closely.

In Spain, moratoria on mortgage and non-mortgage debts are set to expire, prompting many Spanish banks to prepare for an uptick in NPL stocks—the four top banks in the country put aside provisions of €22 billion in 2020, up from €15 billion in 2019.

Many expected UK banks to move quickly in the event of an expected rise in NPLs, given the high economic fallout of multiple lockdowns. Top UK bank provisions rocketed by 3.1x year-on-year, to €21.2 billion, as banks braced for loan losses.

Ireland, France, Portugal and even typically cautious Germany (where SME loans are expected to be the largest source of NPL stock rise) are all on the radar for investors. But the degree of rise in problem loans still has a large degree of variability, with the speed of economic recovery and the end of huge levels of government support still unclear.

COVID-19 and the state of the European NPL market

Early in 2020, as the pandemic took hold, the European NPL market went into lockdown along with the rest of the economy—but as the market opened up in the second half of the year, NPL sellers jumped back in, setting the stage for a busier 2021.

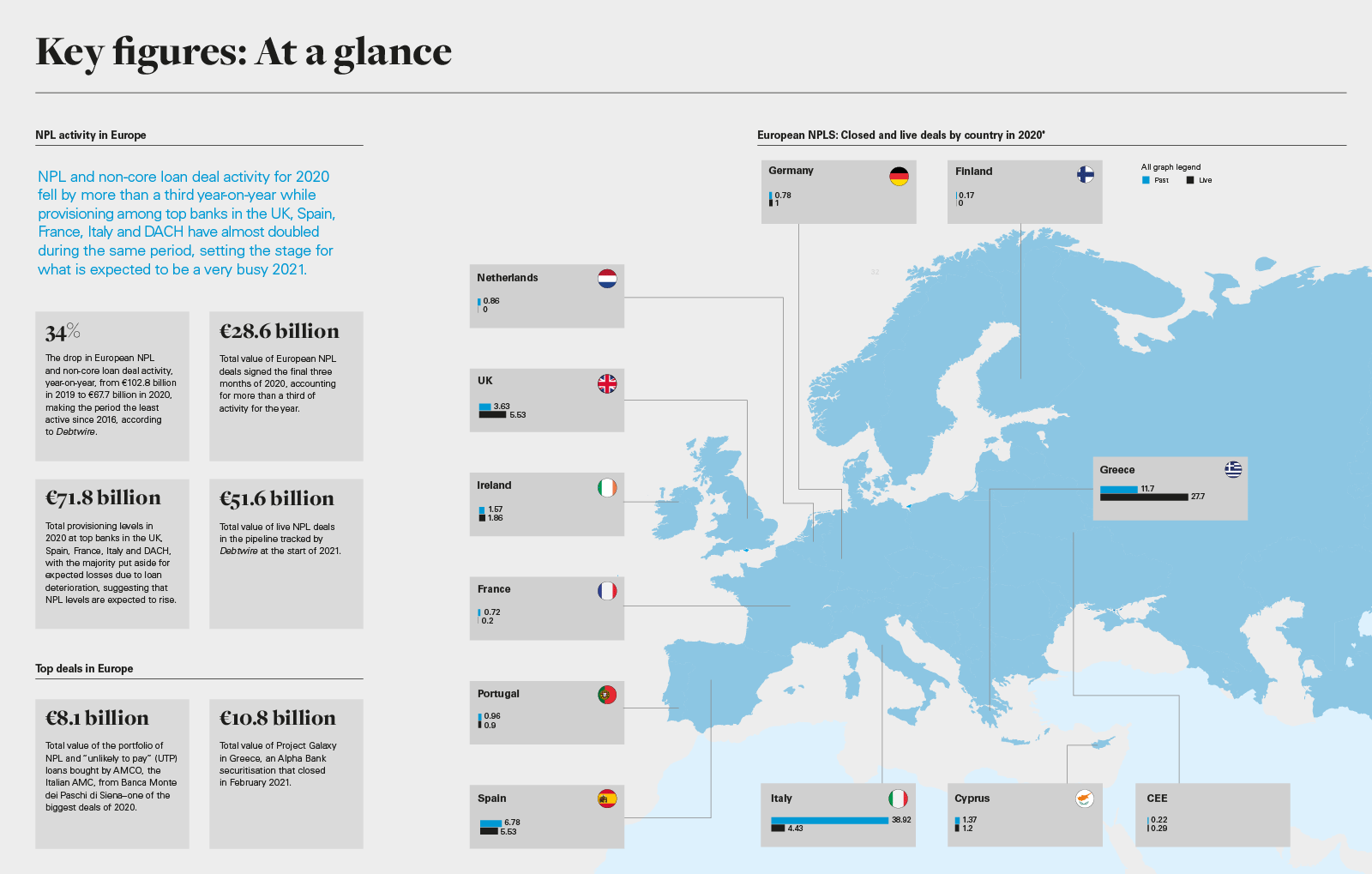

NPL and non-core loan deal activity for 2020 fell by more than a third year-on-year while provisioning among top banks in the UK, Spain, France, Italy and DACH have almost doubled during the same period, setting the stage for what is expected to be a very busy 2021.

Regional spotlight: NPLs in France, Germany, Spain, UK & Ireland

Opportunities for NPL investors are presenting themselves in European jurisdictions outside of the largest markets: Italy and Greece. Here is an assessment of markets where new opportunities for NPL deal flow are emerging.

Where will the European NPL market go from here? A lot depends on vaccine rollouts and the end of debt relief measures. For many, that will be their first chance to assess the damage and plan ahead.

Early in 2020, as the pandemic took hold, the European NPL market went into lockdown along with the rest of the economy—but as the market opened up in the second half of the year, NPL sellers jumped back in, setting the stage for a busier 2021.

As COVID-19 vaccination programmes are rolled out across Europe and markets stabilise, NPL assets are back on the agenda for banks and regulators alike. European NPL stocks are expected to increase through the course of 2021 and into 2022 as insolvency moratoria, employment protection schemes and central bank liquidity support measures unwind.

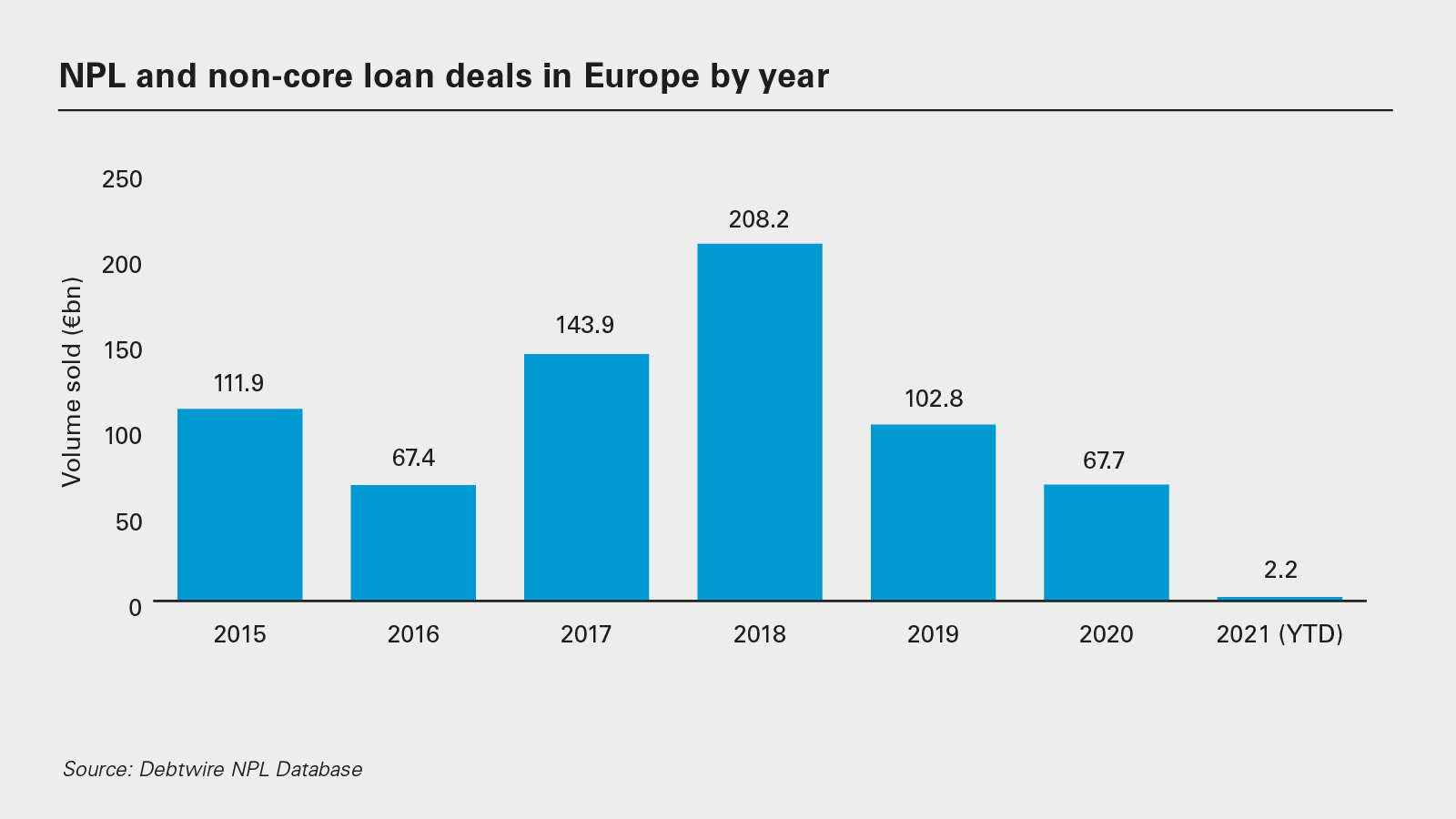

This stands in stark contrast to the position of the market pre-pandemic, when NPL activity in Europe was in steady decline due to lower volumes of NPLs. Of course, Europe's NPL market is not homogenous—some markets have remained busy, such as Italy and Greece—but overall European NPL activity has slowed during the pandemic.

In the decade following the 2008 financial crisis, banks strengthened balance sheets and offloaded unwanted portfolios of loans. In 2019, only €102.8 billion of NPL and non-core deals closed, less than half the €208.2 billion figure for 2018, according to Debtwire's fullyear analysis of the European NPL market in 2020.

According to the European Banking Authority's (EBA) 2020 Risk Dashboard, based on data as of Q3 2020, overall European NPL levels stood at a record low of €510.5 billion, less than half the peak level of €1.2 trillion reached in 2014.

The combination of longterm falls in NPL levels and the COVID-19 lockdown saw NPL and non-core loan deal activity for 2020 down 34 per cent year-onyear at €67.7 billion, making the period the least active since 2016, according to Debtwire.

Deal activity started to revive in the second half of the year as market participants, including selling banks, buyers and state-owned asset management companies (AMCs— vehicles set up by governments to consolidate and sell down bad loan books), returned to work on disposals and managing legacy NPLs. In the final three months of 2020, deals worth €28.6 billion were signed, accounting for more than a third of activity for the year.

Most notable deals (by deal size) that have gone through since the summer of 2020 include AMCO, the Italian AMC, buying an €8.1 billion portfolio of NPL and "unlikely to pay" (UTP) loans from Banca Monte dei Paschi di Siena, and debt servicer doValue buying the mezzanine and junior notes of a €7.5 billion non-performing exposure (NPE) securitisation from Eurobank Eragsias as part of Project Cairo in Greece.

In other significant NPE securitisation deals in Greece, Piraeus Bank signed binding agreements with Intrum to sell 30 per cent of the mezzanine notes for the Phoenix portfolio and Vega portfolio, amounting to €1.92 billion and €4.8 billion gross book value respectively, which are intended to benefit from the Greek asset protection scheme Hercules.

Deal pipelines for pending deals have also been replenished, with Debtwire tracking €51.6 billion in live deals at the start of 2021. Top live deals being tracked in Greece include Project Frontier, a €6 billion disposal ongoing from the National Bank of Greece. Piraeus Bank also submitted an application for a new €7 billion NPE securitisation, Sunrise 1, under the HAPS scheme.

Project Galaxy, an Alpha Bank securitisation with a portfolio worth €10.8 billion, closed in February 2021. Davidson Kempner signed an agreement to acquire 51 per cent of the mezzanine and junior notes.

In addition to the pipeline of current live deals, banks and buyers are also preparing for an influx of new NPL stock prompted by COVID-19 and its impact on financial performance and creditworthiness.

Total provisioning levels at top European banks in the UK, Spain, France, Italy and DACH have almost doubled year-on-year, according to Debtwire, rising from €35.7 billion in 2019 to €71.8 billion in 2020, as institutions prepare for anticipated future losses.

While these provisions suggest a significant increase in NPL stock is expected, the scale remains uncertain. Many banks are still assessing which borrowers will be unable to repay loans when economies reopen and which may be able to recover fully in time.

For example, lenders may decide that companies in industries such as leisure, aviation and commercial real estate—which were trading strongly pre-COVID-19 but were hit particularly hard by lockdown restrictions—will be able to rebound as economies recover and service outstanding debts as their earnings improve.

Total provisioning levels in 2020 at top European banks in the UK, Spain, France, Italy and DACH

Proactivity is key for regulators

While regulators are equally uncertain about the ultimate size of European bank NPL exposure, the chair of the European Central Bank's supervisory arm warned in October 2020 that— in a severe but entirely plausible scenario—NPLs at European banks could rise as high as €1.4 trillion.

The European Commission (EC) is considering various measures and changes to regulations to proactively address any pending spikes in bank exposure to NPL loans.

Regulators want to support Europe's NPL secondary market by making it easier and quicker to get deals to market. The EBA already has data templates in place to help investors analyse NPLs, but uptake has been limited. There is now a push to make templates mandatory for market participants—they were initially only required for new NPLs, i.e., for loans that become non-performing after a specific cut-off date—and to create a central database of NPL information that market participants can access.

The regulators have also indicated that banks should not be penalised if they do not have non-essential data and will be allowed to use a no-data option.

While Europe has a functioning NPL secondary market, it has typically been characterised by smaller tickets and local buyers. Standardising information and data is seen as a crucial step to increase the volume of secondary NPLs.

Supporting the securitisation of NPL portfolios—which has proven successful in Italy and Greece, where banks had the largest NPL exposures in Europe—will also expedite NPL transactions (see "Is securitisation an essential ingredient for success?" on page 6). The legislators have completed the process of implementing targeted improvements to the securitisation framework to account for the special characteristics of NPL securitisations. The amended framework will enable wider use of securitisation as a tool by banks to free their balance sheets from NPLs.

It is hoped that facilitating securitisation and boosting secondary NPL trading will bring a broader pool of buyers into the market, creating deeper liquidity and reducing the time it takes to dispose of NPL portfolios

Calling all new buyers

It is hoped that facilitating securitisation and boosting secondary NPL trading will bring a broader pool of buyers into the market, creating deeper liquidity and reducing the time it takes to dispose of NPL portfolios.

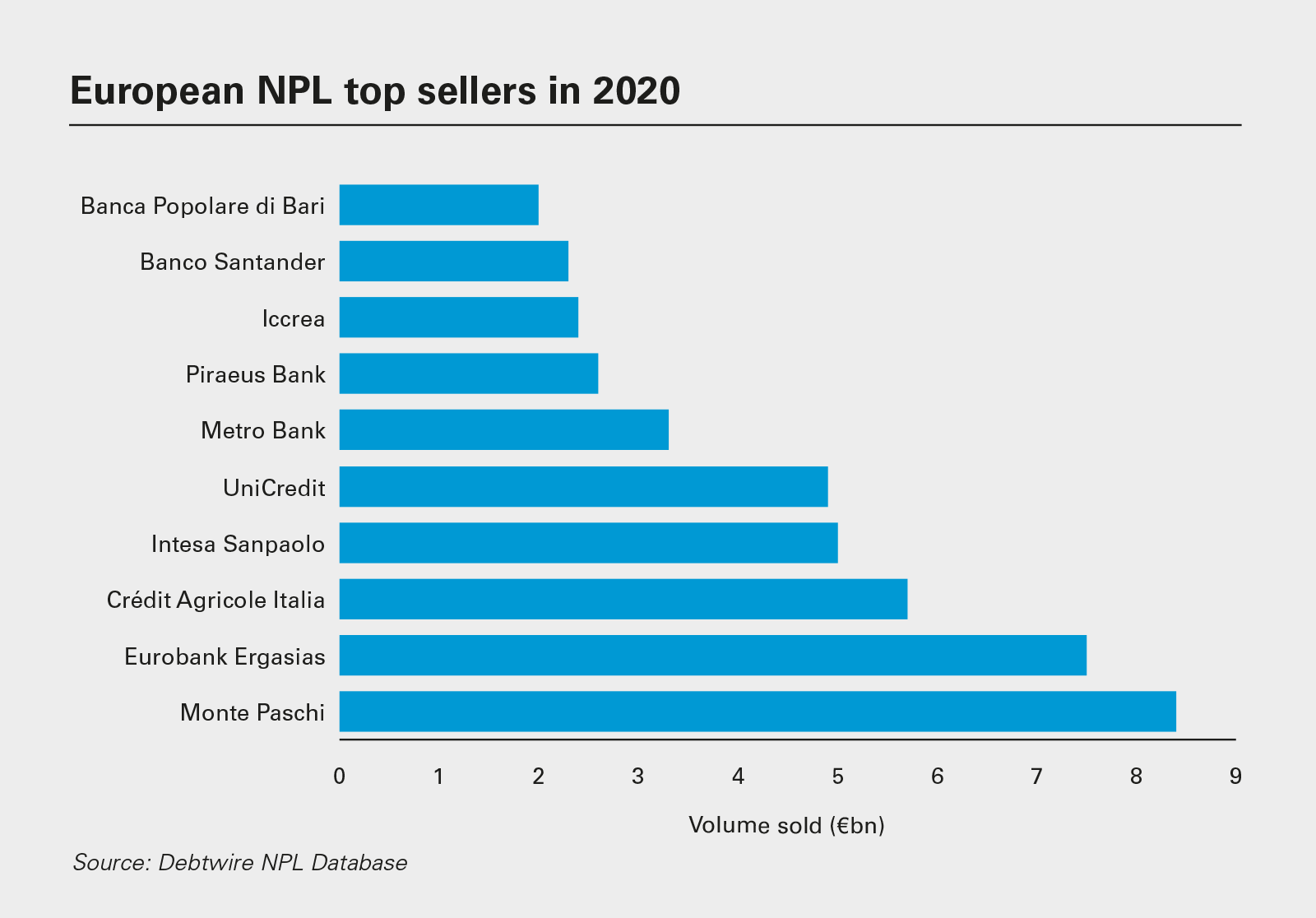

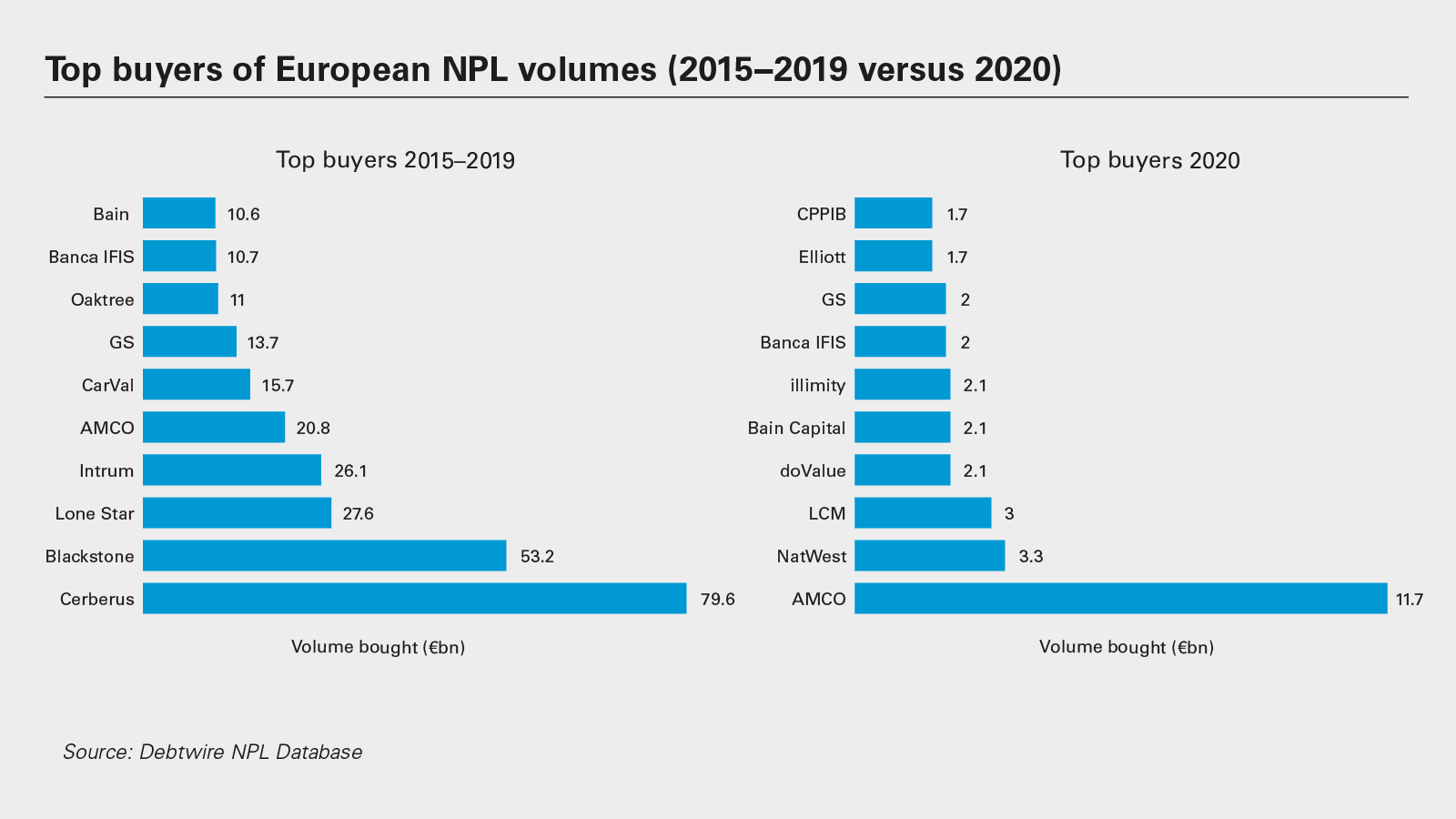

From 2015 to 2019, private equity (PE) managers Cerberus, Blackstone and Lone Star dominated NPL transaction activity, accounting for more than €160 billion in NPL deals between them. In 2020, however, with the exception of a few deals closed by Cerberus, none of these firms were particularly active in NPL transactions.

In 2020, Italy's "bad bank" AMCO was the most active NPL investor, buying up €11.7 billion of NPLs. Other asset managers and banks—including LCM, Goldman Sachs and fixed-income specialist PIMCO—were active buyers last year, with debt servicing platform doValue also ranking among the top-ten buyers.

PE firms, banks and other debt servicers, including CarVal and Intrum, that were more active buyers of NPL assets prior to 2020, will likely once again become key buyers of NPL portfolios as levels increase through 2021. Banks will also be looking to other distressed debt funds, family offices, activist investors and pension funds to come into the market and provide potential exit routes as NPL stocks increase.

In 2020, activist investor Elliott bought a €1.7 billion NPL portfolio from Crédit Agricole Italia. Canadian pension fund CCPIB's €1.6 billion acquisition of a Spanish secured residential loan portfolio from Santander in March 2020 is another example of the European NPL market holding appeal for a broad range of institutions.

Investors are also exploring partnerships as a way to invest in NPL portfolios. Swedish debt purchasing firm Hoist Finance, for example, has agreed to a deal with structured credit fund Magnetar Capital Management. The deal will allow Hoist to buy up NPL portfolios, hold the senior debt and sell down the mezzanine and junior securitised note portions to Magnetar. As a result, Hoist—which is a bank, unlike most of its investor competitors— can invest up to €1 billion in NPLs while benefitting from the preferential capital treatment by achieving significant risk transfer. Other investors, such as buyers aiming to repurpose real estate by taking ownership of properties via purchases of real estate NPLs, could also deepen the buyer universe.

Measures to further develop the secondary and securitisation markets will encourage more investors like these to consider NPL deals seriously.

Is securitisation an essential ingredient for success?

The securitisation of NPL portfolios in Greece and Italy has proven an invaluable tool for reducing bank NPL stocks in these jurisdictions. Both the Garanzia Cartolarizzazione Sofferenze (GACS) scheme in Italy, launched in 2016, and Greece's Hercules Hellenic Asset Protection Scheme (HAPS), introduced in 2019, provide state-backed guarantees for senior tranches of NPLs that are bundled together into special purpose vehicles and sold.

Italy was the largest European market for NPL deals in 2020, with the sale of €38.9 billion of loans, followed by Greece with deals totalling €11.7 billion. The portion of GACS- and HAPS supported transactions in 2020 represented a third of all European NPL activity that year.

Although the mechanisms for NPL securitisations in Europe have been in place as early as 2003, and there were a number of NPL securitisations that took place prior to the 2008 financial crisis, their use was effectively shut down on the continent after the financial crisis. It was only when governments in Italy and Greece stepped in to create securitisation frameworks that deal activity revived using these mechanisms. State-backed guarantee schemes have been particularly successful in these jurisdictions.

Although the tool has helped both Italian and Greek banks to accelerate the pace of their NPL sell-downs, other European governments have yet to step in and create similar state-backed NPL securitisation programmes. There have been a few isolated examples of non-state-backed NPL securitisations in Spain, Ireland, Portugal and Greece, where Eurobank Ergasias completed a €2 billion market NPL securitisation in 2019, but these deals are rare and account for a fraction of overall NPL volumes.

EU NPL securitisation regulation, which came into force in 2019, has put a uniform set of rules in place for all European governments to follow should they choose to do so. The adoption of government guarantee schemes by other European countries under this framework could provide a timely boost for clearing out NPL portfolios following the increased pressure on loan books as a result of COVID-19.

The legislative process for amending the current NPL securitisation framework, so that non-rated NPL securitisations are no longer subject to materially higher capital charges, has been completed and was included in the level I text on 9 April, 2021. These changes are certain to encourage more NPL securitisation deal flow. Legislators have also placed emphasis on expediting the enactment of law governing credit servicers and credit purchasers in order to further develop a secondary market for distressed assets.

Another legislative initiative that is key for the NPL market is the minimum harmonisation rules on accelerated extrajudicial collateral enforcement. The European Commission has also extended its support to national AMCs in such banking sectors where it is needed, while maintaining that involvement of state aid must not be seen as the default solution.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image 'Key figures: At a glance' PDF

View full image 'Key figures: At a glance' PDF

View full image: NPL and non-core loan deals in Europe by year (PDF)

View full image: NPL and non-core loan deals in Europe by year (PDF)

View full image: European NPLs: Closed and live deals by country in 2020 (PDF)

View full image: European NPLs: Closed and live deals by country in 2020 (PDF)

View full image: European NPL top sellers in 2020 (PDF)

View full image: European NPL top sellers in 2020 (PDF)

View full image: Provisions for top European banks, 2019 versus 2020 (€bn) (PDF)

View full image: Provisions for top European banks, 2019 versus 2020 (€bn) (PDF)

View full image: Top buyers of European NPL volumes (2015−2019 versus 2020) (PDF)

View full image: Top buyers of European NPL volumes (2015−2019 versus 2020) (PDF)