The European non-performing loan landscape looks very different in 2022, with large deals driven by urgent government regulation supplanted by small but steady opportunities.

Foreword

The market for non-performing and non-core loan deals remains in business—but not in the way that many expected after COVID-19 shut down vast swathes of the European economy.

The banking sector's sale of legacy loans revived in 2021 following a marked slowdown in 2020, though the market did not return to the large-scale stocks of non-performing loans (NPLs) that were seen before the pandemic.

This may change if more distressed debt begins to emerge, having been protected by state interventions intended to support businesses affected by COVID-19. The events in Ukraine may also drive an increase in bad debt provisions and NPL volumes. For now, though, sellers, buyers and NPL market participants, such as servicers, are operating in a very different environment.

In this report, we take the temperature of that environment. The first section considers the changing dynamic of the marketplace, covering the outlook for NPLs, the rise of the secondary market transactions and the emergence of new types of NPL investors.

In section two, we take a deep dive into key markets across Europe. As in previous years, the economies of Southern Europe, led by Greece, Italy and Spain, were hotspots for NPL transactions. But other areas—notably Ireland, where NPL numbers were already relatively low—continue to see activity. Even in countries where banks are making very few disposals, the secondary market provides opportunities.

With so many unknowns, including the outcome of the situation in Ukraine and its impact on economics, the future for NPLs remains uncertain. But clear trends are emerging, from the growth of new entrants to the growing importance of data and analytics tools in driving value.

European NPLs: The journey from COVID-19 to Ukraine

While the spike in bad debt and subsequent tsunami of NPL and non-core loan deals that was anticipated due to COVID-19 did not materialise, the increasingly volatile market trends may lead investors to discover new and unexpected opportunities.

Regional spotlight on NPLs: Greece, Italy, Spain and beyond

Europe's banks continue to defy expectations that the pandemic would drive a significant increase in NPLs—in fact, according to the EBA, not a single country saw its banking sector's NPL ratio increase in 2021, with the vast majority reporting an improvement.

NPL market dynamics are changing, possibly for good

What does the future hold for NPLs? There's still plenty of business to be done, but buyers and sellers alike will need to change tack to get the most from the available opportunities.

European NPLs: The journey from COVID-19 to Ukraine

While the spike in bad debt and subsequent tsunami of NPL and non-core loan deals that was anticipated due to COVID-19 did not materialise, the increasingly volatile market trends may lead investors to discover new and unexpected opportunities.

European NPL volumes continued to decline in 2021, as unprecedented fiscal and monetary interventions gave many organisations room to breathe that otherwise might have collapsed in the face of pandemic-related disruption.

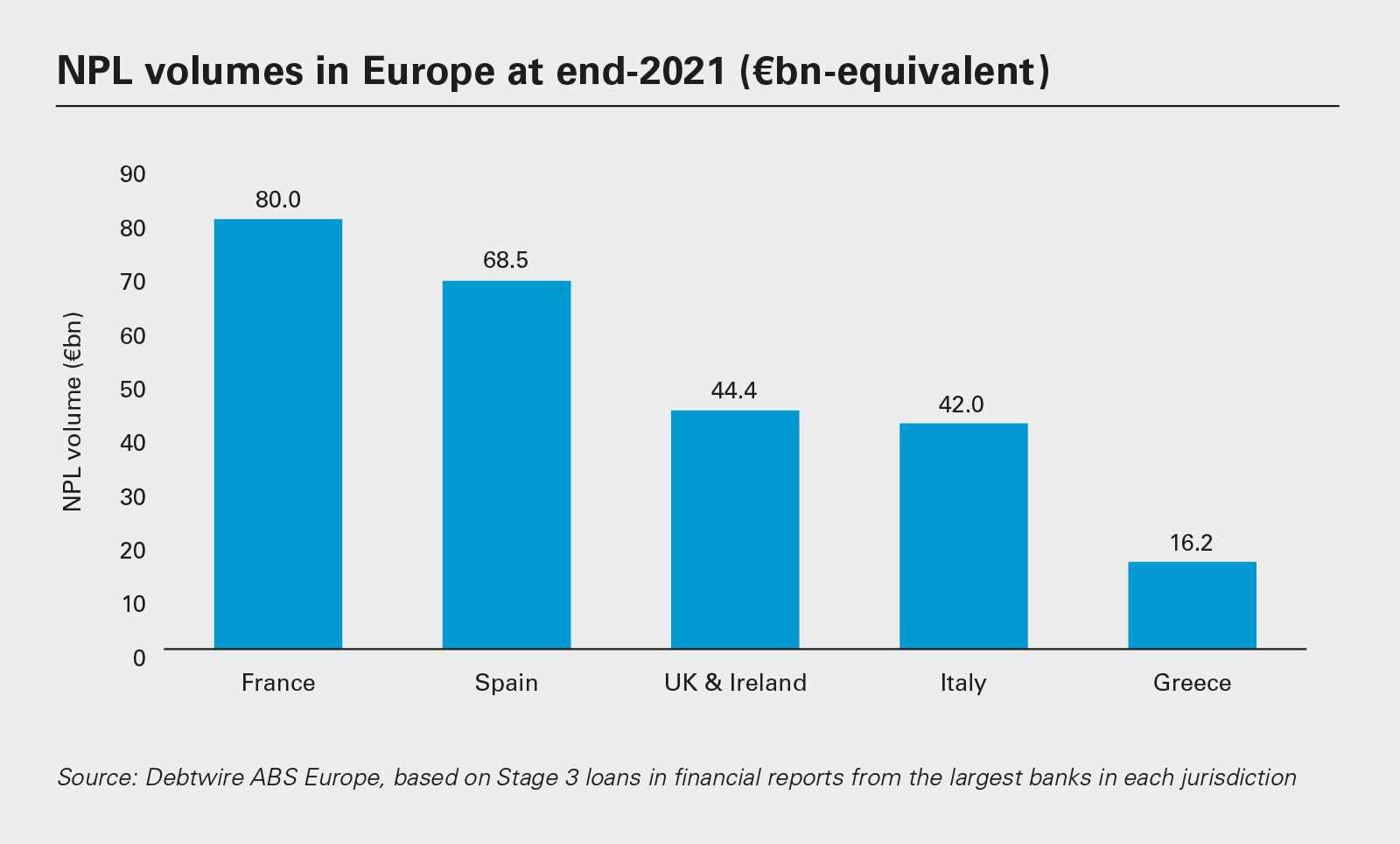

€300+ billion

Value of NPLs held by the largest banks in major jurisdictions across Europe at the end of 2021

As the European Banking Authority (EBA) reported in its Q4 2021 Risk Dashboard: "The risk of significant economic disruption due to COVID-19 has continued to decline in the last two quarters."

Data from Debtwire ABS Europe shows that, at the end of the year, banks across Europe still had more than €300 billion in Stage 3 loans on their books. Looking at the largest banks in major jurisdictions, the bulk of these were in France, Spain, the UK and Ireland, Italy and Greece, with approximately €250 billion in NPLs between them and France leading the pack at €80 billion. While these numbers are still high, they are a far cry from the more than €1 trillion in European NPLs recorded back in 2014.

According to the EBA, countries with significant NPL ratios at the beginning of 2021 registered particularly impressive improvement. Moreover, asset quality increased throughout the banking sector, with a 7 per cent decrease in NPLs in 2021.

Policymakers are also relatively relaxed about the potential impact of the events in Ukraine on Europe's banks. Having said that, the situation is taking its toll—Cyprus-based RCB Bank has unveiled plans to close its banking operations in the face of geopolitical uncertainty, while banks across Europe have flagged write-downs totalling close to US$10 billion due to the conflict. Still, exposures to Russia and Ukraine account for just 0.3 per cent of banks' assets, the EBA points out, and loans to these countries are concentrated in a handful of lenders.

For all that, however, it would be a mistake to grow complacent.

For one thing, the long-tail impact of COVID-19 remains unknown, particularly as governments have withdrawn pandemic-related support. Secondary effects of the crisis, such as supply chain disruption, inflationary pressure and rising interest rates, as well as the ongoing decline of the euro and various currency movements, continue to wash through Europe's economies and may tip some vulnerable businesses over the edge.

Notably, some governments are already considering further relief measures to insolvency laws to prevent a wave of real economy bankruptcies through uncertainties from the energy price shocks resulting from the Ukraine war.

Banks are already reporting evidence of potential stress. Volumes of Stage 2 loans—those in the early stages of underperformance—have begun to increase. So too have NPLs in sectors that have suffered disproportionately due to COVID-19.

Moreover, the events in Ukraine are casting a very long and dark shadow. The International Monetary Fund cut its global growth forecasts in April, citing "war-induced commodity price increases and broadening price pressures"—"Global growth is projected to slow from an estimated 6.1 per cent in 2021 to 3.6 per cent in 2022 and 2023. This is 0.8 and 0.2 percentage points lower for 2022 and 2023 than projected in January."

"EU/EEA banks also have indirect exposures [to the events in Ukraine] like those through businesses with trading links to these countries that could have a broader impact," warns the EBA's Dashboard.

For many market commentators, the potential for a recession in Europe in the next 12 months is becoming a real possibility.

Under the circumstances, it's entirely possible that we will see NPL volumes begin to climb once again.

The stock of NPLs still on the balance sheets means there is scope for further deleveraging, but much of the legacy work has now been completed

NPL disposals slow

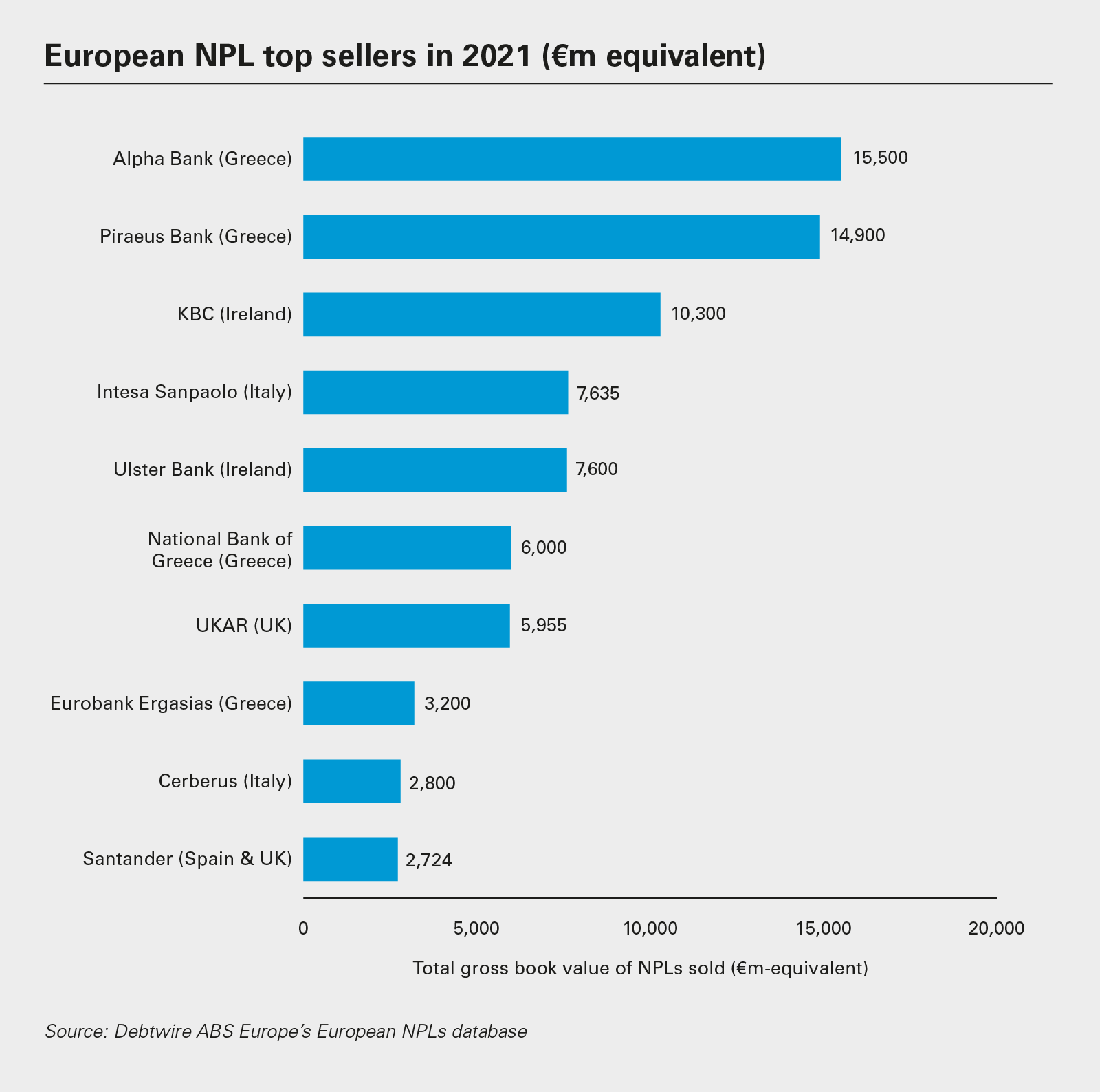

In the absence of a new stock of NPLs driven by the pandemic, however, the primary market for European banks disposing of toxic debt remains relatively flat. Disposals of legacy assets continue, particularly in markets such as Greece and Italy where state interventions underpinned such sales, but these have declined as banks worked through their backlogs.

Analysis by Debtwire ABS Europe shows Europe's banks selling approximately €100 billion in NPLs and non-core loans in 2021. That is higher than 2020, when the pandemic caused extensive dislocation in the market for much of the year.

To put last year's figures into context, the latest analysis by Debtwire ABS Europe shows that European NPL sales were above €100 billion in four out of five years between 2015 and 2019. In 2018, the peak year for disposals, banks completed transactions worth more than €200 billion.

The stock of NPLs still on the balance sheets means there is scope for further deleveraging, but much of the legacy work has now been completed. In the absence of new stock, a return to earlier volumes is simply not possible. Smaller deal sizes are likely to be the norm for the foreseeable future. These will often be follow-on deals that mirror the structure of disposals already completed.

The other reason to expect the pace of disposals to be limited is that state guarantee schemes operating in Italy and Greece are coming to the end of their lifetimes, due to end in 2022 and 2023 respectively.

Even if Italy extends its scheme, as the government hopes the European Commission will allow, structuring further disposals under these arrangements is becoming more challenging now that larger portfolios have been offloaded. The schemes require transactions to be of a certain size and structure to work effectively—because senior debt is guaranteed, but junior and mezzanine debt is not. Unless there is sufficient guaranteed senior debt to provide capital savings to offset any write-downs on the remainder of the debt, purchasers may struggle to achieve their targeted discounts.

There may not be enough NPLs left to create many more such arrangements.

The changing profile of the primary NPL market is leading to shifts in the buyer pool, with two clear and distinct groups of potential acquirers for portfolios coming up for sale.

The first of these groups consists of traditional investors, including private equity (PE) firms, hedge funds and credit funds. This group continues to feature the large investors that have been the mainstay of the buyer pool in recent years—for example, large and experienced PE acquirers of NPLs last year included KKR and Apollo—but smaller players are also entering the market. These are often focused on more digestible portfolio sizes or a specific niche in the market such as a certain sector.

In many cases, these investors are focused on securing a return via a sale on the secondary market. They invest to drive up value in the portfolios through rehabilitation or asset recovery, for example, before parcelling up tranches of their NPLs to sell.

In the opposite corner of the market, specialist servicing firms that helped banks and investors manage their NPL portfolios in the past are now emerging as prominent acquirers of loan books. Armed with expertise and experience in NPL management built up through servicing contracts, firms such as Intrum and Hoist have become active participants in the primary NPL market, securing value by driving improved recoveries from loan books acquired at substantial discounts.

In Greece, for example, Intrum took part in three separate deals in 2021 and five further transactions in Italy. Hoist was also active in both countries.

Consolidation to come?

One question is whether these market shifts presage a wave of broader consolidatory M&A activity. Managing NPL portfolios is capital- and people-intensive and does not necessarily generate the kind of returns being pursued by banks, particularly in an ongoing environment of low margins and reduced profitability.

For that reason, while banks will often see the value of retaining relationships with certain clients—even though their loans have slipped into non-performing territory—the case for offloading work-out units may be alluring. Carving out and selling such units to third-party servicers would reduce banks' cost bases, even if the underlying NPLs remain on their books, with a servicing contract agreed with the acquirer. In other cases, banks might look to offload the NPLs as well, taking further volumes off their balance sheets.

For acquirers of such units, long-term servicing contracts offer the prospect of stable revenue flows and rapid growth. Accepting the underlying exposure of the NPLs as a route to these benefits may be a risk worth taking, particularly for servicers with the analytical expertise to quantify such dangers more accurately.

The search for scale will be an important part of this story for servicers. For example, in April 2022, Hoist Finance announced the divestment of its UK credit management subsidiary, including its unsecured NPL portfolios.

As CEO Lars Wollung said at the time, this reflected the organisation's desire "to grow and invest in portfolios where [Hoist] can generate higher returns".

Servicer consolidation has already accelerated in other markets, with three or four large servicers now often dominating where a dozen firms were active five years or so ago.

Growth in the secondary market

One impact of declining NPL disposals by banks will inevitably be that the secondary market for NPLs is set to become proportionately more significant, at least in the short to medium term. The secondary market may also be boosted by EBA proposals to standardise the requirements for the information that NPL sellers must provide to prospective buyers. The EBA hopes its plans will improve transparency in the secondary market, enable cross-country comparisons and reduce information asymmetries between sellers and buyers.

The appetite of investors to offload some, if not all, of their NPL investments will be an important driver of the trend to increased secondary market activity. As funds seek to repay their own investors, they must either flip their NPLs into new funds or sell the assets. This is putting additional pressure on funds, since returns on loan books acquired prior to the pandemic are likely to have been hindered by the various disruptions experienced in the past two years. Court processes, for example, were postponed, and specialists with the skill to drive rehabilitation of loans were in short supply.

Market consolidation has similar implications. Where banks decide to carve out NPL servicing units, or specialist servicers look to restructure, the secondary market will also come into play.

Still, managing these portfolios well will be as crucial as ever to achieve hoped-for returns. In fact, the performance of European NPL securitisations was mixed in the second half of 2021, according to reporting by Debtwire ABS Europe, with gross collections ratios improving and deteriorating in roughly equal numbers. Italian and Spanish transactions were particularly likely to underperform relative to initial expectations.

The events in Ukraine could further muddy the waters in the secondary market. Loans that may look saleable at a certain price today may feel very different six months from now.

Given the chance to pursue a data-driven strategy to secure higher returns from NPLs and drive price discovery, new investors may be encouraged to enter the market.

Dividends from data

Improvements in data and analytics will play an important role here. Specialist investors are using more sophisticated tools to secure an increasingly granular understanding of portfolio performance. New entrants from the fintech industry are already raising the standard in this regard, creating new opportunities to generate value or offload underperforming assets. The dividing up of larger portfolios for smaller sales will accelerate as a result.

Consolidation plays into this theme. Resources for investment are concentrated in the hands of larger servicers and these businesses are growing their analytics competencies. As the volume of data on NPLs increases—not least with securitisations required to report key information regularly to drive transparency—this trend will no doubt pick up the pace.

Given the chance to pursue a data-driven strategy to secure higher returns from NPLs and drive price discovery, new investors may be encouraged to enter the market. PE funds and other investors with significant amounts of capital to deploy, coupled with the ability to leverage new data analytics tools, will become more active participants.

Dealing with reperforming loans

In an improving post-pandemic economic environment, some NPLs will have an opportunity to become performing loans once again. Banks that have disposed of such loans may wish to buy them back and rebuild a potentially profitable relationship with the customer. Equally, the acquirer may be keen to sell, hoping to realise a return on their original investment.

In practice, however, banking regulators can make such transactions difficult, even limiting a bank's ability to forge new relationships with such customers. Anxiety about arrangements that could increase the risk of further spikes in NPLs—for example, if loans slip once more—has led to restrictions on resales and arrangements of this kind.

The regulatory hazard is not to be overlooked. The need to enable banks to do business with customers that have recovered from difficulty is likely to become more pressing in the coming years. In some sectors, the outlook has improved very quickly in the wake of the pandemic. For example, the food and beverage industry has bounced back faster than expected, as has the tourism and hospitality industry. If banks and regulators can come to an agreement, NPLs in these areas may have a future.

Equally, as European countries seek to rebuild their economies, businesses will need access to new funding. Preventing them from working with banks they once knew well could inhibit growth.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: NPL volumes in Europe at end-2021 (€bn-equivalent) NPL (PDF)

View full image: NPL volumes in Europe at end-2021 (€bn-equivalent) NPL (PDF)

View full image: European NPL top sellers in 2021 (€m equivalent) (PDF)

View full image: European NPL top sellers in 2021 (€m equivalent) (PDF)

View full image: Top European NPL deals signed in 2021 by volume (PDF)

View full image: Top European NPL deals signed in 2021 by volume (PDF)