European leveraged finance in 2023 was saddled with the negative effects of elevated interest rates. But as the market adjusts to the "new normal", rate and price stability offer hope for a brighter 2024.

European leveraged finance overview

Rising interest rates have pushed up borrowing costs and constrained issuance activity

Subdued M&A pipeline and cautious underwriting by banks limit buyout financing opportunities

Where transactions have progressed, the bulk of activity has been propelled by refinancing deals

Private credit proves resilient in the face of wider dislocation, attracting banks into the segment

Jumbo Worldpay financing shows that investor appetite for high-quality credits remains strong, with a potential warming for backdrop in 2024

After a slow year, market behaviour will mimic certain human traits, which will act as drivers in leveraged finance markets in 2024, as lenders and borrowers look to increase activity levels

Restlessness, imitation, creativity, distraction and optimism will, in their own way, each propel market participant activity levels

More banks may move to build out their private debt capabilities, imitating the successful private debt model that demonstrated its resilience through the current cycle

In a flat market, creativity will see lenders repurpose existing funding sources and develop new products to unlock liquidity

Among alternative assets, private debt has matured rapidly and is enjoying a 'golden moment' as a markedly attractive floating-rate product

In 2024, a mounting interest burden will give rise to novel debt structures for LBOs

As a typical credit is held by a single lender or small club, the private debt model enables providers to move more quickly than their peers

Not wishing to miss this golden opportunity, investment banks are quickly establishing or building up their private debt desks, introducing another valuable option to the funding mix

After a challenging period for sponsor deal activity and limited access to finance, the outlook for the year ahead is improving

Expectations of interest rate stability are raising hopes that pricing and modelling capital structures will be easier and allow gaps in pricing expectations between buyers and sellers to narrow

High levels of dry powder and unexited assets will put structural pressure on managers to do deals, improving prospects for deal financing pipelines

Private debt has gained market share and will remain a key part of the acquisition finance mix, but loan and bond markets are rallying, providing sponsors with a wider set of financing options

Among alternative assets, private debt has matured rapidly and is enjoying a 'golden moment' as a markedly attractive floating-rate product

In 2024, a mounting interest burden will give rise to novel debt structures for LBOs

As a typical credit is held by a single lender or small club, the private debt model enables providers to move more quickly than their peers

Not wishing to miss this golden opportunity, investment banks are quickly establishing or building up their private debt desks, introducing another valuable option to the funding mix

Private debt has been one of the most resilient asset classes through the current cycle of rising interest rates. Portfolios have performed well and returns have been excellent. Investor appetite for private debt strategies is strong and managers in the space have continued to grow market share.

But how has the private debt model been able to navigate market headwinds so well? How will managers react if portfolios do start to come under pressure and what will happen when syndicated loan and high yield bond markets rally?

In this Q&A explainer, we provide an overview of what has been driving the private debt space and what lies ahead for the asset class in 2024 and beyond.

How has private debt as an asset class come through the rising interest rate cycle?

Private credit is booming as an asset class. It is probably the great story of alternative assets in the current market. People are calling it a golden moment. Some of the biggest private markets platforms in the world now have more dry powder in private debt than in private equity.

Across the investment market, private credit is now a primary source of finance, and not just in the mid-market, as it used to be, but all the way up to large-cap deals. Not every large-cap deal can be financed in private credit, but you can get well north of €1 billion. There are lots and lots of providers in the market, and they now club together regularly.

This means a sponsor can raise an awful lot of money in the private markets without taking flex risk.

What have rising interest rates meant for private credit funds? Have the criteria to finance a deal changed?

There have been been fewer deals this year than there were in, say, 2021, but that has to be placed in context. Remember that 2021 was the most active year since the global financial crisis in 2008, so it is not too surprising that deal volumes have come down.

High interest rates will affect the way M&A acquirers think about deals, and it has had an impact on the number of deals.

That said, everyone is really busy right now, and has been throughout the second half of 2023. There has been plenty of deal flow. The deals that do happen get done in the private markets.

What will be interesting, as we move into 2024, will be how sponsors and private lenders go about setting up an LBO model for good companies with cash flows that don't support high cash-pay leverage multiples.

Everyone is really busy right now, and has been throughout the second half of 2023. There has been plenty of deal flow. The deals that do happen get done in the private markets. What will be interesting, as we move into 2024, will be how sponsors and private lenders go about setting up an LBO model for good companies with cash flows that don’t support high cash-pay leverage multiples.

These companies will have to meet a higher, ongoing interest burden, and the challenge will be how to structure satisfactory interest cover. It is difficult to do that with six turns of leverage priced at SONIA plus a margin of 5.5 per cent.

Does that mean we will see more deals done at lower leverage? Will sponsors make more use of payment-in-kind (PIK) debt to help them push leverage up, or will the cost of PIK debt erode equity returns too quickly?

It is going to be very interesting to see how dealmakers get transactions done next year and what debt structures they use.

Has there been any sense of a shift from new money deals to doing more working capital and add-on acquisition financing for existing portfolios?

There was a high volume of add-on acquisitions in the first half of 2023, which ran in tandem with a shortage of new LBO activity in the first half of the year. In the second half of the year, however, particularly in Q4 2023, it felt like the market was back to its normal run rate. There has been a constant flow of LBOs in recent weeks.

What movement has there been with respect to financing terms and credit selection from sponsors?

The market is mature now. People used to talk about private debt as an alternative funding source, but don't anymore. It is now the default way of financing a buyout at all but the very largest sizes.

What the market has taken on-board as it has matured is that you can't turn a bad business into a good business with tight legal documents. Private debt managers are focussed on quality assets backed by quality sponsors. The right deals will get the right terms.

What about pricing? How are managers pricing risk, especially given the volatility on pricing in syndicated loan and high yield bond markets?

Funds set their unitranche pricing to deliver the right returns for their investors, but also have to factor in that they are operating in a competitive environment. What that all means is that pricing isn't determined by what is going on in syndicated debt markets. It is drawn from what they can get in the market and what returns they are required to deliver for investors.

How are private debt returns shaping up?

In short, very well. Private credit offers a very attractive floating-rate product. If you are an investor in a private fund at the moment, you could yield approximately 10 per cent on senior secured risk. It is quite remarkable.

How have private debt portfolios held up through the cycle? How are private debt managers responding to stress in portfolios?

There have been examples of stress and distress in some portfolios, but no more than you would expect. There is no difference in default risk between private credit and syndicated loans and bonds, and private credit default risk is not any higher than the long-term average. Portfolios have been stable and we are not anywhere near the default levels of 5 to 6 per cent you see in really bad periods for the market.

In terms of how managers are responding when there is a stressed or distressed credit, the approach will vary from manager to manager, but on the whole managers have been quite supportive, negotiating amend-and-extends and even putting in additional capital for liquidity when necessary.

What makes the private debt model so effective is that a credit is held by a single lender or a small club. It means private debt providers can move quickly and decisively.

You don't need to form a committee. You don't have to worry about trying to corral 50 to 60 per cent of lenders. You don't have institutions in the debt that can't make decisions because they are mandated to be passive. You have lenders that can think quickly and make decisions quickly, and they don't have layers and layers of approvals they need to go through.

Private debt managers will behave in different ways in distressed situations, but the one thing they have in common is that they can all make decisions very fast, and they can all move. The people who did the deal at the front are often still involved. The sponsor is usually still interfacing with the people they always deal with, and that person is often empowered to speak for the firm. It is an invaluable point of distinction.

To what extent are bank-led and private credit financings converging? What does this mean for the private credit model?

Banks have noted the success of private debt, so have naturally wanted to move into that part of the market. We have the leading investment banks establishing private credit desks, and they will no doubt be very successful as they have access to different sources of capital. It adds another option into the funding mix.

What has been interesting to observe is the emergence of the first private debt "CLOs"—where managers are packaging up their loans and then selling tranches of these loans to investors according to their risk. The one nuance is that in a traditional CLO, the equity tranche will be sold, but in a private debt structure the manager will often retain the equity tranche.

We have seen the first of these CLOs in the US. There hasn't been one in Europe yet, but people are certainly thinking about it. The challenge is size. You must have a very big portfolio to be able to do this, so currently it is realistically only an option for a limited group of managers.

The main point is that these CLO structures create a distributable private debt product for the first time. It is going to be very interesting to see how these structures continue to develop in the year ahead.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

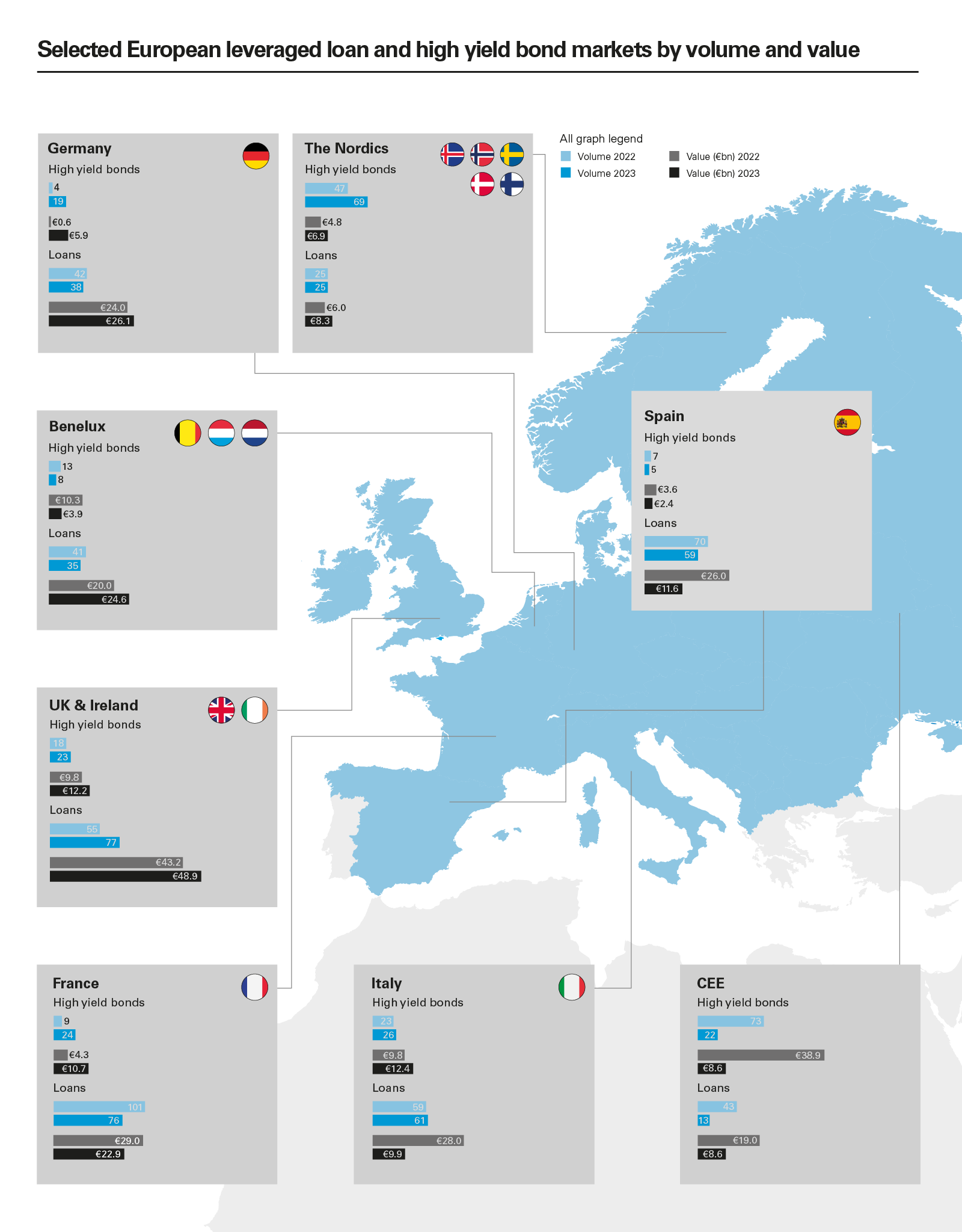

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)