European leveraged finance: Competition sets the pace

What's inside

Rival market dynamics between lenders drives innovation and competition across Europe's leveraged finance markets, opening new doors to sponsors as transaction activity accelerates

Market dynamics reshape borrower choices

Competition between lending channels intensified in 2025, as leveraged finance markets in Europe saw lenders vying for deals and offering borrowers greater flexibility ahead of an anticipated surge in activity in 2026

In Europe, the traditional boundaries between broadly syndicated loans (BSLs), high yield bonds and private credit have become less distinct. Competition for deals intensified throughout 2025, reshaping the landscape for sponsors and issuers.

Refinancing dominated European lending activity, accounting for the overwhelming majority of issuance. But this was far from a defensive manoeuvre. Instead, issuers used the window strategically—extending maturities, embedding portability features and optimising capital structures in anticipation of the improved exit opportunities that dealmakers expect to emerge in 2026.

Private credit players compressed margins below 5 per cent to compete with BSL financing, and increasingly deployed covenant-lite structures. Meanwhile, BSL lenders cut fees and increased flexibility to retain market share. The result has been an environment in which sponsors can have real optionality between channels based on execution speed, pricing and structural requirements. This competitive dynamic has been underpinned by abundant capital. Private credit fundraising remained robust, CLO formation stayed active and insurance capital continued flowing into the asset class.

The pressure to deliver exits has clearly intensified. Private equity holding periods have reached record highs, as managers waited for market conditions to improve. While dividend recaps, NAV loans and secondary market transactions provided some relief, institutional investors are demanding orthodox exits and capital distributions. The refinancing activity in 2025 has positioned portfolio companies to capitalise on an expected near-term increase in M&A and exit activity.

Europe's leveraged finance market entered 2026 not merely open for business but optimised for it. Lenders are well capitalised, competition is fierce and issuers have used the past 12 months to put themselves in a position of maximum preparedness. If the anticipated rebound in dealmaking materialises, the lending market is more than ready to support it.

European issuers optimise debt facilities as exit window opens

European leveraged finance markets steered through a volatile year to provide borrowers with a consistent source of liquidity at attractive prices

With M&A still intermittent, refinancing activity accounted for the bulk of issuance

Refinancing took on a broader strategic context, as issuers lay the groundwork for exit opportunities expected to emerge in 2026

Leveraged finance providers enter the new year well capitalised and ready to finance a new cycle of transaction flow

Sponsor focus: PE maximises optionality as M&A green shoots emerge

Insight

|

5 min read

Headlines

Demand for deal financing still trails supply

Competition between syndicated loan, high yield bond and private credit markets has intensified

Sponsors negotiate narrower margins, lower fees and greater flexibility

Private debt and syndicated loans increasingly viewed as interchangeable

European leveraged loan issuance for buyouts reached €29.3 billion in 2025—just trailing the €32.1 billion recorded in 2024, according to Debtwire.

In an improving but still challenged M&A market, private equity sponsors are taking advantage of increasingly flexible leveraged lending markets to negotiate lower borrowing costs and create bespoke deal structures.

European leveraged loan issuance for buyouts reached €29.3 billion in 2025—just trailing the €32.1 billion recorded in 2024, according to Debtwire.

Meanwhile, European private credit deployment for buyouts made year-on-year gains, with their total value rising to €84.9 billion through the first nine months of 2025, up 14 per cent compared to the same period in 2024, per Debtwire.

Intensifying competition as debt supply outstrips demand

Robust leveraged buyout (LBO) as well as private credit issuance tracked a noticeable increase in European buyout-backed M&A. The latter reached almost US$284.1 billion in 2025, up 13.7 per cent on the US$249.9 billion recorded the year prior, according to Mergermarket.

However, the rise in M&A activity has been intermittent. European deal markets enjoyed a positive start to 2025, before falling back in Q2 amid tariff and global trade uncertainty. Deal flow picked up again in Q3, which ultimately helped M&A to exceed 2024's levels. However, activity cooled off in Q4, and overall there has not been enough of an uplift to absorb the abundant liquidity in the system.

In the private credit space, direct lending fundraising climbed to €58 billion in the first nine months of 2025, handily exceeding the €42 billion total raised in 2024, according to Debtwire. European private credit assets under management now sit at approximately US$500 billion.

Capital flows into European BSL markets have been equally robust, with Debtwire recording €56.8 billion of new European CLO issuance in 2025, up 16.5 per cent on the €48.8 billion total logged in 2024. European high yield bond issuance has also remained active, providing sponsors with additional capital market access.

With these markets replete with capital and M&A volumes still patchy, options for deployment have been limited. In turn, competition between BSL markets and private credit has intensified—not only for new deal financing opportunities, but also in refinancing and repricing situations.

These dynamics drove convergence between BSLs, high yield bonds and private credit throughout 2025.

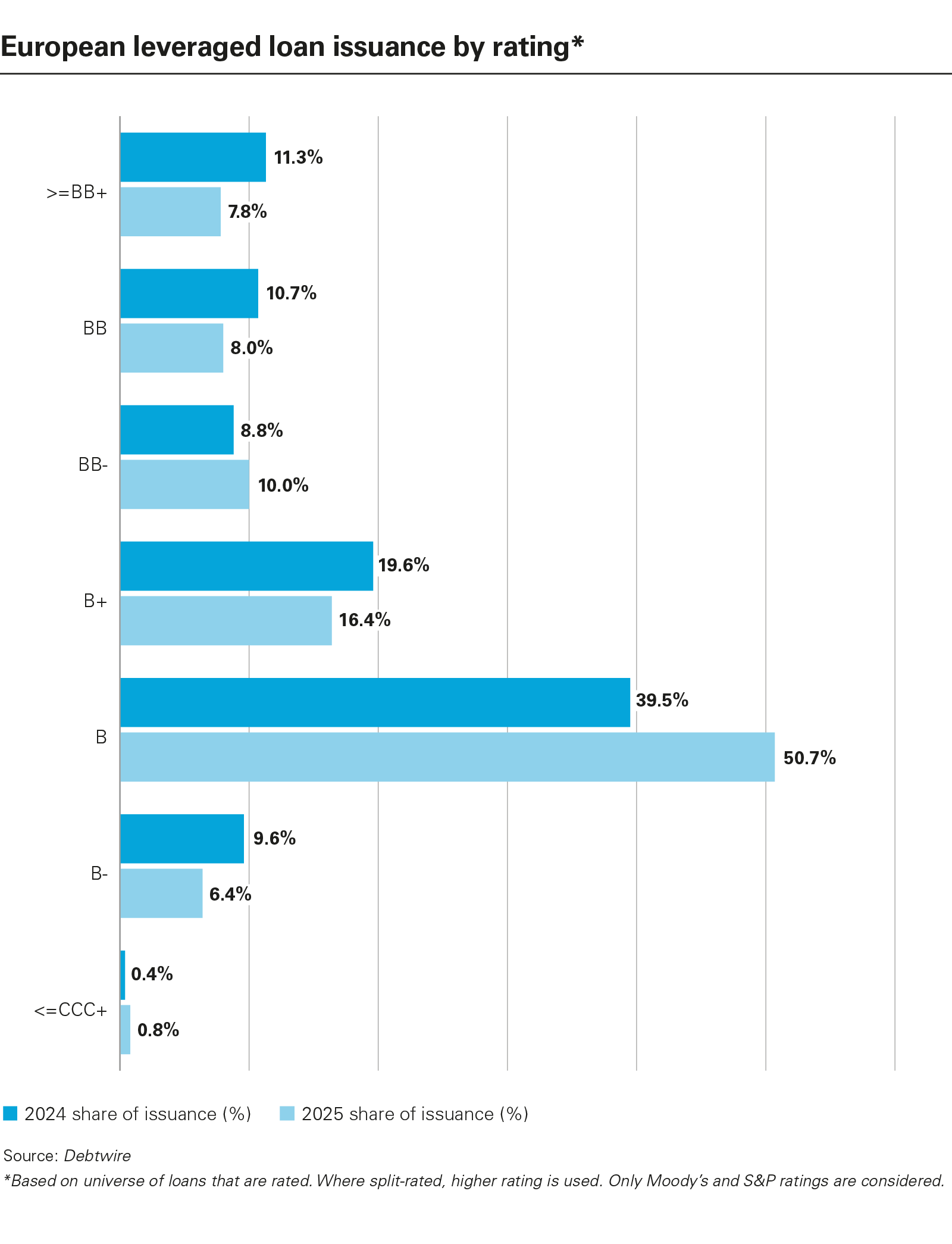

For example, private credit players compressed pricing to compete with BSL financing, with margins below 5 per cent increasingly frequent. Similarly, ratings agency Moody's notes that covenant-lite structures, once the preserve of BSL markets, are becoming more common in the private credit space. Private credit call-protection terms also softened to make the product more competitive, though these still usually feature longer call periods than BSL structures and apply more broadly than only to repricings.

Meanwhile, BSL markets trimmed fees, took on larger underwrites and lowered term loan margins to lure borrowers. Banks have even been able to offer BSL borrowers delayed-draw facilities (committed, unfunded term-loan facilities that offer borrowers the option of drawing down on a facility over an extended period of time), even though the institutional investors and CLOs that invest in BSL debt prefer committed facilities to be fully drawn upfront. Although delayed-draw facilities are rarer in Europe, US case studies highlight the flexibility that BSL markets can offer when needed.

The convergence of private credit and BSL lending has enabled buyout firms to structure creative financing packages and make full use of the increasing optionality available through both lending channels.

With BSL and private credit increasingly seen as interchangeable, sponsors have been able to switch between the two and select the options best suited to specific deals.

Private credit continues to offer speed, certainty of execution and bespoke structures. These include undrawn capital expenditure lines and PIK toggle flexibility, which is now offered as standard for most direct lending structures, even if sponsors do not necessarily require it. Meanwhile, BSL markets can absorb large underwrites and syndications at highly attractive prices.

It is now common for buyout firms, especially large-cap managers with in-house capital markets teams, to evaluate opportunities in both markets simultaneously. They then choose the option that provides the best balance between final pricing (including after any flex), deal execution, call protection and flexibility around structure.

Private credit funds are also increasingly participating in BSL structures themselves, offering elements that traditional lenders are more reticent to offer. These include, for example, delayed-draw facilities and term loan tranches in less common currencies. Though these may involve higher pricing, they enable sponsors to implement their preferred structure at an acceptable, blended cost.

This dynamic evolved over 2025. Sponsors preferred the execution certainty of private credit in Q2 amid tariff turmoil but swung back towards BSL debt later in the year to take advantage of highly attractive pricing.

Sponsors are also leveraging the convergence between private credit and BSLs to use debt structures in novel ways to amplify returns and unlock liquidity.

For example, following its successful IPO of security company Verisure in Stockholm, private equity firm Hellman & Friedman was able to unlock an additional €1 billion payout by putting a holdco payment-in-kind (PIK) structure in place as part of the deal. The structure utilised high yield bonds at the holdco level.

Holdco PIK structures have been a common feature of private credit markets for years but are not often seen in public deals. Employing the structure in a new setting has enabled sponsors to utilise more leverage without adding debt at the operating company level.

For sponsors leading IPOs, the holdco PIK structure allows them to release capital early, rather than having to endure lock-up periods before they can sell down remaining stakes in businesses once listed in order to access liquidity.

Serving sponsor priorities

The interplay between BSLs, high yield bonds and private credit will remain a key feature of deal financing in 2026, as both segments of the market compete to win business from sponsors.

Sponsor priorities have always been the same when it comes to financing structures: maximising leverage, low pricing, flexible structures and certainty of execution.

As the new year gets underway, Europe's leveraged finance ecosystem has seldom been better placed to meet these requirements.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: European leveraged loan issuance by rating* (PDF)

View full image: European leveraged loan issuance by rating* (PDF)