Mining & metals 2021: Forces of transition and influencers of change

What's inside

The mining & metals industry is critical to the success of the world's transition towards net zero, both in reducing its own carbon footprint and providing the materials that will deliver a cleaner and more sustainable future

The mining & metals sector is enjoying renewed global macro-economic prominence, with the minerals and metals it produces—and, increasingly, recycles—being critical to the success of the world's energy transition toward a low-carbon future.

The resilience of the sector and of commodity prices throughout the COVID-19 pandemic, coupled with growing investor and consumer excitement about energy transition materials, has lured generalist investors toward the sector for the first time in years, turning the tide on the ESG concerns and lackluster returns that had previously worked against generalist investor sentiment.

The ESG agenda has undoubtedly been a major driver of change in recent times, and the expectations bar is continuously being raised by investors, governments, communities, consumers and other stakeholders. There is tremendous opportunity for industry players to embed an ESG and low-carbon culture—capturing both risks and opportunities—into their corporate strategies in order to build stakeholder trust, focus on ESG/low-carbon-compatible business lines and generate truly sustainable growth.

In the lead-up to COP-26, in this Insight series from the White & Case Global Mining & Metals team, we examine some of the major forces of transition in the global mining & metals sector, digging into those people, products, policies and institutions that are at the forefront of influencing change in our sector.

Taking ESG seriously: The crucial role of mining investors in the energy transition

Taking ESG matters seriously improves business performance; ESG best practice must become integral to the business and should be a "given" in any mining project.

As governments around the world are pursuing revised mining fiscal policies and more aggressive enforcement, investors need to prepare themselves for an active period of resource nationalism.

Investors are returning to mining & metals amid an almost unprecedented rally in the US capital markets that is taking place despite the continued economic challenges related to the COVID-19 pandemic

Key considerations around bribery and corruption risks, as the mining & metals sector is gaining critical momentum in the world's energy transition toward a low-carbon future.

Estimated global excess production capacity for steel, about one-quarter of global capacity

Carbon: the next frontier of commodities trade tensions

Governments around the world are prioritizing the decarbonization of the metals sector, and in particular steel and aluminum production, in their efforts to combat climate change.

The metals sector is an attractive target for decarbonization due to the energy-intensive nature of traditional production processes; the widespread use of metals in infrastructure, manufacturing and consumer applications; and the importance of metals such as copper for renewable energy generation.

Although domestic policies will play an important role in facilitating the transition, the prevalence of cross-border trade in metals has prompted some governments to propose new rules aimed at promoting sustainable production practices. The most significant proposal is the EU's Carbon Border Adjustment Mechanism (CBAM), which would impose a levy on imports in carbon-intensive sectors such as steel, aluminum, cement and fertilizers from countries with lower environmental standards than the EU.

Similar proposals are gaining momentum in the US Congress, as lawmakers contemplate new measures to limit carbon emissions, and President Joe Biden has expressed support for carbon border adjustments on several occasions. Such measures may help to combat climate change, but they are also likely to generate trade disputes, and could lead to retaliatory actions extending beyond the metals sector.

Curtailing industrial overcapacity is a longstanding priority of many governments, including those of the US and the EU

Overcapacity and the transition to green production practices

The push for more sustainable production in the metals sector comes at a time of heightened trade tensions, particularly in the steel and aluminum industries. These tensions stem largely from the chronic problem of global excess production capacity and its dampening effect on industry profitability; the EU recently estimated global excess production capacity at 624 million tons for steel, or about one-quarter of global capacity.

Having made little progress toward curtailing subsidies and other policies that contribute to overcapacity, the world's major steel and aluminum markets have increasingly resorted to import restrictions to protect their domestic industries. These include antidumping and countervailing duties, used heavily by the US and the EU in particular; safeguard measures, employed by the EU, the UK and Canada, among others; and blanket tariffs and quotas imposed by the US under Section 232 of the Trade Expansion Act.

Even with these measures in place, overcapacity reduces the attractiveness of investments in new manufacturing facilities that have less carbon-intensive production methods.

Curtailing industrial overcapacity is a longstanding priority of many governments, including those of the US and the EU, which have pledged to develop solutions to the problem this year as part of their "renewed transatlantic partnership" under the Biden administration.

Progress on overcapacity would help ease the transition to more sustainable steel and aluminum production, but it is unlikely to come quickly given the apparent reluctance of major producing countries such as China to engage on the issue. In the meantime, some governments see an urgent need to accelerate the transition to less carbon-intensive production methods, and to prevent the "carbon leakage" that could occur where domestic policies to reduce emissions encourage the outsourcing of production to jurisdictions with less ambitious climate policies.

The new Carbon Border Adjustment Mechanism (CBAM) proposed by the European Commission will take effect in 2026, following a three-year transition period

Enter the CBAM

Preventing carbon leakage and promoting cleaner production abroad are the stated objectives of the new Carbon Border Adjustment Mechanism (CBAM) proposed by the European Commission. The CBAM is intended to impose a charge on carbon-intensive imports such as cement, iron and steel, aluminum, fertilizers and electricity, that corresponds with the charges imposed on EU domestic industry under the EU's Emissions Trading System (ETS).

The ETS requires domestic producers in certain carbon-intensive sectors to surrender a number of allowances annually to cover their emissions. Similarly, the CBAM would require importers to purchase annual "CBAM certificates" to cover the emissions embedded in their imports. The price of the certificates would be linked to the price of permits under the ETS.

Importantly, the CBAM would take into account the methods used to produce the imported goods as well as carbon pricing policies in the country of origin. The amount of CBAM certificates required would be based on actual emissions at the installations from which imported goods originate—unless these cannot be adequately determined— and importers would be permitted to claim a reduction in the number of required CBAM certificates to account for a carbon price paid in the country of origin.

The CBAM would take effect in 2026, following a three-year transition period during which it would only require importers to report the level of emissions embedded in their imports. The CBAM would also phase out the free emissions allowances currently provided to EU producers of steel, aluminum, and other goods under the ETS, and would reduce accordingly the amount of CBAM certificates that importers must purchase during this period.

The CBAM's effects on specific industries will depend on trade flows, the climate policies of the EU's trading partners and the emissions intensity of production practices, which can vary widely among countries and producers.

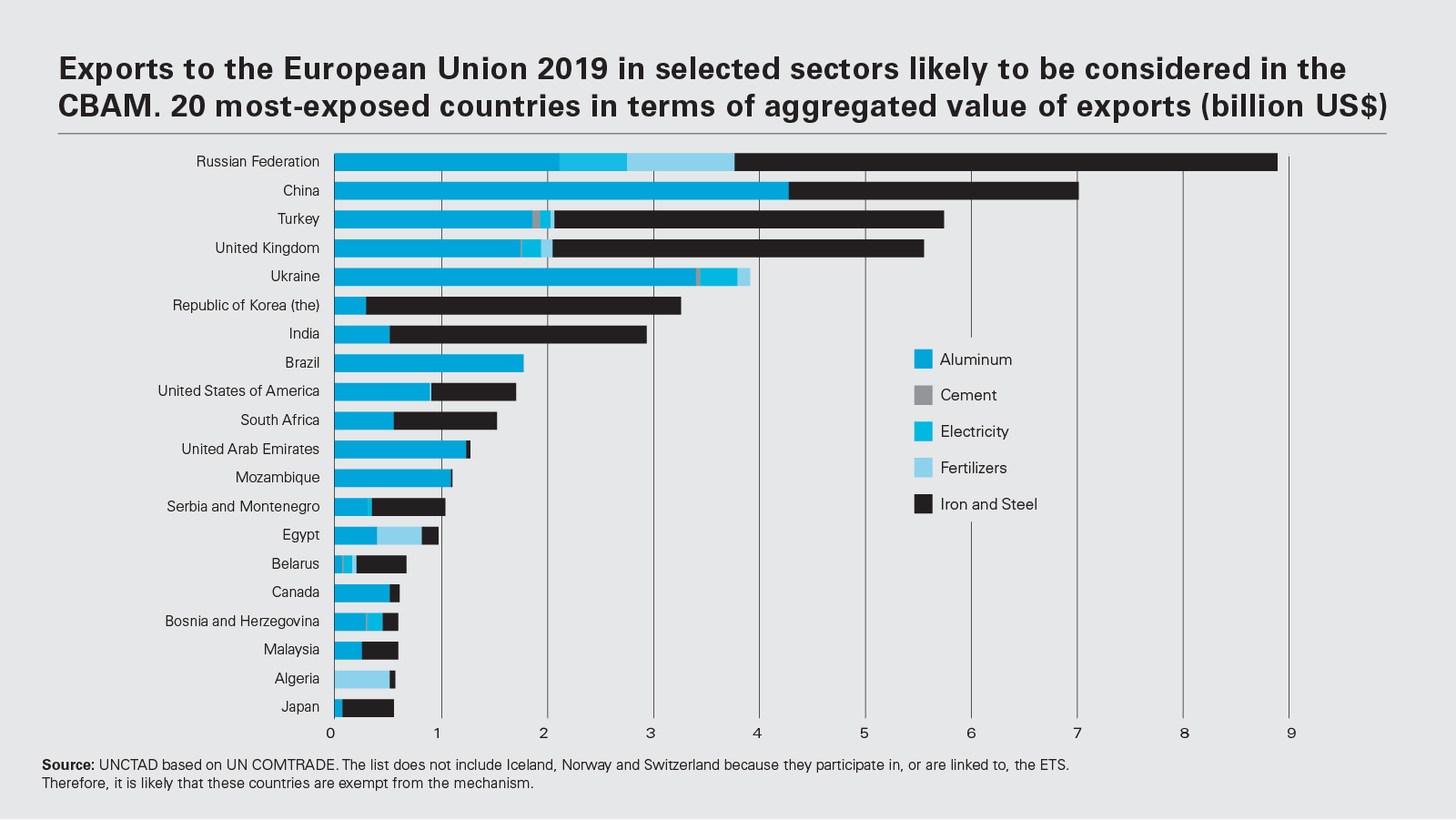

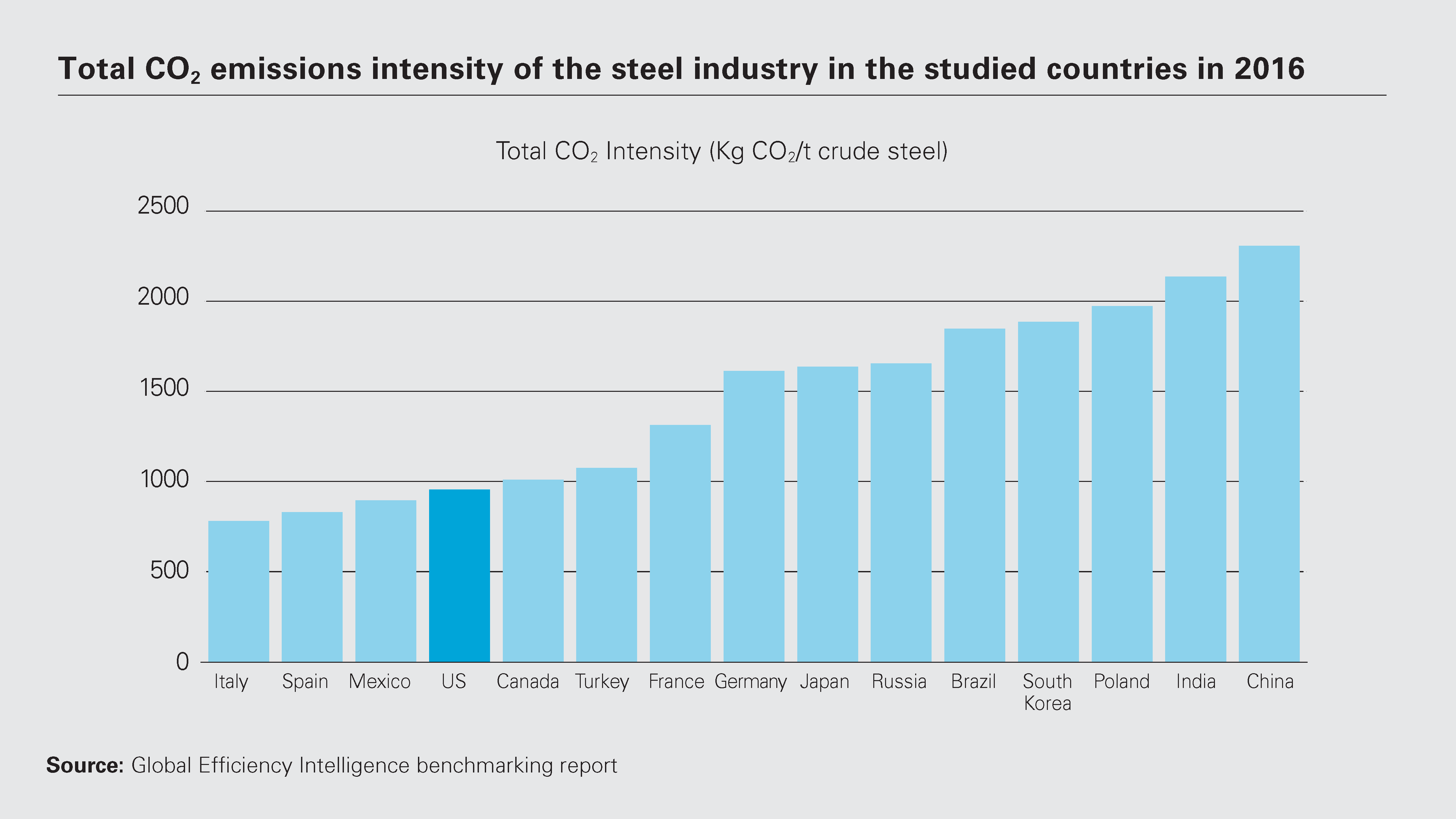

In the steel industry, Russia, China and India are likely to face the greatest adverse impacts from the CBAM, as they are among the largest exporters to the EU of the covered products, lack a national carbon price and have relatively emissions-intensive production practices. Turkish and US producers could see smaller impacts due to their lower carbon footprints.

In the aluminum industry, EU producers expect that the existence of low-carbon production in major exporting countries, namely China and Russia, will greatly limit the CBAM's impact. They expect the CBAM will encourage "resource shuffling," where these countries redirect their low-carbon aluminum products to the EU market and send higher-carbon products elsewhere, with little overall impact on carbon and investment leakage.

The Commission has indicated that it will consider expanding the CBAM's scope to include "more products and services" as well as "indirect emissions" generated through the electricity, heating and cooling used during the production process.

Future expansions of the CBAM's scope could cover copper and zinc production, which the Commission has previously identified as at risk of carbon leakage, as well as production of nickel and silicon, all of which are electro-intensive.

Representatives of these industries have expressed concern that the CBAM as designed would disadvantage European producers regardless of their carbon footprint, as it would not fully account for the costs that even low-carbon producers face as a result of Europe's marginal pricing system for electricity.

The Commission has said it believes the proposed CBAM is fully compliant with World Trade Organization (WTO) rules, but this claim is likely to be closely studied by adversely affected trading partners. Initial estimates suggest that its effects on trade flows from highly exposed countries such as Russia could be significant, potentially generating political pressure for retaliatory actions. Some governments have already accused the EU of developing the CBAM with protectionist intent.

The effects of the CBAM on the US are expected to be modest, as it is a relatively small exporter of the covered products to the EU and the emissions intensity of the US steel sector is comparable to that of the EU.

Although the Biden administration has expressed some reservations about the CBAM, it recognizes that governments seeking to limit emissions have a "legitimate interest" in preventing carbon leakage, and has made clear that it intends to impose fees on carbon-intensive imports as it ramps up domestic regulation of carbon emissions.

July 14 2021

In the US, the budget plan unveiled by Senate Democrats on July 14 envisions a new "polluter import fee" alongside domestic regulations to reduce emissions

The US approach

Proposals to establish a domestic price on carbon emissions face significant opposition in the US Congress, and this is a key factor in the current US policy debate on climate change and carbon border adjustments. Given this obstacle, the Biden administration has not proposed a domestic carbon price, and instead has prioritized regulatory approaches to reduce emissions.

At the same time, the administration has continued to express support for carbon border adjustments, prompting speculation that it may pursue a border adjustment that is not linked to a domestic carbon price. There could be an attempt to quantify the compliance burden that US manufacturers in specific sectors face as a result of non-price policies that constrain carbon emissions, and then assigning an equivalent fee to imports.

A border adjustment based on regulatory costs could prove even more controversial than the CBAM, particularly given the difficulty of reliably quantifying such costs. However, this approach appears to be gaining momentum.

On July 19, 2021, Democratic Senator Chris Coons and Representative Scott Peters introduced legislation—reportedly developed in consultation with the US Trade Representative—that would impose a carbon fee on imports of iron, steel, aluminum, cement and fossil fuels, and would base the amount of the fee on the costs that domestic producers incur to comply with any national or local law, regulation or program designed to reduce emissions.

The budget plan unveiled by Senate Democrats on July 14 appears to endorse this approach, as it envisions a new "polluter import fee" alongside domestic regulations to reduce emissions, but does not propose a domestic carbon price.

Senators supportive of these efforts have characterized them as necessary to protect the US manufacturing sector from foreign competition, particularly with China, which may fuel perceptions that the policy is motivated at least in part by protectionist goals.

In addition to carbon border adjustments, US policymakers are increasingly seeking to incorporate climate objectives into US trade laws and agreements in ways that may exacerbate trade tensions. In June, the Biden administration said it was considering whether the Paris Agreement on climate change should be added to the list of environmental agreements enforceable through the US-Mexico-Canada Agreement.

This demand is likely to resurface in future US trade negotiations, and could lead to sanctions if a country fails to uphold its Paris commitments. The US has also tried to incorporate environmental concerns more squarely into the trade remedies regime, of which the metals sector is a major user, by proposing changes to WTO rules that would make a government's failure to enforce environmental laws an actionable subsidy subject to countervailing duties.

The UK will host the 26th UN Climate Change Conference of the Parties (COP26) in Glasgow October 31 to November 12 2021

Outlook

Whatever their environmental merits, the recent policy proposals from the US and the EU have the potential to disrupt trade flows and generate trade disputes if implemented. This is clear from initial reactions to the CBAM, which Brazil, South Africa, India and China have criticized as a "discriminatory" trade barrier that deviates from the principle of "common but differentiated responsibilities" enshrined in the UN Framework Convention on Climate Change.

China has alleged that the CBAM violates WTO rules. Adversely affected countries may challenge climate-related trade measures through WTO or free trade agreement dispute settlement mechanisms, and could obtain the right to impose retaliatory tariffs if the measures are found to be inconsistent with trade rules. Such measures often target politically sensitive goods that are unrelated to the underlying dispute, such as agricultural products.

Governments might also retaliate in less overt ways, for example by initiating antidumping or countervailing duty investigations of politically sensitive exports from countries that adopt climate-related trade measures.

Frictions over climate-related trade measures are likely to be most pronounced between developed and developing countries. However, tensions might emerge even among developed economies that share similar levels of ambition on climate change, given potential differences in approach and implementation.

Recognizing these potential trade frictions, some leaders have suggested a multilateral agreement for a global minimum price on carbon emissions, which could make unilateral border adjustment unnecessary. However, the prospects for such an agreement currently appear poor.

The proliferation of unilateral border adjustment measures also threatens to reignite longstanding tensions in broader multilateral negotiations on climate change. Developing countries have long sought to pre-empt such measures, most notably at the 18th UN Climate Change Conference (COP18) in 2012, when they unsuccessfully sought a commitment from developed countries not to resort to unilateral measures against developing countries on climate-change-related grounds.

Now, major developing countries plan to reiterate their opposition to carbon border adjustments this November at COP26 in Glasgow. Environmental advocates have warned that tensions over this issue will make it more difficult to secure the ambitious climate pledges that large developed countries are being asked to undertake at COP26.

Complicating matters, climate negotiators have historically been reluctant to discuss whether and to what extent trade restrictions might constitute appropriate climate response measures, due in part to uncertainty as to whose jurisdiction this issue falls within.

Unless this jurisdictional issue is resolved, it appears increasingly likely that decisions regarding the permissibility of specific climate-related trade measures will be left to the WTO's dispute settlement system—potentially placing the WTO on a collision course with the climate agenda.

In a best-case scenario, COP26 might produce a consensus on the proper forum for countries to deliberate the appropriateness of climate-related trade restrictions, and how these can be squared with the core WTO principles of trade liberalization and non-discrimination.

Nevertheless, it appears doubtful that governments seeking to impose carbon border adjustments will put their plans on hold while multilateral negotiations take place. Businesses should begin preparing for trade disruptions as governments resort to unilateral action to address the issue.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: 20 most-exposed countries in terms of aggregated value of exports (billion US$) (PDF)

View full image: 20 most-exposed countries in terms of aggregated value of exports (billion US$) (PDF)

View full image: Total CO2 emissions intensity of the steel industry in the studied countries in 2016 (PDF)

View full image: Total CO2 emissions intensity of the steel industry in the studied countries in 2016 (PDF)