Financial institutions M&A: Sector trends - July 2022

Financial institutions M&A: Sector trends

July 2022

We highlight the key UK & European M&A trends in H2 2021 and H1 2022, and provide our insights into the outlook for M&A moving forward.

Introduction

Key highlights from H2 2021 include the following:

Banks: High levels of M&A across the UK and Europe, notwithstanding uncertainty ignited by the Russia/Ukraine conflict. Europe's banks have emerged from COVID-19 turmoil resolute in their ambitions to shed non-core assets, consolidate regional strongholds and rigorously pursue digitalisation strategies.

Fintech:Europe has bucked the global trend of tightening private capital purse strings. While successful funding rounds rage on, fintechs with critical mass are deploying M&A strategies to consolidate horizontally and integrate vertically.

Asset/Wealth Management: With over 350 deals in the European AWM sector in 2021, M&A consolidation activity is hotter than it has ever been in the past 15 years. Conventional wisdom is now under the microscope—is bigger really better?

Payments:Investor appetite is at an all-time high—while VC investors back growing service providers, PE investors supercharge IPO glide paths and established banks refuse to abdicate market share.

Stock Exchanges/Trading Venues:Europe’s FMI goes digital—data analytics, capital markets solutions, RegTech and DLT-based tech acquisitions feed the steady stream of M&A activity.

Brokers/Corporate Finance:Marginal improvement in investor sentiment for high-quality brokers, particularly across online brokerage, crypto trading and carbon credit trading.

Consumer Finance: BNPL steals the show—20 successful European BNPL provider funding rounds in the past 12 months, covering the full spectrum from Seed through to late-stage.

Specialty Finance/Marketplace Lending:Marginal uptick in M&A levels in the past 12 months, with property, automotive and revenue-based finance attracting the most investor interest.

European financial services M&A trends

Europe’s banks emerge from the COVID-19 pandemic resolute in their ambitions

High levels of M&A across the UK and Europe, notwithstanding uncertainty ignited by the Russia/Ukraine conflict. Europe's banks have emerged from COVID-19 turmoil resolute in their ambitions to shed non-core assets, consolidate regional strongholds and rigorously pursue digitalisation strategies

The long-awaited arrival of Europe’s new breed of decacorns

Europe has bucked the global trend of tightening private capital purse strings. While successful funding rounds rage on, fintechs with critical mass are deploying M&A strategies to consolidate horizontally and integrate vertically

With over 350 deals in the European AWM sector in 2021, M&A consolidation activity is hotter than it has ever been in the past 15 years. Conventional wisdom is now under the microscope—is bigger really better?

Investor appetite is at an all-time high—while VC investors back growing service providers, PE investors supercharge IPO glide paths and established banks refuse to abdicate market share

BNPL steals the show—20 successful European BNPL provider funding rounds in the past 12 months, covering the full spectrum from Seed through to late-stage

Our outlook for bank M&A is extremely positive despite current market uncertainty. Many of Europe’s lenders dedicated significant resources towards fine-tuning their development strategies during COVID-19 lockdowns. The result is emergence with clear goals into an increasing NIM environment.

Hyder Jumabhoy

High levels of M&A across the UK and Europe, notwithstanding uncertainty ignited by the Russia/Ukraine conflict. Europe's banks have emerged from COVID-19 turmoil resolute in their ambitions to shed non-core assets, consolidate regional strongholds and rigorously pursue digitalisation strategies.

Overview

Top 3 drivers of UK and European bank M&A in the past 12 months:

Embracing the future: Pruning overcapacity through internal reorganisations and ambitious non-core disposal programmes

Banks get match fit: Regional consolidation M&A and opportunistic acquisitions in core geographies/ business lines

Europe's challengers dig their heels in: More than five new entrants, more than five consolidation M&A deals and more than 10 successful funding rounds, in the UK alone

Current Market

Very high activity levels

We Are Seeing

Focus on internal restructurings:

Corporate reorganisations (e.g., Société Générale's merger of French retail bank with Credit du Nord)

Branch closures, as European banks cut costs and migrate to digital distribution models (e.g., Lloyds' closure of 60 UK branches and NatWest's closure of 56 UK branches)

Non-core disposals:

Banks concentrate on core markets/business lines (e.g., BNP Paribas sold BNPP Private Banking Spain, Bank of the West, Hello bank! Austria and ClimateSeed in the past 12 months)

European banks with Russian exposures respond to sanctions (e.g., Société Générale's disposal of Rosbank)

Russian banks are forced to retreat from international markets (e.g., Sberbank's disposals of its Croatian, Slovenian and Bosnian banking subsidiaries)

Domestic and regional consolidation:

Mergers of equals—Norway leads the charge in the past 12 months (e.g., Etne Sparebank & Sparebanken Vest and Sparebank 1 Sørøst-Norge & SpareBank 1 Modum)

Trade consolidators—Belgium (e.g., BNP Paribas Fortis' acquisition of Bpost Banque and Crelan's acquisition of AXA Bank Belgium) and Spain (e.g., Banca March's acquisition of BNP Paribas Private Banking Spain and Caixabank's acquisition of 51% of Bankia) top the leader boards as the hottest European consolidation markets in the past 12 months

Steady stream of successful large NPL/UTP/REO transactions, in the form of:

Portfolio sales (e.g., Santander's disposal of €600 million of SME NPLs to Tilden Park and €495 million of unsecured NPLs to Axactor)

Equity investment by financial sponsors into debt servicing JVs, combined with long-term servicing arrangements (e.g., Davidson Kempner's acquisition of 80% of licenced Greek debt servicer CEPAL, which services €10.8 billion of Alpha Bank's NPLs)

Incumbent banks boosting affiliated debt servicing capability (e.g., Piraeus Bank's acquisition of 52% of Trastor)

Outsourcing of debt servicing to industrial-scale specialist debt collection specialists (e.g., Hellenic Bank's outsourcing for €1.32 billion of NPLs to Oxalis/PIMCO)

Sophisticated securitisation structures (e.g., UniCredit securitisation of €2.2 billion of secured and unsecured NPLs, backed by the GACS state guarantee scheme)

Key drivers

European banks continuing to invest in the digital future:

Uptick in direct investments (e.g., BBVA's participation in funding rounds for Atom Bank and Neon)

Opting for the try-before-you-buy model (e.g., Barclays' partnerships with Rainmaking and SaveMoneyCutCarbon)

Tying the knot in the payments arena (e.g., NBG's JV with EVO Payments and UniCredit's JV with Nexi)

Galvanising market share amidst fierce competition from Europe's "challenger" and neo banks:

"Challengers" come of age—8 growth acquisitions in H2 2021. UK remains the hottest market (e.g., Tandem, OakNorth, Solarisbank, bank99 and Starling Bank all inked transformative deals in H2 2021)

Smaller lenders stockpile lending firepower—>25 neo banks across Europe raised capital, primarily from growth equity and venture capital sponsors

Steady stream of new entrants into the banking market—more than 5 new entrants into the UK banking market in H2 2021

Bank balance sheet deleveraging, driven by:

Mounting pressure on Europe's systemic banks to deliver their strategic capital and restructuring plans

Europe's banks actively managing Russian debt exposures (e.g., European banks have approximately US$84 billion of exposure to Russia, a significant portion of which is expected to sour)

Europe's banks being able to re-assess borrower default levels following withdrawal of government-backed COVID-19 credit support measures (e.g., provisioning levels within pan-European banks have nearly doubled year-on-year as they brace for expected losses due to the COVID-19 pandemic)

Hungry buy-side recipients of financial assets, including financial sponsors (e.g., KKR's acquisition of €580 million of residential mortgage NPLs from CaixaBank), industrial-scale debt servicers (e.g., Hoist's acquisition of €2.1 billion of unsecured consumer and SME NPLs from Alpha Bank and acquisition of €400 million of unsecured NPLs from CaixaBank) and specialist credit managers (e.g., CarVal's acquisition of €1.1 billion of mortgage NPLs from KBC Bank Ireland)

Trends to watch

Government intervention to curb cost-cutting through branch closures, remediating concerns relating to reasonable customer access to cash facilities

Established banks challenging the challengers (e.g., Société Générale's Boursorama, Intesa Sanpaolo's Isybank and NatWest's Mettle)

Increasing regulator focus on ESG considerations:

Increasing remit of prudential regulators to ensure UK and European banks meet net-zero carbon emission targets

Increasing scrutiny of sustainability disclosures

Turkey dips its toes into the NPL sale market:

"Test deals" are still relatively small (e.g., Turkiye Garanti Bankasi's disposal of US$37 million of NPLs to Gelecek Varlik Yonetimi)

Larger deals coming to market could attract international interest (e.g., DenizBank's disposal of US$93.9 million of NPLs)

Currently, only local asset managers are permitted to purchase (e.g., Isbank's disposal of US$100 million of NPLs to Emir Varlik Yonetim, Istanbul Varlik Yonetim, Gelecek Varlik Yonetim, Hedef Varlik Yonetim and Arsan Varlik Yonetim)

Local asset managers bulk up in preparation (e.g., merger between Dunya Varlik Yonetim, Hisar Stratejik Yatirimlar and Merkez Alacak Yonetimi Danismanlik ve Destek Hizmetleri)

Growing legislative realisation that small NPL portfolio sales to local debt collection agencies are not helping Turkey's endemic bad debt situation. Positive signs that the following archaic laws could soon be revisited:

Banking laws: NPLs can only be sold to Turkish asset management companies, while UTPs (i.e., Group II loans under close monitoring) can theoretically be sold to foreign investors

Data protection laws: As a general rule, Turkish banks are prohibited from disclosing client-related information to third parties. Exemptions are uncomfortably narrow

Capital markets laws: Asset-backed securities and covered bonds can only be issued in respect of performing loans (i.e., Group I receivables), not NPLs

"Hot topic"—new EU directive on credit servicers and purchasers which will impose onerous pre-sale disclosure and post-sale reporting obligations on European banks (i.e., EU Member States are to publish their implementing rules by 29 December 2023 and to bring them into effect on 30 December 2023)

Increase in activist investor activity aimed at:

Focussing strategic objectives, as Europe's banks leave the COVID-19 pandemic and related government relief measures behind

Tackling climate change and biodiversity loss (Barclays, Standard Chartered and ING have already suffered disruption at 2022 AGMs)

Our M&A forecast

Strong growth in M&A activity as Europe's banks exit hiatus, hastened by the Russia/Ukraine conflict, into a higher interest rate environment. Growth to be spurred by restocked war chests following non-core business disposals, freeing-up of balance sheet capacity through legacy NPL portfolio sales and the need to consolidate market share as well as implement ambitious digital transformation strategies.

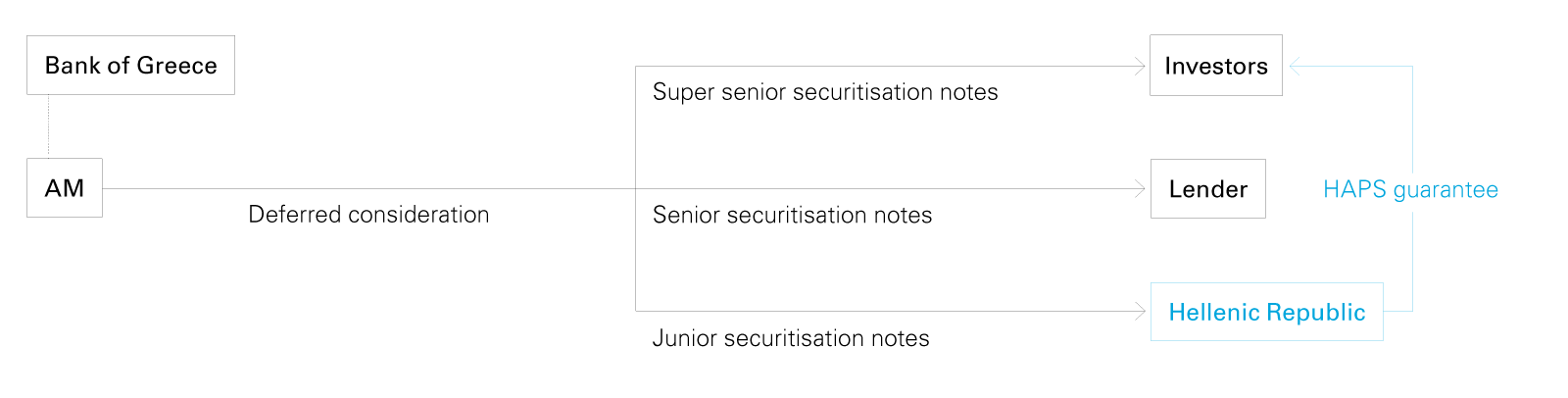

Bank of Greece approves establishment of asset manager (AM)

Lender conducts outright sale of NPLs at book value (thereby achieving significant risk transfer (SRT)), together with a portion of deferred tax credits (DTCs), to AM. Quantum of DTCs is calibrated such that market value of NPLs is achieved across NPLs and DTCs

AM pays for NPLs and DTCs as follows:

Upfront consideration to Lender: Book value of NPLs, paid in kind through issuance by AM of senior securitisation notes to Lender

Deferred consideration to Lender: Delta between book and market value of NPLs, paid in cash to Lender once recoveries under NPLs reach pre-agreed threshold

Consideration to Hellenic Republic: Value of DTCs, paid in kind through issuance by AM of junior securitisation notes to Hellenic Republic. Junior notes are subordinated to senior notes (i.e., will only benefit from recoveries generated by NPLs once principal amount of senior notes and deferred consideration have been paid/repaid in full)

Option to issue super senior notes to 3rd-party investors to finance acquisition of NPLs, which benefit from Hellenic Asset Protection Scheme (HAPS) guarantee

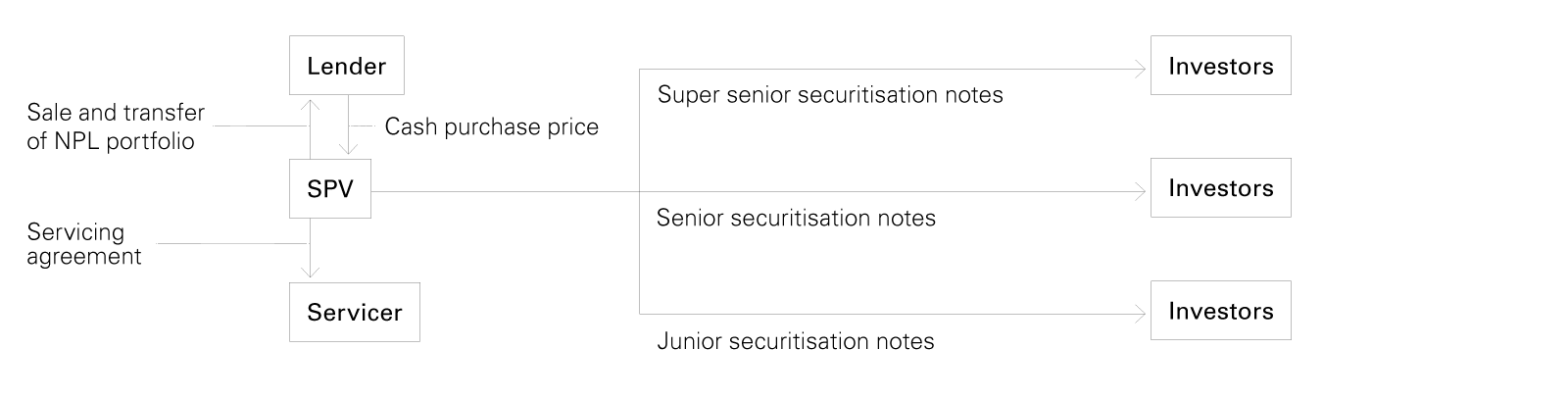

Option 2: 3rd-party/Retained securitisation structure (not supported by HAPS)

Orphan special purpose vehicle (SPV) acquires NPLs from Lender, in return for pre-agreed cash purchase price

SPV generates cash for payment of purchase price through issuance of various tranches of securitisation notes (e.g., senior, mezzanine, junior, etc.)

Two alternatives:

3rd-party: SRT is achieved since securitisation notes are subscribed for by 3rd-party investors

Retained: Securitisation notes are subscribed for by Lender. Lender benefits from more favorable capital/tax treatment in lieu of holding securities (as opposed to underlying NPLs)

SPV appoints specialist debt servicer to manage NPLs

Principal and interest payments under securitisation notes are funded from NPL recoveries by servicer

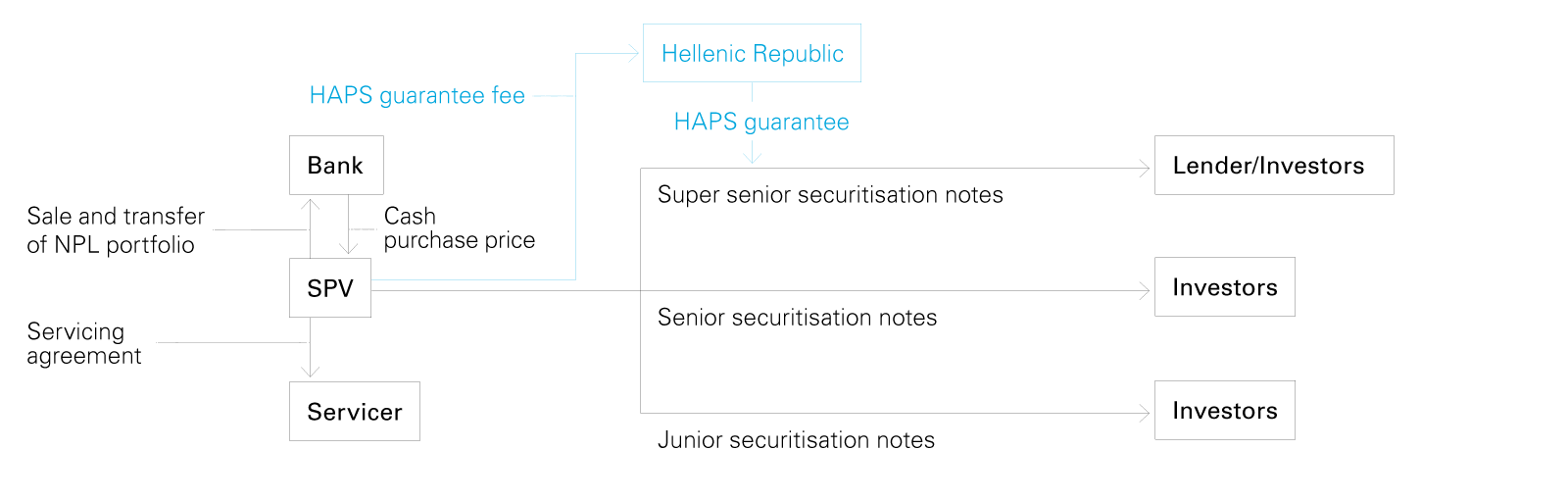

Option 3: 3rd-party securitisation structure supported by HAPS

Orphan SPV acquires NPLs from Lender, in return for pre-agreed cash purchase price

SPV generates cash for payment of:

Purchase price for NPLs to Lender, and

HAPS guarantee fee payments to Hellenic Republic, through issuance of various tranches of securitisation notes (e.g., senior, mezzanine, junior, etc.) to 3rd-party investors (thereby achieving SRT for Lender). Amount of HAPS guarantee fee comprises base rate (benchmarked against credit default swap with equivalent rating) plus penalty element if senior securitisation notes have not been redeemed in full by 3rd anniversary of issuance (calculated by reference to interest/principal payments in respect of senior securitisation notes in first 3 years)

SPV appoints specialist debt servicer to manage NPLs

Securitisation notes have floating coupon and flexible redemption to facilitate pass-on of NPL recoveries by servicer

Senior securitisation notes benefit from HAPS guarantee (with respect to principal and interest) only if:

Condition 1: Rating of securitisation notes is ≥BB-

Condition 2: >50% of junior securitisation notes have been subscribed for by 3rd-party investors

Condition 3: Sufficient quantum of junior and/or mezzanine securitisation notes have been subscribed for by 3rd-party investors to enable accounting re-recognition of NPLs from Lender's balance sheet

Banks—Publicly reported deals & situations

Restructurings/Capital injections

ECB aims to complete a detailed assessment of how international banks manage their EU business by early 2022 (Financial Times, December 2021)

Lifeline funding:

Banque Misr (Egypt): US$201.1 million investment in Afreximbank (February 2022)

Baltic International Bank (Latvia): Successful €12 million funding round (November 2021)

Corporate reorganisations:

J.P. Morgan SE, J.P. Morgan Luxembourg & J.P. Morgan Ireland (Pan-European): Merger (January 2022)

Société Générale (France): Merger of French retail bank with Crédit du Nord (October 2021)

Branch closures

Nationwide Building Society will not leave any town or city in which it is based without a branch until at least 2024 (Finextra, June 2022)

FCA to be granted new powers over the UK's largest banks and building societies to ensure that cash withdrawal and deposit facilities are available across the UK (Financial Times, May 2022)

Cambuslan and Rochford were two UK locations chosen to host shared branches formed out of a collaborative effort between the state-owned post office and Britain's largest retail banks (Financial Times, January 2022)

Access to Cash Action Group, supported by UK retail banks, Age UK, Toynbee Hall and the Federation of Small Businesses, pioneers network of UK shared banking hubs (Finextra, December 2021)

UK banks shut 736 branches in 2021, according to consumer group Which?, which is calling on lenders to pause further closures (Finextra, December 2021)

Dankse Bank (Northern Ireland): Closure of 4 Northern Irish branches (May 2022)

Barclays (UK): Closure of 103 UK branches (April 2022)

HSBC (UK): Closure of 69 UK branches (March 2022)

Lloyds (UK): Closure of 60 UK branches (March 2022)

Halifax (UK): Closure of 17 UK branches (March 2022)

NatWest (UK): Closure of 56 UK branches (February 2022)

Unicaja (Spain): Closure of 395 Spanish branches (February 2022)

TSB (UK): Closure of 70 UK branches (November 2021)

Bank of Ireland (Ireland): Closure of 88 UK branches (October 2021)

Banco Sabadell (Spain): Closure of 320 Spanish branches (September 2021)

Disposals of non-core businesses

Deal highlight:

White & Case advised Alpha Bank, the largest of Greece's four systemic banks by market capitalisation, on the disposal of Alpha Bank Albania, its Albanian banking subsidiary, to Hungary's OTP Bank.

Deal highlight:

White & Case advised UniCredit on its disposal of the majority of its remaining 20% stake in the Turkish bank, Yapı ve Kredi Bankası, to Koç Holding.

Otkritie Bank (Russia): Disposal of 90% of Tochka (June 2022)

ING (France): Disposal of French retail banking business (April 2022)

Sovcombank (Russia): Disposal of Septem Capital (February 2022)

Iccrea (Italy): Disposal of 60% of BCC Pay (February 2022)

Citadele bank (Switzerland): Disposal of Kaleido Privatbank (January 2022)

Emirates NBD (UAE): Disposal of controlling interest in Dubai Bank (December 2021)

BNP Paribas (USA): Disposal of Bank of the West (December 2021)

NatWest (Ireland): Disposal of Ulster Bank's retail, SME and asset finance businesses (December 2021)

Commerzbank (Hungary): Disposal of Commerzbank Zrt (December 2021)

Alpha Bank (Albania): Disposal of Alpha Bank Albania (December 2021)

Santander (Poland): Disposal of 10% of Aviva Towarzystwo Ubezpieczeń na Życie and Santander Aviva Towarzystwo Ubezpieczeń (December 2021)

HSBC (France): Disposal of French retail banking business (November 2021)

Raiffeisen Bank International (Bulgaria): Disposal of Raiffeisenbank Bulgaria (November 2021)

Getin Holding (Ukraine): Disposal of Idea Bank Ukraine (November 2021)

UniCredit (Turkey): Disposal of 20% of Yapi ve Kredi Bankasi (November 2021)

CaixaBank (Austria): Disposal of 9.92% of Erste Group Bank (November 2021)

NLB (Serbia): Disposal of Komercijalna banka (October 2021)

BTA Bank (Ukraine): Disposal of PAO BTA Bank (October 2021)

Crédit Agricole (Serbia): Disposal of Crédit Agricole Srbija (August 2021)

Banque Fédérative du Crédit Mutuel (France): Disposal of FLOA (July 2021)

Handelsbanken (Nordics): Disposal of card acquiring business (July 2021)

BNP Paribas (Austria): Disposal of Hello bank! Austria (July 2021)

Banco Sabadell (Andorra): Disposal of stake in BancSabadell d'Andorra (July 2021)

ING (Austria): Disposal of Austrian retail banking business (July 2021)

Arion Bank (Iceland): Disposal of Valitor (July 2021)

Danske Bank (Luxembourg): Disposal of Luxembourg wealth management business (July 2021)

Sanctions-driven sales

ECB has taken the rare step of appointing a temporary administrator to oversee the wind-down of RCB Bank, a Cypriot lender with strong Russian ties (Financial Times, March 2022)

Ikea (Russia): Disposal of Ikano Bank (June 2022)

Alfa-Bank (Kazakhstan): Disposal of Alfa-Bank Kazakhstan (April 2022)

Société Générale (Russia): Disposal of Rosbank (April 2022)

Sberbank (Croatia): Disposal of Sberbank d.d. (March 2022)

Sberbank (Slovenia): Disposal of Sberbank banka d.d (March 2022)

Sberbank (Bosnia and Herzegovina): Disposal of Sberbank BH (March 2022)

Alisher Usmanov (Uzbekistan): Disposal of 61.54% of Kapitalbank (March 2022)

EBA has raised concerns over banks' exposure to hospitality and leisure-related sectors, where NPL ratios are on the rise. (S&P Global, December 2021)

EU banks could suffer €308 billion of credit losses by 2023 if COVID-19 and the low interest rate environment were to be prolonged, with the largest losses across France, Italy, Germany, the US, Spain and the Netherlands. (S&P Global, July 2021)

NPL/UTP disposals:

Komplett Bank (Norway): Disposal of €68.68 million of consumer NPLs to Intrum (May 2022)

Hellenic Bank (Cyprus): Disposal of €1.32 billion of NPLs to PIMCO (April 2022)

Alpha Bank (Cyprus): Disposal of €2.4 billion of NPLs and REOs to Cerberus Capital Management (February 2022)

KBC Bank Ireland (Ireland): Disposal of €1.1 billion of mortgage NPLs to CarVal Investors (February 2022)

UniCredit (Italy): Disposal of €222 million of secured and unsecured corporate NPLs to Kruk (January 2022)

Alpha Bank (Greece): Disposal of €2.1 billion of unsecured consumer and SME NPLs to Hoist (December 2021)

Novo Banco (Portugal): Disposal of €164.4 million of NPLs to AGG Capital Management and Deva Capital Management (December 2021)

Piraeus Bank (Greece): Disposal of (unspecified) securitised NPL portfolio to Intrum and Serengeti Asset Management (December 2021)

DenizBank (Turkey): Disposal of US$93.9 million of NPLs (December 2021)

Turkiye Garanti Bankasi (Turkey): Disposal of US$37 million of NPLs to Gelecek Varlık Yönetimi (December 2021)

Santander (Spain): Disposal of €600 million of SME NPLs to Tilden Park (December 2021)

CaixaBank (Spain): Disposal of €580 million of residential mortgage NPLs to KKR (November 2021)

Santander (Spain): Disposal of €459 million of unsecured NPLs to Axactor (November 2021)

CaixaBank (Spain): Disposal of €400 million of unsecured NPLs to Cabot and Hoist (November 2021)

NatWest (UK): Disposal of £400 million of commercial real estate NPLs to Attestor, Octane Capital Partners and Ellandi (September 2021)

Acquiring debt/REO servicing capacity:

Piraeus Bank (Greece): Acquisition of 52% of Trastor (January 2022)

Performing portfolio trades (sellers):

Ulster Bank (Ireland): Disposal of €5.7 billion of performing mortgage loans to Allied Irish Bank (June 2022)

Allied Irish Bank (UK): Disposal of £600 million of performing UK SME loans to Allica Bank (November 2021)

Kensington Mortgages (UK): Disposal of £1 billion of performing mortgage loans to Starling Bank (November 2021)

KBC Bank Ireland (Ireland): Disposal of €8.8 billion of performing mortgage loans to Bank of Ireland (October 2021)

Finqus (Netherlands): Disposal of €1.5 billion of mortgage loans to NIBC Bank (July 2021)

Acquisitions – financial sponsors:

Tilden Park (Spain): Acquisition of €600 million of SME NPLs from Santander (December 2021)

KKR (Spain): Acquisition of €580 million of residential mortgage NPLs from CaixaBank (November 2021)

Axactor (Spain): Acquisition of €459 million of unsecured NPLs from Santander (November 2021)

Attestor, Octane Capital Partners and Ellandi (UK): Acquisition of £400 million commercial real estate NPLs from NatWest (September 2021)

Acquisitions – industrial-scale debt servicing:

Intrum (Norway): Acquisition of €68.68 million of consumer NPLs from Komplett Bank (May 2022)

PIMCO (Cyprus): Acquisition of €1.32 billion of NPLs from Hellenic Bank (April 2022)

Kruk (Italy): Acquisition of €222 million of secured and unsecured corporate NPLs from UniCredit (January 2022)

Hoist (Greece): Acquisition of €2.1 billion of unsecured consumer and SME NPLs from Alpha Bank (December 2021)

Intrum and Serengeti Asset Management (Greece): Acquisition of (unspecified) securitised NPL portfolio from Piraeus Bank (December 2021)

Cabot and Hoist (Spain): Acquisition of €400 million of unsecured NPLs from CaixaBank (November 2021)

Acquisitions – asset/credit managers:

Cerberus Capital Management (Cyprus): Acquisition of €2.4 billion of Cypriot NPLs and REOs from Alpha Bank (February 2022)

CarVal Investors (Ireland): Acquisition of €1.1 billion of mortgage NPLs from KBC Bank Ireland (February 2022)

AGG Capital Management and Deva Capital Management (Portugal): Acquisition of €164.4 million of NPLs from Novo Banco (December 2021)

Gelecek Varlık Yönetimi (Turkey): Acquisition of US$37 million of NPLs from Turkiye Garanti Bankasi (December 2021)

Secondary market buyers:

illimity Bank (Italy): Acquisition of €179 million of NPLs (July 2021)

Performing portfolio trades (buyers):

Allied Irish Bank (Ireland): Acquisition of €5.7 billion of performing mortgage loans from Ulster Bank (June 2022)

Allica Bank (UK): Acquisition of £600 million of performing UK SME loans from Allied Irish Bank (November 2021)

Starling Bank (UK): Acquisition of £1 billion of performing mortgage loans from Kensington Mortgages (November 2021)

Bank of Ireland (Ireland): Acquisition of €8.8 billion of performing mortgage loans from KBC Bank Ireland (October 2021)

NIBC Bank (Netherlands): Acquisition of €1.5 billion of mortgage loans from Finqus (July 2021)

Regional & domestic market consolidation

Deal highlight:

White & Case advised Atlas Mara and the other controlling shareholders on the disposal of Union Bank of Nigeria, one of Nigeria's longest-standing and most respected lenders, to Titan Trust Bank.

Deal highlight:

White & Case advised Landesbank Baden-Württemberg, the full-service savings bank in Baden-Württemberg Rhineland-Palatinate and Saxony, on its acquisition of Berlin Hyp, a leading commercial real estate financing provider in Germany.

Deal highlight:

White & Case advised Spain's BBVA on its €2.25 billion voluntary tender offer to acquire 50.15% of T. Garanti Bankası, the second-largest bank in Turkey.

Deal highlight:

White & Case advised France's Crédit Mutuel Arkéa on the disposal of Keytrade Bank Luxembourg, the online challenger bank, to Swissquote Bank.

Banks are on pace to merge at a level not seen since the 2008 financial crisis. It is a sharp turnaround from 2020, when the economy spiralled and many regional and community banks put merger plans on the shelf. (Financial News, September 2021)

Lenders are tipped for further M&A and capital markets activity amid positive signs for the sector, including confidence in asset quality and the prospect of inflation. (Mergermarket, July 2021)

Mergers of equals:

Budapest Bank & Magyar Takarék Bankholding (Hungary): Merger (February 2022)

Etne Sparebank & Sparebanken Vest (Norway): Merger (February 2022)

National Commercial Bank & Samba Financial Group (Saudi Arabia): Merger (January 2022)

Atlas Mara Zambia & Access Bank Zambia (Zambia): Merger (October 2021)

Helsinki Area Cooperative Bank, Itä-Uudenmaan Osuuspankki & Uudenmaan Osuuspankki (Finland): Merger (October 2021)

Trusted Novus Bank (Switzerland): Acquisition of Kaleido Privatbank (January 2022)

BNP Paribas Fortis (Belgium): Acquisition of Bpost Banque (January 2022)

Swissquote Bank (Luxembourg): Acquisition of Keytrade Bank Luxembourg (January 2022)

Alfa Bank Belarus (Belarus): Acquisition of 99.98% of FransaBank (January 2022)

CaixaBank (Spain): Acquisition of 51% of Bankia (December 2021)

Titan Trust Bank (Nigeria): Acquisition of 89.39% of Union Bank of Nigeria (December 2021)

Permanent TSB (Ireland): Acquisition of Ulster Bank's retail, SME and asset finance businesses (December 2021)

Erste Bank Hungary (Hungary): Acquisition of Commerzbank Zrt (December 2021)

Crelan (Belgium): Acquisition of AXA Bank Belgium (December 2021)

First Abu Dhabi Bank (Egypt): Acquisition of Bank Audi Egypt (December 2021)

OTP Bank (Albania): Acquisition of Alpha Bank Albania (December 2021)

My Money Group (France): Acquisition of HSBC's French retail banking business (November 2021)

BBVA (Turkey): Acquisition of 50.15% of T. Garanti Bankası (November 2021)

MONETA Money Bank (Czech Republic): Acquisition of Air Bank (November 2021)

KBC Bank (Bulgaria): Acquisition of Raiffeisenbank Bulgaria (November 2021)

First Ukrainian International Bank (Ukraine): Acquisition of Idea Bank Ukraine (November 2021)

Nordax Bank (Norway): Acquisition of Bank Norwegian (November 2021)

Wielkopolski Bank Spółdzielczy (Poland): Acquisition of 72% of Bank Nowy BFG (October 2021)

Spar Nord Bank (Denmark): Acquisition of 36.71% of Danske Andelskassers Bank (October 2021)

Banka Postanska (Serbia): Acquisition of Komercijalna banka (October 2021)

Kaspi.kz (Ukraine): Acquisition of PAO BTA Bank (October 2021)

Crèdit Andorrà (Andorra): Acquisition of Vall Banc (September 2021)

Sparebank 1 SR-Bank (Norway): Acquisition of c. 38% of Sparebank 1 Forvaltning (September 2021)

KCB (Rwanda): Acquisition of Banque Populaire du Rwanda (August 2021)

Raiffeisen Bank International (Serbia): Acquisition of Crédit Agricole Srbija (August 2021)

BAWAG (Austria): Acquisition of Hello bank! Austria (July 2021)

MoraBanc (Andorra): Acquisition of stake in BancSabadell d'Andorra (July 2021)

Raiffeisen Bank International (Czech Republic): Acquisition of Equa Bank (July 2021)

Strategic M&A— COVID-19 pandemic creates opportunities for some

Banco BPM (Italy): Acquisition of 81% of Bipiemme Vita (April 2022)

Aareal Bank (Germany): Acquisition of CollectAI (March 2022)

BAWAG Group (US): Acquisition of Idaho First Bank (February 2022)

Sovcombank (Russia): Acquisition of CiV Life (December 2021)

HSBC (India): Acquisition of L&T Finance's Indian mutual funds business (December 2021)

Santander (US): Acquisition of remaining stake in Santander Consumer USA (August 2021)

HSBC (S'pore): Acquisition of AXA Singapore (August 2021)

BNP Paribas (France): Acquisition of FLOA (July 2021)

Otkritie Bank (Russia): Acquisition of 40% of Tochka (July 2021)

BNP Paribas (France): Acquisition of remaining 50% of Exane (July 2021)

Union Bancaire Privée (Luxembourg): Acquisition of Danske Bank's Luxembourg wealth management business (July 2021)

Digitalisation

Please refer to the 'Fintech' sub-Report in this series.

Wide investor universe

Deal highlight:

White & Case advised The Co-operative Bank on the acquisition of a significant minority interest in the bank by J.C. Flowers & Co and Bain Capital.

Deal highlight:

White & Case advised Goldman Sachs on the €1.8 billion consortium take-private offer, alongside Advent, Centerbridge, CPPIB and LGT, for Aareal Bank, the Frankfurt Stock Exchange–listed specialist property lender.

Deal highlight:

White & Case advised Orange, the French telecommunication group, on the acquisition of the remaining minority stake held by Groupama in Orange Bank, the French neo-bank.

Deal highlight:

White & Case advised Syndeo Capital, the UK-based financial services specialist financial sponsor, on: its long-term strategic partnership with iFast Corp., the Singapore-listed WealthTech unicorn, in relation to BFC Bank; and its winning auction bid to acquire BFC Bank, a fully licensed UK deposit-taking institution providing cross-border banking and FX services.

PE firms have set their sights on mid-tier UK banks, but a divergence over valuations has stymied deal-making—for now (S&P Global, November 2021)

Private equity:

Gulf Islamic Investments (UAE): Acquisition of Anglo-Gulf Trade Bank (June 2022)

Beach Point Capital and Monarch Alternative Capital (Spain): Acquisition of 40% of WiZink Bank (January 2022)

BDPST (Hungary): Acquisition of 57% of Gránit Bank (January 2022)

Eradah Capital (UAE): Acquisition of controlling interest in Dubai Bank (December 2021)

AAA Capital (Lithuania): Acquisition of Medicinos Bankas (December 2021)

Aareal Bank (Germany): Take-private offer by consortium comprising Goldman Sachs, Advent, Centerbridge, CPPIB and LGT (December 2021)

J.C. Flowers & Co and Bain Capital (UK): Acquisition of minority stake in The Co-operative Bank (September 2021)

Foreign strategic:

Banco Master (Portugal): Acquisition of Banco BNI Europa (January 2022)

Altarius Capital (Portugal): Acquisition of BNI Europa (October 2021)

Pioneer Capital Invest (Russia): Acquisition of Asian-Pacific Bank (October 2021)

Unicorns:

Coinshares (Switzerland): Acquisition of 20.8% of FlowBank (March 2022)

iFast Corp (UK): Acquisition of 85% of BFC Bank (January 2022)

Non-bank:

luteCredit (Moldova): Acquisition of 49.7% of Energbank (February 2022)

Orange (France): Acquisition of remaining 21.7% of Orange Bank (October 2021)

UHNW/family offices/private investment groups:

Kirill Sokolov (Russia): Acquisition of 54% of Vitabank (February 2022)

Vladimir Potanin (Russia): Acquisition of Rosbank (April 2022)

Rasim Ismailov (Belarus): Acquisition of Paritetbank (October 2021)

IPOs/rights issues:

Alpha Bank (Greece): Successful €800 million equity capital raise (July 2021)

Market appetite:

Irish Government (Ireland): Disposal of 1.04% of the Bank of Ireland (January 2022)

Shari Arison (Israel): Disposal of 11.35% of Hapoalim (December 2021)

Irish Government (Ireland): Disposal of 1.97% of Bank of Ireland (November 2021)

UK Government (UK): Disposal of 1% of NatWest Group (November 2021)

Fierce competition for established banks

Deal highlight:

White & Case advised N26, a Berlin-based neo-banking unicorn, on certain regulatory and compliance considerations in the context of its US$900 million Series E funding round.

UK's FCA has found evidence of growing competition in financial services, driven in part by the COVID-19 pandemic and the rise of digital challenger banks. (Finextra, January 2022)

Funds donated by The Banking Competition Remedies Board to inject competition into the UK's business banking market have led to a 13% shift away from large incumbent banks to smaller rivals. (Finextra, November 2021)

Inorganic growth of "challenger" banks:

Raisin Bank (Germany): Acquisition of payments division of Bankhaus August Lenz (June 2022)

bunq (Netherlands): Acquisition of TriCount (May 2022)

Oxbury (UK): Acquisition of Naqoda (March 2022)

Chetwood Financial (UK): Acquisition of Yobota (March 2022)

Tandem Bank (UK): Acquisition of Oplo (January 2022)

Monese (Ireland): Acquisition of Trezeo (December 2021)

OakNorth (UK): Acquisition of Fluidly (December 2021)

Solarisbank (UK): Acquisition of Contis (July 2021)

Starling Bank (UK): Acquisition of Fleet Mortgages' buy-to-let business (July 2021)

Yandex (Russia): Acquisition of Acropol Bank (July 2021)

bank99 (Austria): Acquisition of ING's Austrian retail banking business (July 2021)

bunq (Netherlands): Acquisition of Capitalflow Commercial Finance (July 2021)

IPOs:

Rocker (Sweden): €149 million Nasdaq First North IPO (October 2021)

New entrants:

Bank of London (Clearing): UK launch (November 2021)

Monument (Retail banking): UK launch (November 2021)

Chase (Retail banking): UK launch (September 2021)

Recognise Bank (SME banking): UK launch (August 2021)

Bank North (SME banking): UK launch (September 2021)

JVs:

Recognise Bank: Key account infrastructure JV with ClearBank (November 2021)

Chip: Savings accounts JV with ClearBank (October 2021)

Neo-banks stockpile growth capital:

Trade Republic (Germany): Successful €250 million Series C extension funding round led by Ontario Teachers' Pension Plan Board (June 2022)

Juni (Sweden): Successful US$206 million Series B equity and debt funding round led by a GCC-based SWF Capital and TriplePoint Capital respectively (June 2022)

4Trans (Czech Republic): Successful €18 million Venture funding round led by Atmos Ventures, Tera Ventures, Lighthouse Ventures and Advance Global Capital (June 2022)

ClearBank (UK): Successful £175 million equity funding round led by Apax Digital (March 2022)

Lunar (Denmark): Successful €70 million Series D-2 funding round led by Heartland, Kinnevik and Tencent (March 2022)

Atom Bank (UK):Successful £75 million investment from BBVA and Toscafund (February 2022)

Neon (Brazil): US$300 million equity investment from BBVA (February 2022)

Vivid Money (Germany): Successful €100 million Series C funding round led by Greenoaks Capital (February 2022)

Alpian (Switzerland): Successful £15.6 million Series B+ funding round led by Fideuram-Intesa Sanpaolo Private Banking (April 2022)

Starling Bank (UK): Successful US$130.5 million Series D funding round led by Harold McPike, Fidelity Investments, RPMI Railpen, QIA and Goldman Sachs (April 2022)

Seba Bank (Switzerland): Successful €100 million Series C funding round led by Altive, Ordway Selections, Summer Capital and DeFi Technologies (January 2022)

Qonto (France): Successful €486 million Series D funding round led by Tiger Global and TCV (January 2022)

Monzo (UK): Successful US$100 million follow-on Series H funding round led by Tencent (January 2022)

First Digital Bank (Israel): Successful US$120 million Series A funding round led by Julius Bär and Tencent (December 2021)

Monzo (UK): Successful US$500 million Series H funding round led by Abu Dhabi Growth Fund (December 2021)

TymeBank (South Africa): Successful US$180 million Series B funding round led by Tencent (December 2021)

bunq (Netherlands): Successful €193 million Series A funding round led by Pollen Street Capital (December 2021)

Bank of London (UK): Successful US$90 million Venture funding round led by ForgeLight (November 2021)

Allica Bank (UK): Successful £110 million Series B funding round led by Atalaya Capital and Warwick Capital (November 2021)

N26 (Germany): Successful US$900 million Series E funding round led by Third Point Ventures and Coatue Management (October 2021)

Zopa (UK): Successful US$300 million pre-IPO funding round led by SoftBank Vision Fund II (October 2021)

Kuda (UK/Nigeria): Successful US$55 million post-Seed funding round led by Valar Ventures and Target Global (August 2021)

Solarisbank (Germany): Successful €190 million Series D funding round led by Decisive Capital Management (July 2021)

Revolut (UK): Successful US$800 million Series E funding round led by SoftBank Vision Fund II and Tiger Global (July 2021)

Railsbank (UK): Successful US$70 million Series B funding round led by Anthos Capital (July 2021)

Lunar (Denmark): Successful €210 million Series D funding round led by Kinnevik, Tencent and Heartland (July 2021)

FairMoney (Nigeria): Successful US$42 million Series B funding round led by Tiger Global Management (July 2021)

Here cometh Big Tech

FSB says that the COVID-19 pandemic has enabled Big Tech firms like Google, Amazon and Apple to widen their footprint in financial services. (Finextra, March 2022)

HCL Technologies (Digital banking consulting): Acquisition of Confinale (May 2022)

Apple (Credit scoring): Acquisition of Credit Kudos (March 2022)

Facebook (Digital wallet): Launch of Novi (October 2021)

Activists target Europe's biggest & best

Citi snaps up Europe activism experts to brace for shareholder 'Trojan Horse'. (Financial News, April 2022)

115 investors managing US$4.2 trillion in assets has called on 63 global banks, including HSBC and Deutsche Bank, to take more action to tackle climate change and biodiversity loss. (S&P Global, July 2021)

Barclays: Pressure from Extinction Rebellion and Money Rebellion calling for improved climate strategy (May 2022)

Standard Chartered: Pressure from Extinction Rebellion calling for improved climate strategy (May 2022)

Deutsche Bank: Pressure from Riebeck-Brauerei calling for no-confidence vote vis-à-vis CEO Christian Sewing (May 2022)

HSBC: Pressure from Ping An calling for focus on Asian operations (May 2022)

ING: Pressure from FossielVrij, Milieudefensie and BankTrack calling for improved climate strategy (April 2022)

Aareal Bank: Pressure from Teleios Capital Partners calling for resignation of Chairman Hermann Wagner (March 2022)

Credit Suisse: Pressure from City of Zurich, Swiss Post and Publica calling for reduction in fossil fuel financing (March 2022)

Monte dei Paschi: Pressure from Italy's Treasury calling for resignation of CEO Guido Bastianini (February 2022)

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: Asset management structure (PDF)

View full image: Asset management structure (PDF)

View full image: 3rd-party/Retained securitisation structure (not supported by HAPS) (PDF)

View full image: 3rd-party/Retained securitisation structure (not supported by HAPS) (PDF)

View full image: 3rd-party securitisation structure supported by HAPS (PDF)

View full image: 3rd-party securitisation structure supported by HAPS (PDF)