As has been the case across all European jurisdictions, elevated interest rates have taken a heavy toll on German debt markets over the past year.

A series of rate hikes by the ECB, which pushed up base rates to the highest levels observed in more than two decades, have hindered syndicated loan and high yield bond issuance across the continent, with the German market being no exception.

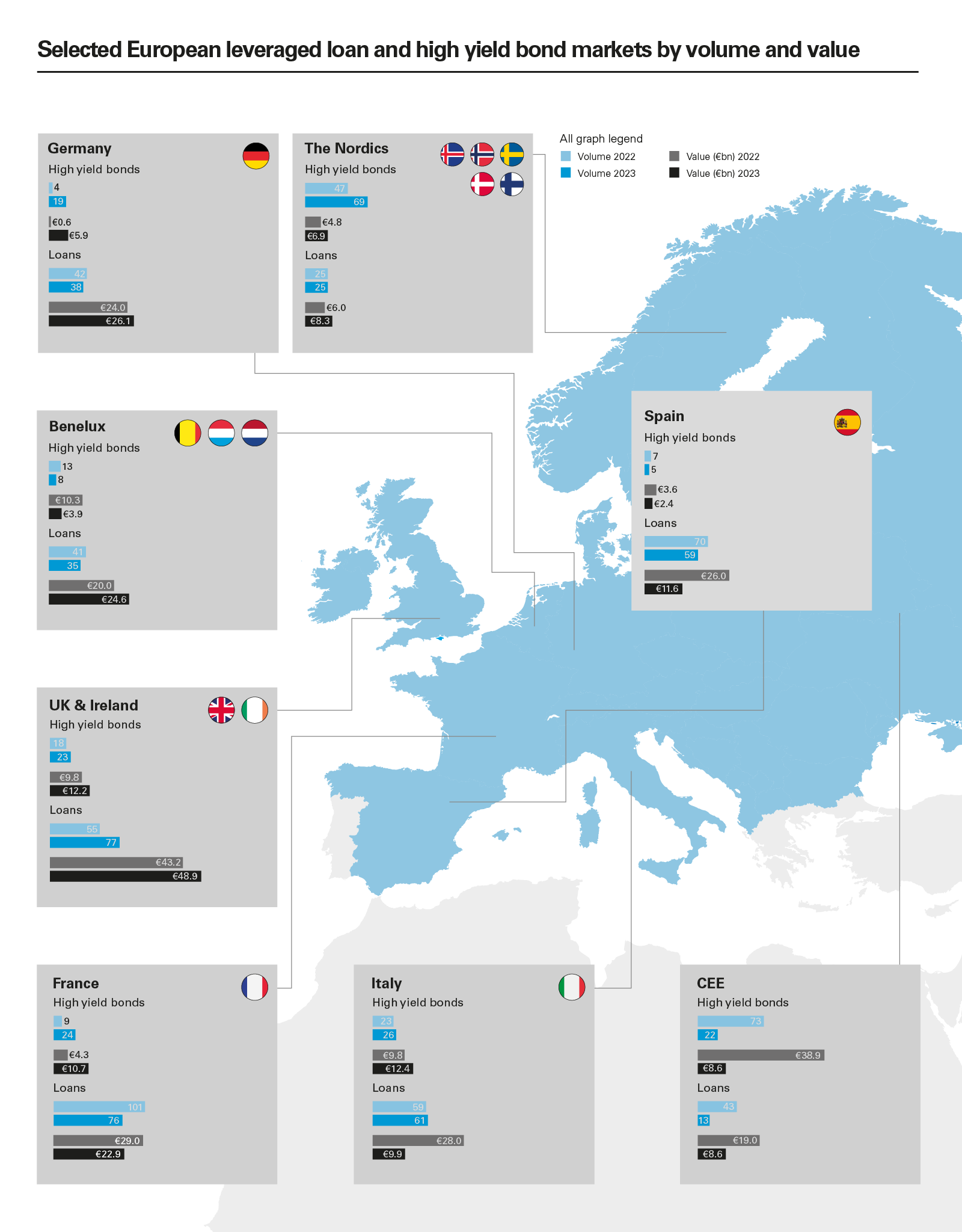

According to Debtwire Par data, syndicated leveraged loan issuance in Germany rose by 10 per cent year-on-year in 2023 to US$28.1 billion. High yield markets fared better, with issuance rising from just US$612 million in 2022 to US$6.5 billion in 2023. In 2022, however, German high yield issuance was the weakest on record since 2015, making for flattering comparisons. When compared to other years, high yield activity in 2023 has underwhelmed.

In a challenging market, refinancing has been the dominant driver of what issuance has proceeded. Refinancing accounted for 42 per cent of all syndicated loan issuance in 2023 and 35 per cent of high yield bond issuance. Financing for buyouts, by contrast, has been limited. High yield buyout financing reached just US$484 million in 2023, while loan financing for buyouts reached US$2.4 billion, accounting for less than 8 per cent of overall syndicated loan issuance.

Growth pains

German syndicated loan and high yield bond activity has been blunted not only by higher interest rates, but also by anaemic GDP growth.

Germany’s economy stagnated in 2023, shrinking by 0.4 per cent, according to forecasts from the ifo Institute for Economic Research. The International Monetary Fund has forecast another difficult year for the German economy in 2024, with growth expected to lag behind the US, UK, France and Spain.

Germany’s economy was impacted markedly by Russia’s invasion of Ukraine in February 2022. Subsequent spikes in energy costs hit the country especially hard, as Germany’s industrial sector uses almost twice as much energy as the next biggest industrial sector in Europe, according to The Economist. Meanwhile Germany’s exports to China—for years one of the single biggest export markets for German manufacturers—declined by 8 per cent in 2023, according to BNP Paribas, as China continued to invest in more local production to replace imports.

Higher cost bases resulting from rising energy prices, coupled with soft exports and weak GDP growth, have squeezed company EBITDA figures. Add in higher borrowing costs, and securing new financing packages has become close to unaffordable for many companies.

Financing markets have also been impacted by distress in the German real estate sector. After a period of consolidation in German real estate, funded by loans and bonds issued at low rates, climbing debt servicing costs and corrections in property valuations have left real estate companies with high debt burdens and mushrooming financing costs. According to Savills, this has seen German real estate transactions fall to their lowest levels since 2014 on a 12-month rolling basis.

A number of high-profile developers, including Gerch, Euroboden and Project Immobilien Group, have borne the brunt of the dislocation. There have been significant knock-on effects in the adjacent construction and infrastructure sectors, where financing markets have all but shut as lenders step back from any assets exposed to real estate risk.

Adapting to change

In the face of these headwinds, borrowers have responded by either holding out as long as possible before refinancing, in the hope that fundamentals improve, or making add-on acquisitions of smaller assets with high EBITDA in an effort to boost earnings and build headroom into capital structures.

As mainstream loan (i.e., TLBs) and bond issuance has declined, however, the German market has proved relatively flexible, with other lender groups stepping in to fill financing gaps.

Direct lenders have remained open for business, although on a selective basis. Borrowers have also noted the reappearance of bank club deals, which have accounted for an increasing proportion of acquisition finance in the mid-market. This reflects how companies and sponsors have relied on their relationship banks, as well as the fact that bank clubs have been able to provide capital at lower cost when compared with direct lending and the capital market alternatives of TLBs and bond issuance.

Direct lenders were able to offer more leverage at the peak of the market on deals than banks, and with base rates low, the cost of this debt was manageable. As base rates have climbed, however, taking on additional turns of leverage has become less appealing, and the lower-cost lower-leverage structures offered by bank clubs have moved back into the frame.

German mid-market financial sponsors have also benefitted from increasing appetite from the country’s regional savings banks or Sparkasse (which have traditionally focused on serving households and local businesses) to do buyout financings. According to Bloomberg, Kreissparkasse Biberach and Sparkasse KölnBonn are among the regional savings banks that have picked up business from larger peers that scaled back their leveraged finance teams.

Brighter prospects

Although bank clubs and increased activity from Sparkasse have helped to provide new pools of financing in tough conditions, companies and sponsors will nevertheless be hoping that mainstream loan and bond markets rebound quickly.

Hopes that interest rates have peaked, as well as the very healthy refinancing pipeline, have already given stakeholders a degree of optimism that German leveraged loan and high yield bond issuance will recover in 2024.

Credits in favourable, non-cyclical sectors, such as pharmaceuticals, B2B technology and travel (which is still benefitting from a post-lockdown boost), will be particularly well-placed. Advisers are also reporting an increase in work related to preparing prospectuses and due diligence ahead of potential bond issuance in Q1 2024.

Borrowers will also be encouraged by expectations of a rebound in the Schuldschein market (privately placed, unsecured debt instruments governed by German law). According to a Bloomberg survey of Schuldschein arrangers, roughly two-thirds expect issuance to climb by as much as 10 per cent in 2024, with refinancing driving the upturn.

The German market is not out of the woods yet, and more insolvencies and restructurings are anticipated in 2024 as issuers come up against maturity walls, but after a bumpy 2023, welcome signs of a market recovery are finally emerging.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2024 White & Case LLP

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)