The European non-performing loan landscape looks very different in 2022, with large deals driven by urgent government regulation supplanted by small but steady opportunities.

Foreword

The market for non-performing and non-core loan deals remains in business—but not in the way that many expected after COVID-19 shut down vast swathes of the European economy.

The banking sector's sale of legacy loans revived in 2021 following a marked slowdown in 2020, though the market did not return to the large-scale stocks of non-performing loans (NPLs) that were seen before the pandemic.

This may change if more distressed debt begins to emerge, having been protected by state interventions intended to support businesses affected by COVID-19. The events in Ukraine may also drive an increase in bad debt provisions and NPL volumes. For now, though, sellers, buyers and NPL market participants, such as servicers, are operating in a very different environment.

In this report, we take the temperature of that environment. The first section considers the changing dynamic of the marketplace, covering the outlook for NPLs, the rise of the secondary market transactions and the emergence of new types of NPL investors.

In section two, we take a deep dive into key markets across Europe. As in previous years, the economies of Southern Europe, led by Greece, Italy and Spain, were hotspots for NPL transactions. But other areas—notably Ireland, where NPL numbers were already relatively low—continue to see activity. Even in countries where banks are making very few disposals, the secondary market provides opportunities.

With so many unknowns, including the outcome of the situation in Ukraine and its impact on economics, the future for NPLs remains uncertain. But clear trends are emerging, from the growth of new entrants to the growing importance of data and analytics tools in driving value.

European NPLs: The journey from COVID-19 to Ukraine

While the spike in bad debt and subsequent tsunami of NPL and non-core loan deals that was anticipated due to COVID-19 did not materialise, the increasingly volatile market trends may lead investors to discover new and unexpected opportunities.

Regional spotlight on NPLs: Greece, Italy, Spain and beyond

Europe's banks continue to defy expectations that the pandemic would drive a significant increase in NPLs—in fact, according to the EBA, not a single country saw its banking sector's NPL ratio increase in 2021, with the vast majority reporting an improvement.

NPL market dynamics are changing, possibly for good

What does the future hold for NPLs? There's still plenty of business to be done, but buyers and sellers alike will need to change tack to get the most from the available opportunities.

Regional spotlight on NPLs: Greece, Italy, Spain and beyond

Europe's banks continue to defy expectations—not a single country saw its banking sector’s NPL ratio increase in 2021, with the vast majority reporting an improvement.

While the pandemic failed to produce heightened levels of toxic debt, the European banking sector also continued its efforts to reduce existing NPL volumes. The trend was particularly strong in Greece and Italy, with banks making good use of the state-backed schemes offering generous guarantees on large tranches of NPL debt.

Elsewhere, however, disposals were more limited, with activity shifting into the secondary market. This may prove to be temporary, with some banks reporting increased provisions in 2021. The longer-term impact of the pandemic is still far from clear and a rise in bad debt is possible in the most exposed sectors of the economy, including retail, leisure and tourism. And while European banks have limited direct exposure to events in Ukraine and Russia, the broader impacts of the situation will begin to bite.

In the meantime, however, the average bank's NPL ratio across the European Economic Area fell from 2.5 per cent to 2 per cent in 2021, according to the EBA.

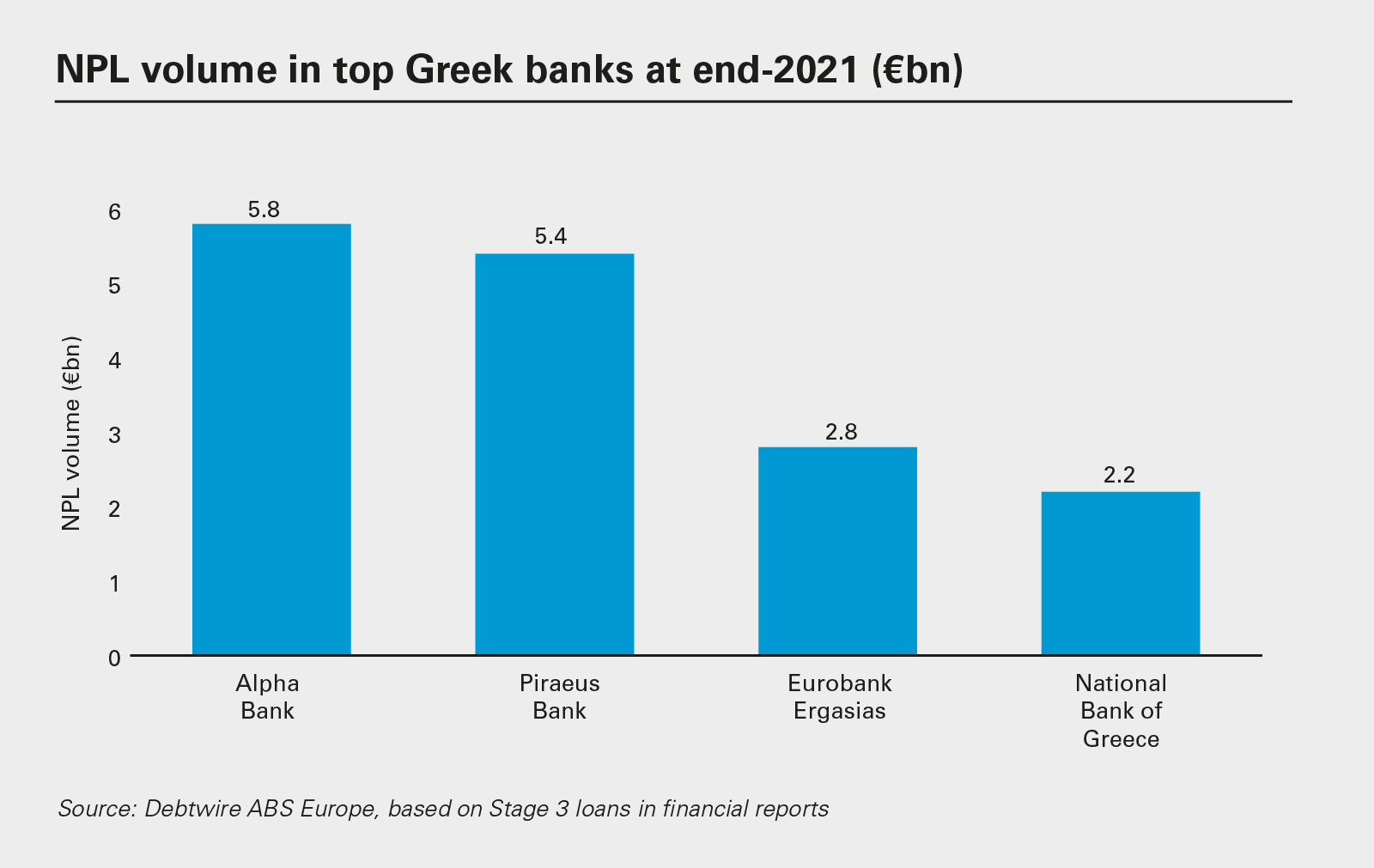

By the end of 2021, the country’s four largest lenders in Greece reported NPLs of approximately €16 billion on their balance sheets.

Greece: Rapid progress

Greece's banking sector continues to make strides towards normalcy, boosted by the government's Hercules Asset Protection Scheme (HAPS), which was modelled on the Italian Garanzia Cartolarizzazione Sofferenze (GACS) scheme. Through HAPS, the state guarantees securitised senior notes on loans while investors buy mezzanine and junior bonds.

The success of the HAPS programme has seen the proportion of Greek bank loans classified as NPLs fall from a high of close to 50 per cent in 2016 to 25.5 per cent at the start of 2021 and just 7 per cent by the end of the year.

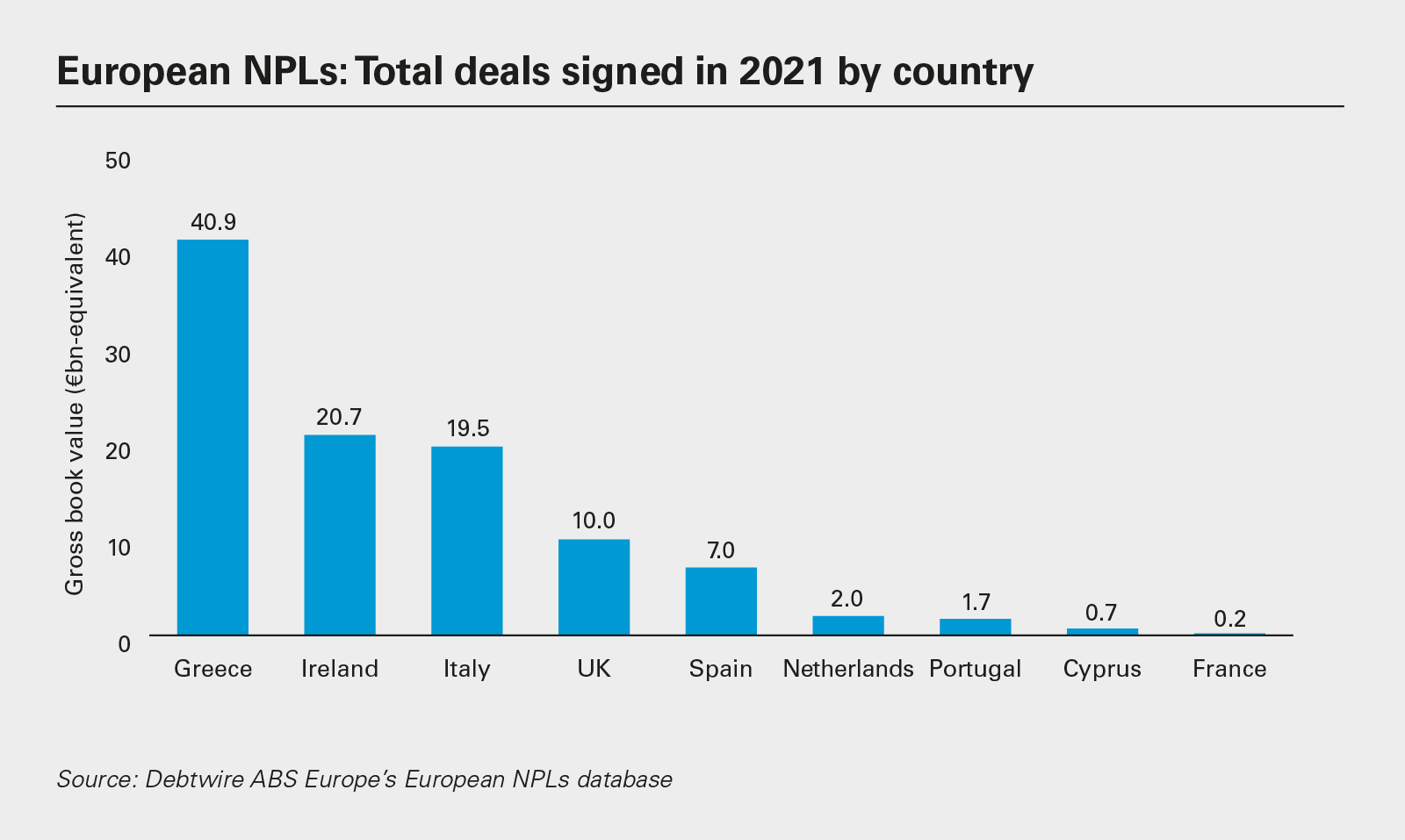

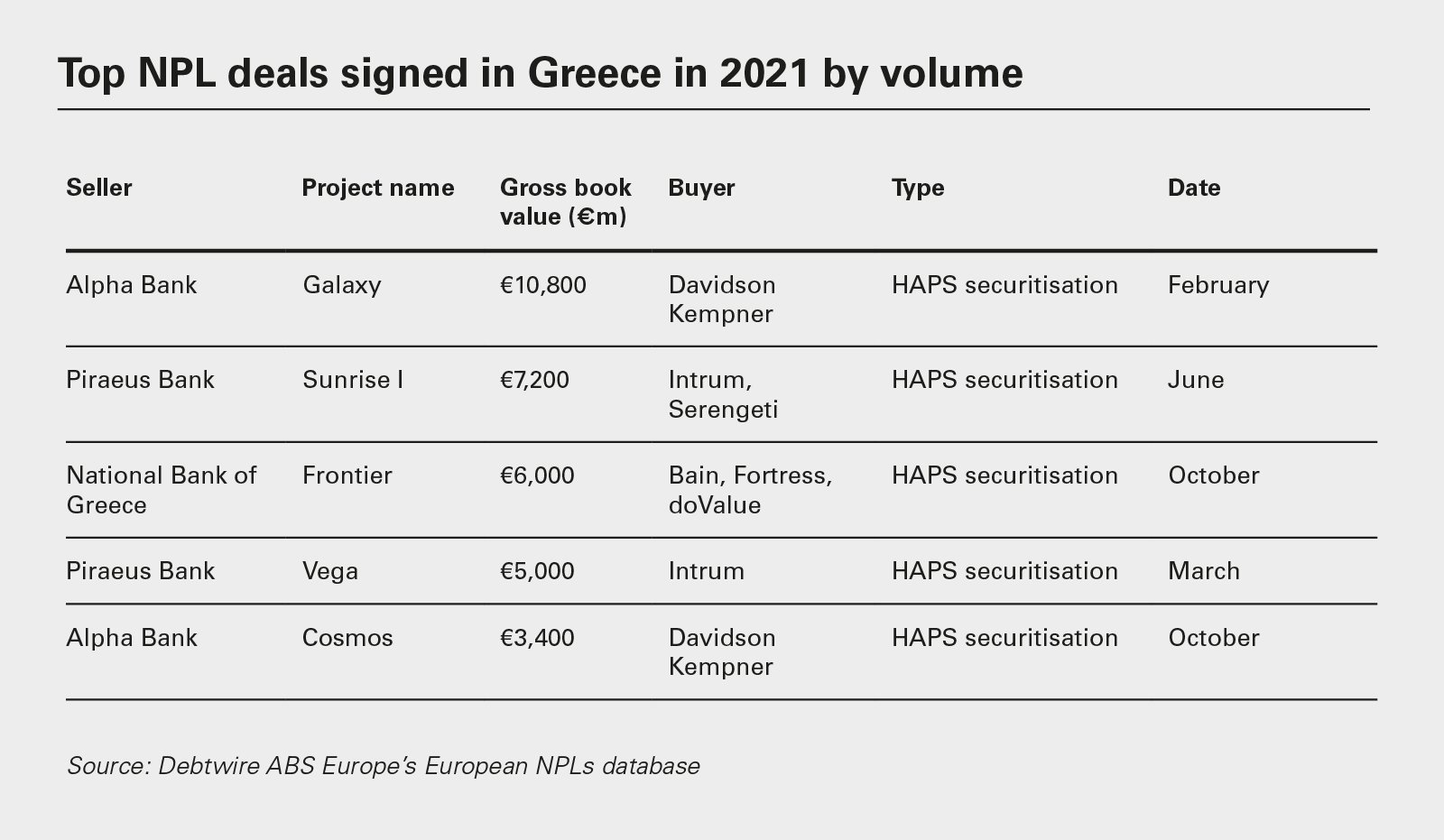

In total, Greek lenders shed appriximately €41 billion in NPLs last year, according to Debtwire ABS Europe. Of the deals contributing to that total, seven involved securitisations that took place through HAPS.

Those included Alpha Bank's €10.8 billion Project Galaxy NPL, with Davidson Kempner buying 51 per cent of the mezzanine and junior notes, Piraeus Bank's €7.2 billion Sunrise I deal with Intrum and Serengeti, and National Bank of Greece's €6 billion Project Frontier transaction with Bain Capital Credit, Fortress Investment Group and doValue.

Outside of HAPS, deals in 2021 tended to be smaller, even as both Alpha Bank and Attica Bank completed €1.3 billion transactions.

Much of the hard work has now been completed for banks in Greece. By the end of 2021, the country's four largest lenders reported NPLs of approximately €16 billion on their balance sheets—significantly less than a year earlier.

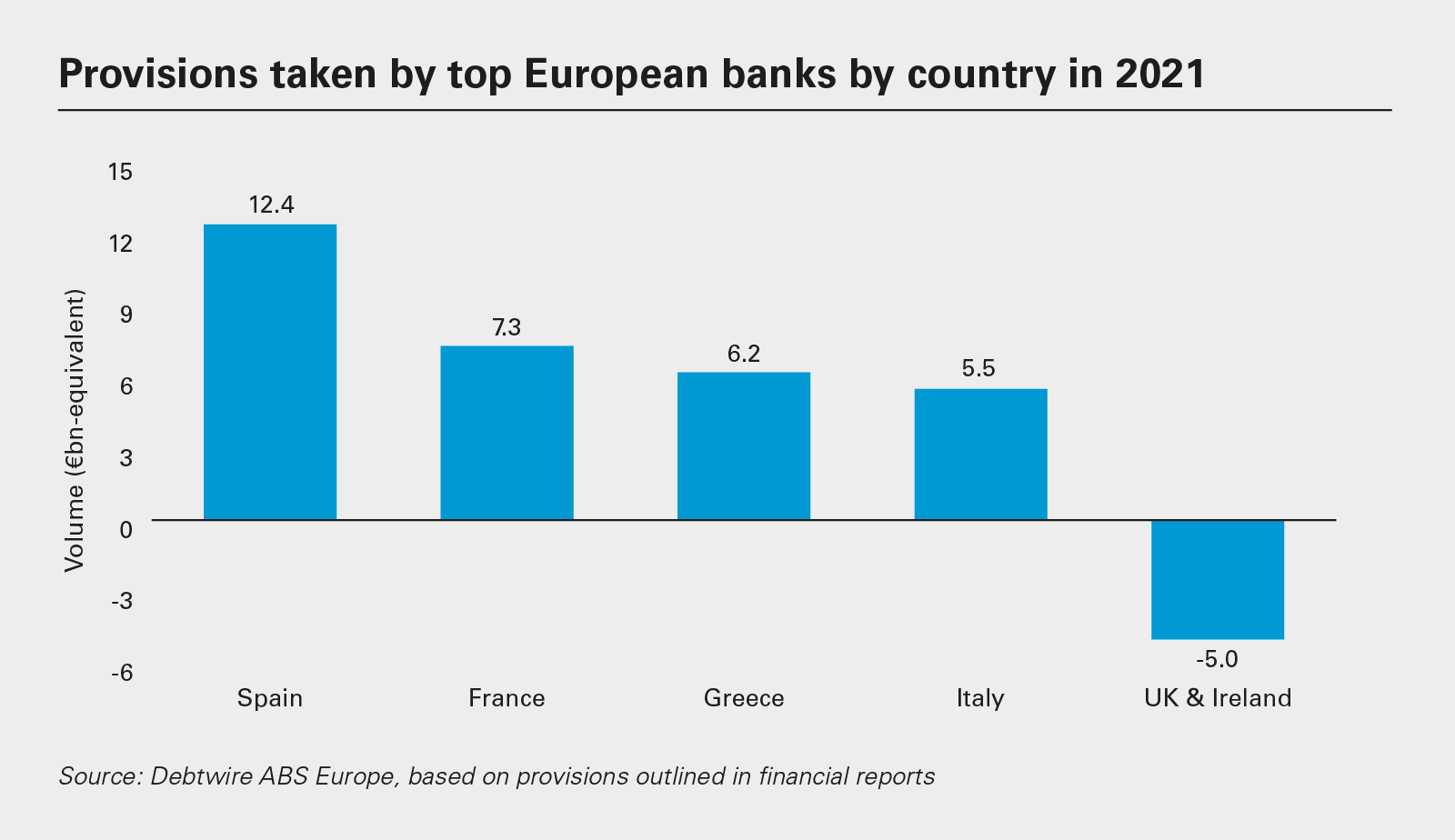

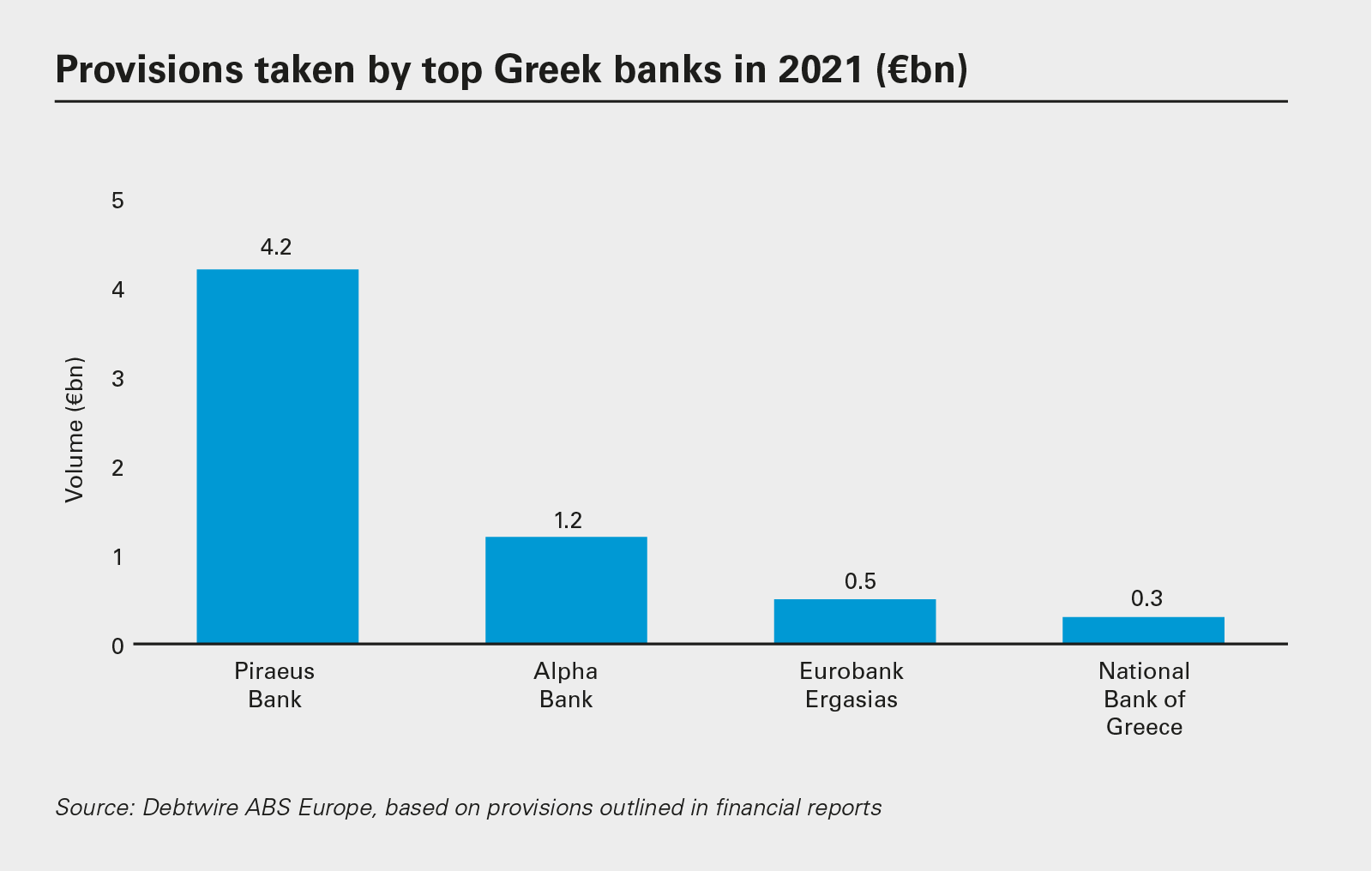

The outlook also remains relatively benign, with little evidence of any post-pandemic surge in NPLs. Greek banks did take net provisions of €6.2 billion in 2021 just in case, but look set to avoid major setbacks.

Italian banks have further reduced their stock of NPLs in the past 12 months, helped by a one-year extension of the state-backed Garanzia Cartolarizzazione Sofferenze (GACS). The scheme, which works in similar fashion to the Greek HAPS programme, had been due to end in June 2021, but the European Commission backed an extension until June 2022.

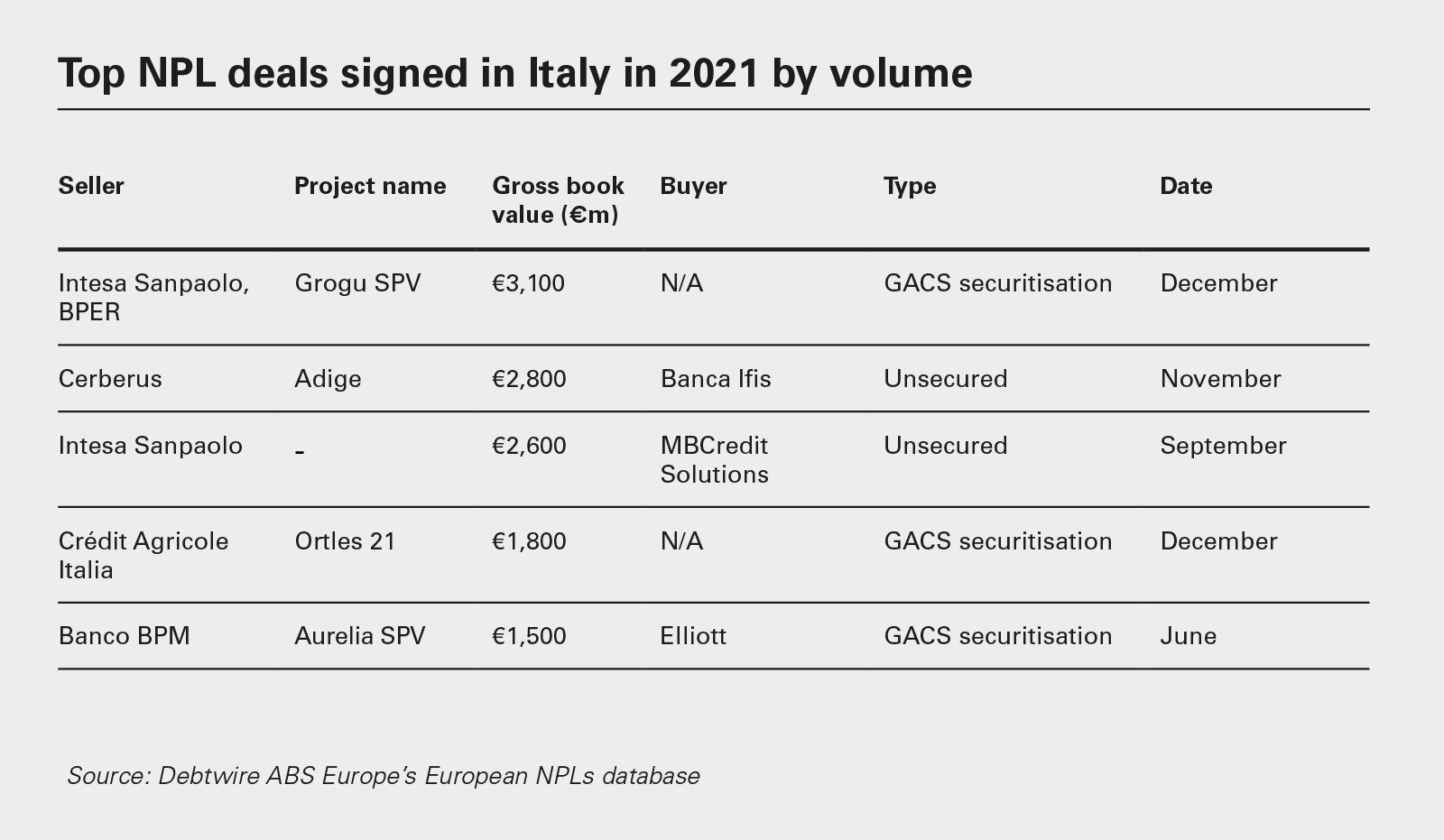

The extension of GACS allowed Italian banks to reduce their NPL load from 4 per cent to 3.1 per cent of their loan books over the course of the year. The sector offloaded NPLs worth a total of €19.5 billion in 2021, including sales of unlikely-to-pay (UTP) portfolios valued at approximately €600 million, according to Debtwire ABS Europe. Almost half that total was accounted for by disposals made under GACS.

Those included Intesa Sanpaolo and BPER's €3.1 billion NPL securitisation, as well as the €1.3 billion Iccrea Banca NPL securitisation of a real estate lease portfolio, which took the total number of deals completed through GACS in the past five years to more than 40—collectively worth close to €100 billion.

Italy's secondary market also continues to be active, with leading transactions last year including Cerberus's €2.8 billion portfolio sale to Banca Ifis.

However, anxiety may be creeping into the market about the performance of Italian transactions. Underperforming deals such as 4Mori Sardegna, Leviticus SPV, Maggese, Belvedere SPV and Popolare Bari NPLs 2016 all reported decreases in collections ratios of low to mid-single digit percentage points, as did Monte Paschi di Siena's giant Siena NPL 2018.

Some analysts are growing nervous. Scope, for example, has recently downgraded the senior notes of 17 out of 26 NPL transactions, with an average downgrade of two notches. That said, several outperforming deals have increased their collections ratios, according to Debtwire ABS Europe. Diana SPV went from 41.15 per cent above business plan to 58.1 per cent and Futura 2019 improved from 21.38 per cent to 37.67 per cent. In the middle, big swings were seen for Yoda SPV, which improved 10 percentage points to 9 per cent above business plan, and Juno 1, which swung from 10.1 per cent above business plan to 6.33 per cent below.

In one bright spot, UBI's Sirio NPL has consistently outperformed its initial business plan, and extended that as of March 2022 with gross collections 110.43 per cent above business plan and a profitability ratio of 145.83 per cent.

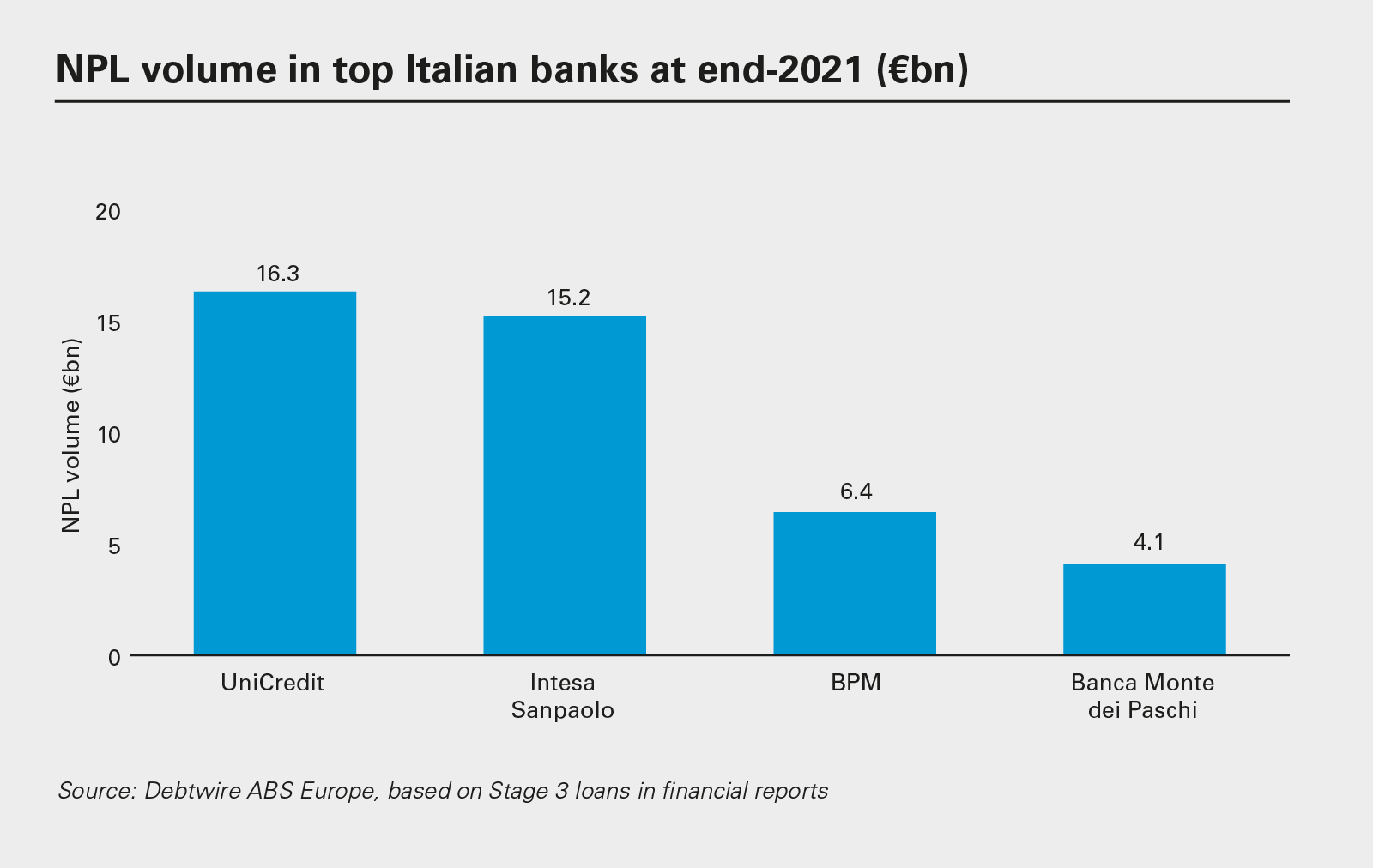

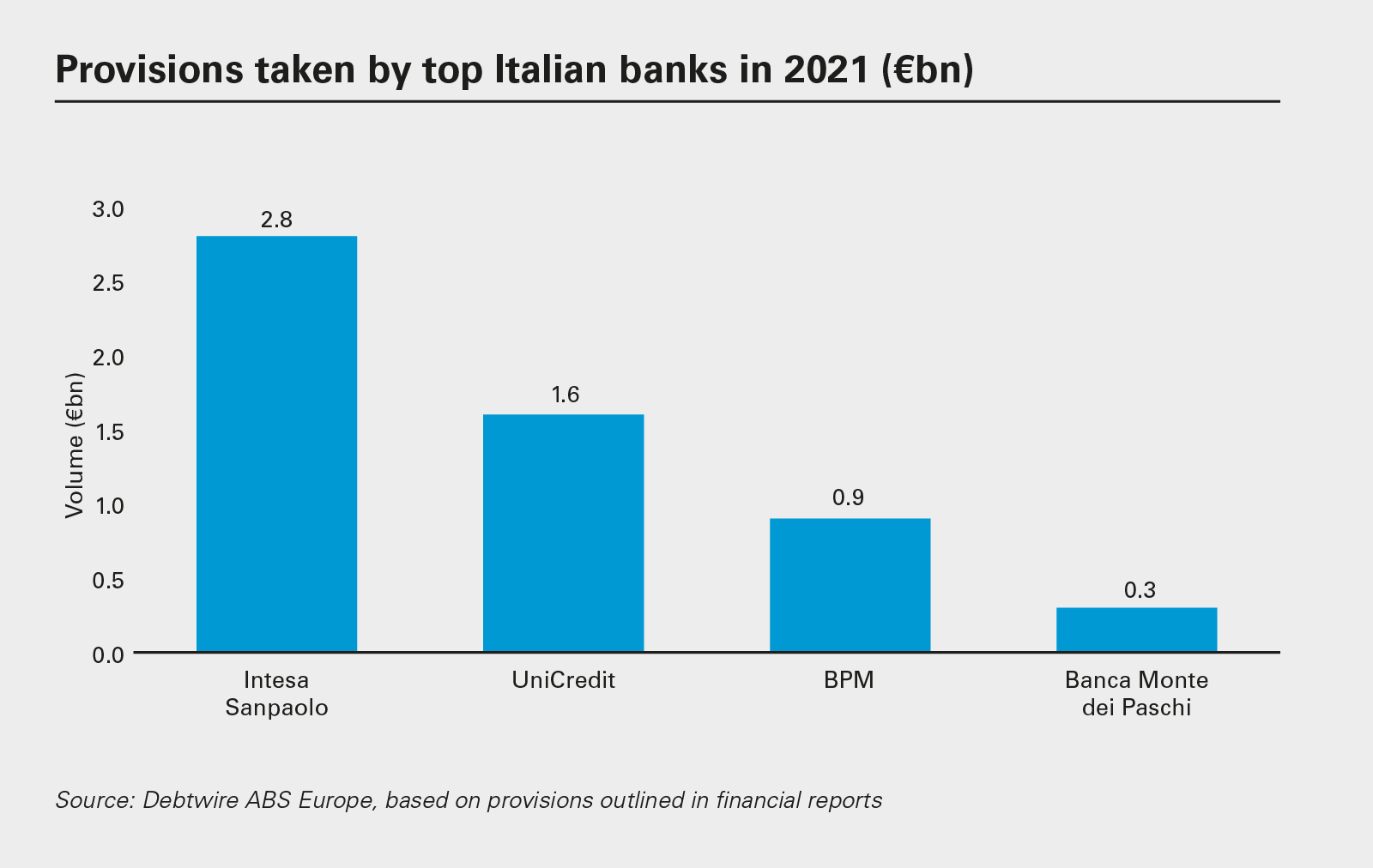

Looking forward, activity levels in Italy are difficult to predict. Italy's government is reportedly lobbying the European Commission for a further extension of GACS, possibly for up to two years. And while Italy's banks disposed of €19.5 billion worth of NPLs in 2021, these institutions still have almost €42 billion in bad debt on their balance sheets and took net provisions of €5.5 billion in 2021.

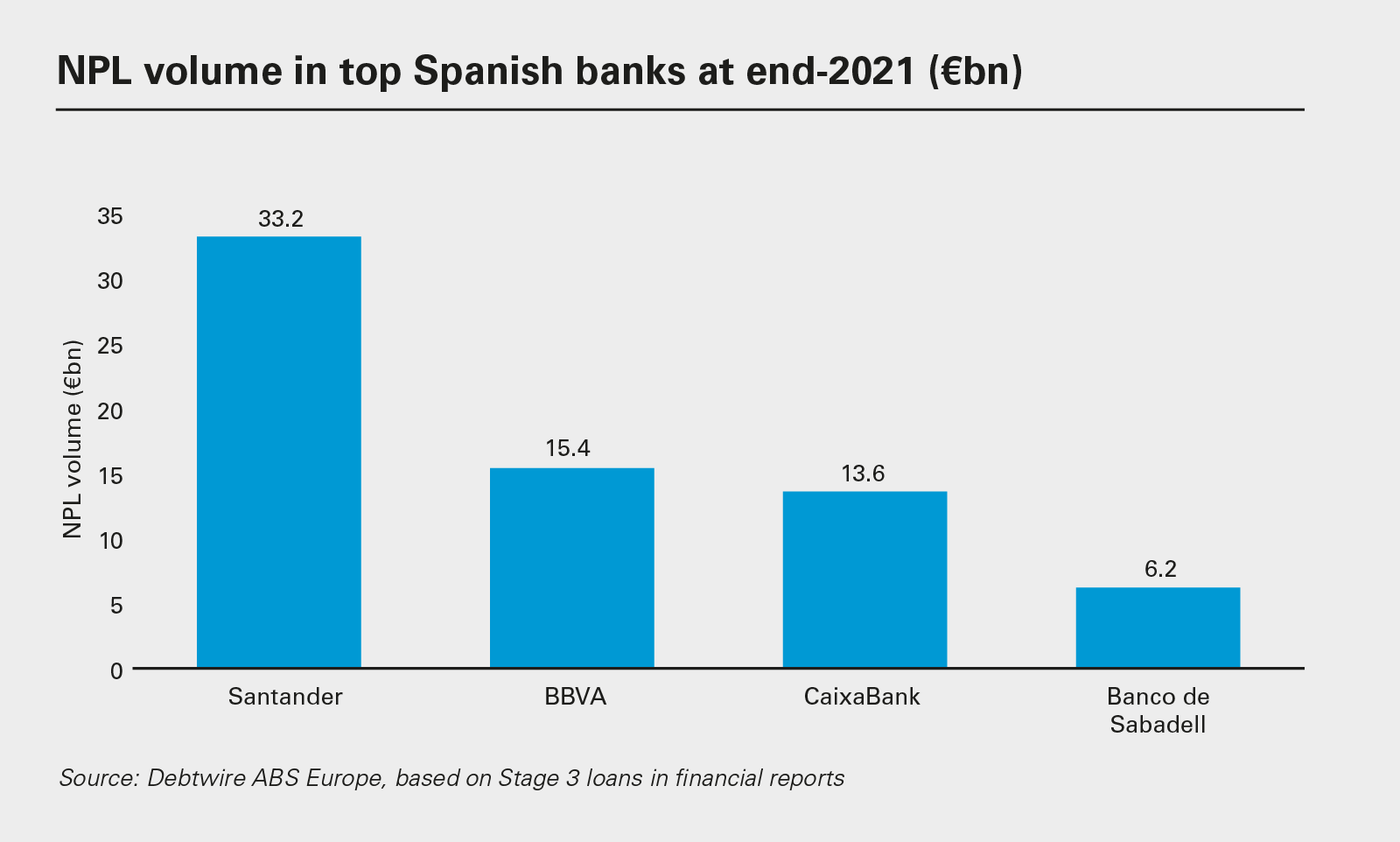

Despite the progress made in recent years, Spain still has one of the largest stockpiles of NPLs in Europe.

The country’s four largest banks have €68.5 billion in bad debt on their balance sheets.

Spain: Slower sales…for now

Most Spanish banks now have their NPL ratios under control and the flow of primary transactions has slowed, but secondary transactions by early-stage buyers are increasing, as are sales and securitisations of reperforming mortgage portfolios and giant servicing contracts are up for grabs.

The EBA reports that NPL ratios in the country's banking sector remained consistent in 2021, with 3 per cent of debt classified as non-performing by the end of the year, compared to 3.1 per cent 12 months earlier.

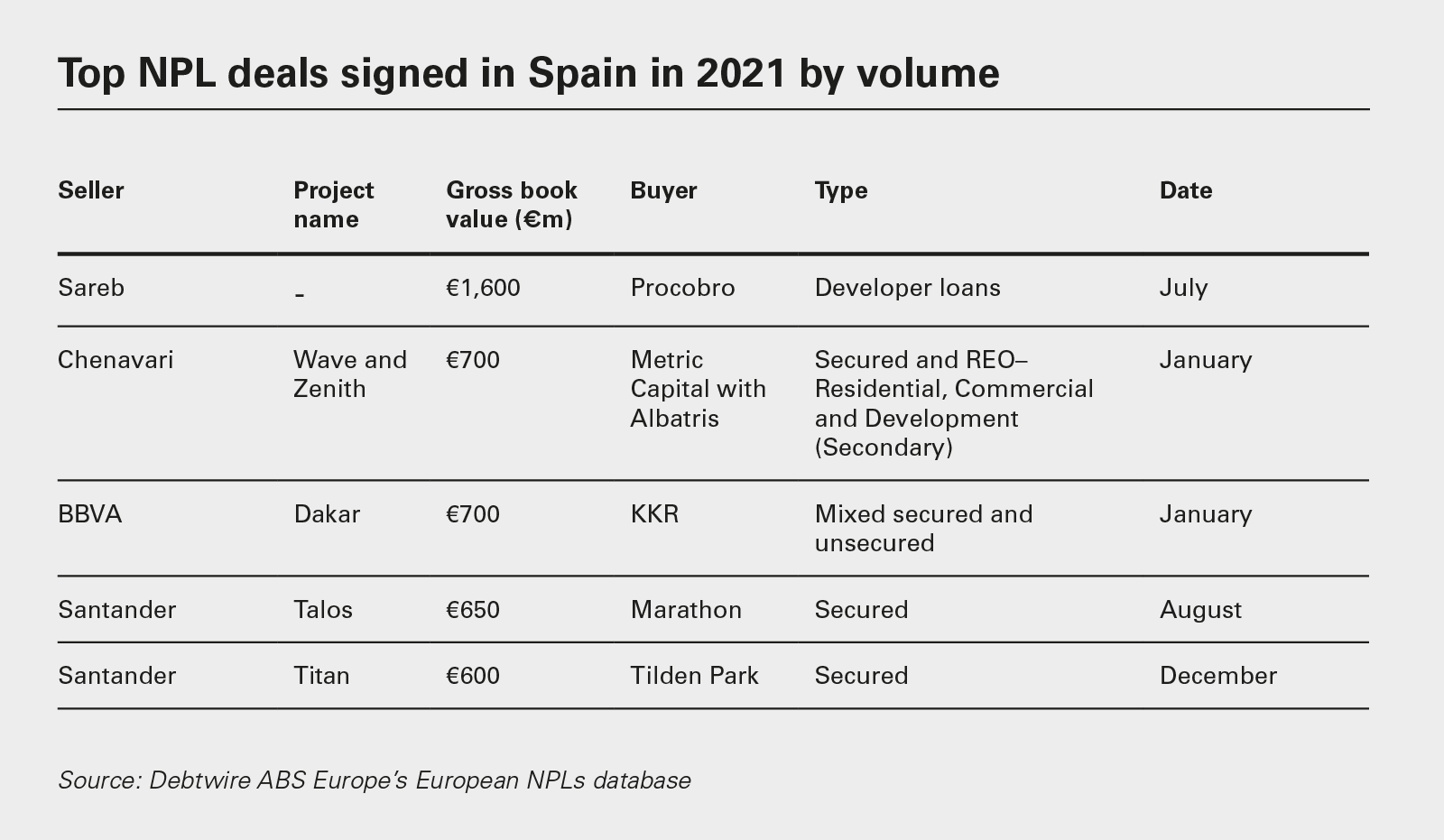

NPL disposals totalled nearly €7 billion in 2021. Notable deals included Sareb's offloading of a €1.6 billion portfolio of developer loans to Procobro and CaixaBank's sale of its €578 million residential NPL portfolio to KKR.

Banco Santander completed five disposals, including the sale of the €650 million Project Talos NPL portfolio to Marathon Asset Management, and the disposal of two Spanish hotel portfolios.

In the secondary market, Debtwire ABS Europe reports that some Spanish securitisations continue to disappoint, although last year did see a modest improvement for Prosil Acquisition (Salduero), whose collections increased a point to 50.5 per cent below business plan at the end of December. Retiro Mortgage Securities, however, deteriorated from 13.3 per cent below to 27.1 per cent below at the end of January.

Despite the progress made in recent years, Spain still has one of the largest stockpiles of NPLs in Europe. The country's four largest banks have €68.5 billion in bad debt on their balance sheets, despite disposals totalling €6.9 billion last year.

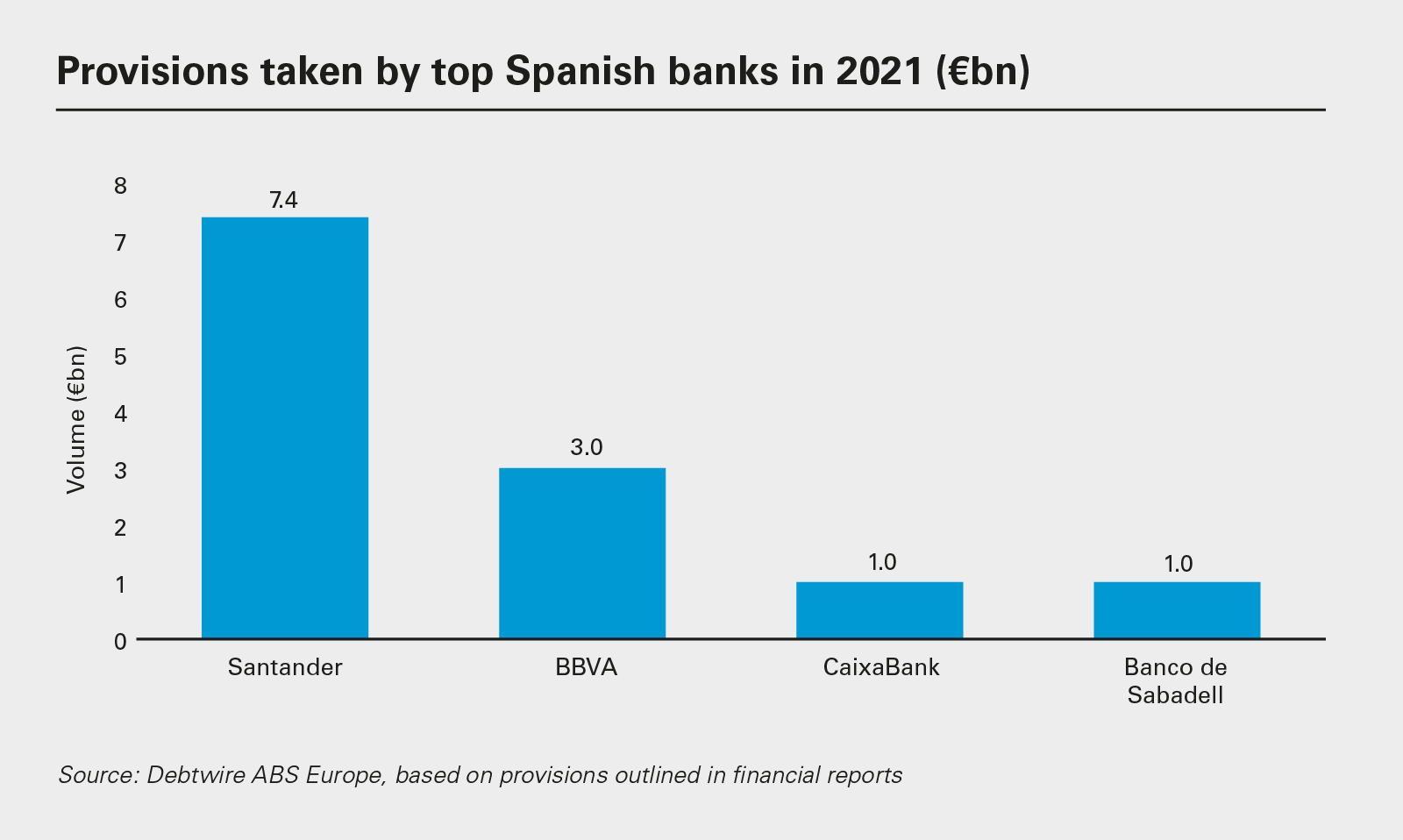

Moreover, provisions have risen sharply over the past 12 months, with the four largest banks earmarking a net €12.4 billion in 2021 for NPLs. Banco Santander took net provisions of €7.4 billion, while BBVA took €3 billion. That could swell the pipeline of deal activity in the months and years to come.

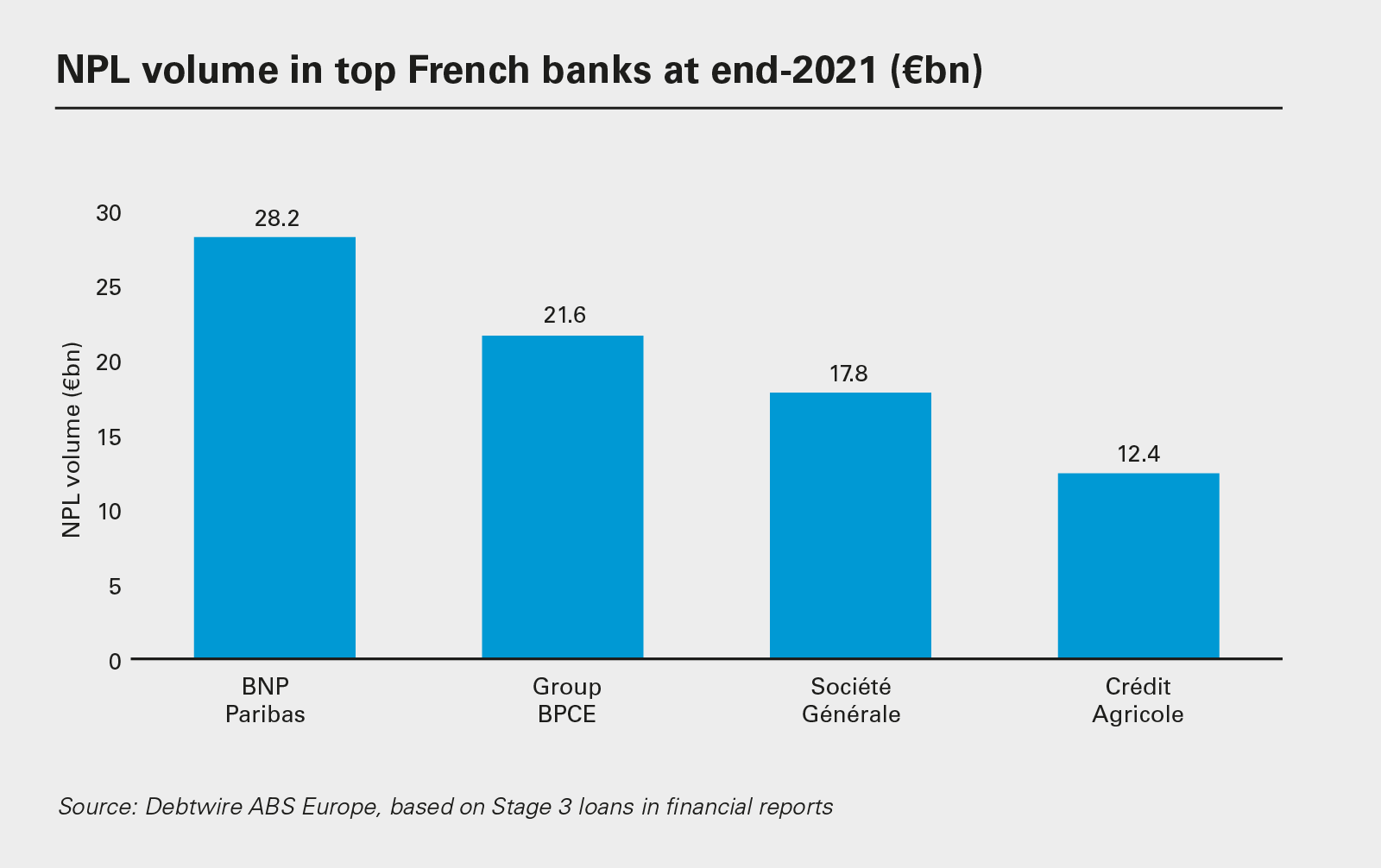

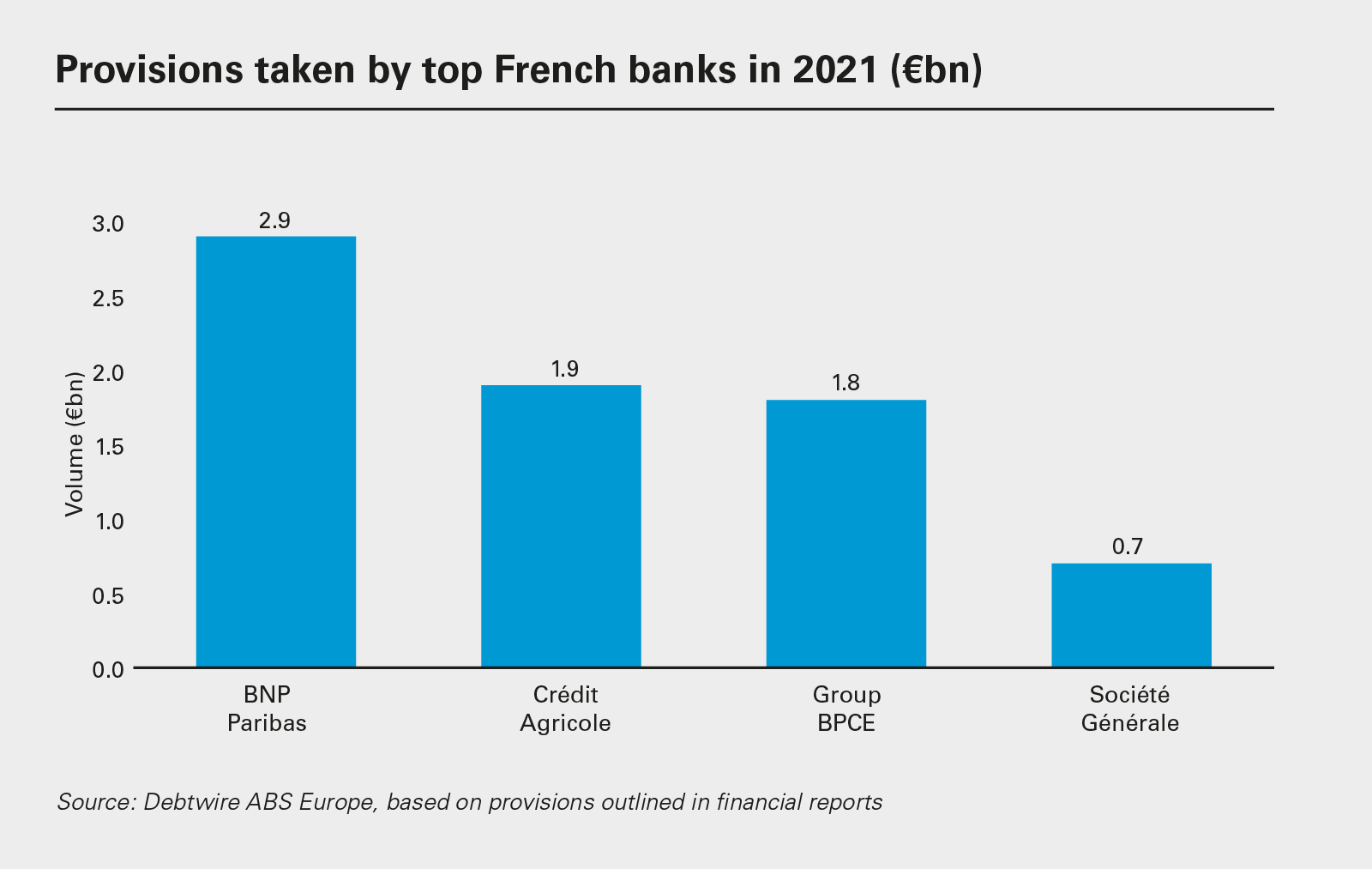

France, one of the European Union's largest economies, continues to report a benign NPL environment, with no sign of any imminent increase in impairments, and limited deal activity in the private market.

The French banking sector's NPL ratio was 1.9 per cent at the end of 2021, down from 2.1 per cent a year previously. Still, the country's four largest banks hold almost €80 billion in NPLs on their balance sheets, so more disposals can be expected in the years to come. That figure shrank by only €4.3 billion in 2021, and the four banks increased their provisions by a net €7.3 billion over the year.

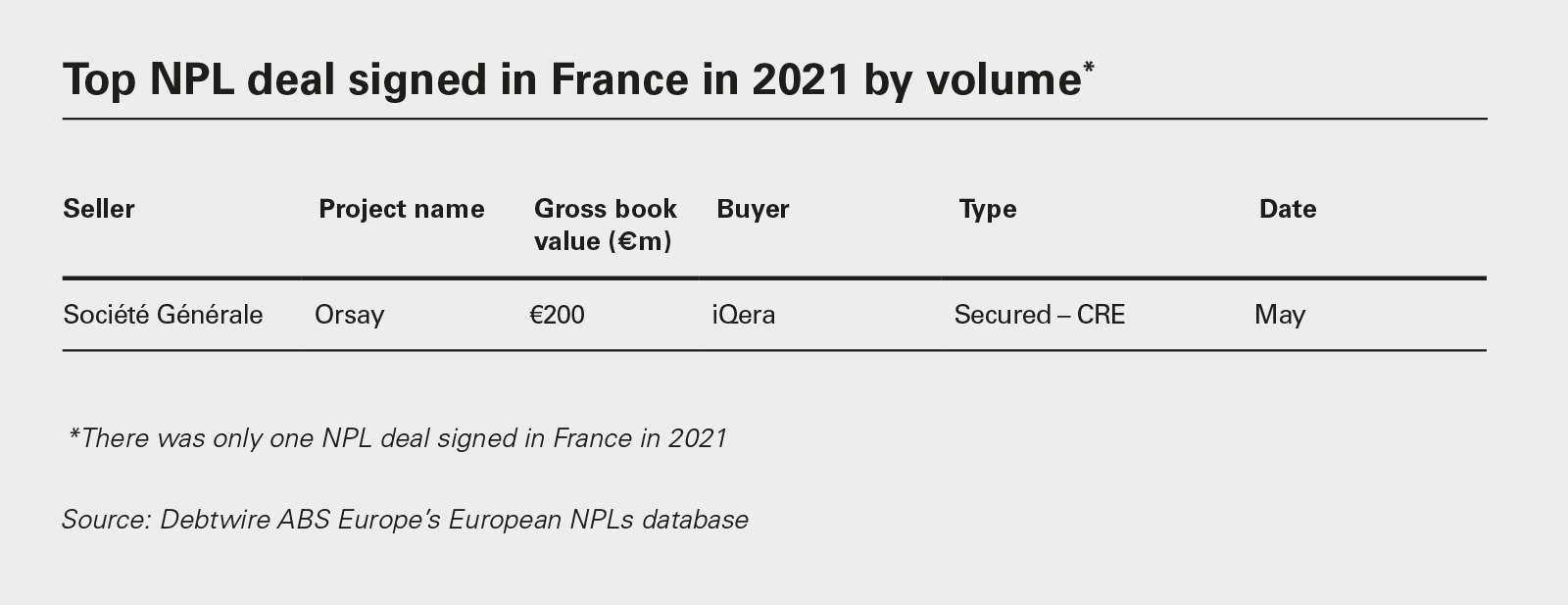

France saw just a single NPL transaction in 2021, the €200 million disposal of small and medium-enterprise NPLs by Société Générale, picked up by iQera.

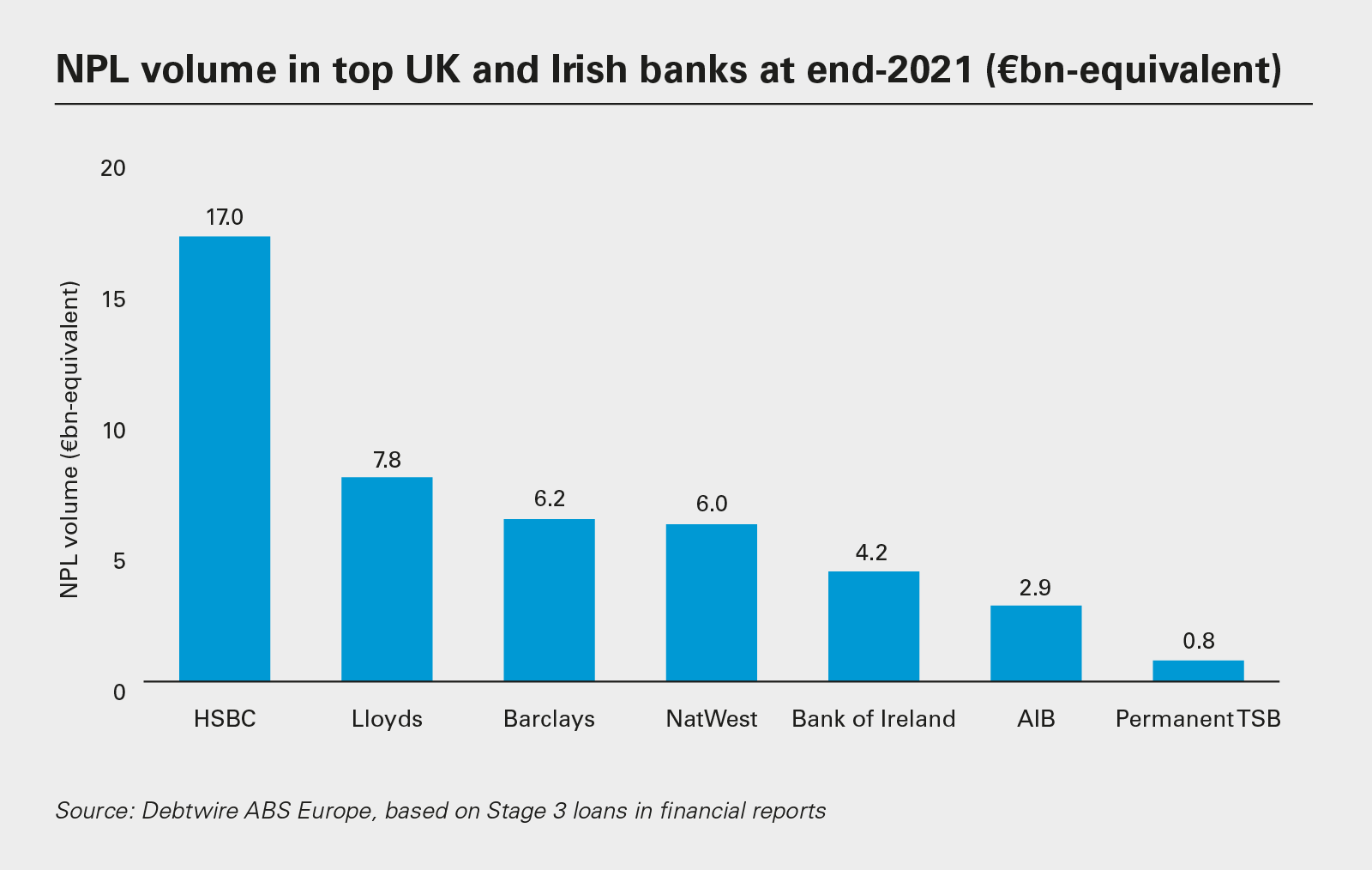

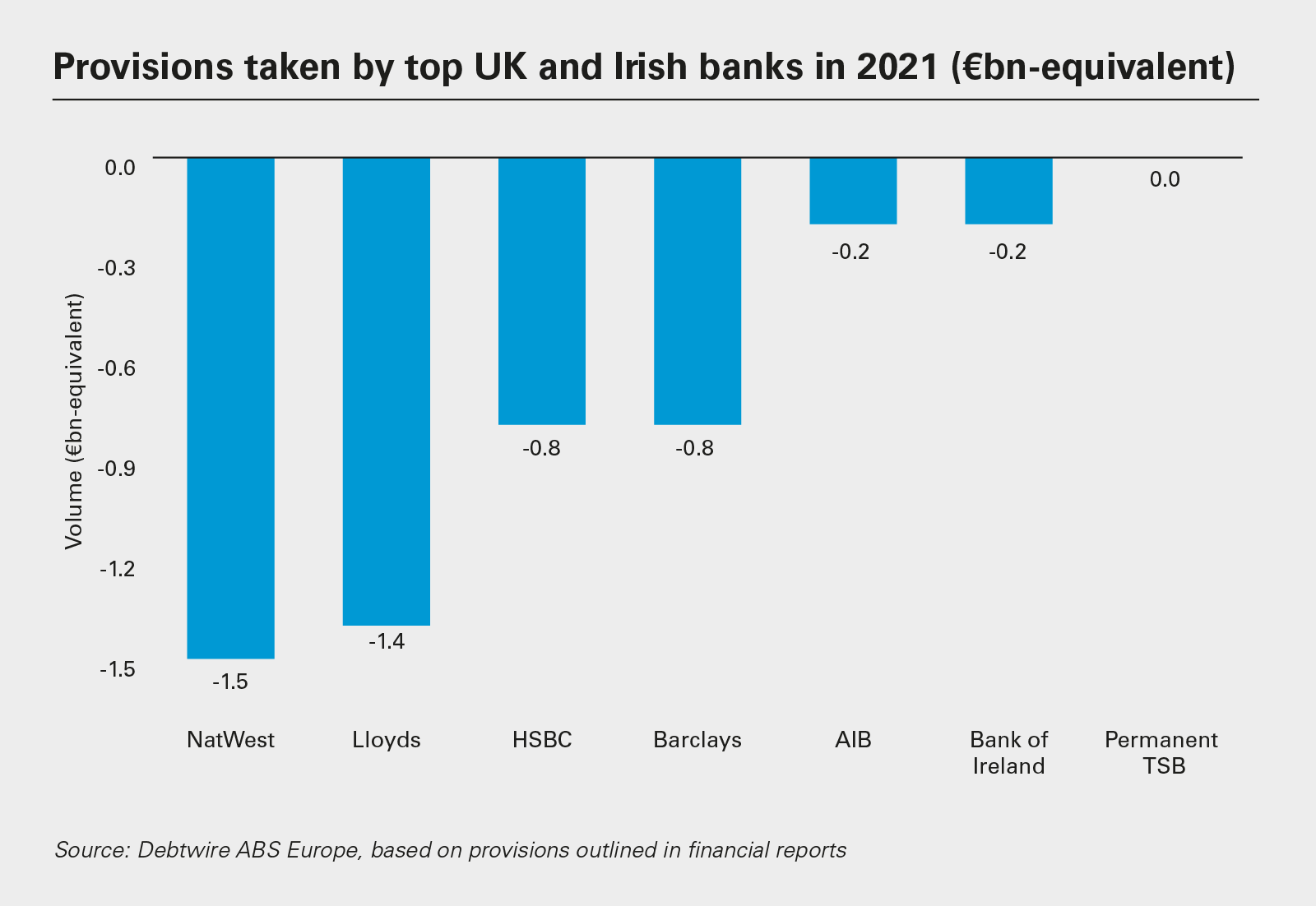

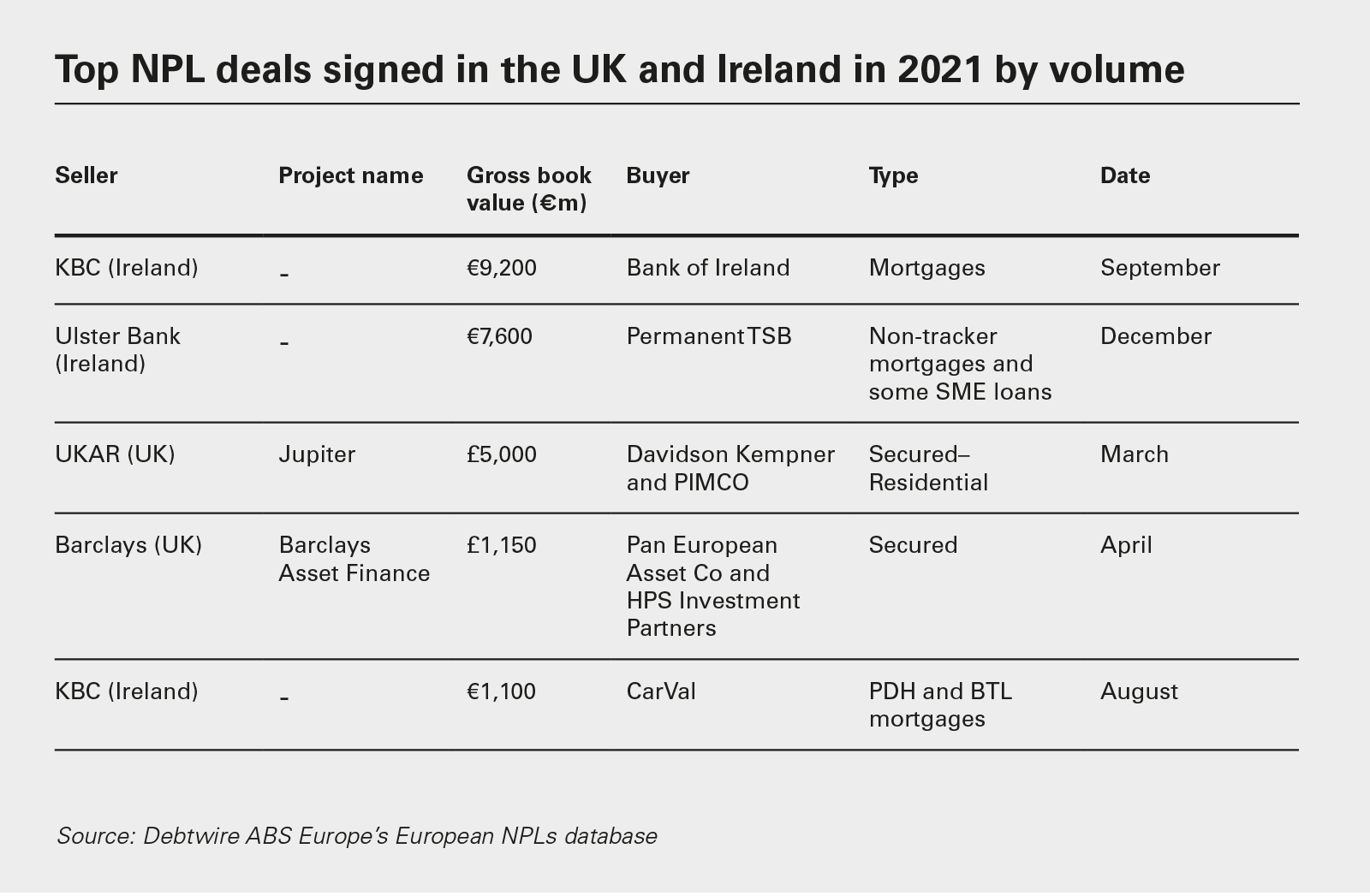

In the UK, the primary market for NPL disposals also remains muted, with just one significant transaction last year, NatWest Bank's £400 million Project Mercatus shopping centre NPL sale to a consortium of investors, which included Attestor, Octane Capital Partners and Ellandi.

Deal flows look unlikely to pick up in the immediate future, with the UK's four biggest banks reducing their NPL provisions by more than €4.5 billion last year. As a result, their NPL ratios averaged only 1.7 per cent by the end of the year.

Ireland continues to see heightened levels of activity, with €20.7 billion in NPLs and non-core loans sold in 2021, though the focus has shifted to disposals of performing loans by overseas lenders exiting the jurisdiction, such as KBC and NatWest. Ireland's three largest banks still hold NPLs and non-core loans with a gross book value of €7.9 billion on their balance sheets, though this was reduced by almost €1.7 billion last year. The sector's NPL ratio also decreased from 3.7 per cent to 2.8 per cent in 2021.

The German banking sector, meanwhile, continues to boast one of the lowest NPL ratios in Europe, with the EBA reporting a figure of 1.1 per cent at the end of 2021, slightly down on the 1.2 per cent at the start of the year. The country's two largest banks were carrying €14.7 billion in NPLs on their balance sheets at the end of the year, down €329 million year-on-year. Provisions increased by a net €395 million over 2021, but German banks announced zero sales of NPL portfolios last year.

One other country worth mentioning is Cyprus, where the Bank of Cyprus announced the Helix 3 sale of €698 million in NPLs to Pimco in November 2021. The disposal of this portfolio of 20,000 loans enabled the bank to bring its NPL ratio down to 8.6 per cent, taking the figure into single figures a year earlier than it had previously expected.

Indeed, while the banking sector in Cyprus is small in the context of Europe as a whole, it does have a significant NPL issue. Its NPL ratio has come down in the past year, but still stands at 4.1 per cent, one of the highest on the continent.

The country is also more exposed than most to Russia. RCB Bank, for example, has faced scrutiny from regulators given its links to Russian bank VTB, which owned a substantial stake in RCB until earlier this year. It recently sold a €556 million portfolio of NPLs to Hellenic Bank.

Moreover, Cypriot loan books loom large for banks in other jurisdictions. In February 2022, Greece's Alpha Bank announced the sale of a portfolio of Cypriot loans and real estate properties to Cerberus—the Project Sky portfolio was valued at €2.4 billion.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: European NPLs:Total deals signed in 2021 by country (PDF)

View full image: European NPLs:Total deals signed in 2021 by country (PDF)

View full image: Provisions taken by top European banks by country in 2021 (PDF)

View full image: Provisions taken by top European banks by country in 2021 (PDF)

View full image: Provisions taken by top Greek banks in 2021 (€bn) (PDF)

View full image: Provisions taken by top Greek banks in 2021 (€bn) (PDF)

View full image: Top NPL deals signed in Greece in 2021 by volume (PDF)

View full image: Top NPL deals signed in Greece in 2021 by volume (PDF)

View full image: NPL volume in top Greek banks at end-2021 (€bn) NPL (PDF)

View full image: NPL volume in top Greek banks at end-2021 (€bn) NPL (PDF)

View full image: NPL volume in top Italian banks at end-2021 (€bn) NPL (PDF)

View full image: NPL volume in top Italian banks at end-2021 (€bn) NPL (PDF)

View full image: Provisions taken by top Italian banks in 2021 (€bn) (PDF)

View full image: Provisions taken by top Italian banks in 2021 (€bn) (PDF)

View full image: Top NPL deals signed in Italy in 2021 by volume (PDF)

View full image: Top NPL deals signed in Italy in 2021 by volume (PDF)

View full image: NPL volume in top Spanish banks at end-2021 (€bn) (PDF)

View full image: NPL volume in top Spanish banks at end-2021 (€bn) (PDF)

View full image: Provisions taken by top Spanish banks in 2021 (€bn) (PDF)

View full image: Provisions taken by top Spanish banks in 2021 (€bn) (PDF)

View full image: Top NPL deals signed in Spain in 2021 by volume (PDF)

View full image: Top NPL deals signed in Spain in 2021 by volume (PDF)

/sites/default/files/2022-06/european-npls-infographic-015.pdf

/sites/default/files/2022-06/european-npls-infographic-015.pdf

View full image: Provisions taken by top French banksin 2021 (€bn) (PDF)

View full image: Provisions taken by top French banksin 2021 (€bn) (PDF)

View full image: Top NPL deal signed in France in 2021 by volume (PDF)

View full image: Top NPL deal signed in France in 2021 by volume (PDF)

View full image: NPL volume in top UK and Irish banks at end-2021 (€bn-equivalent) (PDF)

View full image: NPL volume in top UK and Irish banks at end-2021 (€bn-equivalent) (PDF)

View full image: Provisions taken by top UK and Irish banks in 2021 (€bn-equivalent)

View full image: Provisions taken by top UK and Irish banks in 2021 (€bn-equivalent)

View full image: Top NPL deals signed in the UK and Ireland in 2021 by volume (PDF)

View full image: Top NPL deals signed in the UK and Ireland in 2021 by volume (PDF)