Latin American arbitration in transition

A disruptive era portends a new wave of disputes using well-established frameworks for commercial and investment arbitration

By Carlos Viana, Latin America Interest Group Leader and Editor of Latin America Focus

We are delighted to introduce the first edition of Latin America Focus, a publication produced by the Latin America Interest Group at White & Case. Our intent with this publication is to provide market insights from our practices and proprietary research that could be valuable to senior decision-makers who have an interest in the region.

COVID-19 hit Latin America's economies more heavily than it hit any other region around the world. The region's economies contracted by nearly 7 percent in 2020, compared to a global average of only 3 percent. Current projections indicate a healthy recovery through the end of 2021, perhaps by as much as 6.9 percent according to S&P Global,1 and thereafter steady growth of about 2.5 percent per annum.

As we look forward to 2022 – 2023, Latin America, in very significant part, will likely continue to face the ebbs and flows of populism, resource nationalism and weak institutions that seem to take turns at flooding some of the countries in the region from time to time. Yet, we also see Latin America propelled away from the COVID-19 swamp by the powerful global engines of economic, social and technological evolution that will push heavy foreign investment into the region: unprecedented global liquidity and the search for yields in emerging markets, the energy transition, the commitments to mitigate climate change by global natural resources and energy companies, and the technology-driven push to digitize and automate the increasingly global world economy. We saw these global drivers, and foreign investors' net-net belief that Latin America will resurge in the medium term, supporting our cross-border business in the region through a 2020 – 2021 period that we expected at the outset could be cataclysmic for foreign investment in view of the region's endemic challenges.

In this edition of Latin America Focus, partners in our Latin America Interest Group have written articles based on their personal experiences in the trenches and market research that go to the very heart of both the latest sequel in the Latin American saga of transitions, and the current global forces of growth, the interplay of which will likely shape what is to come in post-COVID-19 Latin America.

Times of transition are frequently associated with greater incidences of disputes, notably investor-state disputes, but also commercial disputes, especially in times of supply-chain disruption. In "Latin American arbitration in transition," our team outlines the past and present of commercial arbitration in Latin America, and its prospects for the future.

Latin America has experienced many sovereign debt defaults over the past century. The most recent installment of these usually long-brewing crises played out as COVID-19 partly disabled the region, involving Ecuador, Argentina, Belize and Suriname. Meanwhile, Venezuela continues mired in default for more than three years as of the time of publication. In the article "Sovereign debt restructurings in Latin America: A new chapter," our team explores some of the lessons learned and innovations employed in these recent sovereign debt restructuring exercises, providing insights into the implications for the future of sovereign and sub-sovereign international finance and, more broadly, cross-border restructurings, in the region.

With the COP26 conference being held in Glasgow in November 2021 and concerns about climate change at an all-time high, it is unsurprising that environmental, social and governance (ESG) trends are a recurring sub-theme through several of the articles in this inaugural edition of Latin America Focus. In "Sustainable finance in Latin America," our team focuses directly on green, social and sustainability-linked (GSS) bonds. This article also covers other kinds of sustainable finance, and international environmental agreements in this area to which Latin American countries are signatories.

Our world is being transformed by what the World Economic Forum calls the 4th Industrial Revolution, and Latin America is no exception. Over the next few years, the region is expected to experience faster growth in interconnection bandwidth capacity than any other region in the world. This is especially important for Latin America given the role that connectivity and digital capacity play in driving inclusive economic growth and prosperity. In "Bridging Latin America's digital divide," our team takes a detailed look at investments in digital infrastructure across the region. We focus especially on mobile networks (including 5G), data centers and sub-sea cables, exploring also how these investments are being (and might be) funded.

Latin American equity markets proved remarkably resilient to COVID-19, in terms both of growth in their major indexes and in new initial public offerings (IPOs), and other stock and rights issuances. Brazil, in particular, saw a large number of new publicly listed companies emerge in 2020 – 2021. "Equity capital markets in Latin America" provides a current overview of the state of equity capital markets in Latin America, emphasizing key growth opportunities.

Finally, the first half of 2020 saw a sharp contraction in M&A in Latin America, but deal flow has rebounded strongly in 2021. In "M&A in post-COVID-19 Latin America," our team explores some of the factors that international investors need to take into account when investing in the region's growing markets in view of the current environment. Data drawn from White & Case's global M&A Explorer tool is used to show current trends among various cross-sections of deals.

We do hope that you enjoy reading these insights, and find them valuable. Please do not hesitate to let me know if there are any topics that you would like us to cover in future editions.

A disruptive era portends a new wave of disputes using well-established frameworks for commercial and investment arbitration

Sovereign debt restructuring solutions developed in Latin America during 2020 and 2021 create a new paradigm for sovereign debt restructurings in the region and globally

GSS bonds and other forms of sustainable finance have become a mainstream feature of Latin American debt capital markets

COVID-19 has created strong incentives for investment in digital infrastructure in Latin America, especially in 5G, private networks, data centers and fiberoptic cables

Strong pandemic-era performance and a look around the corner

Established trends driving M&A globally are also reflected in Latin American deal flow

GSS bonds and other forms of sustainable finance have become a mainstream feature of Latin American debt capital markets

Stay current on your favorite topics

Sustainability issues in Latin America have long been closely linked to finance, but never more so than today. Latin America's tropical forests are among the most biodiverse ecosystems on earth—and highly vulnerable to the increasingly significant effects of climate change. The region's economies are heavily reliant on extractive industries and other sectors that depend on those natural resources and ecosystems. This has the potential to cause tensions between short-term profit priorities and longer-term sustainability goals. It is therefore unsurprising that environmental, social and governance (ESG) considerations have become more important in relevant sectors like mining, oil & gas, power, forestry, agriculture, fisheries and industry in general.

This article focuses on the state of sustainable finance in Latin America (including green, social, sustainable and sustainability-linked instruments) and the opportunities to use sustainable finance to address development priorities in the region.

Latin America’s tropical forests are among the most biodiverse ecosystems on earth—and highly vulnerable to the increasingly significant effects of climate change.

The European Commission defines sustainable finance as: "the process of taking ESG considerations into account when making investment decisions in the financial sector, leading to more long-term investments in sustainable economic activities and projects."1 Since 2015, sustainability in the context of finance has come to be viewed largely in terms of the UN Sustainable Development Goals (SDGs)2 and the Paris Agreement commitments on climate change. Today, no industry or market exists that is insulated from the concern of shareholders, investors, lenders, employees, consumers or society-at-large when it comes to ESG-related performance or the risks and impacts of climate change. This increased concern has led to greater motivation for developing financing products to facilitate achieving the goals, protecting against the impacts or adapting to the changes, whether social, environmental or economic.

Mechanisms such as blended finance, ESG-linked loans, green or social bonds, ESG considerations in foreign direct investment (FDI) and even some aspects of equity capital markets and trade, demonstrate how the field of sustainable finance is as diverse as the issues it seeks to address.

Latin American countries are also well aware of the interdependencies between sustainability and economic development, trade and investment, all of which are the subject of numerous international and regional trade and investment agreements, including the United States-Mexico-Canada Trade Agreement (USMCA). Like its predecessor, the North American Free Trade Agreement (NAFTA), USMCA contains several environmental provisions and a side agreement on environmental and other sustainability safeguards.

Although not a direct form of funding, these CERs can be traded and sold, and used by industrialized countries to meet a part of their emission reduction targets under the Kyoto Protocol.

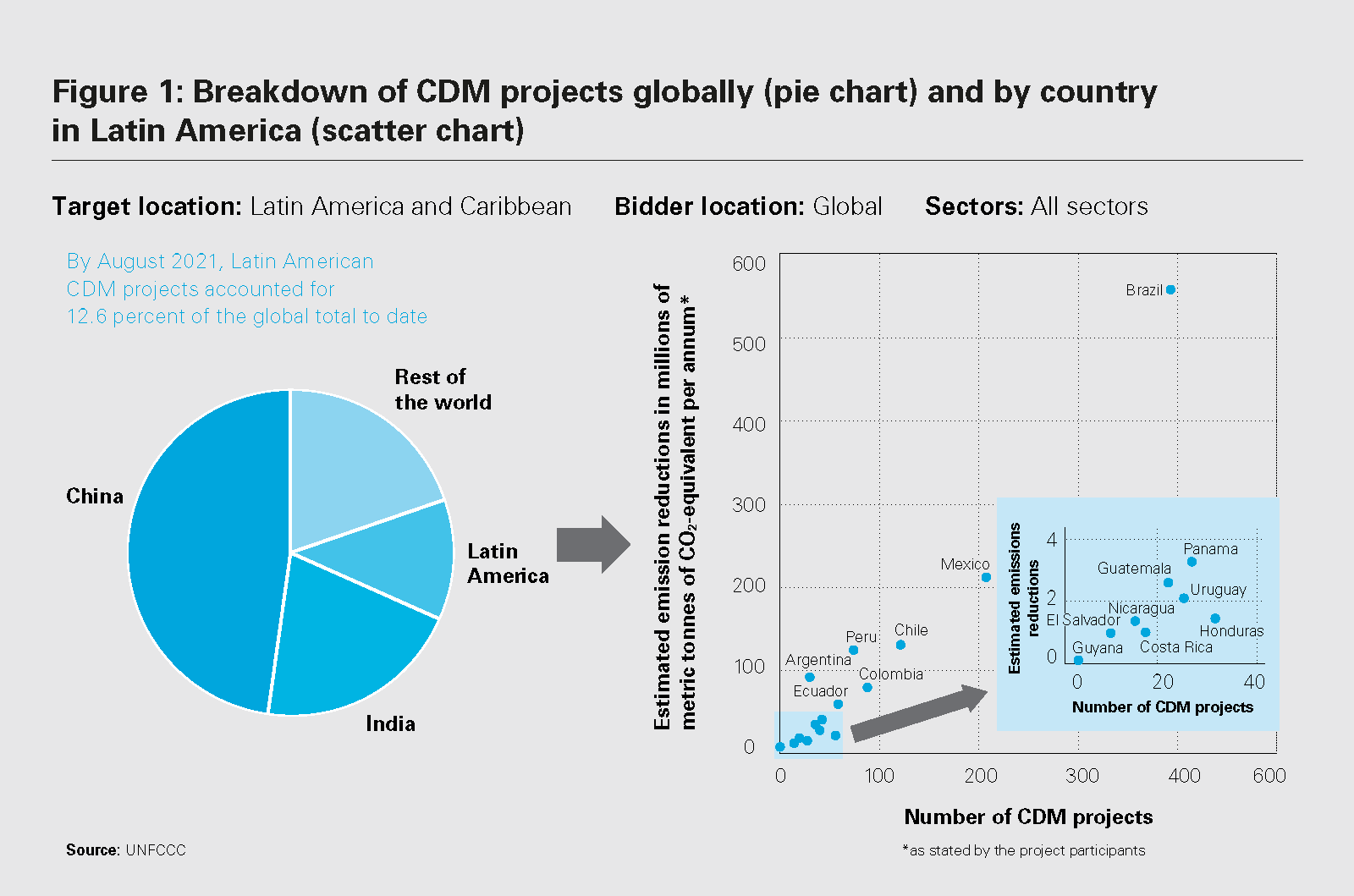

Under the Kyoto Protocol, which preceded the Paris Agreement by almost 20 years, Latin American countries were not considered major contributors to global greenhouse gas (GHG) emissions. They were therefore not subject to binding targets to reduce GHG emissions. Brazil, for example, was classified as a "carbon sink" due to the potential of the Amazon rainforest to sequester GHGs to reduce global warming. Under the Paris Agreement, on the other hand, all ratifying countries have been required to present their national targets, known as Nationally Determined Contributions (NDCs). Article 6 of the Paris Agreement establishes mechanisms that contribute to the mitigation of GHG emissions and support sustainable development3 including the Kyoto Protocol's clean development mechanism (CDM), which allows emission-reduction projects in developing countries to earn certified emission-reduction (CER) credits, each equivalent to one metric tonne of CO2. Although not a direct form of funding, these CERs can be traded and sold. Industrialized countries can and do use them to meet a part of their emission-reduction targets under the Kyoto Protocol. While China and India have accounted for the majority of CDM projects over the years, Latin American countries have also made extensive use of the CDM to create CERs.4

By the end of July 2021, 8,222 projects had been registered globally under the CDM, representing a reduction of just over 1 billion metric tonnes of CO2-equivalent GHG emissions. Latin American projects accounted for 12.6 percent of that reduction (see figure 1).

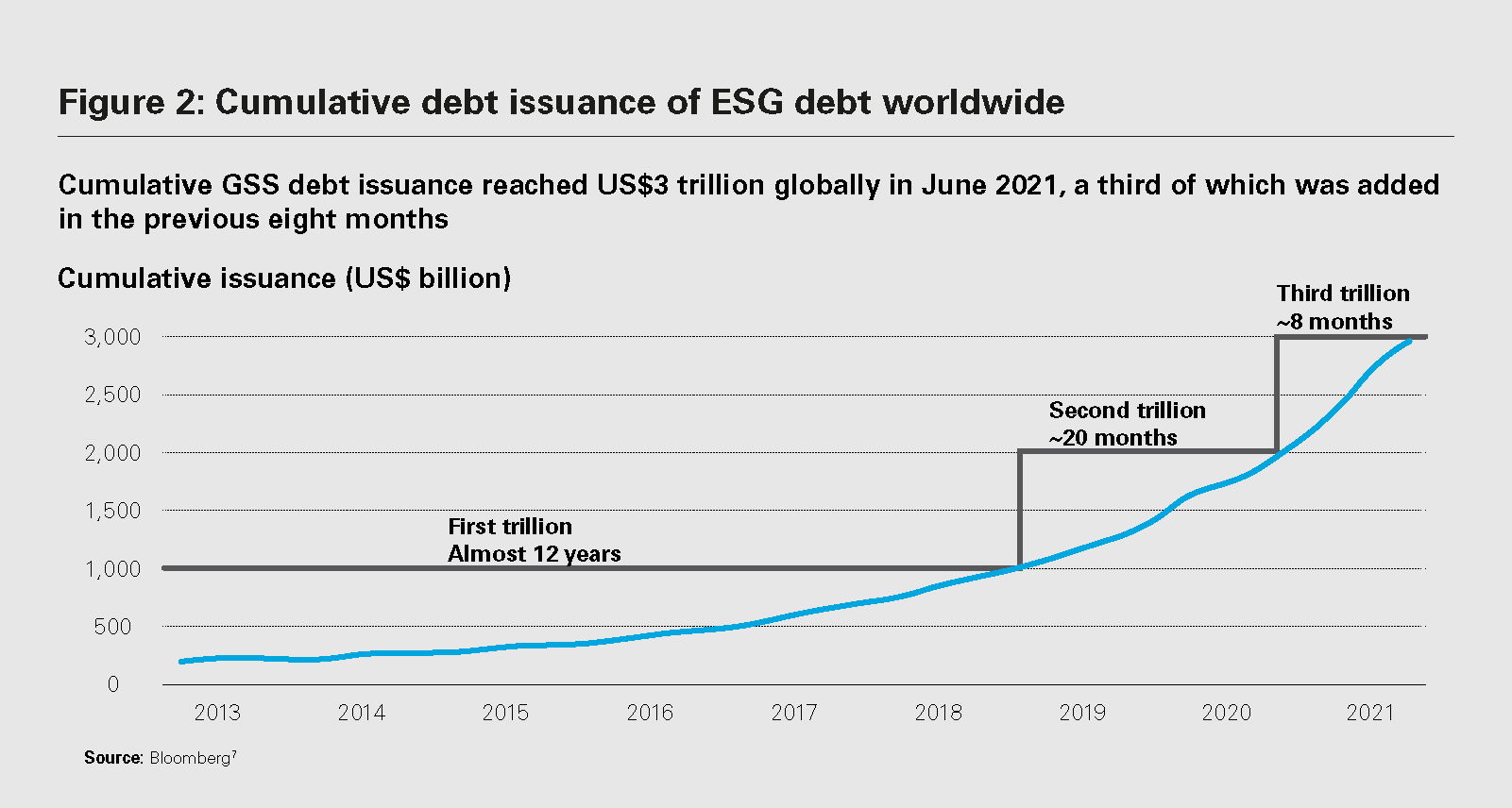

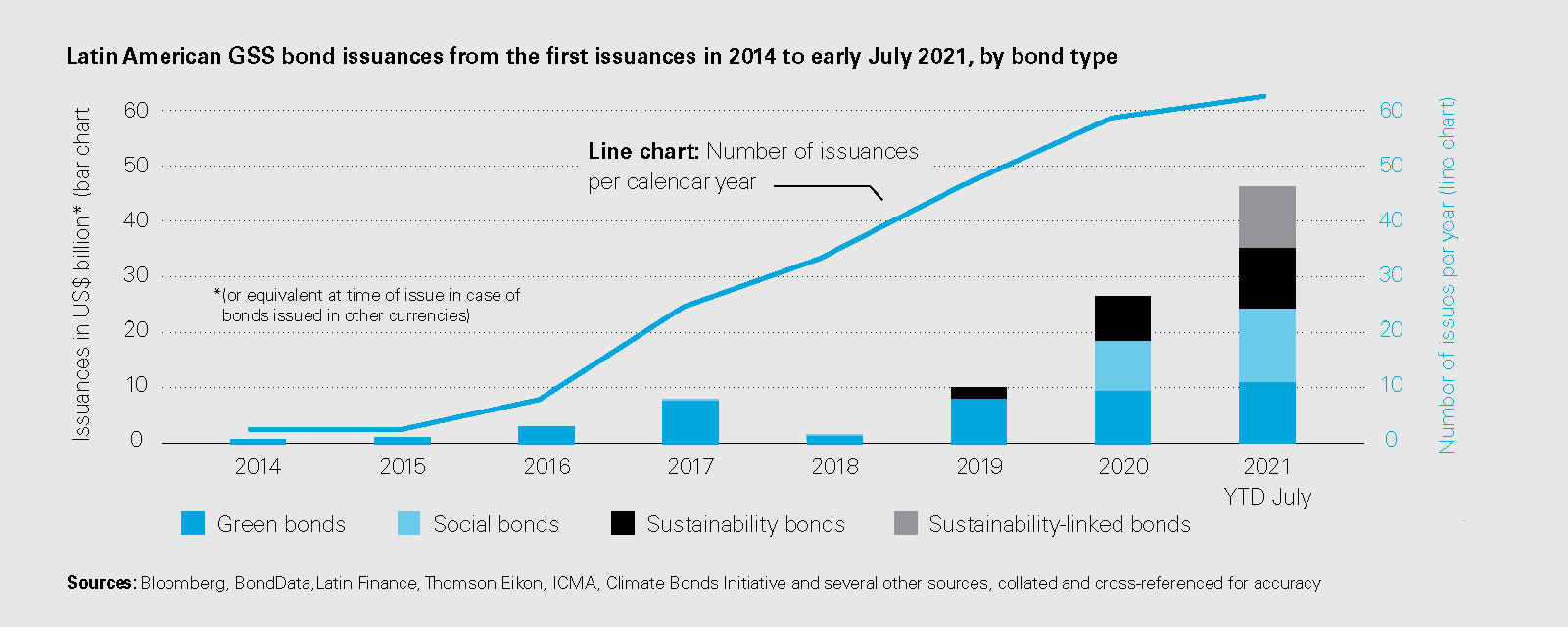

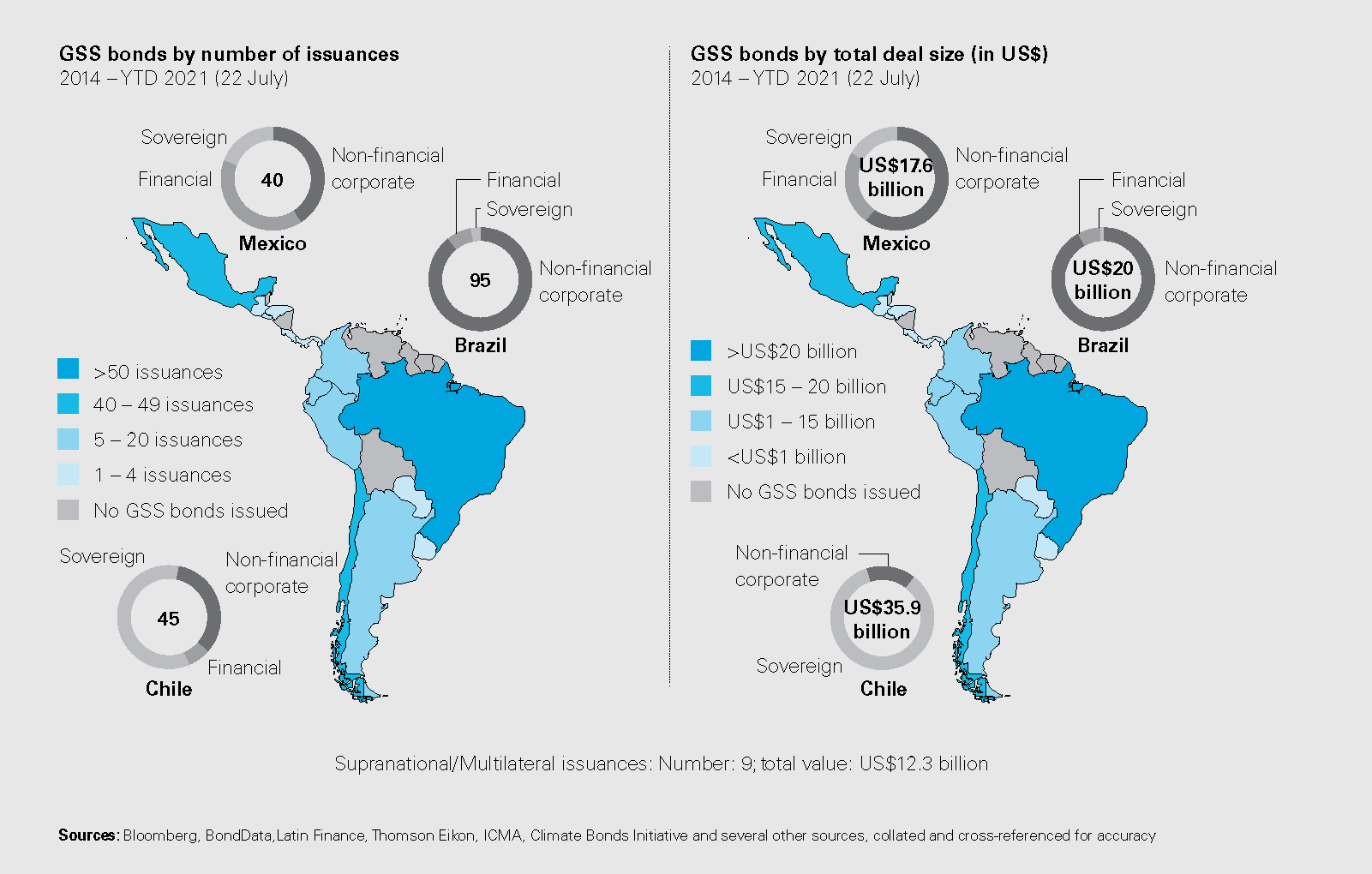

The first-ever green bond (labeled a "Climate Awareness Bond") was issued on July 4, 2007 by the European Investment Bank. Since then, across the world, total ESG debt including GSS bond issuances have reached US$3 trillion, with US$1 trillion being added in eight months during late 2020 and early 2021, alone5 (see figure 2). By comparison, the Organization for Economic Co-operation and Development (OECD) estimated in 2017 that annual green investment required to limit global warming to a two-degree rise will exceed US$4.3 trillion.6 By late July 2021, GSS issuances in Latin America had reached US$45 billion for the year—roughly 1.7 times the total GSS issuances for the region in 2020 (see figure 3). Clearly, GSS bonds are becoming a more important feature in Latin American finance.

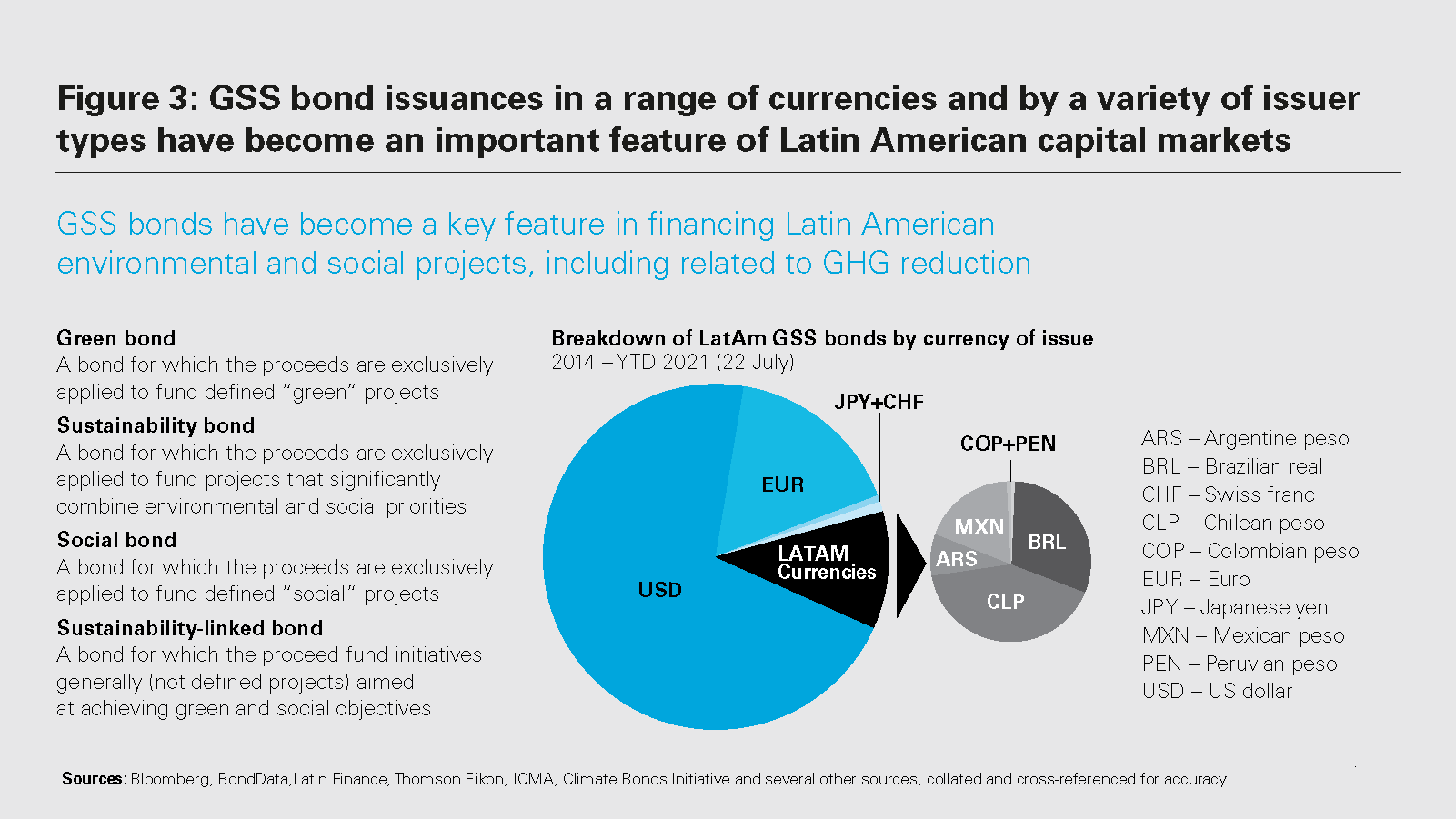

While green bonds are the most established and well developed of the ESG debt instruments, and they account for the lion's share of GSS bond issuances worldwide, sustainability-linked bonds (SLBs) are becoming increasingly popular as an alternative. Since the International Capital Market Association (ICMA) published principles for SLBs in mid-2020, they have become the fastest-growing kind of issuance in Latin America (see infographic in figure 3). The essential difference between green, social and sustainability bonds, and sustainability-linked bonds, is that the former are intended to fund specific ESG-related projects, while the latter are linked to achieving defined ESG performance objectives.

Latin American GSS bonds have been issued both in international and local capital markets, and in a variety of currencies. In 2020, for instance, Banco del Estado de Chile issued a social bond termed a "women's bond" denominated in Japanese yen, raising the equivalent of US$95 million to improve women entrepreneurs' access to financial and non-financial services in Chile and to support the economic empowerment of women in the country.8 The Chilean government has also issued sovereign GSS bonds denominated in euros. The most common denominations however are local Latin American currencies and the US dollar.

GSS issuance in Latin America is led by the private sector, with corporate issuers responsible for 62 percent of the total GSS issuances. Sovereign and supranational issuers represented 35 percent and 3 percent of the total GSS bond issuance, respectively. In terms of volume, the sovereign issuances have been far larger, and they account for 44 percent of the volume to date. This mix varies widely across Latin American countries, however. The private sector (especially forestry and paper companies) has been far more dominant in Brazil, for instance, than in Chile (see infographic in figure 3).

Energy has been the most funded sector, with half of Latin America's green proceeds dedicated to renewable energy projects (mainly solar and wind) excepting Chile, where transport ranks first. However, land use and industry, which are considerably under-funded globally, represent almost a quarter of the issuance in Latin America. In contrast, green buildings and water, which are both commonly funded globally, are among the least funded sectors in Latin America.

Similar to elsewhere in the world, Latin America's financial sector has also begun to promote green finance initiatives in recent years. Mexico's Central Bank and Colombia's financial system regulator are members of the global Network for Greening the Financial System. Mexico's Climate Financial Advisory Board joined the Financial Centers for Sustainability network, announcing plans to turn the country into a regional leader in green finance (although such comment was made prior to the current pandemic). Several private sector Latin American banks have issued GSS bonds, in order to use the proceeds to lend to customers to fund projects that are aligned with ESG objectives.

Investors have always been concerned with “greenwashing” but never more so than today, with the stakes being as high as they are.

How GSS and similar bonds should be certified and rated remains an evolving field. GSS bonds fund such a wide range of projects that a degree of flexibility is required, but this must be balanced with investor need for assurance that their investment really is going to contribute to achievement of the SDGs. While consensus exists generally about what constitutes a green bond or investment, external review processes and standards can vary widely. Two approaches appear to be gathering more momentum than others, however. The first is that of ICMA, which has published principles for green bonds, social bonds, sustainability bonds and sustainability-linked bonds. The second is that of the Climate Bonds Initiative, namely the Climate Bonds Standard and Certification Scheme. The certification process for the latter is conducted through clearly defined procedures, whereas the former relies on external verifiers applying their own methodologies.

A number of indices have also emerged, with varying criteria applying for inclusion. These include:

While third-party certification is important, concerns frequently arise about whether GSS bonds always end up being used for their stated purposes and have a meaningful impact on SDGs or mitigating climate change more generally. Investors have always been concerned with "greenwashing," but never more so than today, with concerns about climate change and other ESG issues being viewed with as much concern as they are. The value of assets under management by managers applying ESG data to investment decisions has risen sharply over the past decade, to US$38 trillion in 2020.10 Furthermore, what asset managers in Latin America might require in terms of ESG reporting differs sometimes from that required in the US, Europe and Asia-Pacific.

Perhaps as a result of the rapid development in GSS finance, ESG data in the market is emerging that is unstructured, opaque and non-standard in format. For this reason, some investors and asset managers are shifting from relying upon third-party certifiers to assembling their own data on the ESG credentials of the assets in which they choose to invest. A healthy market for raw ESG data has emerged as a result. Bloomberg, for instance, now supplies its customers with reported ESG data for almost 12,000 companies and more than 410,000 securities in more than 100 countries, covering more than 15 years of historical data.11 The newly launched Sustainable Fitch suite of ESG products also includes tools to help investors to evaluate the relative ESG credentials of financial instruments and entities.

When considered together with other transparency drivers, such as bank disclosure requirements for ESG risks, and also increasing regulatory requirements, it follows that entities using any source of sustainable finance would do well to ensure that their own ESG reporting is clear, unambiguous and comprehensive.

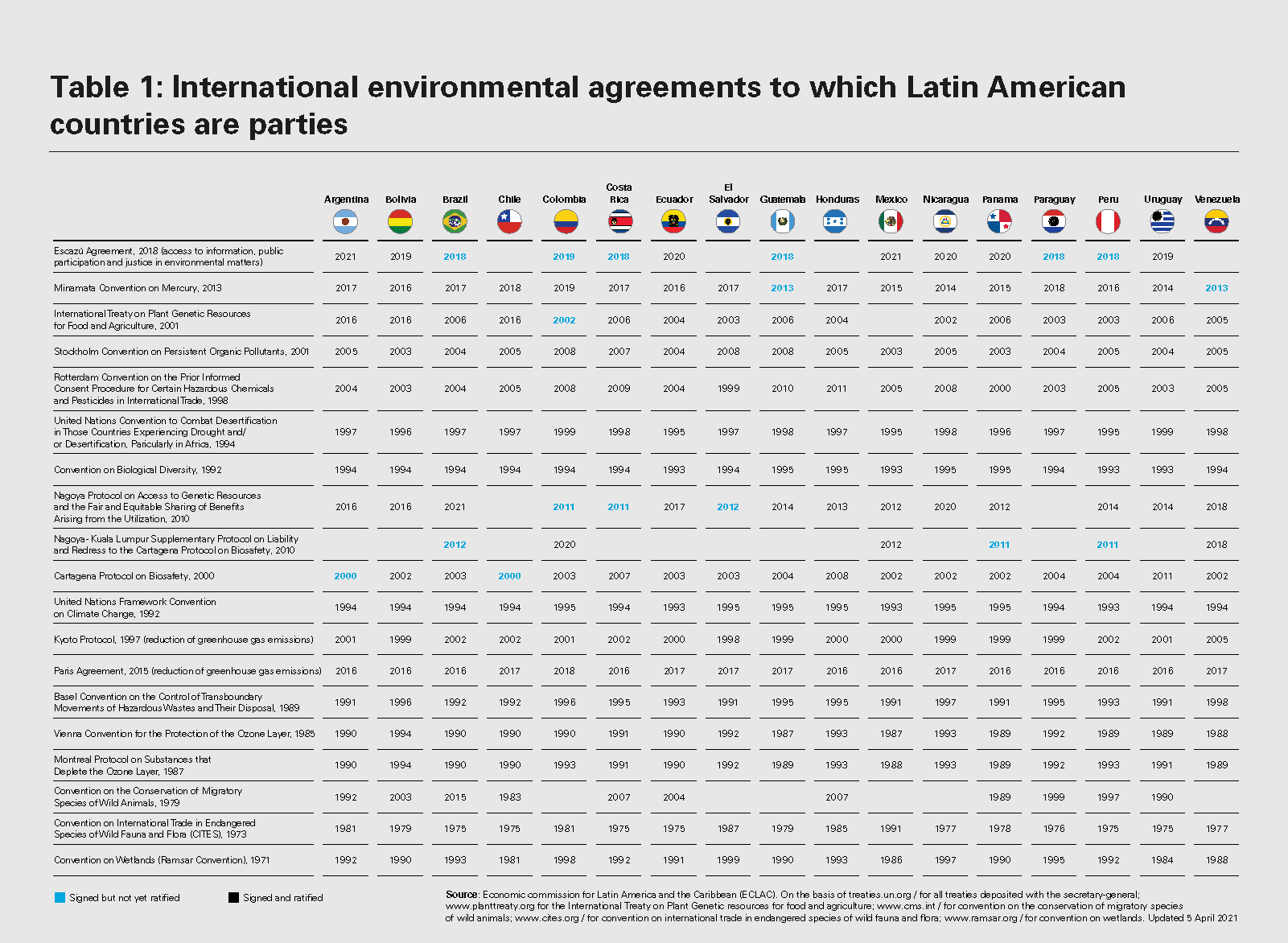

Latin American countries have collectively ratified roughly 20 international environmental agreements (table 1). Some of these create obligations on the part of developed nations to provide funding and other resources to developing nations including those in Latin America, to encourage sustainable economic development. In practice, however, such funding compromise has proved insufficient to fulfill its purpose, and additional resources have been sought through different mechanisms. In recent years, the ESG safeguards built into those mechanisms have become more common, and explicit.

As is usual in international law, ratifying states take steps necessary to ensure that their domestic legislation aligns with their obligations under these agreements and treaties, in some cases promulgating new law for this purpose. Regarding GSS bonds in particular, the following current and recent developments should be noted:

The Financial Superintendency of Colombia (SFC) became the first banking regulator in Latin America to publish a regulatory framework for green bonds, on September 7, 2020, incorporating international standards and including voluntary process guidelines that had been established by the International Capital Market Association, as well as taxonomies issued by the European Union and the Climate Bonds Initiative.

The local Bolsa Nacional de Valores has a green bond standard that follows the ICMA Green Bond Principles (GBPs) and applies to both private and public issues. The guidelines allow bonds that comply with ICMA or CBI principles to be considered as "green" in the local market. External reviews must be performed, by CBI accredited verifiers or others who can provide acceptable evidence of experience in environmental and sustainability assessment.

The Bolsa de Santiago opened a Green and Social Bond Market Segment, following collaboration with local non-governmental organizations (NGOs) in order to increase market transparency and prevent greenwashing. The exchange organized activities related to these instruments through a series of requirements stated in such Green and Social Bond Market Segment. The purpose of such framework is to simplify the issuance framework and make their authorization and supervision easier and more efficient. Guidelines supplied are similar to ICMA principles and the CBI Climate Bond Standard. An external verification report is also required.

A raft of new ESG-related legislation is under consideration in Congress in Chile, including a proposal to ban coal-fired power plants from 2025, and a Framework Law on Climate Change.

Other Latin American countries are undertaking similar initiatives, and these will likely gather momentum later in 2021 and into 2022, as the COP26 Conference in Glasgow unfolds and yields new agreements.

The NDCs published under the Paris Agreement require ratifying governments to take action to achieve the SDGs, especially to minimize global warming. These will no doubt be reinforced at COP26. In turn, this will likely increase demand for GSS bonds and the kinds of projects and other activities that they fund. Although this should present opportunities that lead to more issuances, it will likely also result in closer scrutiny. Issuers and investors should be aware of and willing to accommodate not only the commitments that have been made in the region, but also the priorities, in the context of sustainable development.

NDCs vary widely across Latin America in terms of the urgency they apply to address climate change impacts and in the scale of the targets. Heavily forested countries benefit from offsetting some of their GHG emissions through oxygen produced by their forests, in the quest for net-zero carbon, but sociopolitical considerations also play a role. The energy sector in particular faces a clear divide between countries that are actively pursuing transition from fossil fuels to renewables, and those that are still prioritizing fossil fuel-based technologies. In Mexico, the Inter-Ministerial Climate Change Commission (Comisión Intersectorial de Cambio Climático or CICC) approved the country's updated NDC in December 2020, but instead of setting progressively more ambitious targets, it merely "reaffirmed" the targets established five years ago, and which have been widely criticized as being inadequate.

Blended finance is an approach to structuring funding arrangements in ways that allow investors with different objectives (e.g., financial return versus positive environmental or social impact) to invest alongside each other. According to the International Finance Corporation (IFC), blended finance is "the use of relatively small amounts of concessional donor funds to mitigate specific investment risks and help rebalance risk-reward profiles of pioneering investments that are unable to proceed on strictly commercial terms."12

Blended finance is now a well-known structuring approach in financing essential projects, including in pursuit of the SDGs. The IFC, for instance, frequently applies blended finance—crowding in private finance to deliver sustainable impact in emerging and frontier markets.

For private investors, it can mitigate risk and poor returns for that risk, compared to other investment options available. For investors prioritizing ethical considerations, it can leverage available funding to create a greater level of investment than would have been possible on its own.

As a strategy, blended finance arrangements can be very flexible. Financing can be structured as debt, equity, risk-sharing, or guarantee products with different rates, tenor, security or rank. Under select facilities, they can also be performance-based incentive structures. Solutions depend, among other things, on the market barriers and failures that need to be addressed and the requirements of donors.

From fiscal year 2010 to 2020, the IFC deployed US$1.6 billion of concessional donor funds to support 266 high-impact projects in more than 50 countries, leveraging US$5.8 billion in IFC financing and more than US$6.8 billion from other private sources.13

Other multilateral banks (MDBs) that are actively funding GSS projects in Latin America, either through subscribing to GSS bonds or through structured finance or otherwise, include the IDB and the Corporacion Andina de Fomento – Banco de Desarrollo de América Latina (CAF) the central American (Banco Centroamericano de Integración Económica, CABEI) and FONPLATA, as well as country-specific development banks such as BNDES in Brazil.14

Table 2: Status of Latin American countries regarding carbon-neutrality targets

| Country | Signature | Ratification | Carbon-neutrality target date |

Status |

|---|---|---|---|---|

| Argentina | 22-April-16 | 21-September-16 | 2050 | Policy document issued |

| Belize | 22-April-16 | 22-April-16 | 2050 | Target under discussion |

| Bolivia | 22-April-16 | 5-October-16 | Not stated | - |

| Brazil | 22-April-16 | 21-September-16 | 2050 | Policy document issued |

| Chile | 20-April-16 | 10-February-17 | 2050 | Legislation proposed |

| Colombia | 22-April-16 | 12-July-18 | 2050 | Policy document issued |

| Costa Rica | 22-April-16 | 13-October-16 | 2050 | Policy document issued |

| Ecuador | 26-April-16 | 20-September-17 | 2050 | Target under discussion |

| El Salvador | 22-April-16 | 27-March-17 | Not stated | - |

| Guyana | 22-April-16 | 20-May-16 | 2050 | Target under discussion |

| Guatemala | 22-April-16 | 25-January-17 | Not stated | Target under discussion |

| Honduras | 22-April-16 | 21-September-16 | Not stated | - |

| Mexico | 22-April-16 | 21-September-16 | 2050 | Target under discussion |

| Nicaragua | - | 23-October-17 | 2050 | Target under discussion |

| Panama | 22-April-16 | 21-September-16 | 2050 | Policy document issued |

| Paraguay | 22-April-16 | 14-October-16 | Not stated | - |

| Peru | 22-April-16 | 25-July-16 | 2050 | Target under discussion |

| Suriname | 22-April-16 | 13-February-19 | N/A | Carbon-neutrality achieved |

| Uruguay | 22-April-16 | 19-October-16 | 2050 | Policy document issued |

| Venezuela | 22-April-16 | 21-July-17 | Not stated | - |

Source: Climate Change News, updated to July 7, 2021

Investor demand for GSS bonds and other sustainable finance instruments is unlikely to subside anytime soon. This can be seen in the degree to which such issuances are over-subscribed, and the low coupon rates achieved. A sympathetic administration in the US, the prospect of a green bond standard in the EU, general ESG concern as the effects of climate change become more visible, and ESG drivers in Asia-Pacific all converge to assure us that these instruments will be with us for a long time, and will continue to develop and become more sophisticated. COP26 will, if anything, likely accelerate this process. In coming years, we expect to see the criteria for sustainable finance become more stringent and more uniform standards emerge, as investors demand greater transparency. As demand for ESG transparency increases, and regulatory and policy frameworks become better developed, so ESG standards will also increasingly be included in funding arrangements more generally. In the interim, properly designed GSS bonds and other sustainable finance instruments are likely to remain popular with investors and issuers alike.

1 European Commission (2021), Overview of Sustainable Finance, European Commission website, available at: https://ec.europa.eu/info/business-economy-euro/banking-and-finance/sustainable-finance/overview-sustainable-finance_en#important.

2 https://sdgs.un.org/goals

3 L. L. Benites-Lazaro, P. A. Gremaud and L. A. Benites (2015), Business Responsibility Regarding Climate Change in Latin America: An Empirical Analysis from Clean Development Mechanism (CDM) Project Developers, The Extractive Industries and Society, Volume 5, pp. 297-306.

4 United Nations Framework Convention on Climate Change (UNFCCC) website, accessed on August 20, 2021, available at: https://cdm.unfccc.int/about/index.html.

5 Bloomberg NEF (2021), Sustainable Debt Issuance Hits $3 Trillion Threshold, available at: https://about.bnef.com/blog/sustainable-debt-issuance-hits-3-trillion-threshold/.

6 OECD (2017), Mobilizing Bond Markets for a Low-Carbon Transition, Green Finance and Investment, Paris, France: OECD Publishing.

7 https://www.bloomberg.com/professional/blog/game-on-esg-debt-issuance-passes-3-trillion-with-record-speed/.

8 BancoEstada (2021), BancoEstado Focuses on Gender for Economic Reactivation by Successfully Issuing a Women's Bond in JPY. BancoEstada website, available at: https://www.corporativo.bancoestado.cl/investor-relations/newsroom/news/2020/5191.

9 Economic Commission for Latin America and the Caribbean (ECLAC) (2021), Capital Flows to Latin America and the Caribbean: First Four Months of 2021 (LC/WAS/TS.2021/5), Santiago, 2021, p. 5.

10 P. Torres and B. Foster (2020), Opening the Black Box of ESG Data. Environmental Finance. Summer 2021, p. 12.

11 Ibid.

12 IFC (2021), Blended Concessional Finance. IFC website, available at: https://www.ifc.org/wps/wcm/connect/topics_ext_content/ifc_external_corporate_site/bf.

13 Ibid.

14 M. L. Hoyos (2020), Multilateral Development Banks in Latin America and the Caribbean. Yale School of Management website, available at: https://som.yale.edu/blog/multilateral-development-banks-in-latin-america-and-the-caribbean.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP

View full image: Breakdown of CDM projects globally (pie chart) and by country in Latin America (scatter chart) (PDF)

View full image: Breakdown of CDM projects globally (pie chart) and by country in Latin America (scatter chart) (PDF)

View full image: Cumulative debt issuance of ESG debt worldwide (PDF)

View full image: Cumulative debt issuance of ESG debt worldwide (PDF)

View full image: Figure 3: GSS bond issuances in a range of currencies and by a variety of issuer types have become an important

View full image: Figure 3: GSS bond issuances in a range of currencies and by a variety of issuer types have become an important

View full image: Latin American GSS bond issuances from the first issuances in 2014 to early July 2021, by bond type (PDF)

View full image: Latin American GSS bond issuances from the first issuances in 2014 to early July 2021, by bond type (PDF)

View full image: GSS bonds by number of issuances and GSS bonds by total deal size (in US$) (PDF)

View full image: GSS bonds by number of issuances and GSS bonds by total deal size (in US$) (PDF)

View full image: International environmental agreements to which Latin American countries are parties (PDF)

View full image: International environmental agreements to which Latin American countries are parties (PDF)