European leveraged finance: Competition sets the pace

What's inside

Rival market dynamics between lenders drives innovation and competition across Europe's leveraged finance markets, opening new doors to sponsors as transaction activity accelerates

Market dynamics reshape borrower choices

Competition between lending channels intensified in 2025, as leveraged finance markets in Europe saw lenders vying for deals and offering borrowers greater flexibility ahead of an anticipated surge in activity in 2026

In Europe, the traditional boundaries between broadly syndicated loans (BSLs), high yield bonds and private credit have become less distinct. Competition for deals intensified throughout 2025, reshaping the landscape for sponsors and issuers.

Refinancing dominated European lending activity, accounting for the overwhelming majority of issuance. But this was far from a defensive manoeuvre. Instead, issuers used the window strategically—extending maturities, embedding portability features and optimising capital structures in anticipation of the improved exit opportunities that dealmakers expect to emerge in 2026.

Private credit players compressed margins below 5 per cent to compete with BSL financing, and increasingly deployed covenant-lite structures. Meanwhile, BSL lenders cut fees and increased flexibility to retain market share. The result has been an environment in which sponsors can have real optionality between channels based on execution speed, pricing and structural requirements. This competitive dynamic has been underpinned by abundant capital. Private credit fundraising remained robust, CLO formation stayed active and insurance capital continued flowing into the asset class.

The pressure to deliver exits has clearly intensified. Private equity holding periods have reached record highs, as managers waited for market conditions to improve. While dividend recaps, NAV loans and secondary market transactions provided some relief, institutional investors are demanding orthodox exits and capital distributions. The refinancing activity in 2025 has positioned portfolio companies to capitalise on an expected near-term increase in M&A and exit activity.

Europe's leveraged finance market entered 2026 not merely open for business but optimised for it. Lenders are well capitalised, competition is fierce and issuers have used the past 12 months to put themselves in a position of maximum preparedness. If the anticipated rebound in dealmaking materialises, the lending market is more than ready to support it.

European issuers optimise debt facilities as exit window opens

European leveraged finance markets steered through a volatile year to provide borrowers with a consistent source of liquidity at attractive prices

With M&A still intermittent, refinancing activity accounted for the bulk of issuance

Refinancing took on a broader strategic context, as issuers lay the groundwork for exit opportunities expected to emerge in 2026

Leveraged finance providers enter the new year well capitalised and ready to finance a new cycle of transaction flow

European issuers optimise debt facilities as exit window opens

Insight

|

6 min read

Headlines

European leveraged finance markets steered through a volatile year to provide borrowers with a consistent source of liquidity at attractive prices

With M&A still intermittent, refinancing activity accounted for the bulk of issuance

Refinancing took on a broader strategic context, as issuers lay the groundwork for exit opportunities expected to emerge in 2026

Leveraged finance providers enter the new year well capitalised and ready to finance a new cycle of transaction flow

Europe's leveraged finance markets have given issuers sufficient space to navigate macroeconomic headwinds and prepare for an increase in deals in 2026.

Through periods of uncertainty, the system has slowed but not stalled. Defaults have been benign, sector-specific challenges have not deepened, and issuance across BSL, high yield and private credit markets has been strong. This has afforded lenders the opportunity to lay the foundation for exit opportunities in the coming 12 to 18 months.

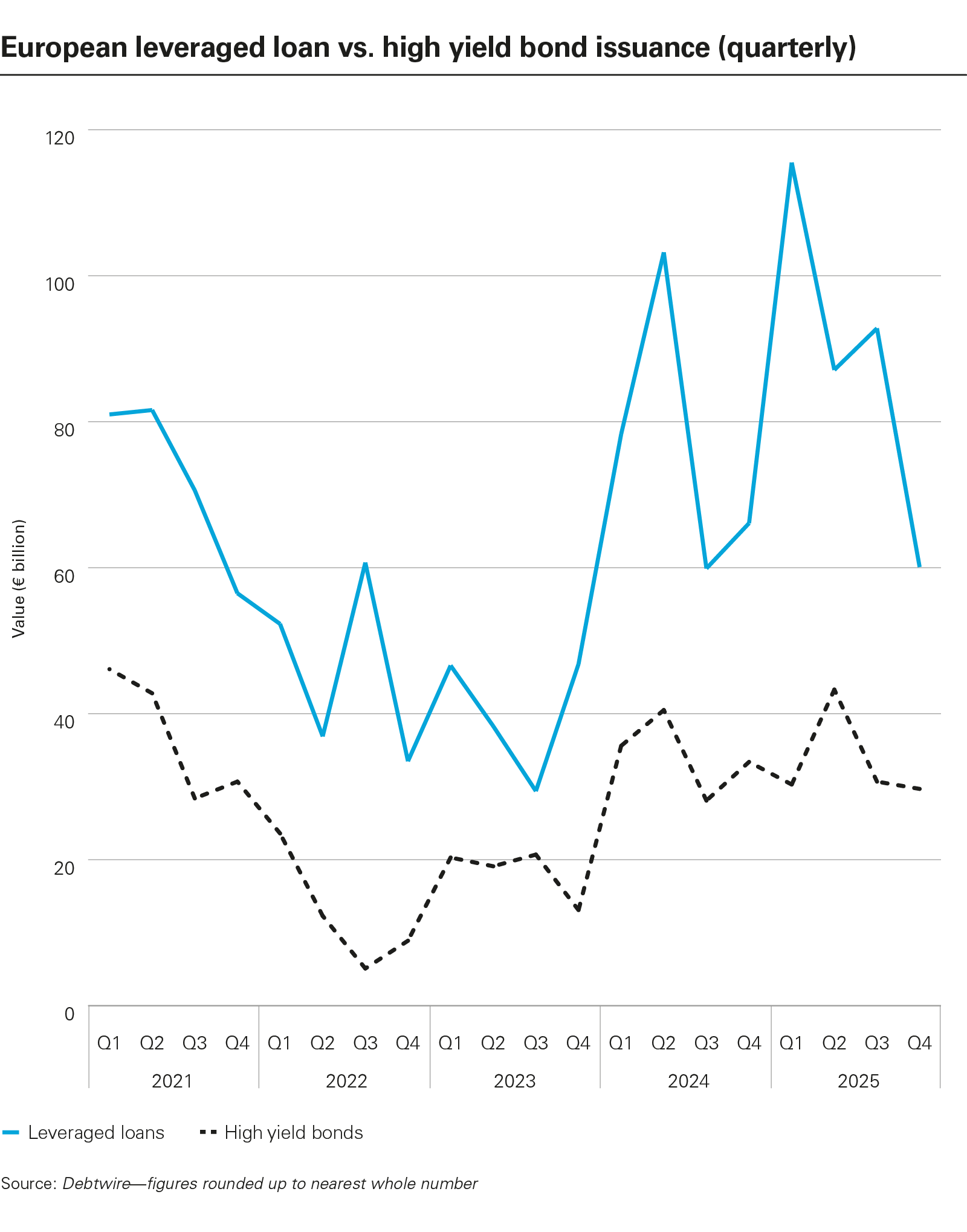

In 2025, European leveraged loan issuance posted year-on-year gains of 15.6 per cent, totalling €355.6 billion. High yield activity reached €134 billion over the same time period, falling marginally, by 2.7 per cent, from 2024 levels. Direct lending issuance reached €84.9 billion from Q1 to Q3 2025, up 14 per cent compared to the same period the year prior.

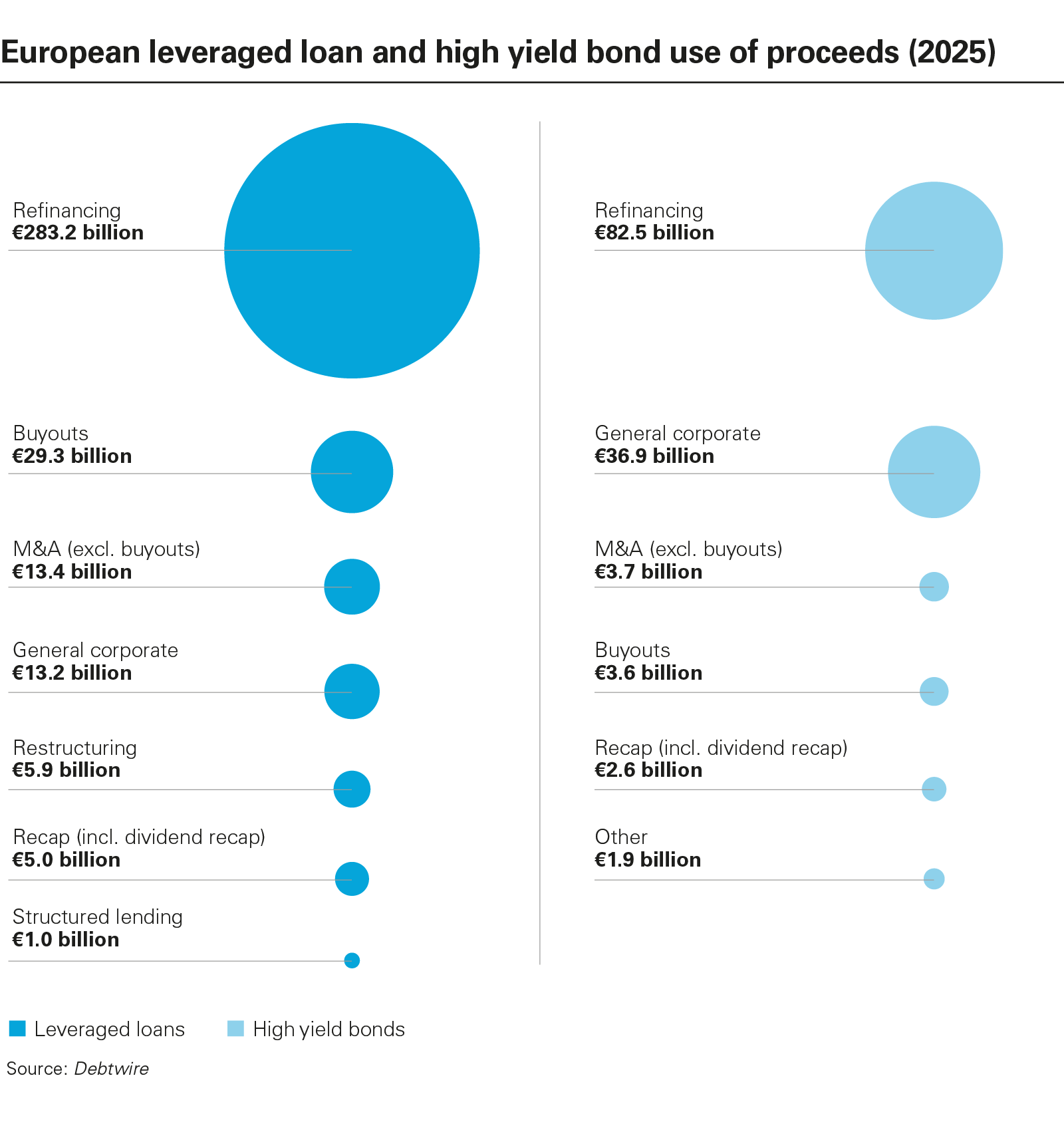

Across all markets, issuance has been dominated by refinancing. Leveraged loan and high yield issuance for refinancing, repricing and amendments reached €283.2 billion and €82.5 billion, respectively, through 2025. This represented almost 80 per cent of all leveraged loan activity and more than 60 per cent of high yield issuance. In the direct lending arena, refinancing accounted for approximately 45 per cent of overall proceeds between Q1 and Q3 2025.

Absent a full recovery in M&A activity and new money transactions, issuers took advantage of liquidity in leveraged finance markets to refinance and reprice borrowing costs at lower margins.

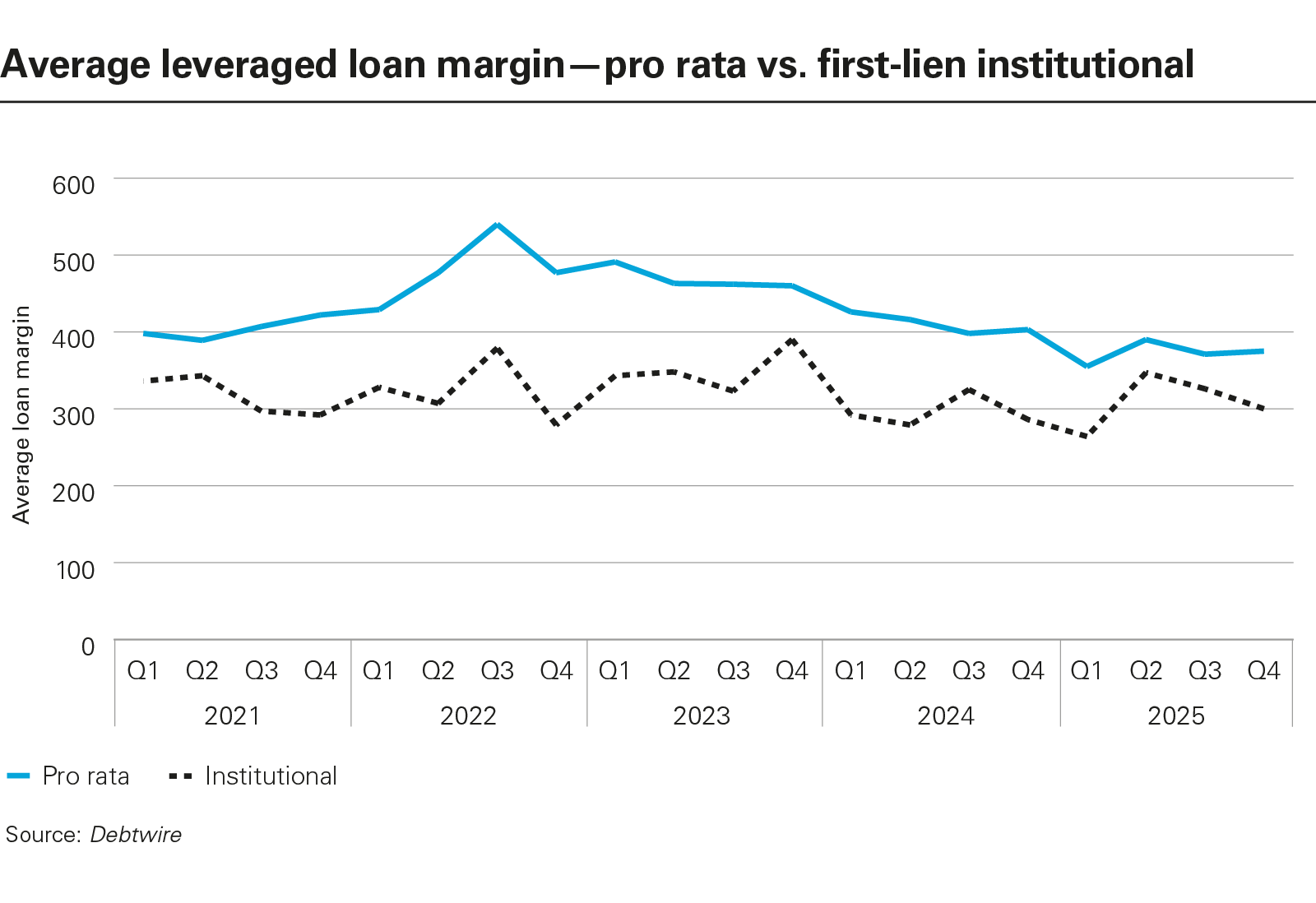

In the leveraged loan space, margins on first-lien institutional loans came in at 3.75 per cent in Q4 2025, according to Debtwire. Meanwhile, direct lending margins averaged 6.59 per cent by the end of Q3, as certain borrowers secured some of the lowest financing costs observed in the history of Europe's private debt market.

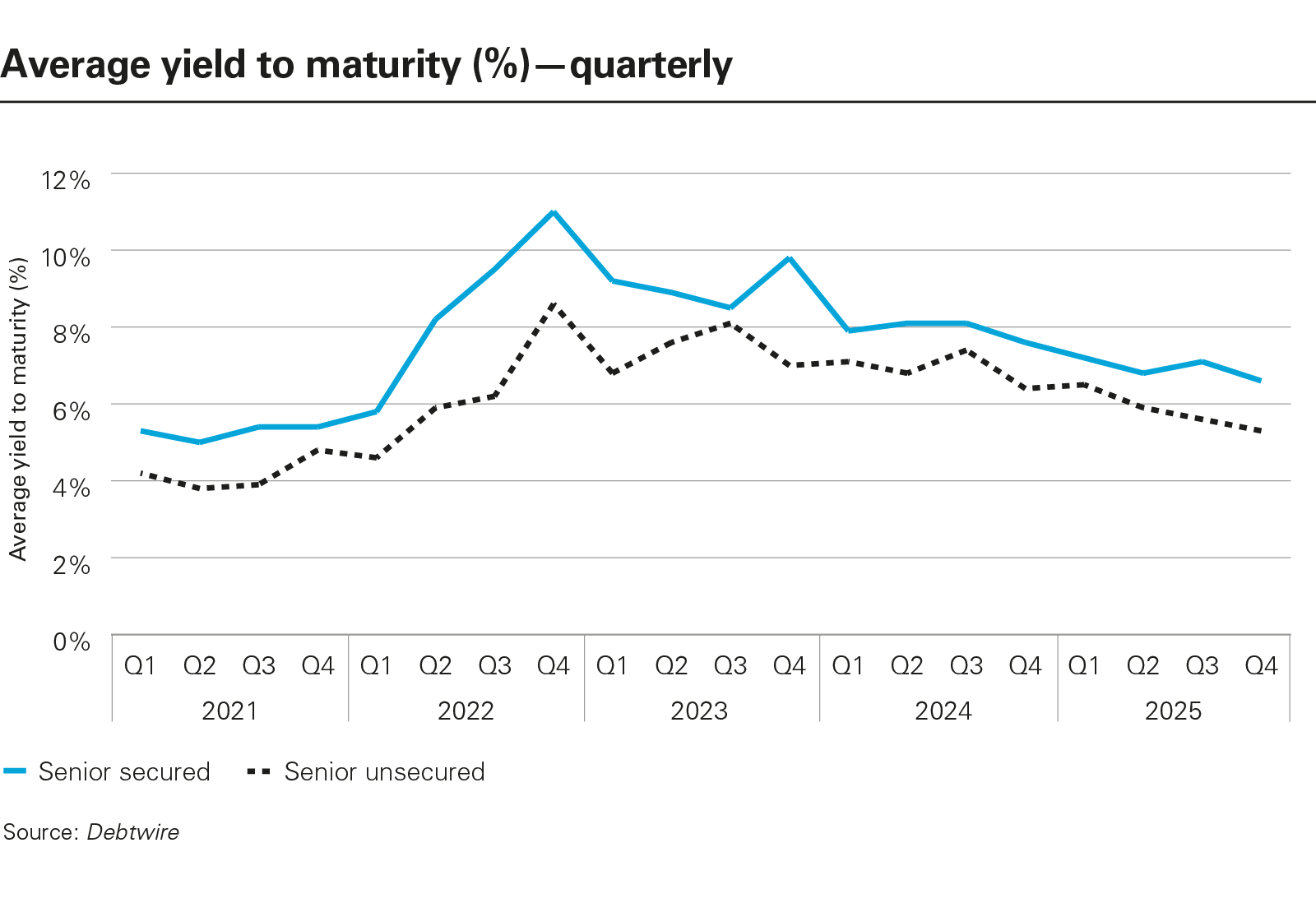

For high yield bonds, average yields to maturity for senior secured loans narrowed to 6.58 per cent by December 2025, and to 5.34 per cent for senior unsecured loans. Both figures are the lowest levels recorded since Q1 2022, reflecting price normalisation as issuer costs and investor risk-return expectations began to converge.

Besides lowering debt servicing costs, the refinancing window also afforded dealmakers the opportunity to extend maturities in loan and bond markets.

Crucially, this was not a short-sighted, opportunistic play to defer maturity walls, but a strategic step by issuers to establish a solid foundation in anticipation of credible medium-term exit and liquidity events in 2026.

Issuers, lenders and dealmakers had hoped that 2025 would be the year that M&A markets reopened—but tariff-related disruption in Q2 2025 put the M&A rebound on hold. However, there are signs that 2026 could finally be the year that European M&A markets truly bounce back.

Issuers, lenders and dealmakers had hoped that 2025 would be the year that M&A markets reopened— but tariff-related disruption in Q2 2025 put the M&A rebound on hold.

In Q3 2025, Europe posted its best quarter for aggregate M&A deal value in more than three years, though momentum did cool in Q4. Nevertheless, bankers anticipate that the ramp-up in global M&A observed through 2025 (up 41 per cent year-on-year) could herald a record year for deal activity in 2026.

For private equity managers, 2026 could mark a turning point, as the structural imperative to exit portfolio companies, make LP distributions and free up liquidity for the next vintage of fundraising continues to intensify. Median private equity holding periods have climbed to 5.8 years, the highest level recorded by data company Private Equity Info.

Holds have stretched as buyout firms have opted to wait out the market dip before divesting assets. Managers have been able to ease liquidity constraints through dividend recaps, secondary markets, NAV loans and minority deals. But demand is building among investors for dealmakers to deliver orthodox exits.

It is against this backdrop that issuers have been able to take advantage of the willingness of the leveraged finance ecosystem to accommodate equity injections, maturity extensions and refinancings. With an exit window emerging, issuers are trying to buy a little extra time to refine their asset-exit positions.

For example, refinancings across BSL and private credit markets frequently incorporated portability terms in 2025. These enabled vendors to sell companies without having to raise new debt, which in the months to come could simplify the deal financing process for potential bidders.

The flexibility and liquidity of the high yield bond market have proven particularly valuable in this context, offering covenant-lite packages. These could benefit future owners and dovetail with the alternative exit routes that issuers have used to retain prized assets for longer.

For instance, the high yield market has been able to accommodate the rising volumes of continuation-vehicle deals (where sponsors roll portfolio companies out of an existing fund into a new vehicle) relatively easily, as portability features are standard in high yield terms.

A similar focus on flexibility has also propelled the growth of the Nordic high yield space. This distinct fixed income market first emerged in the late 1990s to finance the Norwegian oil industry, but has since grown into a popular financing option for issuers from a wide range of countries and sectors. With appetite to underwrite smaller deals, provide long-term maturities and offer less-stringent reporting obligations, Nordic bond issuance climbed to record levels in 2025, with issuers refinancing into Nordic bonds to put portfolio company capital structures in prime position for transactions.

Optimisation rather than maintenance

Europe's leveraged finance markets are primed for growth in 2026, fuelled by fresh liquidity and greater resilience.

Refinancing and maturity extensions have been the main drivers of issuance, but this activity has not been propelled by a "maintenance mode" mentality. Instead, issuers are adopting a forward-looking mindset, preparing themselves for a more favourable exit environment in 2026.

Lenders themselves are ready to support increasing deal flow. Liquidity is abundant thanks to strong private credit fundraising and active CLO formation. Capital pools will deepen further as the flows of insurance and retail cash moving into private credit increase.

Private credit firms are building up their own insurance divisions in response to growing demand from insurers for private credit exposure. Further inflows into private credit are expected from non-institutional investors, as evidenced by the growth of "evergreen" funds, which offer individual investors a pathway for building their exposure to private assets.

These capital inflows will not only encourage ongoing activity in the sectors where there has been a heavy focus in recent years—such as software, business services and healthcare—but other overlooked industries such as defence, where a funding gap has emerged as European governments move to increase security investments.

BSL, high yield and private debt lenders have provided issuers with the capital and flexibility to begin 2026 in a state of maximum readiness, and now stand prepared to support the next cycle of dealmaking and investment as transaction markets turn a corner.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: European leveraged loan vs. high yield bond issuance (quarterly) (PDF)

View full image: European leveraged loan vs. high yield bond issuance (quarterly) (PDF)

View full image: Average leveraged loan margin—pro rata vs. first-lien institutional (PDF)

View full image: Average leveraged loan margin—pro rata vs. first-lien institutional (PDF)

View full image: Average yield to maturity (%)—quarterly (PDF)

View full image: Average yield to maturity (%)—quarterly (PDF)

View full image: European leveraged loan and high yield bond use of proceeds (2025) (PDF)

View full image: European leveraged loan and high yield bond use of proceeds (2025) (PDF)