Climate change litigation in Africa: Current status and future developments

Climate change litigation is increasing steadily worldwide, although few cases have been filed yet in Africa.

By Mukund Dhar, Africa Interest Group Leader

Our seventh edition of Africa Focus focuses on the potential for transformative changes within Africa during a time of historic global transition—not just from a COVID-19 to post-COVID-19 world, but against the backdrop of the United Nations Climate Change Conference COP26 in Glasgow, Scotland.

Issues around balancing greenhouse gas emissions against the development and use of natural resources as Africa industrializes and seeks to overcome roadblocks and challenges to growth and climate change-related challenges and vulnerabilities against GDP growth and increasing prosperity will be seen increasingly across sectors, industries and geographies in Africa. These discussions are already defining the way in which governments, investors, lenders, communities and other stakeholders view opportunities and investments in Africa and will do so more directly and more frequently in the coming years.

What does this mean for the world of business? Litigation related to climate change, a now well-established trend in Europe and North America, seems to have reached Africa, too. In "Climate change litigation in Africa: Current status and future developments," we outline signature cases and examine climate-related matters that might trigger challenges and disputes across Africa.

Equally, we all recognize that there are increasing investment opportunities when it comes to renewable energy. Seven of the ten sunniest countries in the world are in Africa, and wind power is no longer a novel feature in the increasingly sophisticated energy landscape in Africa. In "Renewable energy in Africa: Update in the era of climate change," we explore the significant opportunities for wind, geothermal and hydropower, too.

US foreign policy toward Africa has undergone significant shifts under the Biden administration. In "US government agencies focus on Africa," on the continent and their focus and how that ties in with both energy transition and renewable energy. In "Debt: Outlook for Africa brightens after challenging first half to the year," we discuss recent successful loan and bond issuances by African borrowers, investor resilience and lender interest in high-quality credits throughout the region.

Africa is experiencing a boom in M&A. In "M&A transaction terms: Comparing Africa to Europe," we contrast terms that typically apply to African M&A transactions, with those in Europe. And "African M&A stages a comeback" explores how African transactions appear to be highlighting a renewed sense of confidence among dealmakers. Acquisition and divestment strategies in Africa have become highly sophisticated. As a case study, "Acquisition financing in an era of energy transition" describes the January 2021 sale of a 45 percent stake in Nigerian Oil Mining Lease 17 (OML 17) and related infrastructure assets, using an innovative, first-of-its-kind hybrid financing structure.

Finally, "Southern Africa's PGMs are on the rise" explains how platinum group metals (PGMs) are increasing in southern Africa mining, on the back of demand for net-zero and the green economy.

Climate change litigation is increasing steadily worldwide, although few cases have been filed yet in Africa.

Africa offers vast potential for renewable energy deployment and investments.

Significant differences exist between terms that typically apply in M&A transactions in Africa and Europe.

H1 2021 dealmaking within the continent appears to be turning a corner.

Africa is a priority for several Biden administration agencies working in development finance.

Lender caution following Zambia's debt repayment default in 2020 has weighed on African debt issuance, but successful raisings by high profile borrowers show that investor appetite remains resilient.

An innovative, first-of-its-kind hybrid acquisition financing in Nigeria.

PGMs are helping Southern African mining remain relevant and contributing to a global clean and green transition.

An innovative, first-of-its-kind hybrid acquisition financing in Nigeria*

Sam Nwanze and Nnamdi Azubuike of HeirsHoldings Oil & Gas Limited, Ade Adeola and Dapo Akinpelu of Standard Chartered Bank, and Chike Obianwu and Yemisi Awonuga of Templars contributed to this article.

Over the past decade, international oil majors have been pivoting their investment strategy to offshore assets and divesting their stakes in onshore assets in West Africa. This process has been accelerated by the need of the majors to refocus on their gas-rich assets as part of a portfolio optimization process linked to energy transition.

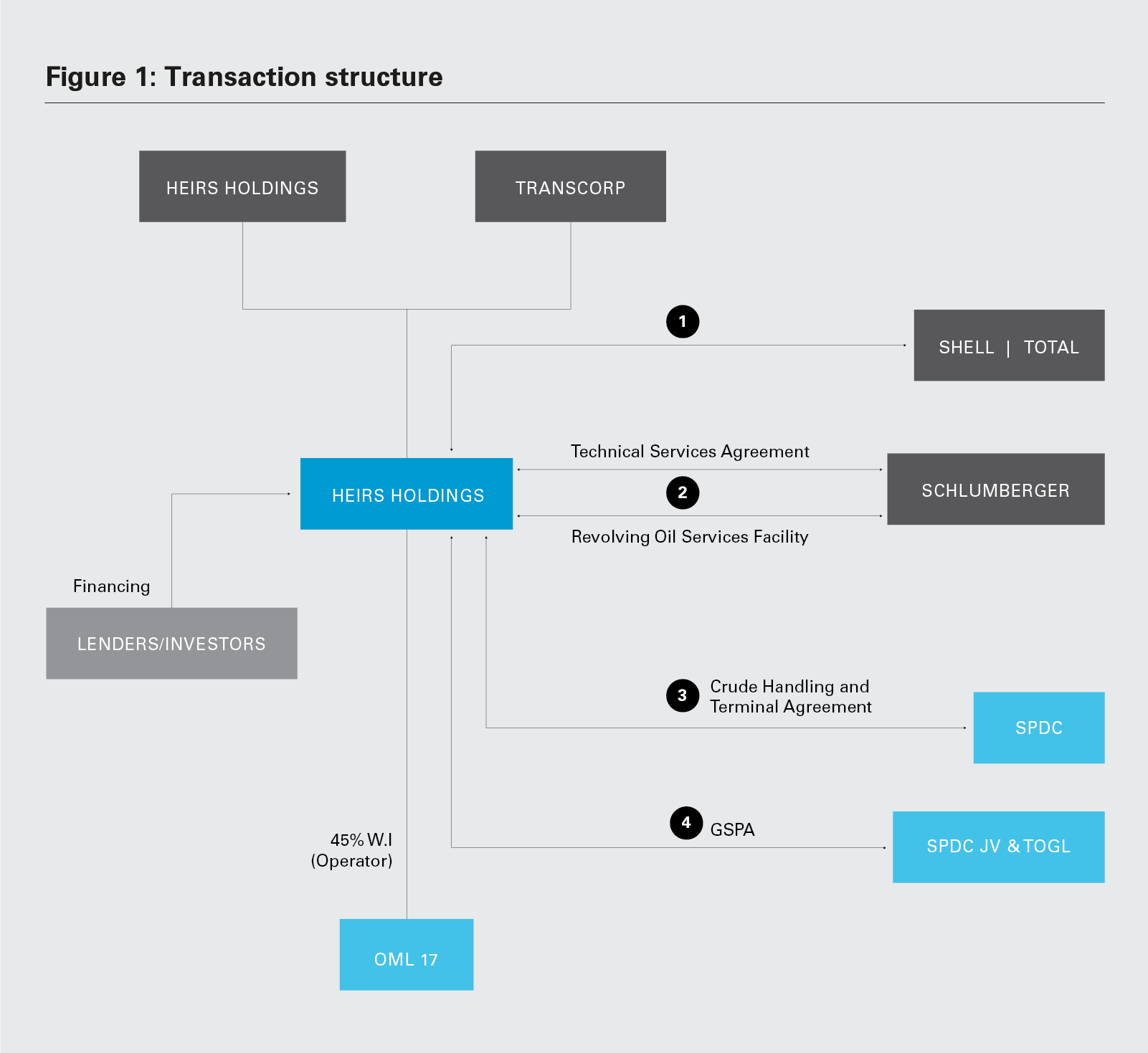

In January 2021, Shell Petroleum Development Company of Nigeria Ltd., Total E&P Nigeria Ltd. and ENI sold a 45 percent stake in Nigerian Oil Mining Lease 17 (OML 17) and related infrastructure assets to Heirs Holdings, a related company of Heirs Holdings Limited and Transnational Corporation of Nigeria Plc. The deal is notable for the extensive cast of players involved on the financing side including international and local banks, multilateral financing institutions and asset managers, as well as technical partners and crude offtakers.

OML 17 is located near Port Harcourt, Nigeria, and features 15 oil & gas fields, six of which are currently producing. OML 17 is in one of the most prolific oil & gas field clusters in Nigeria, and has the potential to double production in the short to medium term through STOGs and workovers. OML 17 was first discovered in the 1960s and, at its peak in the 1970s, production of 120,000 barrels of oil-equivalent (boe) was being achieved—current production is equivalent to 27,000 boe per day. OML 17 is estimated to have proven and probable reserves (2P reserves) of c.1.2 billion boe (NNS), with potential exploration upside of one billion boe. OML 17 is supported by a comprehensive infrastructure network including an installed liquid processing capacity of 240 kbpd, six flow stations and two gas processing plants with c.240 mbpd capacity (Obigbo North & Agbada gas plants) supplying energy to the industries and power plants in Southern Nigeria.

As part of the acquisition, Heirs Holdings has been granted sole operatorship of OML 17. This is a resounding endorsement of the company's operational plans, as well as its management team, strategic partners and service providers, including Schlumberger, and is a critical element in Heirs Holdings' stated intention to quickly ramp up production.

Set out below is an overview of the parties to the transaction and the key commercial contracts that have been put in place.

Heirs Holdings has negotiated agreements with the sellers (Shell/Total/ENI), Schlumberger and other counterparties to create a structure that both maximizes performance and reduces risk for all parties.

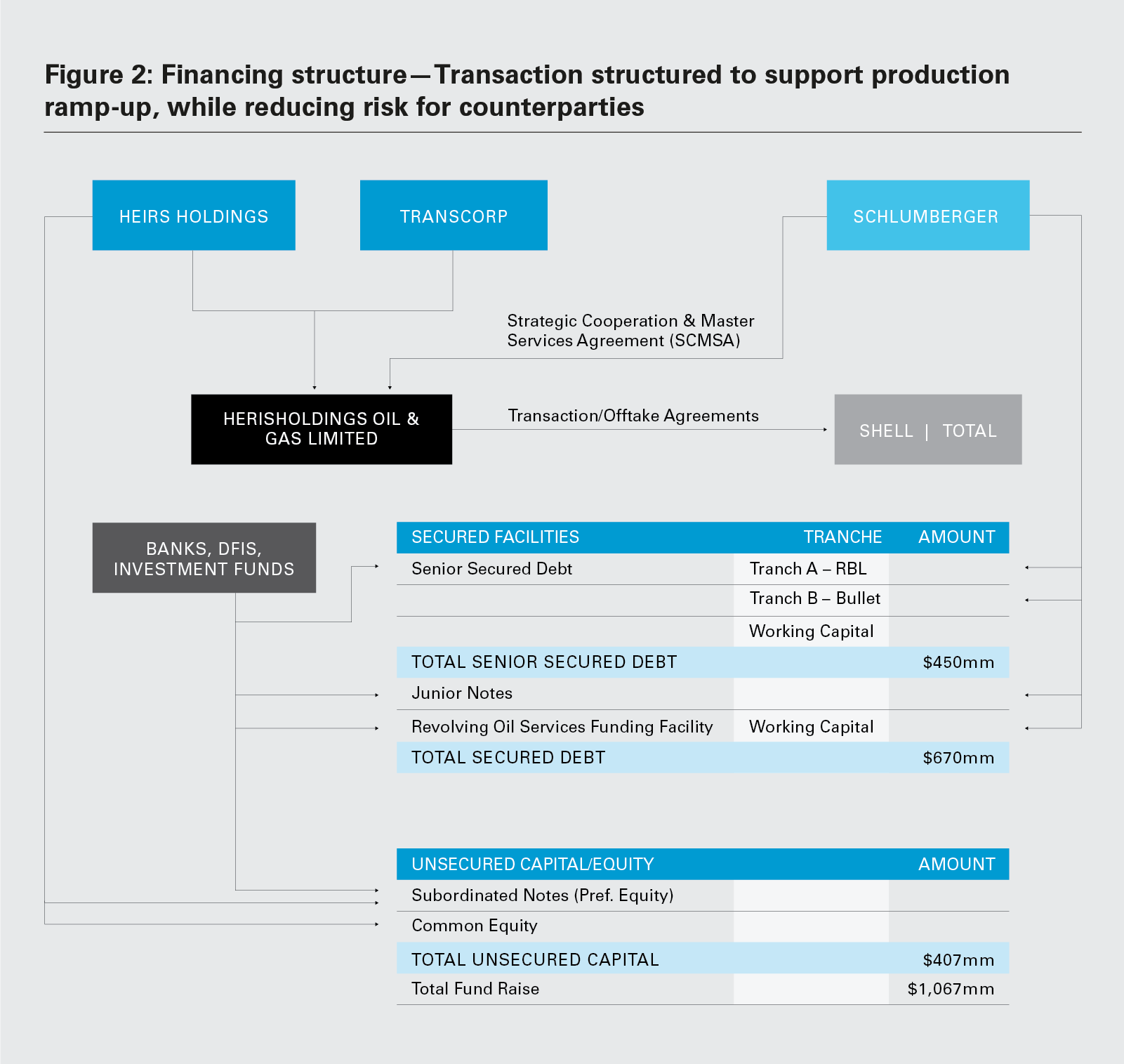

With more than US$1 billion in financing raised, this acquisition represents the largest M&A transaction in Nigeria since 2014. The financing for the acquisition of OML 17 utilizes a highly innovative hybrid structure and comprised the following:

Among other key features, the structure enables Heirs Holdings to increase its lender's commitments across the entire capital structure from time to time, subject to satisfying certain conditions. An illustrative overview of the financing structure is set out below.

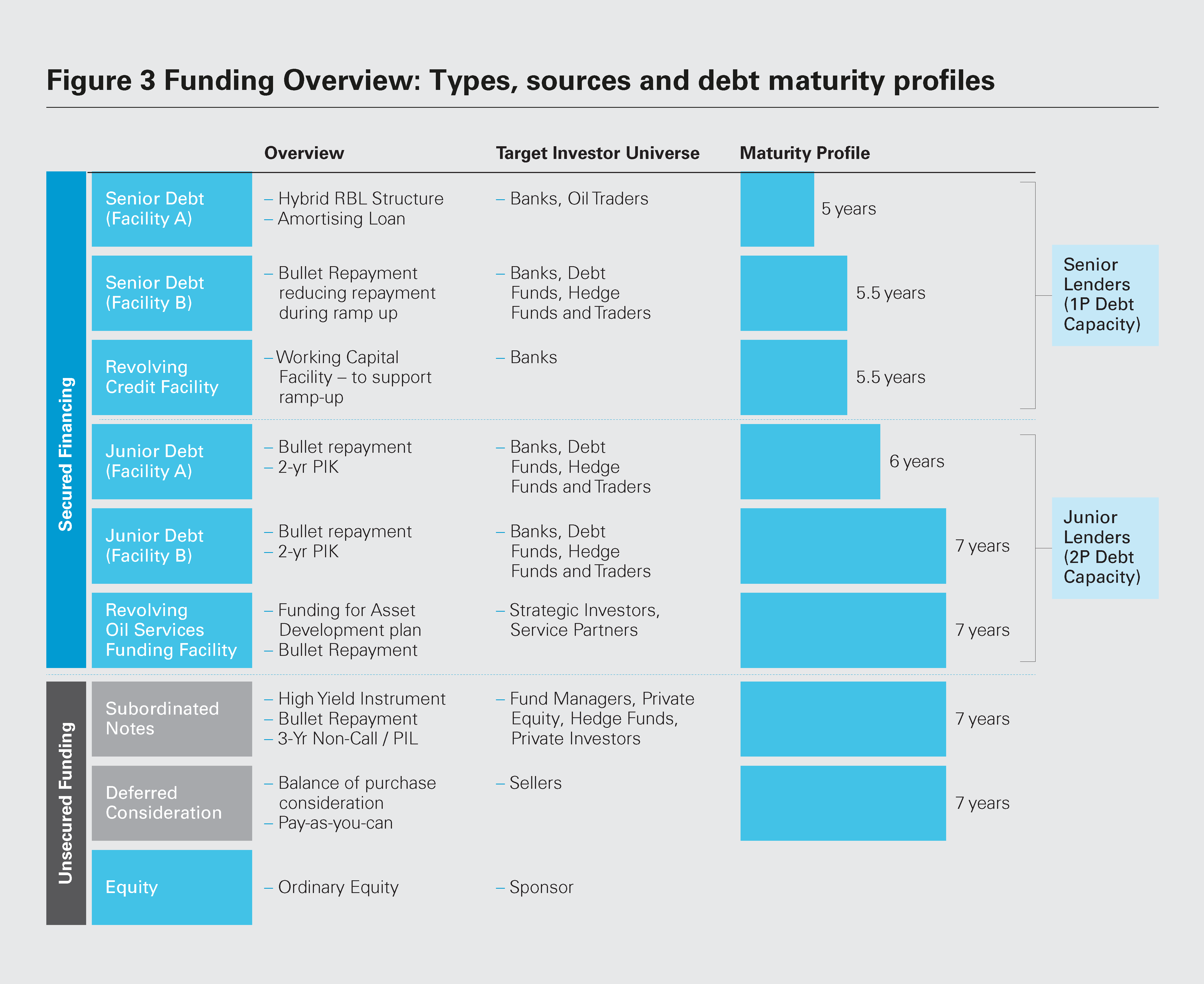

The senior debt comprises three facilities (or tranches) secured on a pari-passu basis. Tranche A is a five-year, US$300 million amortizing term facility, and tranche B is a 5.5-year, US$50 million facility with a bullet payment at maturity. In addition, there is a US$100 million RCF with a two-year tenor that can be renewed subject to mutual agreement between TNOG and the lenders. The senior debt capacity is calculated on a “stretched” NPV basis, using a six-year tenor which extends six months beyond the maturity of tranche B. Tranche B was designed to attract a specific investor class—non-bank financial Institutions such as asset managers and hedge funds—that are comfortable taking refinancing risk.

Tranche A, in comparison, is a traditional reserves-based loan (RBL) facility, whose lender base comprises banks that are typically active in the RBL market (such as Standard Chartered Bank, ABSA and African Import Export Bank) and Nigerian banks that are familiar with the domestic oil & gas sector. The repayment of tranche A will be prioritized in relation to tranche B; mandatory prepayments and senior cash sweeps will be allocated to tranche A on a 100 percent basis until this tranche is fully repaid, after which such prepayments will apply to tranche B.

In addition to other accordions set out in the senior facility, there is also an uncommitted facility made available via an accordion of up to US$300 million. The purpose of this accordion is to prepay the junior debt on a cashless basis and to fund capital expenditures (in this order of priority). This accordion will be in place throughout the five-year tenor of tranche A. Please see further below a more detailed discussion on the cashless redemption mechanism.

The senior facility includes a principal repayment grace period that enables Heirs Holdings to spend the initial months after closing the acquisition deploying its resources solely toward ramping up production. The grace period mechanism is an important point of distinction from a traditional RBL and was a key element of this financing.

The RCF offers Heirs Holdings the flexibility to use the proceeds of disbursements under this facility to fund the acquisition and for general working capital purposes.

The SFA has been structured to enable Heirs Holdings to incur additional indebtedness through a variety of means. In addition to the cashless redemption accordion, referenced above, the SFA provides for a petroleum asset accordion, which enables Heirs Holdings to request an increase in the commitments, with existing facility lenders having a right of first refusal.

The right to exercise the accordion is subject to a number of conditions, including:

In addition to the petroleum asset accordion, Heirs Holdings is permitted, after the first TLA principal repayment date, to incur additional indebtedness from third-party senior secured lenders. The proceeds of such third-party indebtedness are required to be used for acquiring new oil & gas assets.

Incurring additional indebtedness in such circumstances is subject to satisfaction of a number of conditions, including:

The benefit of the above arrangement from the Heirs Holdings perspective is that it can offer senior secured security to new prospective lenders, making this facility attractive to potential lenders and broadening the scope of potentially interested parties. From the existing senior lenders' perspective, the benefit of this arrangement is that the existing senior lenders will have the benefit of security over the new assets acquired, and the new senior lenders coming into the financing will have recourse only to the newly acquired assets. As such, there is no dilution in the value of the pre-existing security from the perspective of the existing lenders.

The SFA also provides for a junior redemption accordion. The junior redemption accordion is an accordion that can be utilized to convert amounts outstanding under the junior facility to senior debt. Upon exercise of this accordion, amounts outstanding under the JFA are deemed to have been incurred as new senior loans; in effect, the relevant junior lenders become senior lenders with respect to the converted amounts.

The SFA also includes a requirement that Heirs Holdings take out hedging in accordance with a pre-agreed hedging policy and with a pre-agreed criteria of hedging counterparties. Heirs Holdings is required to hedge a minimum amount of its quarterly production against oil price fluctuations for the first few years of operations. This insulates senior lenders against adverse oil price changes and offers Heirs Holdings stability in its forecast revenues, which is a critical requirement in a borrowing-based RBL facility.

The junior debt comprises two tranches—A and B—of US$100 million and US$70 million, respectively. The tenor of junior facility A is six years, and the junior facility B has a seven-year tenor. Both facilities have a bullet repayment at maturity and are subordinated to the senior debt both in terms of cash waterfall payments and security. The junior debt is expected to be refinanced within 24 to 36 months of closing by way of exercise of the senior debt accordion that prioritizes prepayment and cancellation of the junior debt by way of transfer of those commitments to the senior facility.

The junior facility agreement (JFA) was targeted at strategic industry investors. The JFA is repaid as a bullet, and has a longer maturity than the facilities provided under the SFA. When the junior tranche was first explained to potential lenders during the market sounding process, it was described specifically as not a “true” junior, but as a facility more akin to a "stretched senior" instrument. The junior facility incorporates an accordion, (this accordion dovetails with the junior redemption accordion set out in the SFA) and provides that upon the exercise of the accordion, the amount requested by Heirs Holdings to be converted shall be deemed to have been repaid on a cashless basis and converted to senior debt. This accordion can be exercised if specified economic and technical conditions are met. To ensure that Heirs Holdings does not incur additional indebtedness under the SFA without first converting any outstanding amounts under the junior, the SFA includes a requirement that prior to incurring additional indebtedness at the senior level, a specified minimum amount of the amounts outstanding under the junior facility shall have first been converted to senior.

Given that junior lenders are subordinated to senior lenders, the JFA carries a margin uplift relative to the SFA. Consistent with its ranking, the JFA offers greater flexibility to the obligors relative to the SFA in terms of applicable covenants and representations. Similarly, as the JFA is not a borrowing base facility, it does not incorporate the same periodic economic and technical assumption update and projection approval provisions found in the SFA.

Both the junior facility A and junior facility B are repaid as bullets, but the junior facility A is required to be converted to senior prior to the JLB, and the junior facility A is converted to senior solely as TLA debt, while the junior facility B is converted to senior solely as senior facility B debt. This provision helped to ensure as broad a market as possible for the junior facility A and junior facility B, and to create an essential point of difference.

Schlumberger/Hybrid Capital have arranged a consortium of investors and banks to provide a US$50 million revolving oil services funding facility (ROSFF) that is “evergreen” and subordinated to senior and junior debt. The facility is priced in line with the junior debt and includes both a cash and PIK interest component for the first two years and full cash interest thereafter. Utilizations under the ROSFF can be applied toward the payment of project costs for capex and opex to support the accelerated ramp-up or expanded production.

The issuance of structured notes and petroleum economic participation units (PEPs) was a key element of the financing, as a synthetic equity instrument. The structured notes are a hybrid debt instrument with debt and equity features designed to give higher risk-taking investors such as equity investors, and asset managers risk-reward exposure to the transaction while being senior to common equity. A number of the private equity and debt funds who committed to the financing at the senior TLB level also expressed an interest in both a fixed-rate instrument as well as an instrument that could offer equity-level return, on a highly subordinated basis. The structured notes and PEPs evolved as a means of satisfying this request from investors.

The structured notes are unsecured subordinated debt securities with a fixed coupon and cleared through the clearing systems. Holders are entitled to receive interest payments only after the expiry of a cash interest grace period. The structured notes require the issuer to meet a specified debt-to-equity ratio prior to the incurrence of additional secured indebtedness. The structured notes are designed to have a fixed dividend component as well as a detachable oil royalty component—both deeply subordinated and payable only upon sufficient cash—that effectively solves for a target IRR to the investor, under McDaniel 2P/ Management Base Cases. The structured notes accrue cumulative dividends of 10 percent (delayed payment starting from 36 months), with a common equity dividend stopper feature—this enables Heirs Holdings to defer dividends until all cumulative deferred notes dividends have been paid. The structured notes are mandatorily redeemable seven years after the closing date.

The PEPs are an equity-like instrument and give holders exposure to the amount of oil being produced and sold by the issuer. The PEPs have a fixed term of eight years (debt service on the PEPs begins three years after closing of the acquisition). The royalty stream under the PEPs will survive any redemption of the structured notes and produces an additional yield to the detachable royalty instrument. The amount payable will move up or down depending on the liquids production rate and realized oil export prices.

In the initial stages, there were extensive discussions about how best to approach the drafting of the documents, and what format the documentation should take. While lenders under the senior and junior facilities were represented by separate counsel, it was important that the various debt facility agreements worked together, and were entered into on terms consistent with the lenders' relative seniority. For example, if a matter is prohibited at the senior and junior level but a waiver or exemption to such prohibition has been approved by the senior lenders, then junior or ROSF lender consent should not also be required (subject to a limited subset of amendments that would require the approval of all secured creditors).

It was commercially agreed that White & Case, as sponsor counsel, should have primary responsibility for drafting the various facility agreements and note instruments, given that the firm had visibility across the entire structure. The approach to drafting adopted was to secure substantive agreement on the SFA, and then to begin negotiations with the junior lenders using the SFA as a base document, excepting provisions that are not appropriate for the junior lenders. The same process was then undertaken for the ROSF. Given the approach to drafting, it was important that a degree of confidentiality was maintained between the lenders under the various tranches of capital.

In keeping with the nature of the acquisition, the closing was carefully and extensively structured by the Standard Chartered and Heirs Holdings teams.

Following financial close, proceeds of disbursements under the SFA and JFA, and proceeds of note issuances earmarked for such purposes, are required to be funded into an escrow account. Amounts standing to the credit of the escrow account can be released from escrow only after specified conditions set out in the SFA have been satisfied. If the conditions to release are not satisfied by a specified longstop date, an automatic unwind mechanism kicks in to return monies to the lenders.

Given the diversity of the lenders, funding at financial close took place in a multi-phase manner. Some lenders were required to provide evidence of funding by delivering acquisition letters of credit at financial close, other lenders were cash funding at financial close, and others were required to cash fund into the escrow accounts only at the latest point permitted under the share purchase agreement.

The successful financing of the OML 17 acquisition demonstrates the confidence Nigerian investors and international financiers have in the market, and illustrates the broad appeal of the innovative financing structure. We have set out below some suggested key takeaways from the financing.

Further, NNPC/NGC is currently being advised by SCB in connection with the development of the Ajaokuta-Kaduna-Kano Project (AKK) —a pipeline project that aims to reduce gas flaring and establish a guaranteed gas supply network between the south and the north of the country. The AKK project is proposed to be completed within 24 months of the launching of the construction, in July 2020. Gas-fired power plant projects with c.3.6 GW capacity and gas-dependent industries (in many cases spurred by existing industry players) are under development across the AKK pipeline route, due to the increased access to gas.

On a broader macro level, we think that gas processing plants and other related projects are a sector ripe for additional investment and one where there is a real opportunity and need for private sector investment in Africa both from commercial banks and development finance institutions. Extensive studies have been undertaken with regards to the negative externalities caused by gas flaring and biomass energy sources, and the next stage in the evolution of the energy picture for Africa will be a move toward cleaner, more diversified and more sustainable energy sources, and gas is a key element of this.

*Reprinted with permission from Project Finance International

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP

View full image: Figure 1: Transaction structure (PDF)

View full image: Figure 1: Transaction structure (PDF)

View full image: Financing structure (PDF)

View full image: Financing structure (PDF)

View full image: Funding Overview (PDF)

View full image: Funding Overview (PDF)