Latin America Group Leader and Editor of Latin America Focus

As we embark on our third year of Latin America Focus, the ever-evolving landscape in the region brings fresh opportunities and challenges for local, regional and international businesses.

After an extremely positive post-Covid growth spurt in 2022, so far 2023 has been a bit more challenging for the region with GDP growth slowing and political uncertainty increasing. Nevertheless, we see plenty of bright spots on the horizon and opportunities for those who know where to find them.

In our third compendium of market insight from the Latin America team at White & Case, we look at what those opportunities are and where challenges might arise for investors.

On the opportunity front, we examine the mining & metals industry in detail. Interest in the region's lithium reserves has soared with the continued growing demand for the mineral for the battery manufacturing process. The "lithium triangle" has turned into a "lithium quad" with Brazil joining Chile, Argentina and Bolivia as a significant supplier of lithium. However, the countries' differing approaches to regulation of the industry means that those looking to source lithium in the region will have to understand the market in each country to determine where, when and how to make significant investments.

The lithium market could potentially be the beneficiary of another Latin American trend: Nearshoring. In a world of escalating geopolitical volatility, there is a shift away from broader globalization towards a more localized approach to manufacturing and trade. Several countries in Latin America have implemented investment and tax treaties, which, along with the ongoing geopolitical shift, make the establishment of industrial plants in the region easier and more enticing than ever before.

In this issue, we also take a look at environmental, social and governance (ESG) considerations; compared to their counterparts in North America or Europe, Latin American companies have arguably been slower to respond to the trend to disclose their approach to ESG. However, within the region this varies widely depending on the industry, as our recent survey of private issuers has shown.

As ever in our volatile world, the threat of market shocks and their impact on businesses and industries remains constant. Three major Latin American airlines and a variety of other businesses recently went through lengthy and difficult insolvency procedures following the Covid crisis. The good news is that most of these businesses are now back on track and performing very well, thanks in part to the creative and unprecedented use of Chapter 11 of the US Bankruptcy Code as well as local insolvency regimes to restructure the debt and the capital structures of the effected companies.

Another bright spot for investors in Latin America in recent years is that international arbitration in the region continues to develop in remarkable fashion, providing foreign investors with recourse to fair and impartial justice when investment disputes arise.

We at White & Case continue to believe that the Latin American market holds long-term promise for the savvy investor. We hope that you find this issue of Latin America Focus, which contains articles from our top experts on the subjects referenced above, interesting and useful as you embark on additional business in the region.

Sustainability disclosures gain momentum among Latin American issuers

Behold the Lithium Quad? Latin America’s race for lithium market share

Lithium is one of the most important minerals when it comes to the energy transition, and Latin America is one of the most important regions for producing lithium.

The demand for lithium is intense, consistently beating expectations since the onset of the pandemic

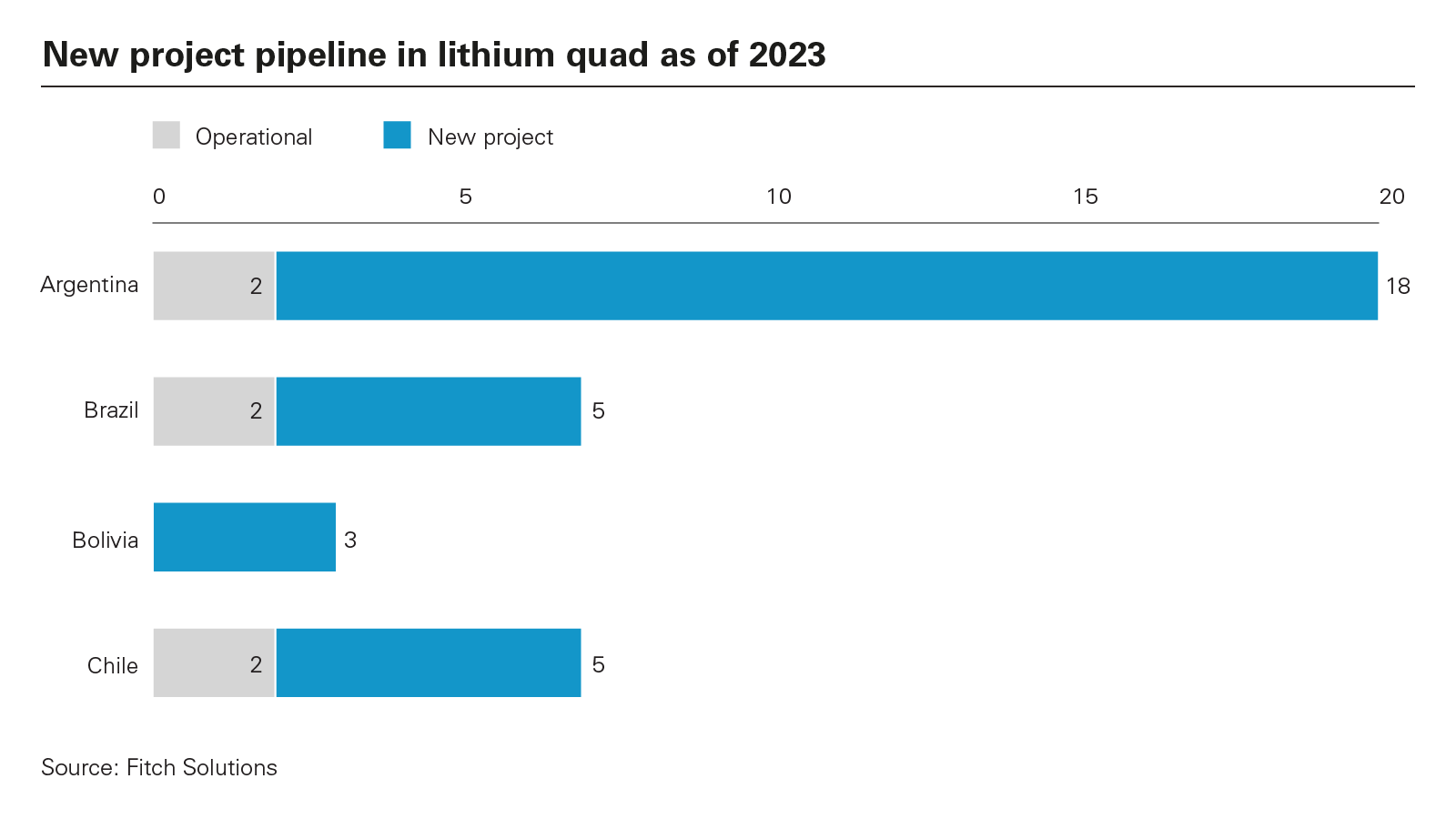

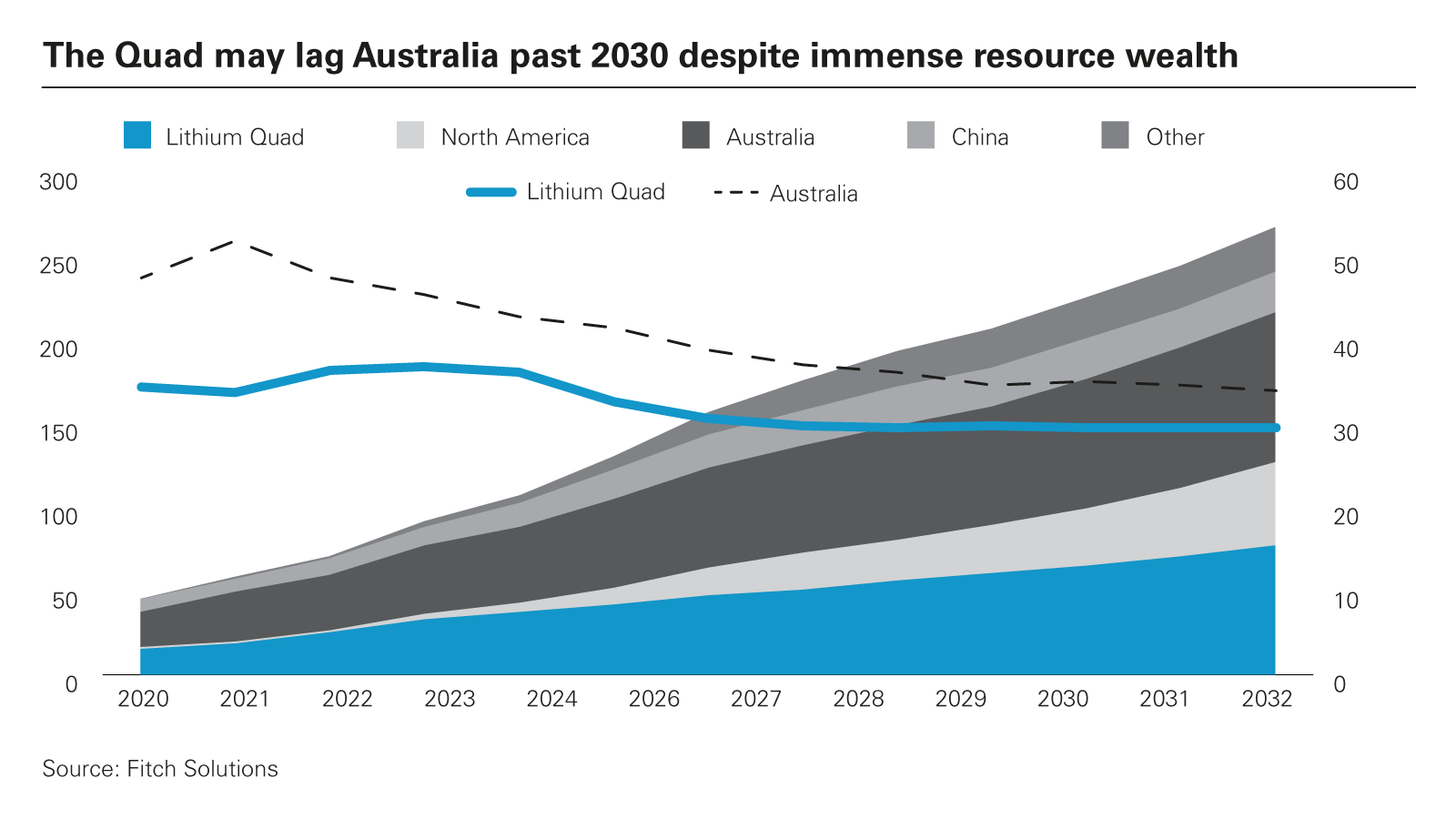

As governments and companies race to secure supplies of lithium for critical battery supply chains, interest in Latin America's considerable lithium reserves has surged. Miners, OEMs and other manufacturers look to Chile, Argentina and Bolivia for future supply.

This "lithium triangle" has historically been led by Chile, which alone was responsible for roughly 30 percent of global mined lithium production in 2022. But in the past 18 months, Brazil has seen several projects begin development or come to market, expanding the triangle into a quad.

Demand pressures in the lithium market are intense because of massive growth from a relatively low base, high degrees of uncertainty for investment and market outlooks, and market segmentation. Lithium is not one product, but several. Lithium carbonate is primarily used for lithium iron-phosphate (LFP), whereas the slightly more expensive lithium hydroxide is typically used for nickel cathode chemistries seen in the premium EV market. Extraction is similarly divided between hard rock spodumene, which normally has higher concentrations of lithium content and brines, the latter of which lacks a universal extraction process, as geology, water tables and the technology uses vary. Miners scrambling to bring new supply online are constrained and affected by geology and difficulties forecasting future balances of supply and demand, as demand for hydroxide and carbonate can diverge in some cases.

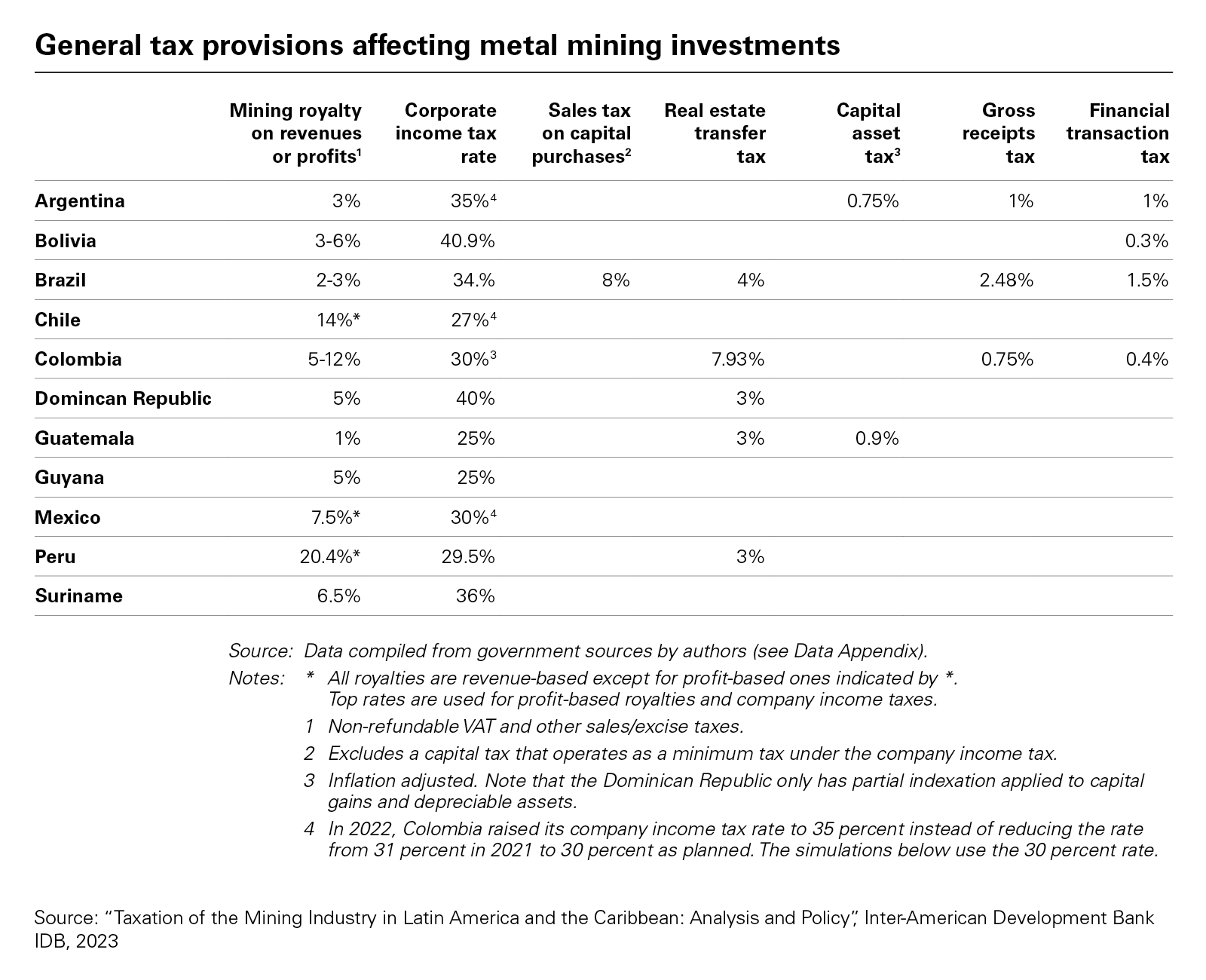

National policies also segment markets. Members of the lithium "quad" in Latin America are taking different approaches in hopes of securing more investment into lithium mining and refining projects, offering real-time case studies for miners and businesses navigating political risks and volatile markets. In each case, pressures to localize more of the lithium value chain after extraction, tax from national resource wealth, and the growing importance of preferential trade access to large export markets are changing how miners and new market entrants assess the value and prospects of developing new mines, refining facilities and cathode plants for battery supply chains in the region.

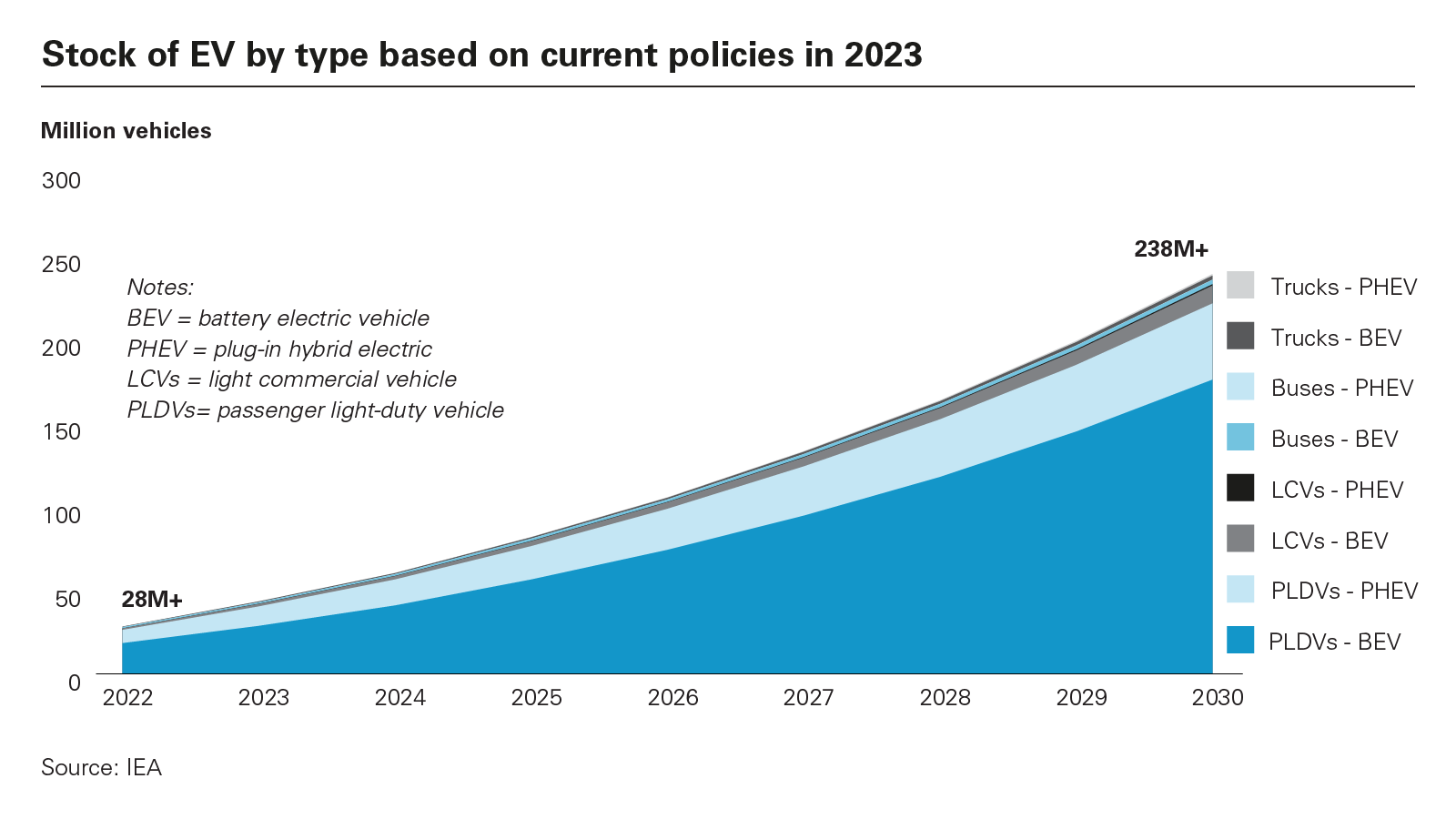

Less than 5 percent of cars sold globally in 2020 were EVs or plug-in hybrids

Chile: The region's lithium leader

Among the quad, Chile has the largest, most established lithium sector. The massive increase in prices seen last year coincided with the beginning of newly elected president Gabriel Boric's term.

Last April, Boric's government launched a "soft" nationalization program requiring lithium miners developing new projects to partner with and cede a majority share to Codelco, Chile's state-owned copper miner. Existing contracts for projects owned and operated by SQM and Albemarle, the two existing operators, are exempt until they expire in 2030 and 2043 respectively, introducing a significant degree of uncertainty over renegotiation. Since lithium is considered a strategic resource in Chile, the state will maintain an active role in its development.

In May of this year, the government also raised royalties on copper and lithium miners, raising the maximum tax burden from 44 percent to 47 percent as well as a 1 percent ad valorem tax on any operations producing 50,000 tonnes or more, and an additional tax of 8 percent to 26 percent on earnings linked to miners' operating margins. Depreciation as well as supply and work costs are taken into consideration for tax purposes.

Miners have broadly responded to the hike by lobbying for faster permitting times. At the time of writing, talks with Chilean lawmakers continue. New regulations also mandate all lithium projects use direct lithium extraction (DLE) techniques to minimize their water consumption extracting lithium from brine, adding a degree of technical difficulty for new projects.

Though these policies may reduce investment, they exploit the geopolitics surrounding critical minerals to bolster Chile's competitive position. The Inflation Reduction Act (IRA) provides tax credits to consumers purchasing cars with batteries using mineral inputs from the US or any country with which the US has a free trade agreement (FTA). Recognizing the crucial role Chile plays on the copper and lithium markets, the US Senate ratified a US-Chile tax treaty that has languished for more than a decade to limit the withholding taxes paid by US investors and companies investing and operating in Chile. The ongoing process to ratify the treaty and parallel efforts to deepen Chile's deep and comprehensive free trade agreement (DCTFA) with the EU underscore the importance of trade and interstate agreements for the economics underpinning critical minerals projects.

The proportion of EVs is expected to rise to 18 percent globally in 2023

Stock of EV by type based on current policies in 2023

Chinese companies have similar cause to re-examine additional investments into Chilean lithium projects to ensure they retain their competitiveness and ensure the eligibility of their products for IRA tax credits. Chinese firms already have a presence in the sector, as SQM is 23.8 percent owned by Tianqi. EV automaker BYD has begun engineering works to construct a US$290 million lithium cathode factory, building on a prior tender from last year to stand up a brine extraction operation. The project would allow BYD to export into the US market while helping Chile retain more of the value chain.

In short, the current Chilean government is betting that the demand and importance of lithium for the energy transition coupled with its market position and trade relationships give it more latitude to raise taxes and place key projects under state control.

Argentina: The market-led model

By contrast, Argentina is using a decentralized, market-led model to develop its lithium sector. Every province of Argentina has the constitutional authority to regulate and tax its own natural resource wealth. Unlike Chile, the sector is also unconsolidated, with 17 lithium miners including Livent, Rio Tinto, Ganfeng Lithium and Albemarle operating in-country.

Effective tax rates on projects are lower than in Chile, with income taxes set at 35 percent, VAT at 21 percent, and gross revenue royalties of 2 to 3 percent. Crucially, the national investment law in Argentina stipulates that fiscal agreements for projects are ensured for 30 years from the day a feasibility study is submitted, with the lone exception being any changes to VAT. The law also limits any provincial government's ability to raise royalties.

The devolution of regulatory and tax powers to provinces have led to mixed outcomes. For example, recent regional constitutional reforms undertaken by the government in the Province of Jujuy have triggered significant protest from the region's indigenous population because of changes that would permit miners to proceed with projects on or affecting indigenous lands after three weeks of public comment and debate. Justice minister Martín Soria requested the Supreme Court strike down the reform in June due to indigenous concerns, an issue that remains outstanding.

As the presidential election heads to a runoff on November 19, 2023, there is as yet no clear frontrunner but Peronist candidate Sergio Massa, Argentina’s current Economy Minister, outperformed expectations receiving 36.6 percent of the vote in the first round leading far-right populist Javier Milei and the conservative former Security Minister Patricia Bullrich who received 29.9 percent and 23.8 percent of the initial vote respectively. Massa has pledged to lead a national unity government should he clear the 40 percent threshold and achieve a 10 percent lead over his competitors in the next round. Whatever shape the new government takes, it will face significant challenges taming inflation and managing the Argentine peso amid sky-high inflation and interest rates, ongoing devaluation and high inflation. Thus far, the state regulates lithium like any other metal and has not labeled it a strategic resource. This could change in the future by necessity depending on the approach to macroeconomic stabilization adopted after the elections.

Even with these constraints, Argentina maintains a healthy pipeline of new lithium projects. Trade agreements similarly boost the attractiveness of the country's projects. Argentina has a standing FTA with the EU through its membership in Mercosur. Although there is not yet an FTA between the US and Argentina, officials have consistently argued that the existing trade and investment framework agreement (TIFA) meets the criteria established in the IRA's text, a condition that could similarly be met through a new bilateral trade agreement negotiated by the US executive branch through the USTR and US Commerce Department. Ongoing negotiations between the EU and Mercosur could also boost the competitiveness of projects to supply European markets, as well as encourage miners to localize refining and cathode production since the quality of lithium hydroxide can vary due to degradation over long sea voyages.

The share of EVs sold globally is projected to account for 60 percent by 2030

Bolivia: The odd man out

Bolivia has historically been the odd man out in the region, despite possessing some of the world's largest lithium reserves, though they may be eclipsed by a recent discovery in the United States. Lithium was declared a strategic resource and national priority in 2008 in Bolivia, launching a process whereby all pilot projects and lithium extraction would be state-run. Public-private partnerships would then be used to produce and commercialize battery metals, allowing the government and national mining arm Yacimientos del Litio Boliviano (YLB) to access international expertise and funding.

Prior to 2023, little progress was made in developing projects in Bolivia. That changed in the past ten months as firms look to secure new long-term supply: China's Citic Guoan Group and CATL have won contracts to develop projects with YLB, with CATL reportedly committing US$1.4 billion to its project. Both projects entail standing up DLE plants. Additionally, YLB signed a lithium agreement with Uranium One Group, a subsidiary of Russia's state-owned nuclear giant Rosatom. However, none of these companies have successfully deployed DLE elsewhere, and western offtakers are unlikely to buy any products sourced from a Russian state-owned enterprise given reputational and sanctions risks. Bolivia has yet to be fully incorporated into Mercosur and lacks an FTA with the US, but it does maintain a complementary agreement with Mexico reducing tariff barriers to potentially sell lithium hydroxide or cathodes into the USMCA trade area.

In Bolivia, the national approach to sector development remains state-led, with some similarities to Chile. However, the lack of clear trade advantages and limited expertise and experience within the government and state-owned enterprises to operate and financially manage mining operations pose significant challenges. Should lithium prices significantly increase again, it could encourage the state to take a more aggressive position negotiating transfers of IP and know-how until it can reduce or displace foreign investment into the sector. Even with the spurt of development, Bolivia's lithium sector will likely lag behind its neighbors.

What sets the lithium boom apart from traditional commodity boom-bust cycles is the degree to which the market is immature and national policies can create long-term competitive advantages

Brazil: The new kid on the lithium block

In the past two years, Brazil has become a fast-growing source of additional supplies of lithium to the market. Bowing to market realities, the government issued an executive order in 2022 exempting lithium exports from an approval process run by the Science and Technology Ministry's nuclear energy committee to facilitate more investment.

Although president Lula da Silva's election victory last year prompted concerns of heightened resource nationalism risks, the government has adopted an investor-friendly approach modeled on Australia, looking to speed up permitting processes to draw in more investment while committing to ensure stability for investment agreements and simplifying regulations where possible. However, a complex tax system, lack of tax incentives for mining projects and considerable litigation risks from notoriously arduous labor laws and regulations pose challenges.

Brazil's lithium sector is centred in Minas Gerais, a region with many large iron ore projects. The regional government has similarly pledged to support private firms to access to the infrastructure, energy and labor needed through the regional investment and trade promotion agency. Brazilian projects extract hard rock spodumene rather than the brine found in the Atacama desert and benefit from the wide array of extant mining activity taking place in Minas Gerais. This reduces the technical complexity and, in some cases, the capex intensity of new projects, lowering the barriers to entry for small and mid-sized miners looking to develop prospects.

Trade is again a key feature of Brazil's approach to sector development. As a member of Mercosur, Brazil already has preferential access to the EU. Though there is no US-Brazil FTA in effect, the two countries have signed a mutual recognition agreement allowing Brazilian exporters certified as authorized economic operators to meet the standards of the US Customs-Trade Partnership Against Terrorism program, reducing inspection times and customs requirements to enter the US market.

There is little impetus to reach an FTA with the US given the limited upside to the Brazilian economy, but ongoing diplomacy between the two countries concerning forestry and carbon sink management, and similar ecological and environmental issues leaves the door open to a later agreement similar to what Argentina is pursuing for IRA eligibility.

The great lithium game

The demand for lithium is intense, with demand consistently beating expectations since the pandemic began. According to the International Energy Agency, less than 5 percent of cars sold globally were battery electric vehicles (EVs) or plug-in hybrids in 2020. Three years on, this proportion is expected to reach 18 percent in 2023, and as much as 60 percent by 2030. OEMS have scrambled for supply over the last two years. They lack confidence in the availability of feedstock, and seek to minimize their exposure to highly volatile, often opaque spot markets. Latin America's "lithium quad" is enjoying the benefits.

With markets concerned about the potential for large deficits of lithium supplies emerging in the next five years, projects everywhere draw interest. But every investment boom into new supply eventually falls back to earth as supply matches and then overtakes demand, forcing marginal producers with higher costs and fewer efficiencies across the supply chain to cut costs, borrow and expand, or otherwise fold and sell out of the market. These dynamics are further complicated for lithium because of the lack of an effective benchmark price or futures market, denying miners the ability to hedge against price volatility and locking them into pricing mechanisms negotiated directly with offtakers that can drive a hard bargain for firms desperate for financing. What sets the lithium boom apart from traditional commodity boom-bust cycles is the degree to which the market is immature and national policies can create long-term competitive advantages, including through the localization of processing and refining.

Each member of the quad has a different approach with different implications for miners as well as something many other emerging market exporters lack: large bases of domestic consumers. Brazil, Argentina and Chile comprise three of the four largest economies in Latin America with a collective GDP on a PPP-adjusted basis in excess of US$4.7 trillion. Even with its challenges attracting investment, Bolivia's GDP is greater than that of Zimbabwe and Namibia combined, two countries leading the way among other emerging markets for lithium supply growth. Localizing the production of lower-cost EV models and investments into energy infrastructure can help sustain interest in lithium projects even as each government seeks to leverage its resource wealth in different ways even as today's projects are for export.

Geopolitics are also central to understanding the drivers of risks and opportunities for businesses looking to invest. President Lula has expressed interest in pursuing a Mercosur-China trade deal after completing negotiations with the EU, a move that would create opportunities for Chinese firms to build new supply chains to sell to Latin American consumers. Chinese OEMs lead producing and selling smaller EV models that are selling at a discount of US$10,000 or more compared to Western equivalents. Chile's longstanding trade ties with the US are also cause for Chinese firms to invest before American, Canadian or European counterparts are willing to commit large amounts of capital in politically risky conditions.

Latin America's critical minerals future is bright. So long as demand continues to rise, investors and miners will look for opportunity. Members of the "quad" will have to adapt accordingly as exporters elsewhere find new ways of attracting investment, take advantage of new trade arrangements, or exploit other advantages, such as physical proximity to end-users.

Nick Trickett (Manager, Business Development, White & Case, London) contributed to the development of this publication.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: New project pipeline in lithium quad as of 2023 (PDF)

View full image: New project pipeline in lithium quad as of 2023 (PDF)

View full image: Stock of EV by type based on current policies in 2023 (PDF)

View full image: Stock of EV by type based on current policies in 2023 (PDF)

View full image: General tax provisions affecting metal mining investments (PDF)

View full image: General tax provisions affecting metal mining investments (PDF)

View full image: The Quad may lag Australia past 2030 despite immense resource wealth (PDF)

View full image: The Quad may lag Australia past 2030 despite immense resource wealth (PDF)